LB&I Virtual Library

Concept Unit

Library Level Number Title

Shelf N/A Crossover

Volume 18 Foreign Currency

Part 18.2 Transactions in a Foreign Currency – Sec. 988

Chapter 18.2.1 Computation of Exchange Gain/Loss - General

Subchapter N/A N/A

Document Control Number (DCN) FCU/C/18_2_1-05

Date of Last Update 12/20/16

Note: This document is not an official pronouncement of law, and cannot be used, cited or relied upon as such. Further, this document may not contain a

comprehensive discussion of all pertinent issues or law or the IRS's interpretation of current law.

Unit Name Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

Primary UIL Code 9470.02-01 Computation of exchange gain or loss - general

2

DRAFT

2

Table of Contents

(View this PowerPoint in “Presentation View” to click on the links below)

General Overview

Relevant Key Factors

Diagram of Concept

Facts of Concept

Detailed Explanation of the Concept

Examples of the Concept

Index of Referenced Resources

Training and Additional Resources

Glossary of Terms and Acronyms

Index of Related Practice Units

3

DRAFT

3

General Overview

Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

This Concept Unit addresses the following issues related to computing an exchange gain or loss on payables and receivables of a

taxpayer:

1. General Rule

2. Booking Date

3. Details

4. Receivables

5. Payables

6. Spot Rate

Except as provided in regulations, a U.S. taxpayer’s functional currency is the U.S. dollar (USD). A Qualified Business Unit (QBU -

any separate and clearly identified unit of a taxpayer that maintains separate books and records) may have a non USD functional

currency if (1) the economic environment in which a significant part of the QBU’s activities are conducted is not the USD and (2) the

QBU is not keeping its books and records in the USD. See IRC 985(b); Treas. Reg. 1.985-1(b) and (c); note that U.S. Corporations

must generally have the USD as their functional currency, although their foreign branches that are QBUs may have non USD

functional currencies. A QBU can have a functional currency that is different from its owner. The functional currency is relevant for

taxpayers or QBU’s that have transactions in multiple currencies. Transactions are generally to be accounted for in the taxpayer's or

QBU’s functional currency. Certain non-functional currency transactions, called “Section 988 transactions” give rise to functional

currency gain or loss.

Back to Table Of Contents

4

DRAFT

4

Transactions of U.S. corporations that require the use of a currency other then U.S. dollar have dramatically increased as more

taxpayers do business globally. Generally, when U.S. resident taxpayers invest and do business transactions in non US currency, all

federal tax determinations must be made in USD. Thus, Section 988 transactions, which are certain monetary transactions

denominated in (or determined by reference to the value of) a nonfunctional currency, may give rise to foreign exchange gains or

losses under Section 988.

General Overview cont’d

Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

IRC 988 includes accruing, or otherwise taking into account, any item of expense or gross income or receipts which is to be paid or

received after the date on which such items is accrued or take into account if the amount the taxpayer is entitled to receive or is

required to pay is denominated in terms of a nonfunctional currency or is determined by reference to the value of one or more

nonfunctional currencies (e.g. payables and receivables held by a taxpayer or QBU that is denominated in nonfunctional currency.)

Back to Table Of Contents

5

DRAFT

5

Relevant Key Factors

Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

Key Factors

IRC 985 to 989 provide rules for determining a taxpayer or QBU’s functional currency, determining taxpayer’s income in its functional

currency and measuring foreign currency gain and losses. In general:

IRC 985 - Defines functional currency including hyperinflationary currency

IRC 986 - Addresses the determination of foreign taxes and foreign corporation’s earning and profits

IRC 987 - Addresses Branch transactions when the branch has a different functional currency from its owner

IRC 988 - Describes treatment of certain foreign currency transactions

IRC 989 - Defines a qualified business unit (QBU) and other terms

This Concept Unit will focus on the computation of exchange gains or losses on payables and receivables held by a taxpayer or QBU

in a currency other than its functional currency. See other concept, transaction, and process units for IRC 989, IRC 987 and other

foreign currency issues.

Note: The Internal Revenue Code (IRC) refers to “foreign currency gains and losses” while the Treasury Regulations use the

term “exchange gain or loss”.

Back to Table Of Contents

6

DRAFT

6

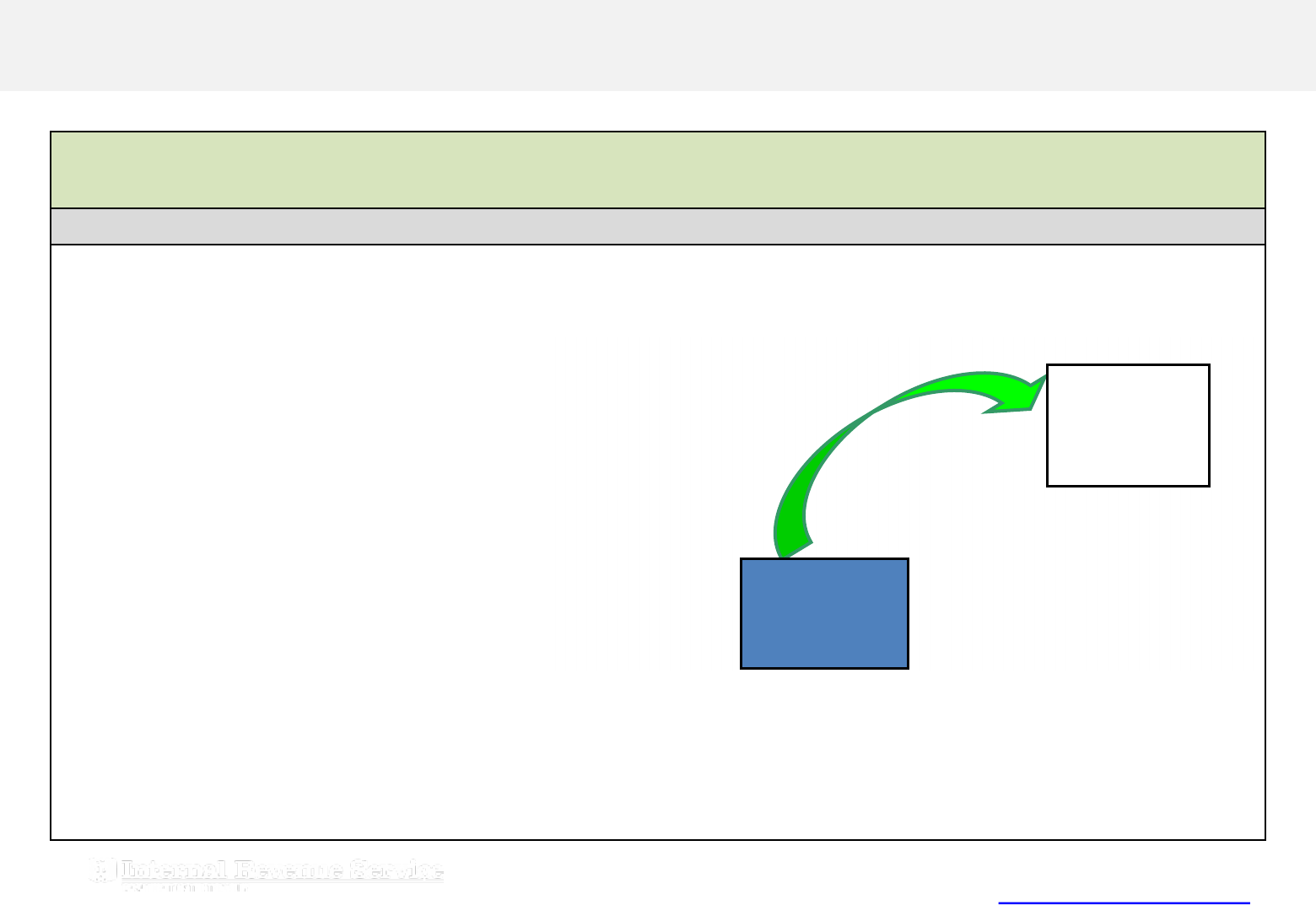

Diagram of Concept

Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

Diagram of Concept

Transaction #1: CFC1 provides

Service to USC resulting in an account

payable on USC books in Yen.

Both Transaction #1 and #2 will result in an exchange gain or loss under Section 988. In Transaction #1, USC will recognize an

exchange gain or loss on the account payable denominated in the Yen, a nonfunctional currency for USC. In Transaction #2, USC will

recognize an exchange gain or loss on the account receivable denominated in the Euro, a nonfunctional currency for USC. CFC1 and

CFC2 will not have Section 988 transactions since the transaction is denominated in each CFC’s respective functional currency.

Back to Table Of Contents

Transaction #2: USC sells product to

CFC2 on credit in the Euro resulting in an

account receivable on USC books in Euro.

USC

US$

CFC1

FC

Yen

CFC2

FC Euro

7

DRAFT

7

Facts of Concept

Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

Facts of Concept

It is very common for U.S. Companies to transact business in currencies other then the US dollar. An examiner needs to

understand:

– the cash flow of these transactions

– how they are recorded for financial accounting and tax purposes

– any foreign currency gain or loss that should be reported, as well as the source (US or foreign) and character (ordinary or capital)

of the transaction.

Non-functional currency transaction amounts have to be translated into functional currency. An example of this type of transaction is

paying an invoice in a non-functional currency.

When the US taxpayer owns, or has a position in, a non US currency asset or liability; an examiner should be able to measure,

translate and establish when foreign currency gains and losses should be determined. This unit will focus on the exchange gains

and losses recognized by a taxpayer or QBU on the receipt or payment of an invoice, recorded on the books of the taxpayer or QBU

as an accounts receivable or payable respectively, that is denominated in a nonfunctional currency.

Back to Table Of Contents

8

DRAFT

8

Detailed Explanation of the Concept

Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

The starting point to applying the foreign currency tax rules is to determine the Taxpayer’s or QBU’s “functional currency.” This is the

currency in which all of the taxpayer’s or QBU’s taxable income and earnings and profits must be computed. Transactions, income

and foreign taxes in any other currency then must be translated back into the taxpayer’s functional currency under the rules of IRC

986, 987, 988 or 989.

Analysis Resources

Foreign Currency Gains and Losses (a.k.a. Exchange Gains and Losses):

The taxpayer or QBU computes foreign currency gains or losses on certain transactions

identified in IRC 988(c)(1)(B) and (C). Included in the listing of these transactions is the

accrual of any item of expense or income receipts that is paid or received after the accrual

date that is denominated in a currency other than the taxpayer or QBU’s functional currency

as defined in IRC 988(c)(1)(B)(ii) and Treas. Reg. 1.988(a)(2)(ii).

The description and computation of

exchange gains and losses on other

types of transactions discussed in

IRC 988(c)(1)(B) are discussed in

other IPS units listed at the end of

this unit.

Recognition Date on Payables and Receivables:

The exchange gain or loss on the above identified transaction (accruals of items of expense

or income) is recognized on the date that the payment of nonfunctional currency is made or

received. Such gain or loss is recognized in accordance with the applicable recognition

provisions of the IRC. If a taxpayer’s or QBU’s right to receive income or pay an expense is

transferred or modified in a transaction in which gain or loss would otherwise be recognized,

exchange gain or loss is recognized only to the extent of total gain or loss on the

transaction.

See Treas. Reg. 1.988-2(c)(1).

Back to Table Of Contents

9

DRAFT

9

Detailed Explanation of the Concept

Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

The starting point to applying the foreign currency tax rules is to determine the Taxpayer’s or QBU’s “functional currency.” This is the

currency in which all of the taxpayer’s or QBU’s taxable income and earnings and profits must be computed. Transactions, income

and foreign taxes in any other currency then must be translated back into the taxpayer’s functional currency under the rules of IRC

986, 987, 988 or 989.

Analysis Resources

Source of Section 988 gain:

The source of foreign currency gain or loss is determined by reference to the residence of

the taxpayer or QBU of the taxpayer on whose books the underlying asset, liability, or item

of income or expense is properly reflected. Whether an asset, liability, or item of income or

expense is properly reflected on the books of a QBU is a question of fact.

For further discussion regarding the

identification and determination of a

taxpayer’s QBUs, please see IPS

Concept Unit “Definition of a QBU”.

See Treas. Reg. 1.988-4(a) and (b).

Computation of Exchange Gain/Loss on Item of Gross Income or Receipt (Accounts

Receivable):

The exchange gain loss on an item of gross income or receipt (recorded as an account

receivable) that is denominated in a nonfunctional currency is computed by subtracting the

nonfunctional currency accrued as an account receivable (multiplied by the spot rate at the

booking date) from the nonfunctional currency received as payment on the account

receivable (multiplied by the spot rate on the payment date).

See Treas. Reg. 1.988-2(c)(2).

Back to Table Of Contents

10

DRAFT

10

Detailed Explanation of the Concept

Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

Please see the analysis below for a listing of factors involved in the transactions, the determination and/or computation of the

transaction, and the relevant authority.

Analysis Resources

Computation of Exchange Gain/Loss on Item of Expense (Accounts Payable):

The exchange gain or loss on an item of expense (recorded as an accounts payable) that is

denominated in a nonfunctional currency is computed by subtracting the nonfunctional

currency paid on the account payable (multiplied by the spot rate at the payment date) from

the nonfunctional currency accrued as an account payable (multiplied by the spot rate on

the booking date).

NOTE: Payment of a payable might result in a separate Section 988 transaction for

disposition of nonfunctional currency.

See Treas. Reg. 1.988-2(c)(3).

Spot Rate Option: The Treasury Regulation allows a taxpayer or QBU to utilize a spot rate

convention to be determined at intervals of one quarter year or less (versus the spot rate at

the actual booking or payment dates) when computing exchange gains and losses on

nonfunctional currency accounts receivables and payables.

See Treas. Reg. 1.988-1(d)(3).

Recognition Date: The date that payment is made or received. Treas. Reg. 1.988-2(c)(1)

Exchange Gain or Loss on item of gross income or receipt (receipt of account receivable):

[(Nonfunctional currency received) x (spot rate on payment date)] – [(nonfunctional currency

accrued) x (spot rate on booking date)]

Treas. Reg. 1.988-2(c)(2)

Exchange Gain or Loss on item of expense (payment of account payable): [(Nonfunctional

currency accrued) x (spot rate on booking date)] – [(nonfunctional currency paid) x (spot rate

on payment date)]

Treas. Reg. 1.988-2(c)(3)

Back to Table Of Contents

11

DRAFT

11

Examples of the Concept

Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

Example – Exchange Gain/Loss on Payment of an Account Payable in Nonfunctional Currency

• USC is a calendar year corporation with the

USD as its functional currency.

• On 01/15/20x9, USC purchases inventory on

account from CFC1 for LC $10,000. The spot

rate on 01/15/20x9 is LC $1.00 = US $0.55.

• On 02/23/20x9, when USC makes payment of

the LC $10,000 payable, the spot rate is LC

$1.00 = US $0.50.

• On 02/23/20x9, USC will realize an exchange

gain on the LC $10,000 account payable.

USC’s gain is computed by multiplying the LC

$10,000 by the spot rate on the booking date

(LC $10,000 x 0.55 = US $5,500) and

subtracting from such amount, the amount

computed by multiplying the LC $10,000 by the

spot rate on the payment date (LC $10,000 x

0.50 = US $5,000).

• Thus, USC’s exchange gain on the transaction

is US $500 (US $5,500 – US $5,000). The

character of the exchange gain is ordinary.

NOTE: There could be an exchange gain or loss

on the disposition of LC by USC depending on

when USC acquires LC.

Back to Table Of Contents

CFC1

LC $

USC

US $

Inventory LC $10,000

12

DRAFT

12

Example - Exchange Gain/Loss on Receipt of an Accounts Receivable in Nonfunctional Currency

Examples of the Concept

Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

• USC is a calendar year corporation with the

USD as its functional currency.

• On 01/15/20x9, USC sells inventory to CFC2

for LC $10,000. The spot rate on 01/15/20x9 is

LC $1.00 = US $0.55.

• On 02/23/20x9, when USC receives payment,

of the LC $10,000, the spot rate is LC $1.00 =

US $0.50.

• On 02/23/20x9, USC will realize an exchange

loss. USC’s loss is computed by multiplying

the LC $10,000 by the spot rate on the date the

LC $10,000 are received (LC $10,000 x 0.50 =

US $5,000) and subtracting from such amount,

the amount computed by multiplying the LC

$10,000 by the spot rate on the booking date

(LC $10,000 x 0.55 = US $5,500).

• Thus, USC’s exchange loss on the transaction

is US $500 (US $5,000 – US $5,500). The

character of the exchange loss is ordinary.

• (Source: Treas. Reg. 1.988-2(c)(4), Example

1.)

Back to Table Of Contents

USC

US $

CFC2

LC $

I

nventory LC $10,000

13

DRAFT

13

Examples of the Concept

Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

Example – Spot Rate Convention Option (Monthly Basis)

• USC is a calendar year corporation with the

USD as its functional currency.

• USC uses a spot rate convention to determine

the spot rate as provided in Treas. Reg. 1.988-

1(d)(3)

• The spot rate determined under the spot rate

convention for the month of January is LC

$1.00 = US $ 0.54, and for the month of

February is LC $1.00 = US $ 0.51.

• On 01/15/20x9, USC sells inventory for LC

$10,000. On 02/23/20x9, USC receives

payment of the LC $10,000.

• On the last date in February, USC will realize

exchange loss. USC’s loss is computed by

multiplying the LC $10,000 by the spot rate

convention for the month of February (LC

$10,000 x US $0.51 = US $5,100) and

subtracting from such amount, the amount

computed by multiplying the LC $10,000 by the

spot rate convention for the month of January

(LC $10,000 x US $0.54 = US $5,400)

• USC’s exchange loss is $300 (US $5,100 – US

$ 5,400). (Source: Treas. Reg. 1.988-2(c)(4),

Example 2)

Back to Table Of Contents

USC

US $

Inventory LC $10,000

CFC2

LC $

14

Index of Referenced Resources

Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

Treas. Reg. 1.988-2(c)(1).

Treas. Reg. 1.988-4(a) and (b)

Treas. Reg. 1.988-2(c)(2)

Treas. Reg. 1.988-2(c)(3)

Treas. Reg. 1.988-1(d)(3)

Treas. Reg. 1.988-2(c)(4), Example 1

Treas. Reg. 1.988-2(c)(4), Example 2

Back to Table of Contents

15

DRAFT

15

Training and Additional Resources

Exchange Gains/Losses on Payables and Receivables Denominated in a Nonfunctional

Currency

Type of Resource Description(s)

SABA Sessions INTL Foreign Currency Issues and IFRS plus Audit Techniques

IBC ONLY – Foreign Currency & Int’l Matrix

IBC Common Errors in translating Foreign Currency

Building Blocks of Financial Products

IE Phase I, Module E – Lesson 1 Foreign Currency

IE Phase III, Module D –Interaction of International and Financial Products Issues

FP Phase I, Lesson 9 Foreign Currency

FP Phase III, Lesson 4 Foreign Currency

Refer to Foreign Currency PN SharePoint Site for a complete listing of Foreign Currency

Centra sessions

White Papers / Guidance FASB 52/ASC 830 Foreign Currency Matters

Reference Materials – Treaties Bittker & Lokken: Fundamentals of International Taxation, Chapter 74 (Foreign Currency)

BNA Tax Management Portfolio 921-2nd Tax Aspects of Foreign Currency

Keyes: Federal Taxation of Financial Instruments and Transactions (Chapter 15, Foreign

Currency Denominated Instruments

Back to Table of Contents

16

DRAFT

16

Glossary of Terms and Acronyms

Term/Acronym Definition

ASC Accounting Standards Codification

CFC Controlled Foreign Corporation

FASB Financial Accounting Standards Board

IFRS International Financial Reporting Standards

INTL International

IRC Internal Revenue Code

LC Local Currency (generic term for non-U.S. currency)

QBU Qualified Business Unit

USC U.S. Corporation

USD U.S. Dollar

Back to Table Of Contents

17

DRAFT

17

Index of Related Practice Units

Associated UIL(s) Related Practice Unit DCN

9470.02 How to Assess Penalties for Failure to file Form 8886 Disclosing

Section 988 Losses

FCU/P/18_02_01-04

9470.02 Overview of Foreign Currency Hedging Transactions FCU/C/18_02_03-05

9470.02 Integration of Executory Contract and the Currency Hedge FCU/T/18_02_03-03

9470.02 Legging into Integrated Treatment FCU/T/18_02_03-02

9470.02 Disposition of a Portion of an Integrated Hedge FCU/T/18_02_03-01

(Formerly FCU/9470.02_03)

9470.02 Disposition of Nonfunctional Currency FCU/T/18_02_01-08

9470.03 Functional Currency of a Qualified Business Unit (QBU) FCU/C/18_3_3_08

9412.05 Computing Foreign Base Company Income DPL/P/02_05_01_01-01

(Formerly DPL/9412.05_05)

9412.00 Subpart F Overview DPL/C/02-01

(Formerly DPL/CU/V_2_01)

9414.01 Calculation of IRC §956 Amount RPA/P/04_01_03-01

Back to Table Of Contents