Economic eects of

Airbnb in Australia

Airbnb Australia

2017

Glossary

ABS Australian Bureau of Statistics

DAE-RIO-M Deloitte Access Economics’ Regional Input-Output Model

DAE-TFM Deloitte Access Economics’ Tourism Forecasting Model

EBITDA Earnings before interest, tax, depreciation and amortisation

FTE Full time equivalent

GDP Gross domestic product

GOS Gross operating surplus

GSP Gross state product

IO Input output

IVS International Visitor Survey

NVS National Visitor Survey

TARDIS model Tourism Accommodation Regional Demand,

Investment and Supply model

TRA Tourism Research Australia

Economic eects of Airbnb in Australia

1

Contents

Executive summary 03

1. Introduction 10

1.1 Purpose and scope of report 11

1.2 What is Airbnb? 11

1.3 Other issues not in the scope of this report 12

2. Supporting government tourism objectives 13

2.1 The Australian industry context 14

2.2 Helping the federal government deliver tourism objectives 15

2.3 Helping state governments deliver tourism objectives 16

3. The contribution of Airbnb to tourism in Australia 17

3.1 Airbnb in Australia 18

3.2 Methodology 20

3.3 Contribution to the Australian economy 20

4. Consumer eects 23

4.1 Benets of Airbnb’s features 24

4.2 Cost savings for consumers 29

4.3 Sydney – a case study 30

4.4 Benets for business travellers 34

5. Producer eects 36

5.1 Benets for Airbnb hosts 37

5.2 Driving competition and growing the market 38

5.3 Supporting local economies 39

Appendix A: Helping state governments deliver tourism objectives 41

Appendix B: Economic contribution modelling framework 46

Appendix C: State-by-state breakdown of economic contribution 49

Appendix D: Consumer eects modelling framework 64

Footnotes 73

Authors 79

Limitation of our work 79

Economic eects of Airbnb in Australia

2

Economic eects of Airbnb in Australia

3

Executive summary

Key points

• Airbnb has grown in popularity in recent years as part of a broader trend towards

the ‘sharing economy’, where peer to peer platforms directly connect customers

and providers. Hosts across Australia accommodated around 2.1 million guests

for 3.7 million nights in 2015-16

• Airbnb guests are now a signicant driver of the tourism economy, with a total

contribution to Australia’s GDP of $1.6 billion in 2015-16, supporting over 14,000 jobs

in addition to the activities of hosts. An analysis of tourism policies across Australian

states and territories nds Airbnb can help contribute to a number of their objectives

• Platforms like Airbnb increase the supply of guest accommodation in volume and

variety terms, so they can both drive growth of the tourism industry and increase

competition. There may be costs and impacts for existing operators, but consumers

stand to gain

• One of the drivers of Airbnb growth has been creating lower cost accommodation

options – we estimate a cost saving of around $26 million in 2015-16 for guests

staying in Sydney who might otherwise have stayed in traditional accommodation

• One of the key non-price dierences of Airbnb is location – three-quarters of

Airbnb properties in major markets are located outside traditional tourist areas.

Other features include bringing people together from other states or countries,

home-like facilities in accommodation, and the features of the Airbnb app itself

such as the rating system. The non-price benets are estimated to be worth the

equivalent of almost $50 million in 2015-16 for guests staying in Sydney alone

• The average star rating for Airbnb listings across Australia is 4.7 out of 5

• Airbnb hosts in Australia earned a median income of $4,920 in 2015-16 – a fairly

modest supplement to a household’s main sources of income, but which may

nevertheless be handy for living expenses, to pay down debt or to increase savings.

Economic eects of Airbnb in Australia

4

In one year in Australia, 2.1 million Airbnb guests

spent $2 billion

supporting 14,000 jobs and $1.6 billion in GDP

Airbnb guests in Sydney saved $26 million

On average, guests across Australia rated their

Airbnb listing 4.7 stars out of 5

Economic eects of Airbnb in Australia

5

Airbnb is a peer to peer platform on which

people can list and book accommodation

around the world – whether that be a spare

bed, a private room or a whole house.

Short-stay rentals facilitated by platforms

like Airbnb are part of a broader trend: the

growth of the ‘sharing economy’, through

which consumers are choosing to share

assets and services via digital platforms.

Airbnb is distinct from traditional tourist

accommodation, in that Airbnb does not

own any of the property listed on its website

– it acts as a platform to connect hosts and

guests to book accommodation, publish

information about host properties, facilitate

payments and collect ratings from hosts

and guests.

This report examines the economic impacts

of Airbnb, estimating the contribution of

guest spending to the Australian economy,

the economic benets enjoyed by guests,

and the income earned by hosts. By adding

to both the volume and variety of guest

accommodation, we nd that there are a

number of benets for guests, hosts, and

the tourism industry.

The contribution of Airbnb

to tourism in Australia

Airbnb plays an important role in

supporting tourism in Australia, by

facilitating accommodation bookings

and advertising Australian destinations to

consumers around the world. In 2015-16,

over 800,000 stays were booked with

Airbnb in Australia. Hosts across the nation

accommodated around 2.1 million guests

for 3.7 million nights in places as diverse

as Collingwood to Coober Pedy. Airbnb has

grown rapidly in Australia since its launch

in 2012, with its innovative market oering

allowing ordinary people to host tourists

from around the world. According to Airbnb,

over 80 per cent of Airbnb hosts across

Australia share the homes in which

they live.

Our analysis is based on the tourism

expenditure of Airbnb’s guests in Australia.

Airbnb guests spent over $2 billion around

Australia in 2015-16, based on Airbnb

bookings and survey data from Airbnb

and Tourism Research Australia.

This includes the amount paid to Airbnb

hosts for accommodation, as well as

expenditure on items like food, drinks and

entertainment, but excluding fees charged

by Airbnb. The economic contribution

study is based on Input-Output (IO)

modelling techniques.

Our analysis found that the total economic

contribution is on average 1.6 times the

direct contribution.

The total economic contribution associated

with the tourism expenditure of Airbnb

guests in 2015-16 was $1.6 billion in value

added, with 14,409 full time equivalent

(FTE) jobs supported around Australia, in

addition to the activities of hosts. A state

-by-state breakdown is shown in the

table below.

While induced eects were not assessed

quantitatively in this report, these eects

may be locally signicant in some regions,

especially where tourism plays a signicant

role in the economy.

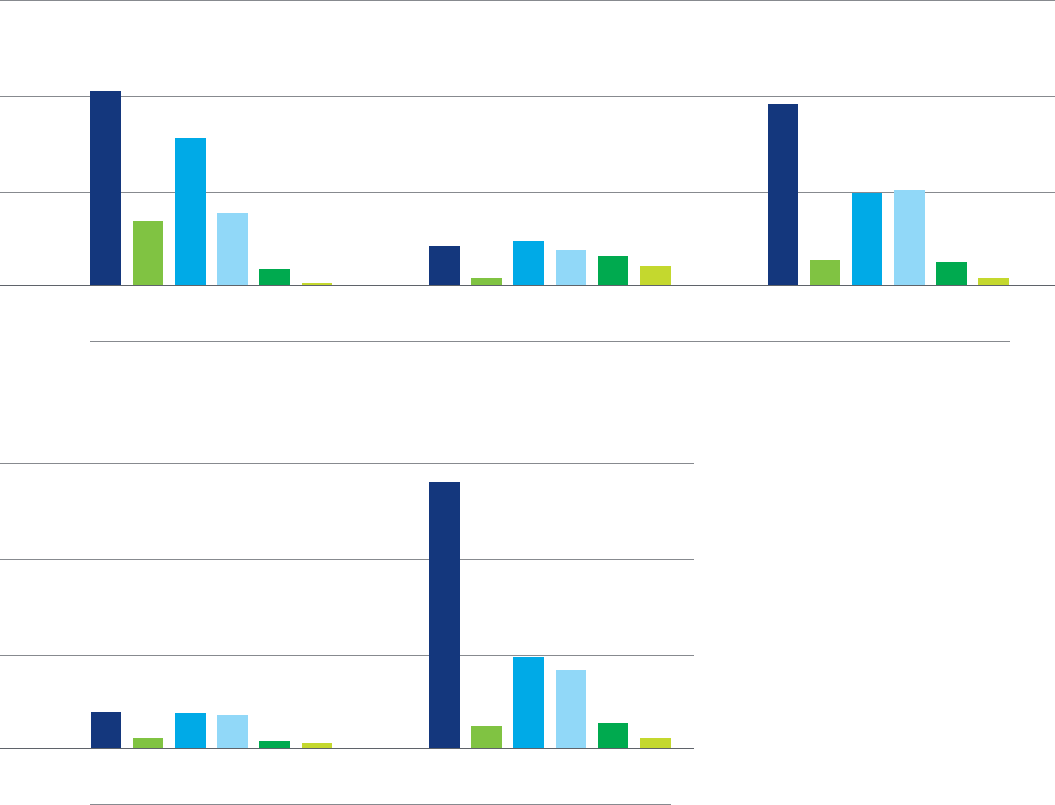

Table i: Economic contribution of tourism expenditure associated with Airbnb in Australian states and territories, 2015-16

Direct contribution

($m)

Indirect contribution

($m)

Total contribution

($m)

Total employment

(FTE)

New South Wales 376.8 135.7 512.5 4,452

Victoria 305.2 107.3 412.6 4,084

Western Australia 76.5 23.2 99.7 780

Queensland 160.5 56.8 217.4 2,115

Tasmania 42.1 12.5 54.5 599

South Australia 29.1 9.1 38.2 407

Northern Territory 5.1 1.3 6.5 55

Australian

Capital Territory

9.9 2.7 12.6 99

Interstate

indirect activity

– 252.8 252.8 1,818

Australia 1,005.3 601.6 1,606.9 14,409

Source: Deloitte Access Economics based on Airbnb, TRA and ABS data. These contributions do not include induced impacts,

which is the spending of those who receive additional income.

Economic eects of Airbnb in Australia

6

Total contribution

$1,606.9m

Total employment

14,409

Western Australia

Total contribution ($m)

99.7

Total employment (FTE)

780

Northern Territory

Total contribution ($m)

6.5

Total employment (FTE)

55

Queensland

Total contribution ($m)

217.4

Total employment (FTE)

2,115

New South Wales

Total contribution ($m)

512.5

Total employment (FTE)

4,452

ACT

Total contribution ($m)

12.6

Total employment (FTE)

99

Tasmania

Total contribution ($m)

54.5

Total employment (FTE)

599

Victoria

Total contribution ($m)

412.6

Total employment (FTE)

4,084

South Australia

Total contribution ($m)

38.2

Total employment (FTE)

407

Economic eects of Airbnb in Australia

7

Supporting government

tourism objectives

Airbnb is aligned to both federal and state

government objectives. The key federal

objective – Tourism 2020 – sets stretch

targets for Australia’s tourism industry.

Short-term private rental services like

Airbnb can assist the government in

meeting its accommodation supply and

tourism expenditure targets. At the state

level, Airbnb generally supports a number

of policy goals, including those related to

visitor expenditure, room supply, regional

dispersal and tourist experience.

Consumer eects

Guests who book accommodation through

Airbnb benet from its features and the

lower average cost of accommodation on

the platform. Airbnb’s innovative platform

allows guests to nd accommodation

outside major hotel districts and enjoy a

personal connection with their host and

the surrounding community. Airbnb’s

bidirectional ratings system also encourages

quality service, with listings across Australia

rated 4.7 stars on average. The features

(other than price) of Airbnb are further

described in Figure i.

Traditional accommodation providers

have also been part of digital innovation

trends in recent years, including greater

use of comparison websites that increase

competition, increased use of guest ratings

and easier ways to nd accommodation in

certain locations. Nevertheless, the features

in Figure i, along with competitive prices,

have seen Airbnb have a number of

eects in the market.

Figure i : Features of Airbnb

Location Bidirectional reviews

Peer to peer platformAvailability

Cultural experiences Business benets

The majority of Airbnb listings

are located outside traditional

hotel districts worldwide

Guests rate listings and host

rate guests following a stay,

encouraging better service

Airbnb expands

accommodation supply,

increasing availability during

peak periods

Airbnb facilities personal

connections between hosts

and guests

Consumers can enjoy

unique properties in dierent

locations, generating a cultural

experience

Business travellers can take

advantage of 'at home' facilities

and use Airbnb listings for team

sessions or retreats

Economic eects of Airbnb in Australia

8

Firstly, Airbnb facilitates people oering

their homes for short term accommodation,

which can occur at lower prices than

traditional tourist accommodation. These

cost savings, as well as the features of

Airbnb, encourage some consumers to book

Airbnb listings. The lower average prices

may also induce price-sensitive consumers

who could not otherwise have aorded to

travel – thus growing the size of the overall

short term accommodation market.

Secondly, Airbnb is adding to the overall

variety in the market– listings are available

in a variety of locations outside major

hotel districts, in diering congurations

(from apartments to treehouses) and are

provided through a peer to peer platform.

These dierences may create extra traveller

non-price benets known as ‘consumer

surplus’ – the dierence between what

consumers are willing to pay for Airbnb

accommodation, and what they actually

paid. Guests may be willing to pay more for

Airbnb accommodation due to the

features described.

Airbnb also has a platform for business

travellers – Airbnb for Business. Over

200,000 clients have registered and used

the Airbnb for Business platform worldwide.

In addition to the broader consumer

benets and cost savings for employers, the

ability to rent an entire space – such as a

whole apartment or house – is particularly

useful for businesses wishing to facilitate

a retreat or osite team session. It is also

benecial for business travellers on an

extended stay or preparing for relocation,

as the property is more similar to a home

than a hotel.

Sydney – a case study

To illustrate these two eects, Deloitte

Access Economics examined the Sydney

accommodation market as a case study. As

we have described throughout the report,

many of the features of Airbnb listings

and traditional hotels are considerably

dierent. Airbnb listings and hotel rooms

are not perfectly substitutable, however they

compete in the market for accommodation.

Airbnb listings also typically do not have

many of the services which are provided

by hotels and expected (and valued) by

guests, such as a permanent reception desk,

baggage storage or daily housekeeping.

Airbnb bookings data and traditional

accommodation bookings data from the

Australian Bureau of Statistics showed that

rooms in Airbnb listings are, on average,

$88 cheaper per night compared to

traditional accommodation in central

Sydney, while this dierence is $50 per

night outside central Sydney. This cost

dierential excludes Airbnb shared rooms

and private rooms within dwellings to

provide better comparability to hotels.

Using this price dierential and an analysis

of how Airbnb interacts with the traditional

accommodation market, we estimate that

Sydney guests saved $25.8 million in

2015-16.

Overall, we estimate that total consumer

surplus for Airbnb trips to Sydney was

$48.4 million in 2015-16. This is based

on the dierence between aggregate

willingness to pay (derived using elasticities)

and the total amount spent on Airbnb

accommodation in Sydney in 2015-16.

1

This value indicates how much extra

consumers are willing to pay for Airbnb

accommodation.

Producer eects

Platforms like Airbnb are adding to

accommodation supply and in doing so,

are generating competition in the market.

There may be costs and impacts for existing

operators in the accommodation market

due to this competition, particularly given

Airbnb’s rapid growth. However, Airbnb is

also growing the overall size of the market –

with consumers induced by Airbnb’s lower

average prices or its innovative features.

Despite the potential impacts on existing

operators, consumers stand to gain from

competition in the long term through

improved quality and reduced prices.

Airbnb hosts benet from additional

income. Airbnb hosts in Australia earned

a median income of $4,920 in 2015-16 – a

fairly modest supplement to a household’s

main sources of income. However it can be

used for living expenses, to pay down debt

or increase savings. This extra income can

also support hosts to explore new business

ventures – in 2013, 27 per cent of Sydney

Airbnb hosts surveyed were freelancers,

entrepreneurs or self-employed.

Airbnb hosts can also enjoy the cultural

exchange facilitated by Airbnb. Both the

host and guest can experience another

culture through Airbnb, whether that be

through a conversation, a meal or a guided

tour. This can be a learning opportunity

for hosts, and can help develop a greater

understanding of diversity, culture

and community.

Airbnb can activate local communities

by distributing visitors across cities. 74 per

cent of Airbnb properties in major markets

across the world are located outside the

traditional tourist districts – meaning

that both visitors and their spending

is dispersed rather than concentrated,

helping local businesses outside areas

which traditionally benet from tourism.

Public discussion surrounding the potential

neighbourhood and amenity impacts of

Airbnb continues, and it is acknowledged

appropriate regulation could help address

these concerns. Airbnb has previously

supported legislation to address potential

neighbourhood and amenity impacts,

such as the amendments to the Owners

Corporations Act 2006 (Vic). However, we

did not consider regulation in detail as part

of this analysis.

Economic eects of Airbnb in Australia

9

$88

$50

Australian Bureau of Statistics data showed

that rooms in Airbnb listings are, on average,

cheaper per night compared to traditional

accommodation in central Sydney,

while this dierence is

per night outside central Sydney

Sydney

guests saved

$25.8 m

in 2015-16

Economic eects of Airbnb in Australia

10

1. Introduction

“Our guests are always out and

about. Without kitchen facilities in

the room, they tend to go out for

meals, though we’ve had a few

pizza deliveries!“

Sharon,

host from Perth

Economic eects of Airbnb in Australia

11

1.1 Purpose and scope of report

Since its Australian launch in August 2012,

Airbnb has facilitated over 1.3 million short

stays in Australian cities. In excess of 150

million guests, including over 2.5 million

Australian guests, are currently on

the platform.

Airbnb engaged Deloitte Access Economics

to assess the economic eects of Airbnb

in Australia. This report aims to quantify

the economic contribution of Airbnb guest

spending to the Australian economy, and

evaluate the economic benets enjoyed

by guests, hosts and the wider community.

These eects are considered in the

remaining chapters of this report:

• The tourism industry in Australia

and support for government tourism

objectives, described in Chapter 2

• The economic contribution of tourism

facilitated by Airbnb, described in

Chapter 3

• Benets for guests, including business

travellers, described in Chapter 4

• Producer eects, described in Chapter 5.

Each of these chapters will also consider the

impacts in a qualitative fashion.

1.2 What is Airbnb?

Airbnb is a peer to peer platform on which

people can list and book accommodation

around the world. Established in San

Francisco in 2008, Airbnb today has

properties listed in over 65,000 cities and

towns, including around 800 Australian

cities, towns and suburbs. Airbnb has grown

rapidly following its Australian launch in

2012, with around 800,000 stays booked

in 2015-16 – out of 1.3 million stays

since 2012.

Unlike most tourist accommodation,

properties on Airbnb are listed by the

person in possession of the property. This

is in comparison to hotels and serviced

apartments – many of which are owned

and managed by large private companies.

Airbnb enables ordinary people to list their

spare rooms, homes and holiday houses

as available for short term stays. According

to Airbnb, over 80 per cent of Airbnb hosts

across Australia share the homes in which

they live.

Short-stay rentals facilitated by platforms

like Airbnb are part of the sharing economy,

through which consumers are choosing

to share assets and services via digital

platforms. While at its core, Airbnb lls

the same role as traditional short-stay

accommodation – providing a place to sleep

at night – the way in which it delivers this

service is dierent to existing operators.

This dierentiated service leads to a number

of benets for guests and hosts, as well as

positive eects for local communities.

Other platforms exist which provide a

similar service to Airbnb. For example, Stayz

– on which people can list whole homes and

apartments for short-term stays – has been

in operation since 2001. Some real estate

agents can also list and arrange short-term

leases of holiday homes and apartments.

1.2.1 Listing a property on Airbnb

A person who has a space that they would

like to list on Airbnb is required to register

as a host on Airbnb’s website to use the

platform. The registration process involves

signing up to the platform and completing

information about their property, including

a description of the space available and

uploading photos. The host also provides

personal details, and can add a government

identication to verify their account.

The person who lists the property is able to

set the cost of renting the accommodation,

with Airbnb receiving a small percentage

fee per booking. The host also decides the

availability of the property and booking

settings. Hosts on Airbnb have a range

of options, for example, whether instant

bookings are available, or whether stay

requests need to be conrmed by the host.

Hosts can also set minimum requirements

for guests, including veried identication,

prole picture or rating.

Hosts are protected through Airbnb’s host

guarantee, which will reimburse eligible

hosts for damages up to $1 million.

1.2.2 Booking a stay on Airbnb

Guests register through the Airbnb platform

in a similar manner to hosts. Guests can

also verify their account using government

identication, and link other online proles

to their Airbnb account.

Guests can book a stay via Airbnb’s website

or on its mobile application. Guests can

search for listings using dierent criteria,

such as by date, city, neighbourhood, price

or type of property. A sample listing is

shown in Figure 1.1 below.

Source: Airbnb

Figure 1.1: Airbnb listing

Economic eects of Airbnb in Australia

12

Depending on the host’s booking settings,

a listing may be available for instant booking

or the stay may need to be approved by

the host. The host will be able to see the

guest’s prole and any reviews written by

other hosts when accepting the reservation

request. Similarly, the guest will be able to

see other guests’ reviews of the listing.

When an instant booking is made or a

booking request is accepted, the guest’s

reservation is automatically conrmed.

Hosts and guests agree a check-in time

and how the keys to the property will be

exchanged. Hosts can also add a security

deposit to their listing before the reservation

is booked.

Guests are charged for the reservation by

Airbnb at the time the booking is conrmed.

Airbnb then remits payment to the host

24 hours after check-in. Guests are also

charged a guest service fee by Airbnb.

While staying at a property, Airbnb guests

are asked to follow house rules set by the

host. These may include requests not to

smoke, prohibitions against holding parties

or dealing with the misuse of common

areas. After the stay is completed, both the

guest and the host are invited to submit a

review on their experience within 14 days

of checkout and provide a star rating out

of ve about their experience.

1.2.3 Other Airbnb services

Airbnb recently expanded its oering to

include city tours and activities through

Airbnb Experiences. The platform features

local experts and guides who have joined

Airbnb to share their city and their passion

with travellers from around the world.

Guests can book these experiences through

Airbnb, with the sessions ranging from one-

day tours to week-long immersive classes

with accommodation included. Experiences

are broadly categorised into sports, nature,

social impacts, entertainment, food and the

arts, with examples including surng classes

in Los Angeles, true hunting in Florence

and samurai swordplay workshops in Tokyo.

The Airbnb website and mobile application

also features a separate section dedicated

to places and neighbourhoods. Local

hosts share their knowledge to develop

guides for travellers exploring dierent

neighbourhoods in each city – such as

Fitzroy in Melbourne, or Redfern in Sydney.

The guides can not only be used to explore

a city, but also to help choose which

neighbourhood best suits a guest’s

needs and interests.

1.3 Other issues not

in the scope of this report

It is acknowledged that there are some

community issues relating to Airbnb, such as

noise levels and strata issues. As this report

focuses on the economic benets of Airbnb,

it does not consider these topics in detail.

Airbnb listings are, in many cases, located in

suburban neighbourhoods – meaning that

there is potential for conicting views. For

example, Tourism Accommodation Australia

has noted in a submission to the Federal

Opposition that there are possible amenity

issues associated with short term letting,

such as anti-social behaviour, increases in

building wear and tear and degrading of

amenities and capital values.

2

Appropriate

regulation can help address these concerns

to ensure that individual players do not

negatively aect neighbours and amenity.

This report does not analyse in detail the

drivers of the cost dierential between

hotel accommodation and Airbnb listings.

The regulatory requirements for hotel

accommodation and Airbnb listings

are dierent. Airbnb has previously

supported legislation to address potential

neighbourhood and amenity impacts,

such as amendments to the Owners

Corporations Act 2006 (Vic). However, this

report does not analyse or compare the

regulatory arrangements for home sharing

or traditional accommodation.

Economic eects of Airbnb in Australia

13

2. Supporting government

tourism objectives

“Airbnb has given me the

condence to accept people for

who they are and in its own way,

it is teaching people to be more

accepting by welcoming dierent

cultures into one’s home.“

Spencer,

host from Redfern

“I already had friends of friends

staying in my spare room – so

why not go one step further?“

Jodie,

host and Airbnb entrepreneur

from Melbourne

Economic eects of Airbnb in Australia

14

Tourism is an important part of the

Australian economy, with both levels of

government setting objectives to achieve

industry potential. Airbnb can help

governments achieve these objectives

through the expansion of room supply and

greater average tourism expenditure.

2.1 The Australian industry context

This section outlines how tourism in

Australia is growing, and how the traditional

part of the market is also growing in both

occupancy and supply terms. Short-term

private rentals are growing and represent a

modest component of the overall sector.

2.1.1 Tourism in Australia

Tourism was estimated to contribute

$53 billion to Australian Gross Domestic

Product (GDP) in 2015-16, representing

3.2 per cent of national income.

3

Deloitte

Access Economics identied tourism as one

of the 'Fantastic Five' sectors driving the next

wave of Australian prosperity in its thought

leadership report, Building the Lucky Country

– Positioning for Prosperity? Catching the

next wave.

7.4 million international visitors aged

15 years and over visited Australia in the

year ending September 2016, increasing

by 11 per cent over the period

4

– the fastest

rate of growth since the mid-1990s. At

the same time, domestic overnight trips

increased by 5 per cent to 89.4 million

trips, with overnight spend reaching $59.8

billion.

5

Clearly, Australian tourism is bucking

domestic and international trends, with total

tourism expenditure growing more than

three times faster than the overall economy

in the past year.

Table 2.1: Tourism in Australia, year ending September 2016

Metric International Domestic

Overnight visitors (international)

/trips (domestic)

7.4 million 11% 89.4 million 5%

Number of nights 251 million 4% 330 million 4%

Overnight visitor expenditure $38.8 billion 11% $59.8 billion 5%

Source: Tourism Research Australia

6

Deloitte Access Economics forecasts

international visitor trips to grow by 6.3 per

cent per year and visitor nights by 6.2 per

cent per year on average over the next three

years. This places the aggregate number

of international visitors to Australia in 2019

at 9 million, and the total number of nights

at 310 million. In terms of domestic travel,

Deloitte Access Economics forecasts trips

to grow by 3.3 per cent and visitor nights to

grow by 3.2 per cent each year on average

over the next three years.

7

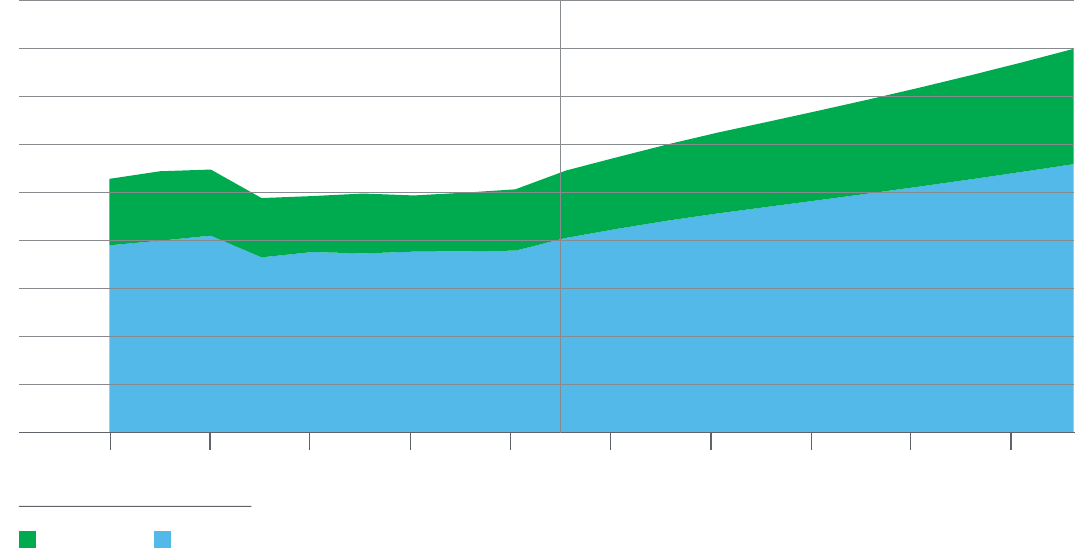

2.1.2 Traditional visitor accommodation:

growing strongly

Estimates of visitor nights and hotel supply

suggest that the most signicant part of

the market, the traditional hotel market

is growing strongly. Traditional visitor

accommodation is dened here to include

hotels, motels, guesthouses and serviced

apartments, consistent with the Australian

Bureau of Statistics (ABS) denition of tourist

accommodation.

8

The latest available data shows that

domestic tourists stayed 84.1 million nights

in traditional visitor accommodation in

2015-16, with international visitors staying

28.7 million nights.

9

Domestic visitor nights

in traditional accommodation are predicted

to reach 112.0 million by 2024-25, with

international visitor nights forecast to reach

48.1 million.

10

This represents a 10-year

average annual growth rate of 3.3 per cent

for domestic visitor nights and 5.5 per cent

for international visitor nights.

Economic eects of Airbnb in Australia

15

160

140

180

Nights (millions)

120

100

80

60

40

20

0

2005-06

Source: Tourism Research Australia

11

2007-08 2009-10 2011-12 2013-14 2015-16 2017-18 2019-20 2021-22 2023-24

Chart 2.1: International and domestic visitor nights in traditional visitor accommodation, 2005-06 to 2024-25

International Domestic

Room occupancy rates in tourist

accommodation establishments with

15 or more rooms rose by 1.3 percentage

points to 66.6 per cent in trend terms in

June 2016.

12

According to STR Global, room

occupancies in Australia were 75.7 per cent

in 2016 – a gure which includes all hotels,

regardless of establishment size.

This compares to 72.8 per cent in 2010.

13

Deloitte Access Economics expects hotel

supply in Australia will increase by 15,800

rooms over the period to December 2019.

Room nights sold are forecast to grow at 2.7

per cent per year, and room nights available

at 2.1 per cent per annum over the next

three years – representing a narrowing gap

between supply and demand compared to

previous forecasts.

14

2.1.3 Short-term private rentals

Aside from Airbnb, other platforms which

facilitate short-term private rentals include

Stayz, TripAdvisor, FlipKey and Couch

Surng. Some larger platforms do not

operate in Australia, including the Expedia-

owned HomeAway. However, Stayz was

acquired by HomeAway in 2013. Some real

estate companies also manage holiday

home rentals.

It is dicult to estimate the size of this

market, given many of the companies which

facilitate private rentals are privately owned.

Airbnb has an estimated market share

of less than 2.0 per cent.

15

Airbnb shares

some similarities with these online booking

sites, but features such as bidirectional

ratings, fully integrated payments and

the predominance of non-traditional

accommodation options combine to

create a dierent experience.

2.2 Helping the federal government

deliver tourism objectives

Tourism 2020 is the key federal government

objective relevant to Airbnb. Tourism 2020,

initially launched in 2010, set stretch targets

for Australia’s tourism industry. Relevantly,

it was identied in 2013 that between

6,000 and 20,000 new capital city rooms

(including the Gold Coast and Tropical North

Queensland) will be required to meet visitor

demand by 2020, assuming occupancy

rates of 80 per cent.

16

The most recent

data shows that occupancies in commercial

accommodation across Australia reached

75.7 per cent in 2016, according to

STR Global.

17

As at February 2017, the

accommodation sector had progressed 88

per cent towards the upper bound Tourism

2020 target of 20,000 capital city rooms, with

17,694 rooms added to accommodation

supply since the end of 2009.

18

Short-term

private rental services like Airbnb can assist

the government in meeting these targets.

Economic eects of Airbnb in Australia

16

Importantly, Airbnb properties are

distributed across capital cities and

regional areas, and between the CBD

and metropolitan areas. This may assist

in achieving another key area of strategic

focus in Tourism 2020: improving regional

dispersal.

19

Of the 74,400 listings booked in

2015-16 in Australia, 25,900 were outside

the greater capital city areas of Australian

states. This is particularly important, given

regional areas have experienced a decline

20

in accommodation supply in recent years.

Airbnb can also assist the government

in meeting another key objective of Tourism

2020 – increasing overnight spend to

$140 billion by 2020. As at February 2017,

tourism expenditure had tracked 38 per

cent towards the upper bound Tourism

2020 goal.

21

Airbnb survey data shows that

Airbnb guests spend more than the average

tourist, with Airbnb guests spending $237

per night on average, and general overnight

visitors spending $146 per night.

22

Higher

yielding visitors may assist the government

in meeting this upper bound target.

2.3 Helping state governments

deliver tourism objectives

Each state government around

Australia has tourism-related objectives

and strategies, many of which are aligned

with the national Tourism 2020 goal.

The service provided by Airbnb supports a

number of these strategies, and may assist

governments in achieving their objectives.

While the specic nature of objectives

obviously varies between jurisdictions,

some key themes emerge. The rst is in

line with Tourism 2020 – to increase room

supply. As noted earlier, Airbnb can assist

in increasing accommodation supply,

particularly during peak periods and major

events (where supply may be limited) and

in regional areas (which have experienced

a decline in supply in recent years

23

).

Additional supply in regional areas may

also support regional dispersal objectives,

such as those in Victoria, Tasmania and

South Australia.

Increasing tourism expenditure to meet

Tourism 2020 goals is also a common theme

across jurisdictions. Tourism expenditure

can increase through greater visitor volume

or through higher-yielding tourists. Airbnb

survey data from guests across Australia

indicates that Airbnb guests spend, on

average, 62 per cent more than the average

tourist. This additional expenditure may

assist governments in meeting Tourism

2020 objectives.

More broadly, a number of governments

focus on enhancing the visitor experience.

Airbnb’s peer to peer service can change

how visitors interact with a destination,

by creating a network of hosts who are

advocates for their local community and

state. The hosts consulted with as part of

this study each frequently recommended

local businesses and tailored experiences

to their guests, creating a sense of

community and facilitating an enjoyable

and authentic stay.

Each state government’s strategies are

evaluated separately in Appendix A.

Economic eects of Airbnb in Australia

17

3. The contribution

of Airbnb to tourism

in Australia

“I underestimated how many

customers would not be local

residents, and how many Airbnb

properties were located in such

close proximity to the store“

Katinka,

Tasmanian small business owner

“I enjoy giving good levels of

service, and spend time with my

guests to help them nd what

they are looking for in Byron Bay.

Having an extensive knowledge

of local cafes, restaurants and

entertainment, I am able to refer

guests to specic activities that

are more closely aligned to

their tastes“

Donald,

host from Byron Bay

Economic eects of Airbnb in Australia

18

Airbnb plays an important role in supporting tourism in Australia, by facilitating accommodation bookings and advertising Australian

destinations to consumers. This chapter details the value added to the Australian economy and the employment in Australia facilitated

by Airbnb through its platform to book accommodation.

3.1 Airbnb in Australia

In 2015-16, over 800,000 stays were booked with Airbnb around Australia. Hosts across the nation accommodated around 2.1 million

guests for 3.7 million nights in capital cities and regional towns. On average, each host had 15 bookings over the nancial year.

A breakdown of bookings in each jurisdiction is shown in Table 3.1.

According to 2015 survey data collected by Airbnb, around 71 per cent of Sydney trips, 66 per cent of Melbourne trips and 63 per cent of

Perth trips were for the primary purpose of vacation or leisure. A high proportion of trips were also booked to visit friends or relatives, with

15 per cent of Sydney trips and 22 per cent of Melbourne and Perth trips primarily booked for this purpose. The survey data is detailed in

Table 3.2.

Tourism facilitated by Airbnb contributes $1.6 billion in value added,

with 14,409 full time equivalent jobs supported around Australia

Table 3.1: Airbnb bookings, broken down by state or territory, 2015-16

State or Territory Total bookings Total guests Total nights booked

New South Wales 289,600 742,800 1,418,900

Victoria 235,900 651,600 1,134,300

Queensland 133,300 343,800 586,700

Western Australia 62,100 171,500 292,900

Tasmania 46,800 124,500 126,300

South Australia 24,400 64,100 109,000

Australian Capital Territory 9,200 20,000 47,30 0

Northern Territory 4,200 8,800 18,000

Total 805,500 2,127,100 3,733,300

Source: Airbnb

Economic eects of Airbnb in Australia

19

Around 51 per cent of Airbnb bookings in Australia between July 2015 and June 2016 were made by Australian guests. The remaining listings

were booked by international guests, with 4 per cent of guests each from the United States and United Kingdom, 3 per cent from Singapore

and 2 per cent from China and Germany.

Table 3.2: Primary purpose of visit survey results, 2015

Table 3.3: Guest origin for Airbnb trips in Australia, 2015-16

Purpose of visit Sydney Melbourne Perth Rest of Australia

Vacation/leisure 71% 66% 63% 77%

Visiting friends or relatives 15% 22% 22% 12%

Business 11% 6% 8% 7%

Conference/convention 0% 4% 2% 2%

Job search/interview 1% 0% 1% 0%

Study 1% 1% 1% 1%

Short-term

housing while relocating

1% 1% 3% 1%

Guest origin Guest arrivals Proportion of total

Australia 1,077,910 51%

United Kingdom 77,673 4%

United States 76,020 4%

Singapore 71,305 3%

China 46,952 2%

Germany 35,355 2%

Malaysia 27,582 1%

France 26,949 1%

New Zealand 23,969 1%

Canada 18,891 1%

Other countries 644,494 30%

Total 2,127,100 100%

Source: Airbnb

Source: Airbnb

Economic eects of Airbnb in Australia

20

3.2 Methodology

The economic contribution of trips

facilitated by Airbnb is a measure of the

direct activities of Airbnb guests, as well

as their indirect contributions through the

supply chain. Airbnb stays are a key part

of the tourism sector, with local, interstate

and international guests hosted

around Australia.

This analysis is based on stays facilitated

by Airbnb in Australia. The analysis does

not take into account the fact that, in

the absence of Airbnb, guests may have

still travelled and stayed in alternative

accommodation. In addition, this

analysis does not consider the economic

contribution associated with the Airbnb

platform itself. Airbnb prots, revenue

and expenditure activities are specically

excluded from the analysis.

The economic contribution analysis is based

on data provided by Airbnb on the number

of guests and their expenditure in 2015-16.

The analysis also draws on publicly available

expenditure data from Tourism Research

Australia (TRA) and the tourism satellite

accounts from the Australian Bureau of

Statistics (ABS).

The estimate of economic contribution is

driven by the expenditure of Airbnb’s guests.

In 2015-16, the average Airbnb guest spent

1.6 times more per day than the average

tourist in Australia. Expenditure data was

provided by Airbnb for guests staying in

Sydney, Melbourne and the Australian total,

with expenditure estimates for visitors to

the other capital cities and the states and

territories estimated from TRA data. This

is then weighted by the total number of

nights attributable to Airbnb customers in

each region, to estimate the total level of

expenditure in the region.

The pattern of guest expenditure highlights

the sectors of the economy that benet

(in revenue and employment terms) from

Airbnb’s guests, including food service

(restaurants, cafes, bars, etc.), shopping,

transportation, leisure and groceries

being the key categories of expenditure.

Value added is the most appropriate

measure of the economic contribution to

gross state product (GSP). It is the sum

of the returns to the primary factors of

production – labour and capital (i.e. wages

to workers and prot to shareholders) –

and can be calculated by adding the

gross operating surplus and wages paid

to workers in the tourism sector.

The estimates of the direct and indirect

economic contribution are based on

Input-Output (IO) modelling techniques.

The Australian Bureau of Statistics (ABS)

produces IO tables which provide the value

added for each sector of the Australian

economy, as well as the linkages between

sectors. This allows the expenditure by

Airbnb guests to be traced through the

economy, to estimate the value added at

each stage. Deloitte Access Economics’

Regional Input-Output Model (DAE-RIO-M)

is used to estimate the direct value add and

employment for each region. The indirect

value add and employment, generated by

expenditure on the intermediate inputs is

determined based on the cost structure

of each industry.

While we have not assessed the value of

induced eects quantitatively, in addition

to the direct and indirect economic

contribution, in some regions tourism

expenditure associated with Airbnb would

likely result in additional consumption

beyond expenditure on intermediate

inputs. In areas where tourism is especially

important to local industry, these eects

could be locally signicant.

Appendix B provides further

background on the economic

contribution modelling framework.

3.3 Contribution to the

Australian economy

The total economic contribution associated

with the tourism expenditure of Airbnb

guests in 2015-16 was $1.6 billion in value

added, with 14,409 full time equivalent

(FTE) jobs supported around Australia.

The total tourism expenditure of Airbnb

guests in Australia in 2015-16 is estimated

to be $2.041 billion. This gure includes

spending on items such as food, shopping

and entertainment, as well as the amount

paid to Airbnb hosts for accommodation.

Table 3.4 shows a breakdown of Airbnb

guest expenditure. As the amount spent

varies by jurisdiction, these gures

are based on state-by-state

expenditure estimates.

Economic eects of Airbnb in Australia

21

Table 3.4: Tourism expenditure of Airbnb guests in Australia, 2015-16

Category Total expenditure ($m) Share of expenditure

Accommodation $441.6 22%

Food service (e.g. restaurants) $554.1 27%

Groceries $185.6 9%

Shopping $353.8 17%

Other leisure (e.g. entertainment) $245.8 12%

Transportation $216.7 11%

Other services $43.7 2%

Total $2,041.3 100%

Source: Deloitte Access Economics estimates for categories based on Airbnb and TRA

24

survey and other data

It is necessary to consider how the

expenditure ows through the economy

to estimate the economic contribution

associated with Airbnb guest spending.

The amount spent directly by Airbnb guests

at local businesses represents revenue for

those businesses. Each business employs

workers and capital to provide goods or

services to the Airbnb guest. The returns

to labour (employee wages) and returns on

capital (business owner’s prots) associated

with the Airbnb guests’ spending comprise

the direct economic contribution.

However, some of the revenue earned

by those businesses is spent sourcing

intermediate inputs and paying other

expenses to run the business. For example,

a restaurant might source ingredients from

a market, and pay for gas, electricity and

water. This expenditure generates ow-on

economic activity, as supplying businesses

will also employ workers and capital to

produce goods and services. This additional

economic activity comprises the indirect

economic contribution.

Guests also pay hosts to stay in their

Airbnb accommodation. This revenue

represents income for hosts, with the

prots (or gross operating surplus) from this

exchange comprising the direct economic

contribution.

25

The indirect contribution

reects the purchase of intermediate

inputs by hosts to be able to provide Airbnb

accommodation. This principally includes

intermediate inputs provided by the

construction and nance sector required

to build and pay for the property. It also

includes other intermediate inputs used to

provide Airbnb accommodation (such as

cleaning services).

The total economic contribution is the

sum of the direct and indirect economic

contribution. The direct and indirect

contribution are calculated by considering

the value added to the Australian

economy arising from Airbnb guests’

visitor expenditure.

Our analysis has found that the total

economic contribution is on average

1.6 times the direct contribution.

Visitor expenditure of Airbnb guests is

estimated to directly contribute $1 billion

in value added to the Australian economy,

with a further indirect contribution of $602

million in value added. Tourism expenditure

of Airbnb guests also supported 14,409 FTE

jobs around Australia (see Table 3.5).

“Airbnb is good for the

local community. We’ve

been able to direct our

guests towards local

events in our area, which

they wouldn’t have known

about otherwise. One

family from Ecuador

enjoyed our local

community fete!”

Jess and Ashe,

hosts from Canberra

Economic eects of Airbnb in Australia

22

Table 3.5: Economic contribution of tourism expenditure associated with Airbnb in Australia, 2015-16

Table 3.6: Economic contribution of tourism expenditure associated with Airbnb in Australian states and territories, 2015-16

Direct contribution Indirect contribution Total contribution

Expenditure ($m) $2,041.3

Value added ($m) $1,005.3 $601.6 $1,606.9

• Labour income ($m) $449.2 $307.3 $756.5

• Gross operating surplus ($m) $556.1 $294.3 $850.4

Employment (FTE) 10,025 4,384 14,409

Direct contribution

($m)

Indirect contribution

($m)

Total contribution

($m)

Total employment

(FTE)

New South Wales 376.8 135.7 512.5 4,452

Victoria 305.2 107.3 412.6 4,084

Western Australia 76.5 23.2 99.7 780

Queensland 160.5 56.8 217.4 2,115

Tasmania 42.1 12.5 54.5 599

South Australia 29.1 9.1 38.2 407

Northern Territory 5.1 1.3 6.5 55

Australian Capital Territory 9.9 2.7 12.6 99

Interstate indirect activity 252.8 252.8 1,818

Australia 1,005.3 601.6 1,606.9 14,409

Source: Deloitte Access Economics based on Airbnb, TRA

26

and ABS

27

data

Note: Expenditure is calculated in the input-output model using basic prices, which reect the revenue received by producers of goods

and services. The spending on accommodation is based on the amount of revenue received by hosts (i.e. it excludes Airbnb charges).

These contributions do not include induced impacts, which is the spending of those who receive additional income.

Source: Deloitte Access Economics based on Airbnb, TRA

28

and ABS

29

data

Note: Expenditure is calculated in the input-output model using basic prices, which reect the revenue received by producers of goods

and services. The spending on accommodation is based on the amount of revenue received by hosts (i.e. it excludes Airbnb charges).

These contributions do not include induced impacts, which is the spending of those who receive additional income.

Table 3.6 provides a breakdown of the economic contribution by state or territory. This highlights that the two largest contributions to

value add are in New South Wales and Victoria, which together account for 58 per cent of total value add and 59 per cent of employment.

This reects the higher number of listings in these cities, their higher tourism visitation, and may also reect the relative cost of

accommodation in these states compared to the other states and territories.

The table also reects that in calculating the economic contribution of tourism expenditure state by state, some indirect activity is excluded

as it leaks out of that jurisdiction’s economy as imports. However, this interstate activity is accounted for in the national totals.

A state-by-state breakdown of the economic contribution, including capital city and regional gures, is contained in Appendix C.

Economic eects of Airbnb in Australia

23

4. Consumer eects

“Airbnb is a great way to

meet people and make friends.

I keep in touch with some guests

through Facebook, especially

those who stay in the main

house. I form real connections

with people – it’s only sad you

often don’t see them again!”

Melissa,

host from Darwin

“Airbnb is good for the local

community. We’ve been able to

direct our guests towards local

events in our area, which they

wouldn’t have known about

otherwise. One family from

Ecuador enjoyed our local

community fete!”

Jess and Ashe,

hosts from Canberra

Economic eects of Airbnb in Australia

24

Source: Deloitte Access Economics

Guests choose to use Airbnb for a range of reasons – sometimes price,

but often for a dierent type of service. The value of these non-price

benets, measured by consumer surplus, is twice the value of cost

savings enjoyed by Airbnb guests in Sydney.

Airbnb provides a number of benets

to guests who book stays on the

platform. These benets arise due to

the dierentiated service provided by

Airbnb and the lower average cost of

accommodation on the platform.

This chapter outlines the dierentiation

benets associated with the Airbnb

platform and accommodation booked

through Airbnb, as well as additional

benets for business travellers using

the Airbnb for Business platform.

It also describes the economic model used

to quantify these consumer eects and

cost savings, using Sydney as a case study.

4.1 Beyond lower prices:

benets of Airbnb’s features

While cost may be a factor in motivating

travellers to use Airbnb,

30

it’s not the only

reason. A number of studies have suggested

that collaborative consumption is driven

by the perceived value and benets of

these transactions.

31

These benets are related to the specic

product oered by Airbnb to consumers in

the market, and the extent to which it diers

from the current traditional oering. These

features of Airbnb are summarised in the

diagram below.

Figure 4.1: Features of Airbnb

Location Bidirectional reviews

Peer to peer platformAvailability

Cultural experiences Business benets

The majority of Airbnb listings

are located outside traditional

hotel districts worldwide

Guests rate listings and host

rate guests following a stay,

encouraging better service

Airbnb expands

accommodation supply,

increasing availability during

peak periods.

Airbnb facilities personal

connections between hosts

and guests

Consumers can enjoy

unique properties in dierent

locations, generating a cultural

experience.

Business travellers can take

advantage of 'at home' facilities

and use Airbnb listings for team

sessions or retreats

Economic eects of Airbnb in Australia

25

These features create additional consumer

surplus for travellers using Airbnb. In this

context, consumer surplus is dened as the

dierence between what consumers are

willing to pay for Airbnb accommodation,

and what they actually paid – in other

words, the value individuals receive from

their Airbnb over and above what they

paid for it. The dierentiation benets

described in the diagram may inuence

the amount consumers are willing to pay

for accommodation, and therefore the

amount of consumer surplus they receive.

The following sections describe the

benets of Airbnb’s features qualitatively,

while a case study in Section 4.3 quanties

consumer surplus for people using Airbnb

in Sydney.

4.1.2 Location and availability

of Airbnb properties

The vast majority of properties listed on

Airbnb are located outside the traditional

hotel areas of major cities around the

world.

32

This is in contrast to the location of

traditional tourist accommodation, which is

generally centred on the CBD and the

inner suburbs.

The varied location of Airbnb properties

leads to two key benets.

Firstly, it allows consumers to book

accommodation close to their desired

location. In providing greater choice, Airbnb

is more likely to facilitate a booking which

meets the needs of guests. For example,

guests may choose to stay outside the CBD

if visiting a suburban business, hospital

or university.

Sharon – using the vacant part of the house

When Sharon and her family moved into their Perth home two years ago, they soon

realised that the lower level of their house wasn’t being used, and decided to list the

private room on Airbnb after renovating the space.

Sharon’s home is located between Perth’s city centre and Fremantle, making it

convenient for travellers who want easy access to Perth’s sights via car. Sharon

estimates that around one third of her guests are tourists from Asia, a third are

interstate business travellers, and the remainder are from rural and regional parts

of Western Australia – often receiving medical treatment at the nearby Fiona Stanley

Hospital. Her home is also close to Garden City Shopping Centre, the Swan River and

public transport.

“Our guests are always out and about. Without kitchen facilities in the room, they tend

to go out for meals, though we’ve had a few pizza deliveries!”

The income earned from Airbnb is supplementary to Sharon’s primary income, though

it is particularly welcome while Sharon is on maternity leave. The earnings generally

go towards luxuries, including employing a cleaner for the home. As Sharon has a

professional background in luxury accommodation, she particularly enjoys that aspect

of hosting on Airbnb.

Sharon’s guests tend to be independent travellers, but she always greets them in

person on arrival. A handy guide in the room provides local recommendations to eat

and sightsee, though guests are always welcome to contact Sharon for her

local expertise.

Secondly, visitors are able to explore areas

‘o the beaten track’ by staying in an area

outside the location of traditional tourist

accommodation. Guests can stay in the

suburban areas of a city, generating a

living experience more similar to a local

resident.

33

Guests may place value on this

dierentiated and authentic experience.

34

The other key benet of Airbnb is its

facilitation of expanded accommodation

supply. While this point will be discussed

further in the following sections, the

greater availability of Airbnb properties in a

wider area means that it may be easier, on

the whole, for a guest to book a short-term

stay in a city. This can be particularly so

during periods of peak demand, such as

special events or long weekends.

Economic eects of Airbnb in Australia

26

Meeting the demand for rooms during Mardi Gras

The Sydney Gay and Lesbian Mardi Gras is an annual event which has its origins in

a night of political protest in 1978. Today, it is a two-week festival which celebrates

diversity and queer pride. In 2016, over 12,500 members of the queer community and

their supporters joined the key event, the Mardi Gras parade, on 178 oats. Around

300,000 people attended the parade as spectators.

Airbnb supported the Mardi Gras as a major partner in 2015 and 2016, and entered

a corporate oat in the Mardi Gras parade in both years. In 2016, Airbnb’s house-

oat was oered as a prize in a competition. Pink Media Group arranges Mardi Gras’

sponsorships and partnerships on their behalf.

Mardi Gras is not only the biggest queer celebration in Australia, but is also Sydney’s

second most-attended event, following only New Year’s Eve. In this context, Pink

Media reports that accommodation can be expensive and dicult to come by, with

hotels and other lodgings frequently selling out. The availability of Airbnb properties

may mean that more interstate and international visitors can attend the event, with

around 100,000 attendees coming from the rest of Australia and around 50,000 from

overseas. Visitors tend to stay around a week for the event, and according to Pink

Media, many continue to travel around Australia.

Airbnb oers an alternative place to stay for Mardi Gras participants, and at a range of

price points to suit dierent budgets. Importantly, many Airbnb listings are located in

Surry Hills, Darlinghurst and Newtown – neighbourhoods which are not only nearby to

Mardi Gras events, but according to Pink Media Group, also have a high proportion of

queer residents in their communities. Given there is limited hotel availability in these

suburbs, Airbnb facilitates an enhanced experience for Mardi Gras attendees. Hosts

are also able to benet from the interaction, particularly those who are attending

the event.

4.1.3 Cultural experiences

Consumer preferences for

accommodation vary signicantly.

Preferences may be inuenced by personal

tastes, purpose of travel, travel party size

or a range of other factors. Travellers may

look for a number of key attributes when

booking accommodation – such as location,

the number of beds or rooms, free Wi-Fi or

kitchen facilities.

Airbnb’s platform allows for the listing of

a wide variety of property types in varying

locations. This means that travellers are

more likely to nd a listing which meets all

of their wants and needs, especially when

outside the realm of traditional tourism

accommodation. The location of a listing

is important to guests who are seeking

a particular cultural experience when

travelling – such as terrace house in Surry

Hills, or a cottage in Fitzroy.

35

Airbnb also provides certain unique listings

that are unavailable in the traditional

tourist accommodation market. Airbnb’s

listings include treehouses, castles and

caves; this may suit tourists seeking a more

unique experience. Airbnb hosts may be

able to facilitate a wider range of requests

which are often disallowed in traditional

tourist accommodation, such as travelling

with pets.

Airbnb properties can also provide

additional ‘at-home’ facilities, such as a

laundry and kitchen, or a separate study.

These facilities provide additional benets

to travellers, especially in the context of

long-term stays.

Economic eects of Airbnb in Australia

27

Donald – personalising the Byron Bay experience

After having an excellent experience as an Airbnb guest, Donald decided to give

hosting a go, and listed his Byron Bay studio on Airbnb. With tourism being the largest

industry in Byron Bay, Donald has had no shortage of guest requests, and the Airbnb

platform allows him to manage his hosting.

“By varying the price and my style of advertising, I can control the level and type of

occupancy to suit my needs. This allows me to attract the guests I want at the time

I want.”

Having the exibility to attract certain types of guests allows Donald to provide his

guests with highly personalised service.

“I enjoy giving good levels of service, and spend time with my guests to help them nd

what they are looking for in Byron Bay. Having an extensive knowledge of local cafes,

restaurants and entertainment, I am able to refer guests to specic activities that are

more closely aligned to their tastes.”

This has resulted in over 100 positive reviews from guests enjoying Donald’s

recommendations. This, in turn, has led to more guest requests from both locally

and abroad.

Donald’s recommendations have positively impacted local businesses. For example, by

taking the time to understand what sort of food his guests are looking for, Donald can

provide them with local knowledge of where to nd quality meals.

“Tourists will spend more if they are recommended places that they like. I can refer my

guests to specic restaurants where they are more likely to get exactly what they want,

and this leads them to spend more locally, generating incremental business for

the region.”

4.1.4 Bidirectional reviews

Airbnb employs a bidirectional review

system, whereby guests and hosts

are invited to rate their counterpart

following the conclusion of a reservation.

Importantly, each party is unaware of

their own rating before submitting their

response, reducing the prospect of

potential retaliation bias.

36

Ratings can encourage the provision of

better service, as ratings are publicly

available on the platform. Reputation can

also aect listing prices according to one

US study.

37

Guests are able to view reviews

when searching for accommodation, and

may take this into account when choosing

a property. Hosts are also able to see a

guest’s rating when a guest requests a

reservation at their property, and may

similarly choose whether to approve the

stay based on ratings. Hosts can also set a

minimum ratings requirement for guests

where instant booking of their property is

available. TripAdvisor performs a similar

role in the traditional accommodation

market, although accommodation

providers cannot rate guests. Out of all

Airbnb reservations in Australia between

July 2015 and August 2016, listings were

rated 4.7 stars on average.

Table 4.1: Average ratings for Airbnb listings

Jurisdiction Rating

Western Australia 4.65

Victoria 4.68

Australian Capital Territory 4.65

South Australia 4.69

New South Wales 4.66

Northern Territory 4.63

Queensland 4.7

Tasmania 4.69

Australia 4.67

Source: Airbnb

Economic eects of Airbnb in Australia

28

Lyn – hosting festivalgoers in Adelaide

Lyn and her husband live in a two-storey townhouse in the south-west corner of

the Adelaide CBD. Given they only occupy the rst oor in their home, Lyn decided to

list the ground oor on Airbnb during Adelaide’s festival season. Two years later, the

bookings continue to ow through and supplement Lyn’s part-time work as a teacher.

Airbnb has given Lyn the opportunity to do something she always wanted – to work

in the tourism industry – and share her passion for Adelaide and South Australia.

Lyn’s home is conveniently located next to some of Adelaide’s best small

bars and restaurants, as well as near tourist attractions like the Central Market.

Lyn recommends local restaurants, bars and attractions based on what guests

are interested in, both within Adelaide and across South Australia’s wine regions.

“My guests are able to experience real life, not tourist life, by using Airbnb.”

Some guests are quite independent, while others seek Lyn’s assistance in building an

itinerary and exploring Adelaide. Many use Adelaide as a base to visit South Australia’s

wine regions, or as a stopover before or after a trip on the Great Ocean Road, the

Ghan or to Kangaroo Island.

“Recently, we had a retiree travelling around the world stay with us for just over a

week. She chose Airbnb because she didn’t want to be by herself each night – she

wanted to share her day and her experiences with someone else.”

The income Lyn and her husband earn from Airbnb funds their own overseas travel.

Recently they have visited the United States and Japan, with a trip planned for Italy in

the near future. Going forward, the income will also support Lyn and her husband in

their retirement.

Ratings also support the development of

the online Airbnb community. In allowing

guests to review the space in which they

stayed, rapport is generated between the

host and the guest and between others

on the platform. While this community is

an integral feature of Airbnb, one study

has noted that social interactions between

hosts and guests can introduce positive

bias in reviews. Omitting negative feedback

from reviews is said to occur due to the

empathy generated in social interactions

between hosts and guests. One study

estimated this eect by assuming that

social interactions are more likely to occur

where a guest is staying in a private room

of a private residence, and less likely to

occur where a host has more than three

listings. Fradkin et al found that trips to

private rooms have a 0.005 star higher

rating and trips to hosts with multiple

listings have a 0.112 lower rating, holding

guest characteristics xed.

38

Notably,

however, this bias is minimal.

4.1.5 Peer to peer platform

The peer to peer nature of Airbnb may

provide additional benets to guests. In

many cases, hosts will greet guests on

arrival, and assist their guests in settling in

to the accommodation and the local area.

This additional service may be valued by

guests, as they are able to connect with

a local resident in the area.

39

Airbnb also

facilitates hosts to write guides for guests,

which are available on the Airbnb platform

(as shown in Figure 4.2).

Economic eects of Airbnb in Australia

29

Figure 4.2: Host guidebook on

Airbnb mobile application

Some guests may also derive value from

the peer-to-peer connection facilitated

by the platform, with this experience

oering value beyond the provision of the

good or service purchased. Peer to peer

networks like Airbnb allow participants to

form friendships and develop and maintain

social connections.

40

Guests and hosts can

also share recommendations and personal

experiences, allowing tourists to connect

with the local community.

41

Source: Airbnb

Jess and Ashe - community connections in suburban Canberra

Ashe and Jess signed up to Airbnb after hearing about a friend’s experience listing his

home while on holiday. Jess and Ashe’s home is located in Weston Creek, around 20

minutes’ drive to central Canberra. Their Airbnb listing is a self-contained studio at

the rear of the property, with side access and separate kitchen facilities. A number of

people have stayed at the property while looking for more permanent accommodation

in the area, including people from overseas and interstate. The self-contained nature

of the studio particularly appeals to people looking for an extended stay.

“We initially thought people may only want to stay in the inner city – but were

surprised at how many travellers also came here for the surrounding Canberra

attractions, which are within easy reach from Weston Creek”

Ashe and Jess have enjoyed meeting their guests and hearing their stories. Although

the separate studio gives guests privacy, Ashe and Jess are always happy to have a

drink with guests or share local recommendations on request. They have also been

able to facilitate conversations with friends and colleagues for business travellers.

Importantly, Ashe and Jess see Airbnb as contributing to their local economy – by

linking tourists to local businesses and events.

“Airbnb is good for the local community. We’ve been able to direct our guests towards

local events in our area, which they wouldn’t have known about otherwise. One family

from Ecuador enjoyed our local community fete!”

4.2 Cost savings for consumers

The additional room supply facilitated

by Airbnb increases competition in the

market, while also providing dierent

types of accommodation for consumers.

Increased competition and additional

supply in the market can have a number

of eects, including lower prices for

consumers and greater availability during

peak periods.

This report does not analyse in detail the

drivers of the cost dierential between

hotel accommodation and Airbnb listings.

It is likely there are a number of factors.

There is a relatively low marginal cost in

letting an empty room in a property or an

apartment that would have been empty

while the owner was on an

extended holiday.

Airbnb listings also typically do not

have many of the services which are

provided by hotels and expected (and

valued) by guests, such as a permanent

reception desk, baggage storage or daily

housekeeping. Finally, the regulatory

requirements for hotel accommodation

and Airbnb listings are dierent. This

report does not analyse or compare the

regulatory arrangements for home

sharing or traditional accommodation.

Lower accommodation prices can

have a number of eects. Clearly, for

those who are incentivised to switch

from using traditional accommodation to

Airbnb, there are resulting cost savings.

The magnitude of these savings depends

on the dierential between Airbnb prices

and hotel prices.

Economic eects of Airbnb in Australia

30

Importantly, the lower average price of

Airbnb listings may encourage people

to travel who could otherwise not have

aorded hotel prices, or encourage more

frequent travel. These new entrants to

the accommodation market increase the

overall size of the market, and can help

boost tourism more broadly. In one study,

67 per cent of respondents agreed that

peer to peer accommodation expands

their selection of places to travel, with the

lower accommodation cost making more

destinations aordable. 41 per cent of

respondents also agreed that peer to peer

accommodation increases the frequency of

their travel, mainly due to the social aspects

of using peer to peer accommodation.

42

In a survey undertaken across the United

States, United Kingdom, Germany and

France, respondents indicated that price

was the most important factor in choosing

Airbnb. The survey, conducted by Morgan

Stanley and AlphaWise in 2016, also

showed that 2 per cent of trips would

not have been taken if not for Airbnb.

43

There are also benets for those who

continue to use traditional accommodation.

In the longer term, hotels may reduce

their prices in order to compete with

Airbnb listings – leading to cost savings

for this segment of the market. Whether

this occurs depends on the extent to

which hotels compete with Airbnb listings.

However, the location of Airbnb listings

in Australia – primarily outside the major

hotel districts – may bring into question

the extent to which Airbnb and the hotel

industry directly compete.

It is important to note that Airbnb listings

are not always less expensive than hotels.

As shown by CBRE analysis in the United

States,

44

the average daily rate for Airbnb

may exceed that of hotels, depending on

the type of listing. But the overall eect of

Airbnb is to drive competition – with lower