Research and Information Service

Briefing Paper

Providing research and information services to the Northern Ireland Assembly 1

Paper 03/24 1 March 2024 NIAR 123-23

Northern Ireland

economic overview

Finance and Economics Team, Research and Information Service

This Briefing Paper has been prepared for the incoming Committee for the

Economy, to provide an overview of the Northern Ireland economy as of early

March 2024. Drawing on the most recent available data, it looks at areas in

which Northern Ireland’s economy is performing well and highlights some

challenges facing it.

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 2

Key Points

Positives

Economic growth

Northern Ireland’s economy has grown 38% in real terms since the

Belfast/Good Friday Agreement was signed in 1998. During the same period,

the economies of the United Kingdom, Scotland, and Wales grew by 41%, 38%,

and 40%, respectively.

Labour market

Northern Ireland’s labour market has recovered well since the COVID-19

pandemic. Total employment (employees plus the self-employed) has almost

recovered to its pre-pandemic level. There are currently 840,000 people aged

16-64 in employment.

Furthermore, the unemployment rate is currently very low – 2.6% in the period

of October – December 2023.

Trade

Northern Ireland has been performing well in terms of its overall trade balance

(the balance of exports relative to imports). As of 2022, exports of goods and

services were at a record high of £13.3 billion (bn) – with a trade surplus of £3.5

bn.

Challenges

Inflation

Inflation remained stubbornly high over the past year and a half, peaking at

11.2% in October 2022. However, headline inflation has been on a downward

trend since then, and as of January 2024, was just 4%.

Core inflation (which excludes energy, food, alcohol and tobacco) has remained

more stubbornly high. It fell to 5.1% in January 2024 – down only slightly from

5.2% in both November and December 2023.

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 3

Economic inactivity

High economic inactivity has been a significant, long-term issue for Northern

Ireland. The headline rate has been much higher than the United Kingdom

average for decades, and has remained stubbornly high. As of December 2023,

the headline rate in Northern Ireland was 26.8% relative to 20.8% in the United

Kingdom. In relative terms, Northern Ireland is similar to the United Kingdom

average for most of these – but performs significantly worse in terms of

economic inactivity due to long-term sick or disabled.

Productivity

Northern Ireland’s productivity gap when compared to the United Kingdom

average is another long-running economic issue. Key productivity metrics for

Northern Ireland have been persistently and consistently below the United

Kingdom average over the past two decades.

Labour Supply

A potential challenge faced by the Northern Ireland economy is weak labour

supply growth. This is a combination of low growth in working age population

and net migration.

Inclusion

Inclusion (in terms of how economic growth and opportunities are distributed

across society) are below acceptable levels in a number of metrics in Northern

Ireland. For example, employment rates for disabled people in Northern Ireland

are much lower than those for non-disabled people; and are far below the

United Kingdom average. Employment rates for the most deprived areas in

Northern Ireland are also significantly lower than those in the least deprived

areas, and the Northern Ireland average.

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 4

Introduction

This Briefing Paper has been prepared for the incoming Committee for the

Economy (CfE) (the Committee), to provide an overview of the Northern Ireland

economy as of March 2024. Drawing on the most recent available data,

1

it looks

at areas in which Northern Ireland’s economy is performing well and highlights

some challenges facing it. In particular, it addresses employment,

unemployment, trade balance and ongoing economic challenges, such as

Northern Ireland’s productivity gap, economic inactivity, inflation and inclusion.

The Paper is presented as follows:

• Section 1 – Context-setting;

• Section 2 – Positives – areas in which the Northern Ireland economy is

performing well;

• Section 3 – Challenges – key challenges facing Northern Ireland’s

decision makers; and,

• Section 4 – Key takeaways.

The Paper is not intended to address the specific circumstances of any

particular individual. It should not be relied upon as professional legal advice or

as a substitute for it.

1

All data referenced in this paper was current as of 1 March 2024.

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 5

1 Context setting

Prior to outlining Northern Ireland’s current economic outlook, this section

provides context in terms of key findings arising from the outgoing Committee

for the Economy’s micro inquiry on Northern Ireland’s economic context (sub-

section 1.1) and existing Department for the Economy (DfE) policies (sub-

section 1.2).

1.1 Micro Inquiry – Economic Outlook

In autumn 2020, the former Committee undertook an Economic Outlook Micro

Inquiry; aiming to engage with key stakeholders, seek their views and thereafter

develop a themes-based report providing evidence on how the economy has

been impacted as a result of the COVID-19 pandemic and ideas on how to

rebuild it better.

In November 2020, the Committee held a discussion event with a wide range of

stakeholders including Chambers of Commerce, business and industry

representatives and economists.

Thereafter, it published a summation of the key themes arising from the micro

inquiry, which stakeholders had felt were necessary to rebuild and boost the

economy, including: technology and digital infrastructure; skills and

employment; transport infrastructure; and, energy for businesses and

consumers.

1.2 Relevant DfE policies

There are a number of policies, strategies and action plans currently published

by DfE that are relevant to the areas discussed in sections 2 and 3 of this

Paper. These include the 10X Economy, and its associated delivery plan – a

strategy which focuses on innovation and productivity growth; and building on

Northern Irelands economic strengths.

In particular, DfE’s Skills Strategy for Northern Ireland (Skills for a 10X

economy) sets a strategic framework for the development of Northern Ireland’s

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 6

skills system to 2030 – with a view to supporting the successful delivery of the

10X Economy.

The Trade and investment for a 10X Economy publication outlines the strategic

priorities and high level ambitions that will shape DfE’s approach to trade and

investment; and DfE’s Energy Strategy, Path to Net Zero Energy sets out a

pathway for energy to 2030 that will “mobilise the skills, technologies and

behaviours needed to take us towards our vision of net zero carbon and

affordable energy by 2050”.

2 Positives

Drawing on the most recent available data, this section looks at areas in which

Northern Ireland’s economy is performing well:

2.1 Economic growth;

2.2 Labour market; and,

2.3 Trade.

2.1 Economic growth

Northern Ireland’s Gross Domestic Product (GDP) (a measure of the value of

the goods and services produced in a country or region – which estimates the

size and growth of the economy) has grown 38% in real terms since the

Belfast/Good Friday Agreement was signed in 1998. During the same period,

the economies of the United Kingdom, Scotland, and Wales grew by 41%, 38%,

and 40%, respectively, as highlighted in Figure 1 below:

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 7

Figure 1: GDP growth, Northern Ireland & United Kingdom, 1998-2021,

(2019 prices)

Source: ONS, April 2023

2.2 Labour market

This sub-section briefly outlines the performance of Northern Ireland’s labour

market in two key metrics: employment; and, unemployment.

2.2.1 Employment

Northern Ireland’s labour market has recovered well since the COVID-19

pandemic. As Figure 2 below shows, total employment (of those aged 16-64)

has almost recovered to its pre-pandemic level:

138.1

141.1

60

70

80

90

100

110

120

130

140

150

160

NI UK

1998=100

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 8

Figure 2: Total employment (age 16-64), Northern Ireland, Jan 2019 – Dec

2023

Source: NISRA, February 2024

However, this aggregate performance conceals a wide variation in the

composition of employment in Northern Ireland.

Total employment (of those aged 16+)

2

is slightly below its pre-pandemic level

(in the period of December 2019-February 2020). This is because a large

increase in the number of employees has been more than offset by a fall in the

number of self-employed people during the same time period. The “other”

category includes those on government training schemes and unpaid family

workers. This is shown in Figure 3 below:

2

Statistics on the composition of employment (employees, self-employed, and “other”) are available

only for those aged 16+; whereas headline figures for employment and employment rates are

typically stated in terms of those aged 16-64.

Pre-pandemic

846k

Current

840k

740

760

780

800

820

840

860

Nov-Jan 19

Jan-Mar 19

Mar-May 19

May-Jul 19

Jul-Sep 19

Sep-Nov 19

Nov-Jan 20

Jan-Mar 20

Mar-May 20

May-Jul 20

Jul-Sep 20

Sep-Nov 20

Nov-Jan 21

Jan-Mar 21

Mar-May 21

May-Jul 21

Jul-Sep 21

Sep-Nov 21

Nov-Jan 22

Jan-Mar 22

Mar-May 22

May-Jul 22

Jul-Sep 22

Sep-Nov 22

Nov-Jan 23

Jan-Mar 23

Mar-May 23

May-Jul 23

Jul-Sep 23

Sep-Nov 23

Total employment (000s)

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 9

Figure 3: Drivers of employment change (age 16+), Feb 2020 – Dec 2023

Source: NISRA, February 2024

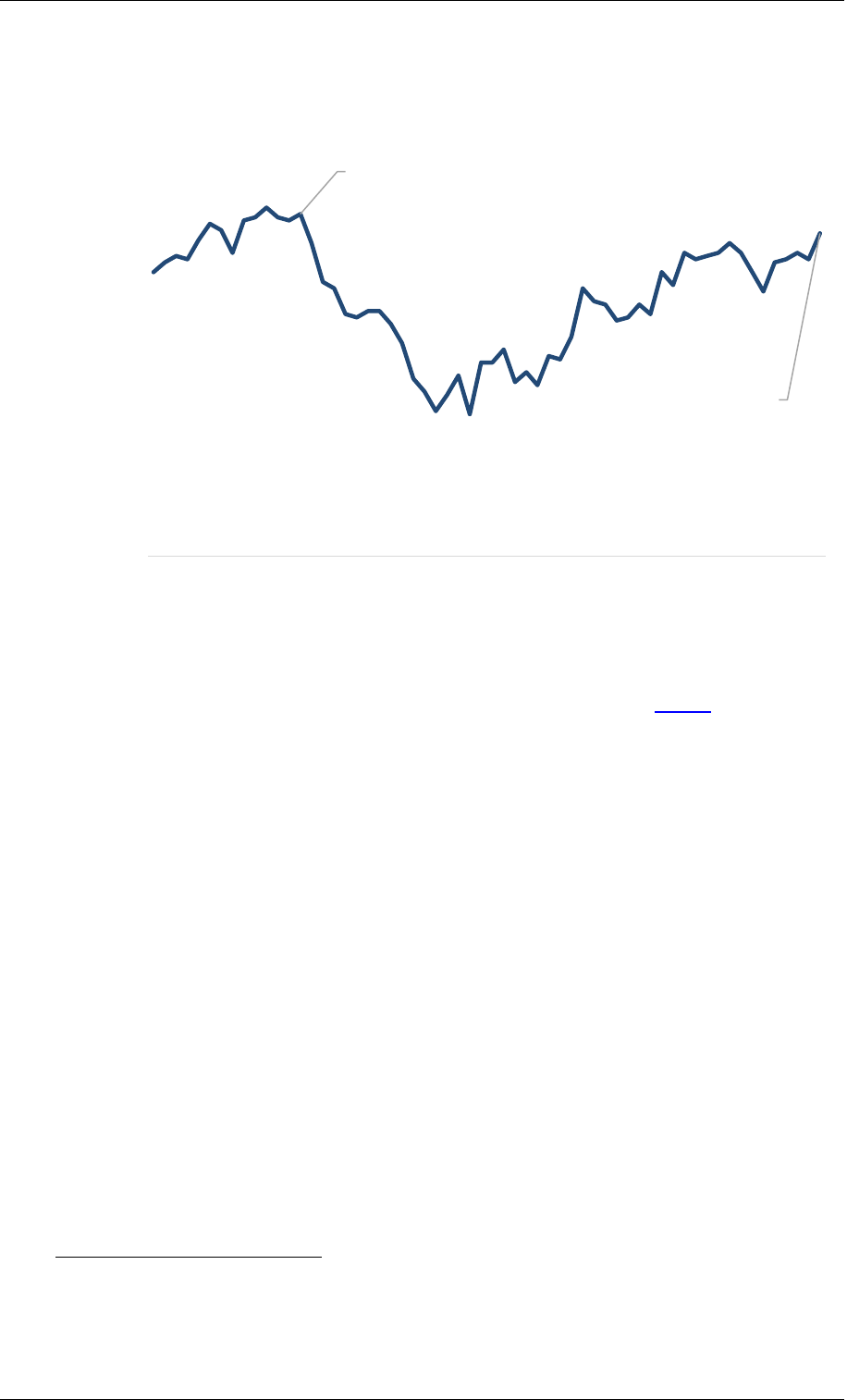

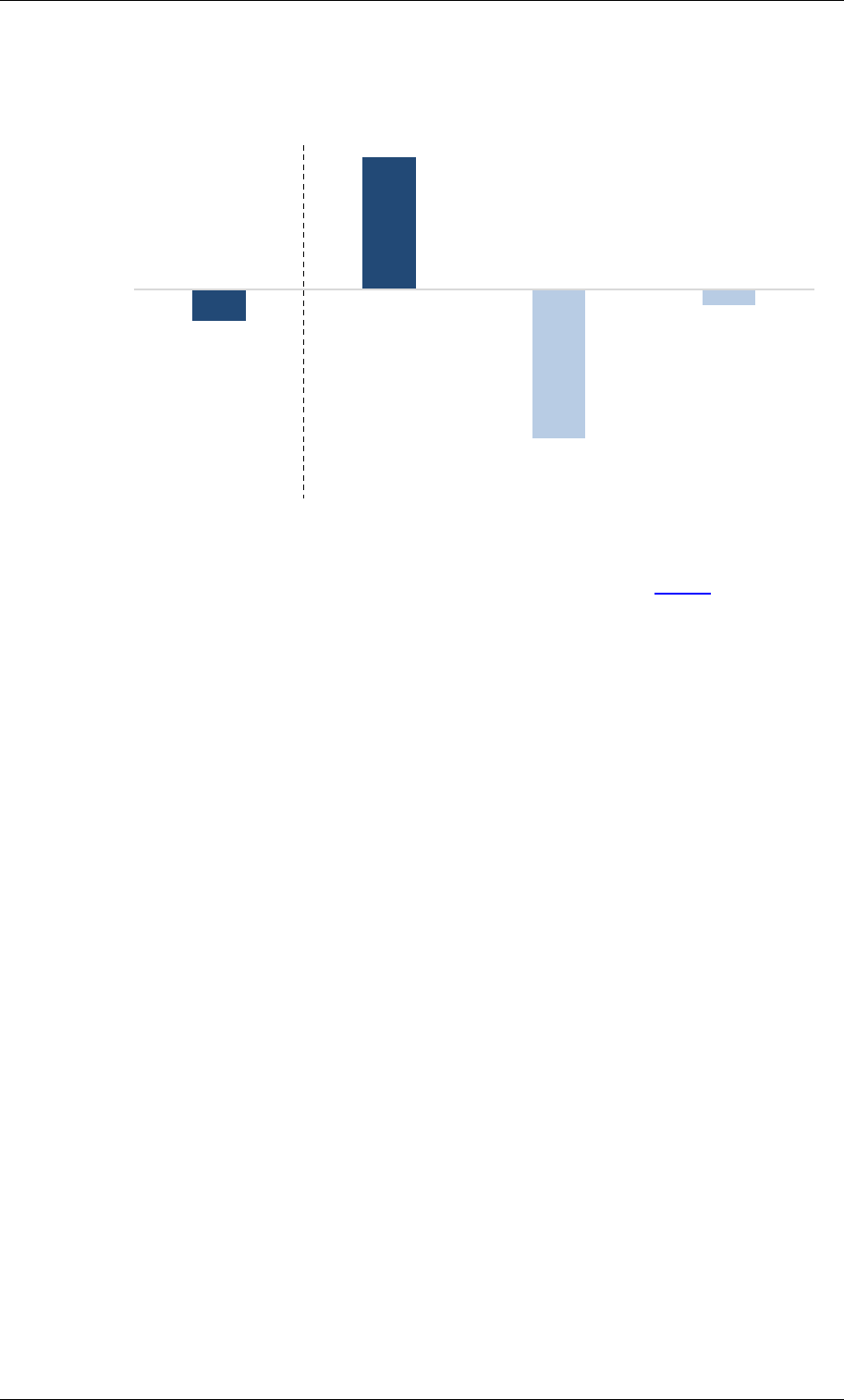

2.2.2 Unemployment

In addition to high employment levels, the unemployment rate in Northern

Ireland is now at a near-historic low. The rate in the period of October-

December 2023 was just 2.6% – below the United Kingdom average of 4.2% –

as shown in Figure 4 below. Whilst this is a positive in the economic narrative, it

also reflects the fact that there are large numbers of people in Northern Ireland

classified as economically inactive. Therefore, whilst they do not count as

unemployed, they are outside the labour market altogether (see subsection

3.2):

-6,000

+25,000

-28,000

-3,000

-40,000

-30,000

-20,000

-10,000

0

10,000

20,000

30,000

Employment Employees Self Employed Other

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 10

Figure 4: Unemployment rate (age 16+), Northern Ireland and UK, Jan 2010

– Dec 2023

Source: ONS, NISRA, February 2024

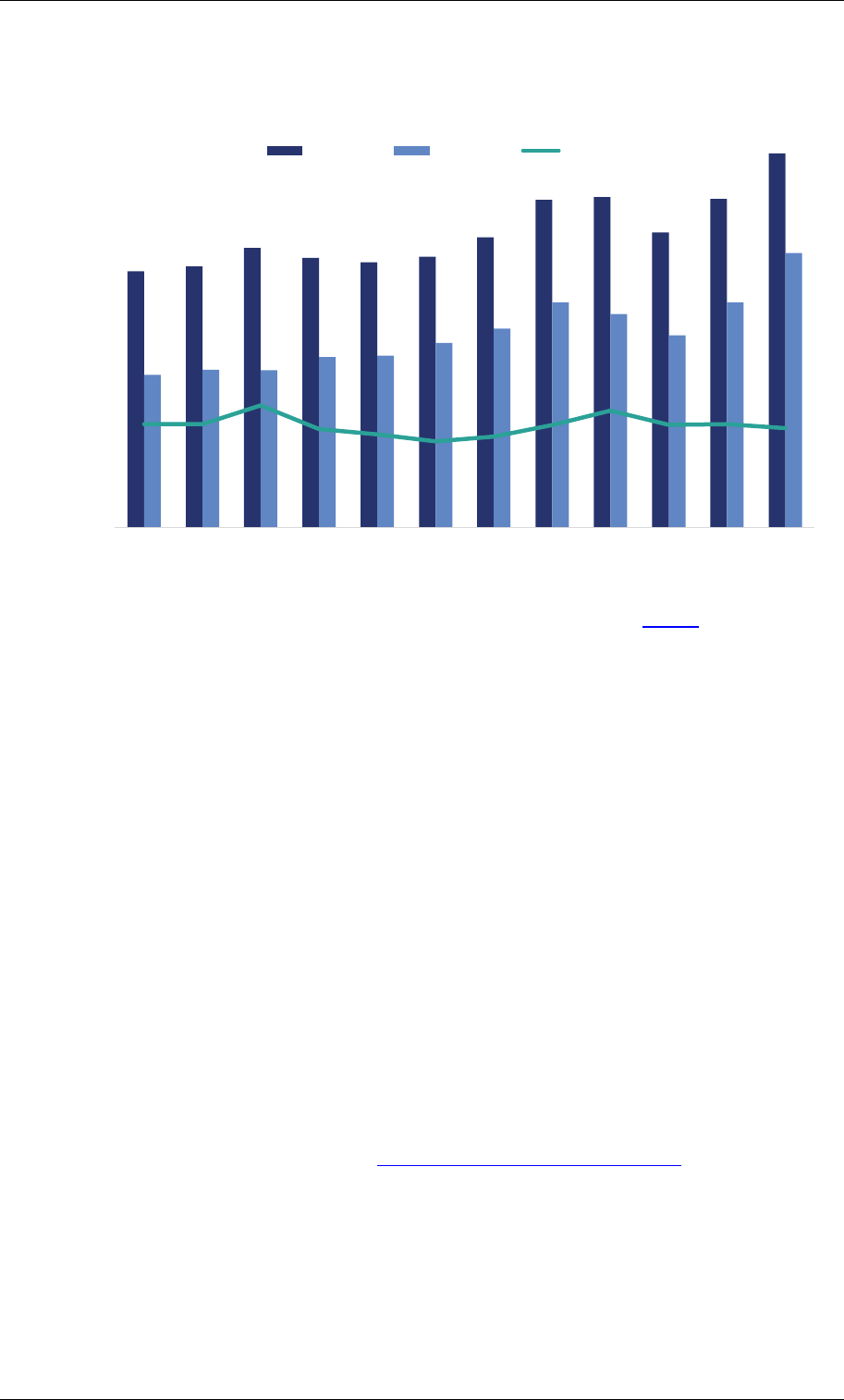

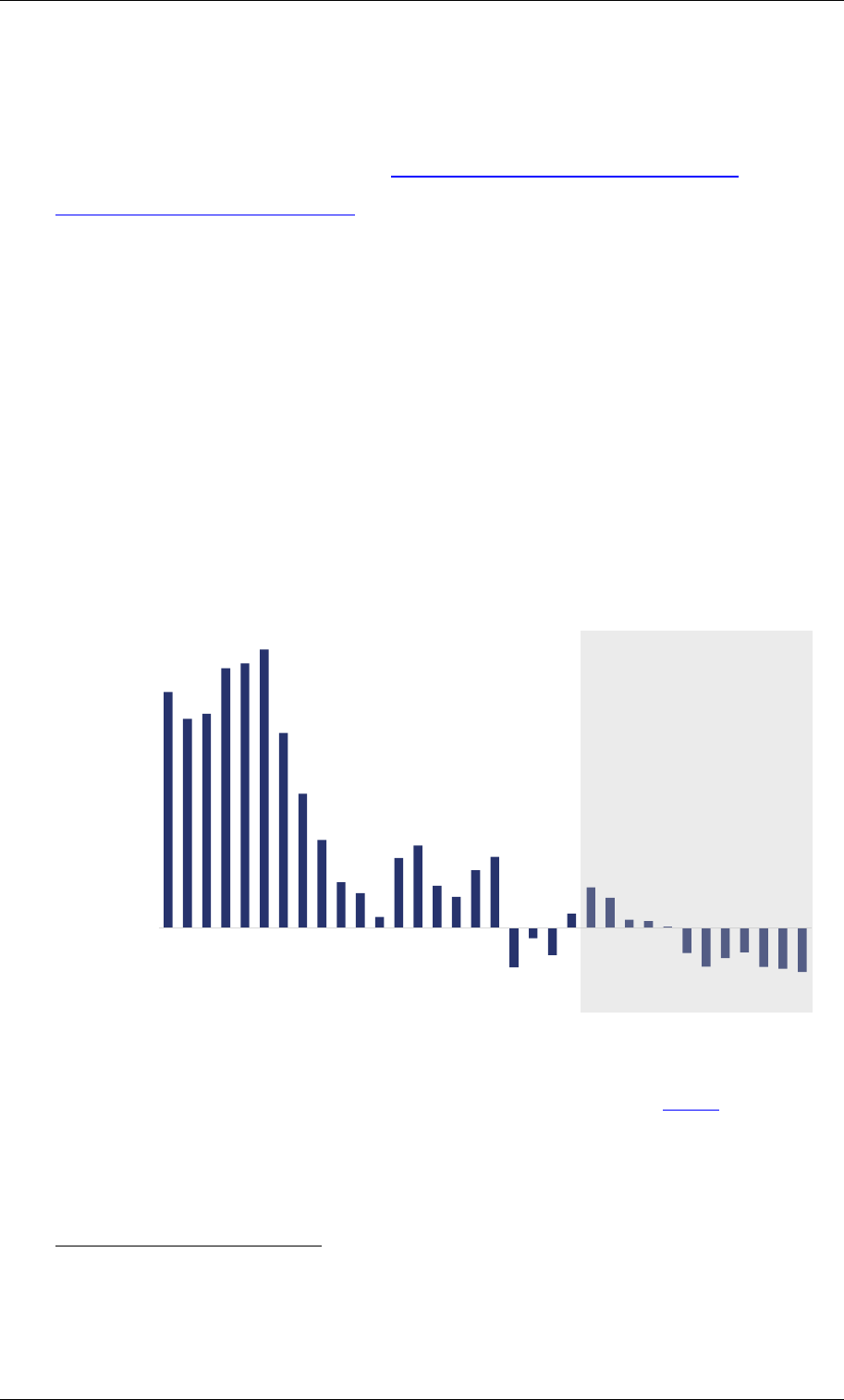

2.3 Trade

Northern Ireland has also been performing well in terms of its overall trade

balance (the balance of exports relative to imports). As of 2022, exports of

goods and services are at a record high of £13.3 bn – with a trade surplus of

£3.5 bn – as highlighted in Figure 5 below:

3

3

NISRA trade values are published in current prices, and therefore do not include the effects of

inflation over time.

2.6%

4.2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

Unemployment rate (%)

NI UK

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 11

Figure 5: Northern Ireland exports, imports & trade balance, 2011-2022

Source: NISRA, December 2023

3 Challenges

This section focuses on some of the key challenges facing Northern Ireland’s

economy. These include: above-target inflation; persistently high economic

inactivity; lower productivity than the United Kingdom average; potentially weak

labour supply growth; and, poor inclusion performance.

3.1 Inflation

Consumer Price Inflation (CPI) remained high over the past year, staying above

10% for the nine months between July 2022 and March 2023; peaking at 11.2%

in October 2022. However, headline inflation has been on a downward trend

since then. It was 4% in January 2024 – unchanged from December 2023.

Whilst this is still higher than the Bank of England’s target of 2%, it is nearly

three times lower than it was in October 2022.

The biggest contributors to January’s 4% headline rate of CPI inflation were:

restaurants and hotels (1%) food and non-alcoholic drinks (0.8%) and

recreation and culture (0.8%), as illustrated in Figure 6 below:

3.7

3.7

4.3

3.5

3.3

3.1

3.2

3.7

4.2

3.7

3.7

3.5

0

2

4

6

8

10

12

14

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Trade values (£ billion)

Exports Imports Trade balance

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 12

Figure 6: Components of CPI inflation, January 2024

Source: ONS, February 2024

Core inflation (which excludes energy, food, alcohol and tobacco) has remained

more stubbornly high. It was 5.1% in January 2024 – down only slightly from

5.2% in December 2023.

It is worth noting that whilst inflation is falling, that does not mean price levels

are falling. In fact, they are still increasing, but at a slower rate of increase.

Figure 7 below illustrates this:

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 13

Figure 7: CPI and “core” inflation, Jan 2019 – Jan 2024

Source: ONS, February 2024

3.2 Economic inactivity

High economic inactivity has been a significant, long-term issue for Northern

Ireland. The headline rate has been much higher than the United Kingdom

average for decades, and has remained stubbornly high. As of December 2023,

the headline rate in Northern Ireland was 26.8% relative to 20.8% in the United

Kingdom. Figure 8 below highlights this:

4.0%

5.1%

0%

2%

4%

6%

8%

10%

12%

Inflation rate 9%)

CPI Core (excl. energy, food, alcohol & tobacco)

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 14

Figure 8: Economic inactivity rate, Northern Ireland & United Kingdom,

Jan 2010 – December 2023

Source: ONS, NISRA, January 2024

There are a number of reasons for economic inactivity among the working age

population in Northern Ireland (such as retirement, student status, carers for

relatives, long-term sickness and disability). In relative terms, Northern Ireland

is similar to the United Kingdom average for most of these – but performs

significantly worse in terms of economic inactivity due to being long-term sick or

disabled. Long-term sick and disabled accounts for 41% of total inactivity in

Northern Ireland, as opposed to just 30% in the United Kingdom.

26.8%

20.8%

15%

17%

19%

21%

23%

25%

27%

29%

31%

Nov-Jan 10

May-Jul 10

Nov-Jan 11

May-Jul 11

Nov-Jan 12

May-Jul 12

Nov-Jan 13

May-Jul 13

Nov-Jan 14

May-Jul 14

Nov-Jan 15

May-Jul 15

Nov-Jan 16

May-Jul 16

Nov-Jan 17

May-Jul 17

Nov-Jan 18

May-Jul 18

Nov-Jan 19

May-Jul 19

Nov-Jan 20

May-Jul 20

Nov-Jan 21

May-Jul 21

Nov-Jan 22

May-Jul 22

Nov-Jan 23

May-Jul 23

Inactivity rate (%)

NI UK

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 15

Potential scrutiny point:

1) How will the Executive/departments address the persistently

high levels of economic inactivity? In particular, what

practical steps will they take to reduce the proportion of

long-term sick and disabled in Northern Ireland relative to

the United Kingdom average?

3.3 Productivity gap

Northern Ireland’s productivity gap to the United Kingdom average is another

long-running economic issue. Key productivity metrics have been persistently

below the United Kingdom average over the past two decades. Currently, as

illustrated in Figure 9 below: GDP per capita (20% gap); GDP per filled job

(10% gap); and GDP per hour worked (12% gap):

Figure 9: Productivity measures, Northern Ireland vs. United Kingdom,

2004-2021

Source: ONS, June 2023

70%

75%

80%

85%

90%

95%

100%

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

Relative to the UK

GDP per capita GDP per filled job GDP per hour worked

UK = 100%

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 16

The productivity gap highlighted at Figure 9 is a result of a combination of two

things:

1. The sectoral mix of the Northern Ireland economy – more reliance on

lower-productivity sectors relative to the United Kingdom average; and

2. Productivity differences within sectors – for example, lower

productivity in the financial services sector in Northern Ireland relative to

the United Kingdom average in the same sector (which itself could be

caused by a number of factors, including poor management

performance).

In other words, the productivity gap is due to a combination of what Northern

Ireland does; and how it does it. It should be noted that there are lots of

potential reasons for lower productivity – for example, the second (“how it does

it”) category, could include human capital, lack of research and development,

etc. Estimating the extent to which each of these factors contributes to Northern

Ireland’s productivity gap requires further research.

Potential scrutiny point(s):

2) What areas will the Executive or the DfE focus on to close

the productivity gap? When will that happen? If not, please

detail why not.

3) When seeking to do that, what balance will they strike

between attracting investment in higher productivity sectors

versus investing in management and upskilling?

4) What type/size of firms will government support focus most

on?

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 17

3.4 Labour supply

A potential challenge faced by the Northern Ireland economy is weak labour

supply growth – an issue noted in Ulster University’s Competitiveness

Scorecard for Northern Ireland.

4

This is a combination of low growth in working

age population (internal) and net migration (external).

3.4.1 Internal labour supply

Growth in Northern Ireland’s working age population has been weak in the last

decade. Moreover, according to Northern Ireland Statistics and Research

Agency (NISRA) estimates, growth for that group is anticipated to be flat from

2026, and negative from 2029 onwards.

5

That means the working age

population will decrease after 2029, as highlighted in Figure 10 below:

Figure 10: Working age population growth, Northern Ireland, 2002-2035

Source: NISRA, January 2022

4

Section 5.4.3

5

The ONS notes that national population projections are not forecasts and do not attempt to predict

potential changes in international migration.

-0.4%

-0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

2002 2005 2008 2011 2014 2017 2020 2023 2026 2029 2032 2035

Working age population growth (%)

Forecast

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 18

3.4.2 External labour supply

It should be noted that when a working age population is not growing – that is,

staying the same or contracting – additional reliance is placed on migration for

future labour supply. That trend presents a challenge for Northern Ireland when

considered in the context of inward migration from the United Kingdom and

internationally in recent years, which has been somewhat limited. Existing and

potential future immigration rules in the United Kingdom also could have

implications for labour supply growth in Northern Ireland. Figure 11 below

highlights the trend from 2002-2022:

Figure 11: Northern Ireland net migration, UK & Rest of world, 2002-2022

Source: NISRA, August 2023

3.5 Inclusion

There are other long-running challenges facing the Northern Ireland economy,

which are worth noting. Inclusion is one of them; defined by the OECD as

“…economic growth that is distributed fairly across society and creates

opportunities for all…”. It is below acceptable levels in a number of metrics in

Northern Ireland. For example, employment rates for disabled people in

Northern Ireland are much lower than those for non-disabled people; and are far

below the United Kingdom average.

-6,000

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

12,000

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Net migration

UK International Total

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 19

The employment rate for disabled people in Northern Ireland in 2021 was just

37.3%, compared with 79.6% for non-disabled people. The equivalent disabled

employment rate in the United Kingdom in 2021 was 53%. Figure 12 below

highlights this:

Figure 12: Employment rate, Northern Ireland, disabled & non-disabled,

2014-2021

Source: NISRA, October 2023

Making improvements in this area would have positive implications from

economic, social, and health perspectives. However, to illustrate the scale of

the challenge, if the gap in employment rate for disabled to the non-disabled in

Northern Ireland was halved (making it similar to the United Kingdom average),

there would be more than 40,000 more disabled people in employment in

Northern Ireland. At the average productivity level, this additional employment

would be equivalent to around 5% of Northern Ireland’s GDP.

Employment rates for the most deprived areas in Northern Ireland are also

significantly lower than those in the least deprived areas, and the Northern

Ireland average. In 2021, the rate in the most deprived areas was 56.1% -

compared with a regional average of 70.2%, and a rate in the least deprived

areas of 77.6%.

37.3%

79.6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2014 2015 2016 2017 2018 2019 2020 2021

Employment rate (%)

Disabled Non-disabled

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 20

For illustrative purposes, if the employment rate in Northern Ireland’s most

deprived areas was increased to match the Northern Ireland average, there

would be almost 29,000 more people in employment – equivalent to more than

3% of Northern Ireland’s GDP, as Figure 13 shows:

Figure 13: Employment rate, Northern Ireland, most deprived & least

deprived areas, 2014-2021

Source: NISRA, October 2023

Potential scrutiny point:

5) What steps will the Executive and the DfE take to reduce the

employment rate gap for those in Northern Ireland’s most

deprived areas; and those with a disability?

70.2%

56.1%

77.6%

40%

45%

50%

55%

60%

65%

70%

75%

80%

85%

2014 2015 2016 2017 2018 2019 2020 2021

NI average Most deprived Least deprived

NIAR 123-23 Northern Ireland economic overview

Providing research and information services to the Northern Ireland Assembly 21

4 Key takeaways

Northern Ireland's economy has been performing well on a number of important

measures: the economy has grown 38% in real terms since the signing of the

Belfast/Good Friday Agreement in 1998; employment levels have almost

returned to pre-pandemic levels; the unemployment rate is at a near-historic

low; and, exports are at record high levels.

However, those positives are offset by some significant challenges – both in the

immediate and longer terms. For example, the persistence of high inflation over

the past year has put pressure on businesses and consumers; and whilst it has

fallen from its peak in late 2022, it still remains above the Bank of England’s 2%

target.

Moreover, the high rate of economic inactivity remains one of Northern Ireland’s

most significant challenges, despite record low unemployment. Specifically, the

proportion of economically inactive working age adults that are long-term sick or

disabled is much higher than the United Kingdom average.

Additionally, persistently low productivity, weak labour supply growth and poor

inclusion performance in terms of disability and deprivation all need addressed.

This Paper – drawing on most recent available data – provides an update for

the incoming CfE on key aspects of the Northern Ireland economy and potential

scrutiny points, which could help to inform the Committee’s deliberations when

formulating its forward work plans and when engaging in future with the DfE and

other stakeholders. In particular, it has noted some of the areas in which

Northern Ireland’s economy has been performing well – including: the economy

growing almost 40% since the Belfast/Good Friday agreement was signed; total

employment surpassing its pre-pandemic peak; historic low unemployment

rates; and export values at a record high level. It has also outlined some of the

key challenges facing Northern Ireland’s economy. Those include: above-target

inflation; persistently high economic inactivity; lower productivity than the United

Kingdom average; potentially weak labour supply growth; and, poor inclusion

performance.