1

China’s Interest Rate System and Market-based Interest Rate

Reform

This article, authored by Governor Yi Gang, was published in the Journal of Financial

Research (Issue 9, 2021). The full text is as follows:

Interest rate is an important macroeconomic variable, and its liberalization is one of

the core reforms in China’s economic and financial sector. Since the reform and

opening-up, China has been steadily advancing interest rate liberalization to establish

and improve the mechanism in which interest rates are determined by market supply

and demand, and the central bank has been guiding market rates with monetary policy

instruments. After over 30 years of continuous efforts, China has achieved remarkable

results in its market-based interest rate reform. A complete system of market-based

interest rates has been formed, and the yield curve has come close to a mature pattern,

creating favorable conditions for enabling interest rates to play an important role in

adjusting the macro economy.

1. Interest rate is an important macroeconomic variable.

As the price of money, interest rate is of guiding significance to macroeconomic

equilibrium and resource allocation. Reflecting the degree of fund scarcity, interest

rate is an important indicator pricing the factor of production, as wages and rents.

Meanwhile, it is also a reward for delayed consumption. Effects of the interest rate on

behaviors and resource allocation are mainly measured by the real interest rate, i.e. the

nominal interest rate minus the inflation rate. In theory, the natural rate of interest is

the real interest rate at macroeconomic equilibrium where the aggregate supply equals

the aggregate demand. In practice, the level of interest rate directly affects the savings

and consumption of the public, the investment and financing decisions of enterprises,

imports and exports, and the balance of payments, thereby asserting broad influences

on the whole economy. Therefore, interest rate is an important macroeconomic

variable.

Interest rate plays an important role in adjusting the macro economy, mainly by

affecting consumer demand and investment demand. In terms of consumption, the

rise of interest rates will encourage savings and discourage consumption. In terms of

2

investment, higher interest rates will reduce the total volume of profitable investments

and dampen investment demand, filtering out projects with low rate of returns.

Interest rate also influences imports and exports as well as the balance of payments.

The decline of domestic interest rates will stimulate investment and consumption and

increase the aggregate demand, thereby increasing imports and resulting in a decrease

in net exports. Meanwhile, it will narrow the spread between the interest rates of

domestic currency and foreign currencies, which might lead to capital outflow and

affect the balance of payments. Undoubtedly the interest rate transmission mechanism

and the relationship among macroeconomic variables in the reality are much more

complex than the simplified version stated above.

The equilibrium interest rate is determined by market supply and demand, and

it is the result of savings, investment and financing activities by market

participants, including businesses, residents and financial institutions, who

mainly save and lend via banks, invest or get financed in the bond market, the

stock market and the insurance market, and then allocate financial resources to

the real economy and various assets. The market plays a decisive role in resource

allocation, and the allocation process is guided by prices of market transactions on the

premise of clearly-established ownership of equity. In the process, as the price of

funds, the interest rate determines fund flow and thereby the allocation of financial

resources. The miracle of China’s economic development since the reform and

opening up proves that, compared with the planned economy, the socialist market

economy, where resources are mainly allocated by the financial market, is much more

efficient and has brought much more benefits to the people. In the medium and long

term, macro interest rate should be basically in line with the natural interest rate.

However, as a concept abstracted from theories, the natural interest rate is difficult to

estimate. Therefore, in practice, the “Golden Rule” is often used to measure the

reasonable interest rate level, that is, when the economy is on a steady growth path

where the per-capita consumption hits its maximum, the inflation-adjusted real

interest rate (r) should equal the real economic growth rate (g). When r is constantly

higher than g, social financing costs will remain high, putting businesses at distress

and adversely impacting economic development. When r is lower than g, the nominal

interest rate is usually lower than the growth rate of nominal GDP. This is favorable

for debt sustainability, namely, stable or even lower leverage ratios, thus giving the

3

government some extra policy space. However, studies show that, at least in emerging

markets, debt crises are still unavoidable when r is lower than g. In general, it is

reasonable to have an r that is slightly lower than g. Empirical data suggests that in

China, for most of the time, the real interest rate is lower than the real economic

growth rate, which may be called an optimal strategy that allows leeway. However, r

cannot be constantly and significantly lower than g. An interest rate that is too low for

long will distort the allocation of financial resources, lead to overinvestments,

overcapacity, inflation and asset bubbles, and cause funds to circulate within the

financial system. Therefore, ultra-low interest rate policy is hard to sustain in the long

run.

Interest rate not only affects the investment returns and financing costs of micro

entities, but also acts more as a critical factor in balancing the aggregate supply and

demand in the macro economy. Therefore, all mature market economies have come to

take interest rate as a major macro regulatory instrument. In determining policy

rates, the central bank must conform to economic principles and the

requirement of macro regulation and inter-temporal designs. The ultimate goal of

China’s monetary policy is to “maintain the stability of RMB value and promote

economic growth”, and interest rate is the key to achieving the goal.

Following the strategic arrangements made by the Central Committee of the

Communist Party of China (CPC) and the State Council, we have been advancing the

market-based interest rate reform, which conforms to both national conditions and

international standards. While relaxing the interest rate control in an orderly manner,

we attach great importance to the establishment and improvement of the market-based

interest rate system in which interest rates are determined by market supply and

demand and guided by monetary policy instruments of the central bank, and we give

full play to the role of the interest rate in adjusting the macro economy.

2. China has established a complete system of market-based interest rates.

After 30 years of continuous efforts to advance the market-based interest rate reform,

China has basically established a market-based mechanism for interest rate formation

and transmission and a complete system of market-based interest rates. We adjust

liquidity in the banking system mainly with monetary policy instruments and send

4

regulation signals with policy rates. We guide the benchmark rates in the market to

move around the policy rates with the interest rate corridor, and transmit them to

lending rates through the banking system. In this way, the market-based mechanism

for interest rate formation and transmission has been established to adjust the supply

and demand of funds and the allocation of resources, thereby achieving the goal of

our monetary policy.

Figure 1 China’s interest rate system and framework for interest rate regulation

Table 1 Major types of interest rates in China

Interest rate type

Current rate

Introduction

Open market

operation (OMO) rate

7-day reverse repo

at 2.2 percent

Short-term reverse repo rate

Medium-term

lending facility (MLF)

rate

1-year MLF at 2.95

percent

The interest rate at which the central

bank lends to the market for medium terms.

Standing lending

facility (SLF) rate

7-day SFL at 3.2

percent ( = 7-day

reverse repo rate +

100BP)

The interest rate at which the central

bank provides short-term capital to

financial institutions as demanded, which is

the cap of the interest rate corridor.

Loan prime rates

(LPR)

1-year LPR at 3.85

percent,

4.65 percent for

maturities of 5 years and

above

The arithmetic average of loan rates

provided for customers of best credit

qualities by LPR quoting banks.

Benchmark

deposit rate

Demand deposits at

0.35 percent, 1-year

deposits at 1.5 percent

Interest rates published by the PBC as

a guidance for commercial banks to set

interest rates on customer deposits.

5

Interest rate on

excess reserves

0.35 percent

The rate at which the central bank

makes interest payments on the excess

reserves deposited by financial institutions,

which is the floor of the interest rate

corridor.

Interest rate on

required reserves

1.62 percent

The rate at which the central bank

makes interest payments on the required

reserves deposited by financial institutions.

Shanghai

Interbank Offered Rate

(Shibor)

2 percent

overnight, and around

2.35 percent for

3-month maturity

The arithmetic average of interbank

offered rates quoted by banks with high

credit ratings.

Government bond

yield

10-year

government bonds yield

around 2.85 percent

Reference rates for the market-based

bond market

In our market-based interest rate system, the most important types of interest rates

include:

(1) OMO rates and interest rate corridor. The 7-day reverse repo rate, one of the

OMO rates, is a short-term policy rate of the central bank and is currently at 2.2

percent. Through daily OMOs, the central bank keeps the liquidity in the banking

system adequate at a reasonable level and sends short-term policy interest rate signals,

so that short-term rates, such as the pledged depository-institution repo rate (DR),

could move around the policy rates and be transmitted to other market rates.

Meanwhile, through the interest rate corridor with the standing loan facility (SLF)

rates as the cap and the interest rate on excess reserves as the floor, the central bank

limits the movements of short-term interest rates within a reasonable range. The SLF

is a tool for the central bank to provide short-term funds to financial institutions as

demanded. As financial institutions may borrow from the central bank at the SLF

rates, they don’t have to borrow from the market at higher prices. Therefore, the SLF

rates could be regarded as the cap of the interest rate corridor. Currently, the 7-day

SLF rate stands at 3.2 percent, which equals the 7-day reverse repo rate plus 100 basis

points. Recently, the People’s Bank of China (PBC) launched reforms to promote

electronic transactions of SLF in an orderly manner, which are expected to raise

transaction efficiency, stabilize market expectations, enhance the stability of the

liquidity in the banking system, maintain the stable operation of money market

6

interest rates, and effectively prevent liquidity risks. The interest rate on excess

reserves is the rate at which the central bank makes interest payments on the excess

reserves deposited by financial institutions. As financial institutions can always

deposit their surplus funds into the excess reserve account and receive interest

payments at the interest rate on excess reserves, they would not be willing to lend to

the market at prices below such a rate. Therefore, the interest rate on excess reserves

can be regarded as the floor of the interest rate corridor. Currently, the interest rate on

excess reserves stands at 0.35 percent.

Figure 2 Short-term policy interest rates and the interest rate corridor

(2) MLF rates. The MLF rates are medium-term policy rates of the central bank,

which, together with the 7-day reverse repo rate, constitute the central bank’s policy

interest rate system. Currently, the 1-year MLF rate stands at 2.95 percent, which

represents the marginal cost of medium-term funds at which the banking system

borrows from the central bank. Since 2019, the PBC has gradually established a

mechanism for regular MLF operations, meaning that MLF operations are carried out

once in the middle of each month. By carrying out MLF operations in a fixed time

window at a fixed frequency, the PBC improves the transparency, regularity and

predictability of MLF operations, continuously sends the medium-term policy interest

rate signals to the market, and guides the movement of the medium-term market

interest rates. Let’s take the yield to maturity (YTM) of 1-year interbank negotiable

certificate deposits (NCDs) (AAA+ rated) as an example. In the past two years, it

generally moved around the MLF rates, except for the first quarter of 2020 when it

7

temporarily deviated from the MLF rates due to the impact of the COVID-19

pandemic.

Figure 3 Medium-term policy interest rates and NCD rates

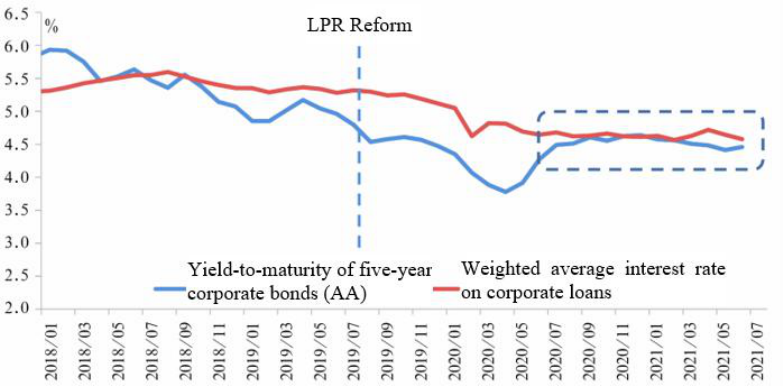

(3) LPR. In August 2019, the PBC launched the LPR reform, in which the panel

banks quote the LPR based on MLF rates and a comprehensive consideration of the

cost of funds, risk premium and other factors, so as to fully reflect the market supply

and demand. After two years of continuous advancement, financial institutions have

basically set prices with reference to the LPR when issuing loans, and completed the

conversion of the pricing benchmark for outstanding loans. The LPR has replaced the

benchmark lending rates to become the major pricing reference for financial

institutions, and the lending rates become evidently more market-based. After the

reform, the implicit lending rate floor is removed and the LPR timely reflects the new

trend of slightly declining market rates. In this way, we effectively leverage the role

of LPR in guiding the real lending rates to decrease and set up an interest rate

transmission mechanism featuring “a transmission from MLF rates to LPR and then to

lending rates”, thus greatly smoothing the transmission channel of monetary policies

and strengthening the mutual reference between lending rates and bond rates.

8

Figure 4 Post-reform mutual reference between lending rates and bond rates has intensified

to some extent

(4) Interest rates on reserves. Interest rates on reserves are the interest rates at

which the central bank pays for the reserves deposited at the central bank by financial

institutions. The rates are classified into two categories-the interest rate on required

reserves and the interest rate on excess reserves. At present, the interest rate on

required reserves stands at 1.62 percent in China, which helps to balance the interests

of various stakeholders and bolster the sustainable development of financial

institutions. In 2020, the interest rate on excess reserves dropped from 0.72 percent to

0.35 percent, on par with the benchmark rate of demand deposits. This aligned the

interest rate on household demand deposits at commercial banks with that on excess

reserves that commercial banks deposit at the central bank, which was relatively fair.

In addition, due to decreased return on excess reserves of commercial banks and

increased opportunity costs of idle money, commercial banks are motivated to boost

the efficiency of fund use and are encouraged to increase credit supply with their own

funds so as to better serve the real economy .

9

Figure 5 Interest rates on reserves

(5) Shanghai Interbank Offered Rate (Shibor). The PBC introduced Shibor in 2007,

which is a simple, no-guarantee, wholesale interest rate calculated by arithmetically

averaging all the interbank RMB lending rates offered by the panel of quoting banks

with high credit ratings. Featuring a complete maturity structure covering eight

maturities from overnight to 1-year, Shibor can serve as a reference to the pricing of

financial products of diverse maturities. At present, it has been applied in financial

product pricing in different layers of the money market, bond market and derivatives

market among others. Since the introduction of Shibor, the PBC has been performing

supervision and administration in an attempt to ensure the quality of Shibor quotations.

Meanwhile, in line with the general principle of drawing upon international consensus

and best practices, the PBC actively participates in the reform of international

benchmark rates, and guides the interest rate self-regulatory mechanism and the

National Association of Financial Market Institutional Investors (NAFMII) to release

a series of domestic reference texts on the transition from London Interbank Offered

Rate (Libor), creating favorable circumstances for domestic financial institutions to

respond to the withdrawal of Libor.

10

In addition, the benchmark deposit rates used to play an important role in the past.

As the market-based interest rate reform advances, at present, financial institutions

can independently determine their actual deposit rates. As every household holds

some deposits, these deposits are the most important products of financial services to

the public, which are related to their immediate interests. The deposit rates are

determined by the market under certain rules. As the guiding rates, the benchmark

deposit rates released by the PBC serve as an important reference to the pricing of

deposit interest rates by financial institutions. From the perspective of international

experience, deposit rates are generally more stable than other market rates. Currently,

domestic 1-year benchmark deposit rate stands at 1.5 percent, based on which

financial institutions can adjust their actual deposit rates upwards or downwards. This

level is regarded as a golden level, adaptive to the demand of inter-temporal policy

design. In September 2013, the self-disciplinary mechanism for setting interest rates

was established under the guidance of the PBC, which realized self-disciplinary

management on interest rate setting by financial institutions. The mechanism, with

reference to the benchmark deposit rates, has put in place a self-disciplinary

agreement on deposit rates, and plays an important role in maintaining fair and sound

competition order in the deposit market. In June 2021, the mechanism changed the

determination of the self-disciplinary ceiling for deposit interest rates, which had

shifted from adjusting the benchmark deposit rates upwards by a designated multiplier

to adding basis points to the benchmark interest rates. This helps further regulate the

competition order of deposit rates, improve the maturity structure of deposit rates, and

create a sound environment for the market-based reform of interest rates. When

needed, market entities can adjust their deposit rates downwards at their own

discretion.

11

Figure 6 Benchmark deposit rates

3. China’s Yield Curve Tends to Be Mature.

In the market-based interest rate system, the benchmark yield curve is crucial as

it provides pricing reference to various financial products for diversified market

entities. The yield curve reflects the maturity structure of interest rates ranging from

those of a shorter maturity to those of a longer one, and represents a system composed

of major benchmark rates of financial products with various maturities. The short end

of the yield curve shows overnight and 7-day depository-institutions repo rate

(DR007), whereas the long end demonstrates the government bond yields. From an

international perspective, even in the US where the bond market is rather developed,

its Treasury yield curve mainly works at the middle and long end, and the short-end

interest rates such as those in the money market are mainly determined with reference

to federal funds rate and Libor (SOFR after the reform). For different sections of the

yield curve, the central bank and the market have different roles to play. At the

short end of the yield curve, the central bank controls base money supply, and

provides short and medium-term base money through OMOs, MLF and others,

exerting direct impact on the short and medium-term benchmark market rates. At the

medium and long end of the yield curve, the benchmark rates are formed through

market transactions based on the market expectations of the development trend of the

macro economy as well as the stance of monetary policy. With an observation of

these rates, investors and policy makers can grasp important market information.

12

The Chinese government bond yield curve is getting mature in terms of its

construction and publication. Since the publication of the first yield curve for

RMB-denominated government bonds in 1999, the construction and publication of the

Chinese government bond yield curve have become increasingly stable and mature.

The providers include infrastructures, such as the China Central Depository &

Clearing Co., Ltd. (CCDC) and the China Foreign Exchange Trade System, and

global information services companies, such as Bloomberg. The yield curves

produced by the CCDC are published by China’s Finance Ministry, the PBC, and the

China Banking and Insurance Regulatory Commission on their official websites. The

US Treasury yield curves of major influence are those produced by the US Treasury

Department and Bloomberg. On the Chinese government bond yield curve, the

10-year government bond yield has drawn the most attention from the market and

given rise to active trading, with an average daily volume of nearly 500 transactions,

or more than RMB20 billion.

Figure 7 Chinese government bond yield curve (overnight to 10Y)

The Chinese government bond yield curve has had increasingly extensive uses.

Widely applied by market institutions in risk management, fair value measurement,

and transaction pricing, it is playing an important role in the bond market. Perpetual

bonds and floating-rate bonds issued or re-priced with reference to government bond

13

yields have amounted to nearly RMB3.7 trillion. With their issue prices benchmarked

against the ChinaBond government bond yield curve, over RMB30 trillion of local

government bonds and ultra-long maturity government bonds have been issued so far.

Internationally, the three-month Chinese government bond yield was included in the

Special Drawing Rights (SDR) interest rate basket in 2016, providing a pricing

benchmark for investments by overseas central banks and commercial institutions in

China’s bond market.

The Chinese government bond yield curve is still not as market-based as that of

developed markets. A mature yield curve can effectively reflect changes in

macroeconomic growth as well as in inflation. Judging by market size, the

outstanding amount of Chinese government bonds stands at RMB21 trillion, while

that of US Treasury bonds exceeds USD28 trillion. Moreover, Chinese government

bonds, especially long-term government bonds, have a relatively low turnover ratio,

with that of longer-than-10-year government bonds below 100 percent and much

lower than the 530 percent in the US. In terms of bid-ask spreads, the average market

maker spread in China’s government bond market is notably higher than that in the

US. The recent years have seen a rise in the correlation between Chinese government

bond and US Treasury yields. For instance, since 2016, the coefficient of correlation

between the 10-year Chinese government bond yield and the 10-year US Treasury

yield has been 0.67, as compared with the 0.3 recorded over the years 2010-2015. The

difference between Chinese government bond and US Treasury yields is reflective of

various factors combined.

Figure 8 10-year Chinese government bond yield and US Treasury yield

14

Then let’s talk about conventional and non-conventional monetary policies. Asset

purchases do not fall into the conventional monetary policy toolkit. Rather, they are

reluctant choices of the central bank when the market gets into trouble. Prolonged use

of asset purchases will jeopardize market functioning, monetize fiscal deficits,

undermine central bank reputation, blur the boundaries between central bank solutions

to market failures and its monetary policy stance, generate moral hazard, and cause

many other problems. Therefore, such operations should by all means be avoided. In

case asset purchases are indeed necessary, three principles should be followed. First,

central bank interventions should be aimed at restoring normal market operation

rather than playing the role of the market. Second, the central bank should act ahead

of the market and intervene in order to quickly stabilize market sentiment and avoid

worsening market failures. Third, the central bank should rein in asset purchases and

end them as early as possible so that the intensity of asset purchases matches the

severity of market failures. Currently, interest rates have been on a downward trend in

the world’s major developed economies, with some having adopted near-zero policy

rates or even negative interest rates. As China is expected to keep its potential

economic growth within the range of 5-6 percent, it is well positioned to conduct a

normal monetary policy and to maintain a normal, upward sloping yield curve. China

will pursue a normal monetary policy for as long as possible, with no need to engage

in asset purchases at present.

In line with the strategic arrangements made by the CPC Central Committee and the

State Council, the PBC will further move ahead with the market-based interest rate

reform and enhance the market-oriented interest rate formation and transmission

mechanism. On the one hand, continued efforts will be made to improve the central

bank policy rate system. We will consolidate the central bank policy rate system in

which OMO rates are taken as short-term policy rates and MLF rates as medium-term

policy rates so that market rates will move around policy rates in ideal circumstances.

We will improve the interest rate corridor and take steps to achieve wholly electronic

conduct of SLF operations. On the other hand, we will continue to enhance the

cultivation of market benchmark rates. The mechanism for the formation of LPR

quotes will be optimized while panel banks will be urged to improve the quality of

their quotes, go through performance assessments, and leave the panel if they don’t

qualify. Past LPR quotes will be released when appropriate. Additionally, we will

15

expand the application of the repo rate DR in financial products to further consolidate

its role as a benchmark. And we will follow market-based principles to develop the

government bond yield curve.

Meanwhile, not only should we lift restrictions through the market-based interest rate

reform, but no less attention should be paid to the formation of interest rates. A major

problem found in the process lies in the impediments to the formation and

transmission of market-based interest rates. The reasons behind include market

segmentation, which has resulted from regulatory arbitrage and the immaturity of

financial markets, and fiscal and financial institutional problems, such as soft

budgetary constraints on financing platforms as well as disorderly competition for

deposits. In the next stage, more work needs to be done to strengthen regulation,

improve business environment, tighten budgetary constraints, and defuse financial

risks in order to create more favorable conditions for furthering the market-based

interest rate reform.