TECHNICAL MEMORANDUM

Date:

May 2024

To:

County of San Bernardino

Mark Wardlaw, Land Use Services Director

From:

Colin Drukker, Principal

Subject:

Housing Element Program 4

Summary of Short-term Rental Outreach and Study Findings

Executive Summary

OVERALL CONCLUSION

Clear and empirical data was not found indicating that short-term rentals (STRs) have a substantial and distinct

impact on the availability of long-term, rental or ownership housing options in most unincorporated Mountain and

East Desert communities. However, an accumulation of data and analysis of key factors indicates that STR activity is

negatively affecting the long-term ownership and rental housing market in Joshua Tree (see Table ES-1).

Figure ES-1. Key Factors Indicating STR Activity Affecting Long-term Housing Market, by Community

Unincorporated Mountain Unincorporated East Desert

FACTOR

Big Bear

City

Crestline

Lake

Arrowhead

Running

Springs

Homestead

Valley

Joshua Tree

Morongo

Valley

1. Community History

- - - -

2. STR Presence

- - -

-

3. Seasonal Homeownership

- - - - -

-

4. Occupancy Trends

-

-

-

-

-

-

5. Non-seasonal Vacancy

- - - -

6. Highly Active STRs

-

- -

-

indicates STR activity may be affecting

the housing market

-

indicates STR activity unlikely to be affecting

housing market

Note: the above table and summary findings below reflect data that is available for larger communities, especially those communities that contain the largest

number of STRs. When data is available, analysis for other communities is contained elsewhere in the memo.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 2 of 37

SUMMARY FINDINGS

The primary driver of rising housing costs in the unincorporated Mountain and East Desert communities was the COVID

Pandemic. Areas that were once viewed as too far from major employment centers became part of the conventional

housing market for many households. Additionally, retirees and white-collar workers along the coast and other affluent

areas, flush with cash from home equity and/or high salary jobs, viewed the unincorporated Mountain and (especially)

East Desert communities as desirable and relative bargains, and were willing and able to pay much higher rents and

pay much higher sales prices. The historic lack of housing production across the state (lowest in nearly 20 years) meant

that these households were competing for a relatively small supply (that largely consisted of existing housing stock).

The COVID Pandemic exacerbated and/or distorted the normal housing market across the County, state, and entire

nation, making it extremely difficult to clearly distinguish the influence of short-term rental (STR) activity in

unincorporated Mountain and East Desert communities. Inferring the degree of influence from the data available

involved an evaluation of multiple factors, as summarized below. Based on this evaluation, there is not enough evidence

to conclude that STR activity has had a substantial and distinct impact on the availability of long-term, rental or

ownership housing options in most unincorporated Mountain and East Desert communities. However, the factors, in

aggregate, support a conclusion that STR activity is distinctly and negatively affecting the long-term ownership and

rental housing market in the Joshua Tree community.

1) COMMUNITY HISTORY | Resort/Destination vs Permanent Settlement

The potential impact of STR activity on the housing market is greater in communities that do not have a long

history of seasonal housing. The Mountain region developed in the early 1900s as a place for seasonal recreation

and has maintained its nature as a predominantly 2nd home/resort area. Parts of the East Desert region also

originated as unique short-term destinations, but most grew slowly as small, remote year-round residential

communities.

• The only incorporated community in the Mountain region, the City of Big Bear Lake, is overwhelmingly a

seasonal community, with roughly 70% of all homes owned as vacation/2nd homes in 2010 (74% in 2022). The

unincorporated communities contain somewhat higher rates of year-round occupants, though Crestline and

Wrightwood are the only areas (large enough to be reported in the Census) where year-round occupants

represent a clear majority (over 55%).

• Many of the communities were originally settled by cattle and sheep ranchers, with homesteading continuing

through the mid-1900s, and small year-round settlements emerging at various spots along the Twentynine

Palms Highway. Pioneertown has different roots, originating as a motion picture set for Old West films in the

1940s. While the Joshua Tree area was established as a National Monument in 1936 and as a National Park in

1994, the 1980 Community Plan stated, “Joshua Tree evolved from a rural retirement area to a community

which is attracting an increasing number of new residents.”

2) STR PRESENCE | Number of STRs

The potential impact of STR activity is greater in communities where the number of STRs is high, especially

compared to the total number of housing units. The communities of Big Bear City, Joshua Tree, and Homestead

Valley all contain a high number of STRs that also represent 15% or more of the total housing stock. In these

communities, STRs represent big enough portion of the housing stock that, if the STRs are not taking place in

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 3 of 37

units that are already vacation/2nd homes, STR activity could meaningfully decrease the overall supply of

available ownership and rental housing units.

• Over 3,800 STRs are located in one of three communities: Big Bear City (1,400 + 428, including Sugarloaf) and

Lake Arrowhead (951) in the Mountain region, and Joshua Tree (1,082) in the East Desert region. Three other

communities represent much of the remaining balance of STRs: Crestline (278) in the Mountain region and

Homestead Valley (295) in the East Desert region.

• These numbers of STRs represent the following approximate percentage of the total housing stock in each

community (compared to latest available Census data): Big Bear City including Sugarloaf (15%), Lake Arrowhead

(8%), Joshua Tree (29%), Crestline (4%), and Homestead Valley (15%).

3) SEASONAL HOMEOWNERSHIP | Rates of housing owned as vacation/2nd homes

With 99% of STR activity being “whole home” rentals, STR activity can only take place in housing that is owned

as a vacation/2nd home (aka seasonal housing). The potential impact of STR activity would appear to be greater

if a community’s rates of vacation/2nd homeownership increased over time. Over the past 10 years Joshua Tree

has transitioned from a year-round community to a one where over 1 in 5 homes are vacation/2nd homes. Rates

of year-round occupancy in other communities in either region have remained largely consistent.

• In Joshua Tree, more than 1 in 5 homes were owned as vacation/2nd homes in 2022, compared to 1 in 20 as

recently as 2012. The popularity of Joshua Tree National Park (attendance doubled between 2013 and 2017)

initially spurred changes in Joshua Tree's housing market. Between 2000 and 2012, only 2% to 5% of all housing

units were recorded as vacation/2nd homes. Between 2013 and 2017, the rate increased substantially,

reaching 19% in 2017 and staying at 18% through 2019. The COVID Pandemic further increased the popularity

of Joshua Tree as a destination and this rate increased slightly, reaching a historic high of 21% in 2022.

• Other unincorporated communities in the study area, in terms of year-round residency, are largely the same

as they were before Airbnb and Vrbo became popular or have increased rates of year-round residency. This

factor indicates that STR activity has not affected the supply of long-term housing in these communities.

4) OCCUPANCY TRENDS | Rates of year-round rental occupancy

The potential impact of STR activity could be inferred by a substantial decrease in the percentage of units that

are occupied by rental households, as a reduction in rental households may indicate a pattern of property owners

converting long-term rental properties into short-term rental properties. The rate of year-round rental

occupancy is at a historic low in Joshua Tree, while rates in other communities are the same or higher as levels

prior to the rise of Airbnb and Vrbo (2010/2011).

• In Joshua Tree, the percentage of year-round rental households stayed at or around 39% between 2015 and

2019. During the COVID Pandemic, this rate dropped to 37% in 2020 and 34% in 2021. However, this rate was

still above the rate in 2010 (baseline comparison year that represents a time that was not influenced by STR

activity). In 2022, the rate of year-round rental occupants dropped to 26%, which is an 8% drop from the

previous year, 5% below 2010, and a historic low for Joshua Tree. While part of this decrease reflects an

increase in ownership households, the rate of ownership households is 14% below levels from 2010.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 4 of 37

5) NON-SEASONAL VACANCY RATES | Vacancy rates and housing affordability

The potential impact of STR activity is greater in communities where the supply of non-seasonal housing units

for sale or rent is extremely low, as increased competition leads to higher sales prices and rents. The non-

seasonal housing supply in Joshua Tree, Morongo Valley, and Big Bear City are among the lowest, while other

communities are relatively balanced or appear to have excess available supply.

• A balanced vacancy rate is 4% to 6% for ownership housing and 5% to 8% for rental housing.

• The non-seasonal ownership vacancy rate in Joshua Tree hovered at or above the balanced range through

2017. Starting in 2018, the rate dropped to 1% and remained at or below 1% through 2022. This tight housing

ownership market is driving up not only sales prices but also rents as the increase in home prices has made

buying an obstacle to renters who would otherwise pursue buying. This leads to more renters pursuing the

same number of homes, which enables landlords to demand higher rents.

• The non-seasonal rental vacancy rate in Morongo Valley historically stayed above the balanced range but began

a persistent decline in 2018. Still, the non-seasonal rental vacancy rate did not fall below 5% until 2022,

indicating that the Pandemic may have played the dominant role in driving supply below a balanced range.

• The non-seasonal rental vacancy rate in Big Bear City displayed a sustained decline in its non-seasonal rental

vacancy rate from 15% in 2012 to 5% in 2015 to below 2% in 2017, with rates only falling more through 2022.

Increases in rent, however, did not increase substantially until during the Pandemic.

6) HIGHLY ACTIVE STRs | Frequency of STR activity

The potential for STRs to be preferred over (and replace) long-term rentals is greater in communities with a

higher number of highly active STRs (over 60 nights/year). Such highly active STRs earn, on average, more income

compared to use as a long-term rental. Based on discrete County transient occupancy tax data, Joshua Tree, Big

Bear City, and Lake Arrowhead have the largest number of highly active STRs: a minimum of 355, 291, and 208,

respectively.

• The 355 highly active STRs in Joshua Tree also represent over 9% of the total housing stock. While the number

of highly active STRs are also high in Big Bear City and Lake Arrowhead, the 291 and 208 units represent only

2% of those communities’ total housing stock.

• Data from AirDNA and AllTheRooms indicates that STR activity continues to grow in Joshua Tree and is viewed

more favorably as a market for STR investment compared to other places in the unincorporated county. For

example, AirDNA assigns a market score benchmarked against other every other market using five metrics:

investability, rental demand, revenue growth, seasonality, and regulation. The STR market in Joshua Tree is

rated by AirDNA as 97/100 or “Great”, while AirDNA ratings in for Lake Arrowhead and Big Bear City markets

are substantially lower.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 5 of 37

Table of Contents

EXECUTIVE SUMMARY ............................................................................................................................................. 1

Overall Conclusion .......................................................................................................................................................... 1

Summary Findings .......................................................................................................................................................... 2

BACKGROUND & PURPOSE ...................................................................................................................................... 7

2021–2029 Housing Element .......................................................................................................................................... 7

Program 4 Initiation ........................................................................................................................................................ 8

COMMUNITY OUTREACH ......................................................................................................................................... 8

ECONOMIC TRENDS ............................................................................................................................................... 11

National and Regional Housing Trends ......................................................................................................................... 11

Income and Housing Costs ........................................................................................................................................ 11

Housing Construction Trends ................................................................................................................................... 13

Housing Affordability by Occupation ........................................................................................................................ 14

Short-term Rental Trends ............................................................................................................................................. 16

A Brief Timeline of Short-term Rentals in San Bernardino County ........................................................................... 16

Influential Events and Trends ................................................................................................................................... 16

Short-term Rental Statistics in Unincorporated San Bernardino County ................................................................. 18

STR Market Evaluation .............................................................................................................................................. 21

HOUSING COST & SUPPLY ...................................................................................................................................... 22

Changes in Housing Values ........................................................................................................................................... 22

Home Values by Community .................................................................................................................................... 22

Short-term Rentals Sales Prices ................................................................................................................................ 23

Short-term and Long-term Rental Values ................................................................................................................. 25

Changes in Occupancy .................................................................................................................................................. 26

Occupancy Rates in Unincorporated Communities .................................................................................................. 26

Changes in Vacancy ...................................................................................................................................................... 29

Non-seasonal Vacancy Rates in Unincorporated Communities ............................................................................... 29

New Construction ......................................................................................................................................................... 33

Relationship and Timing of STR Permit to New Construction .................................................................................. 33

EXTERNAL STUDIES AND ARTICLES ON SHORT-TERM RENTALS ............................................................................... 35

Appendix

San Bernardino County Short-term Rental Data & Housing, by Granicus (under separate cover)

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 6 of 37

List of Figures

Figure ES-1. Key Factors Indicating STR Activity Affecting Long-term Housing Market, by Community ............................ 1

Figure 1. Outreach Materials and Meeting Images (2023) ............................................................................................... 10

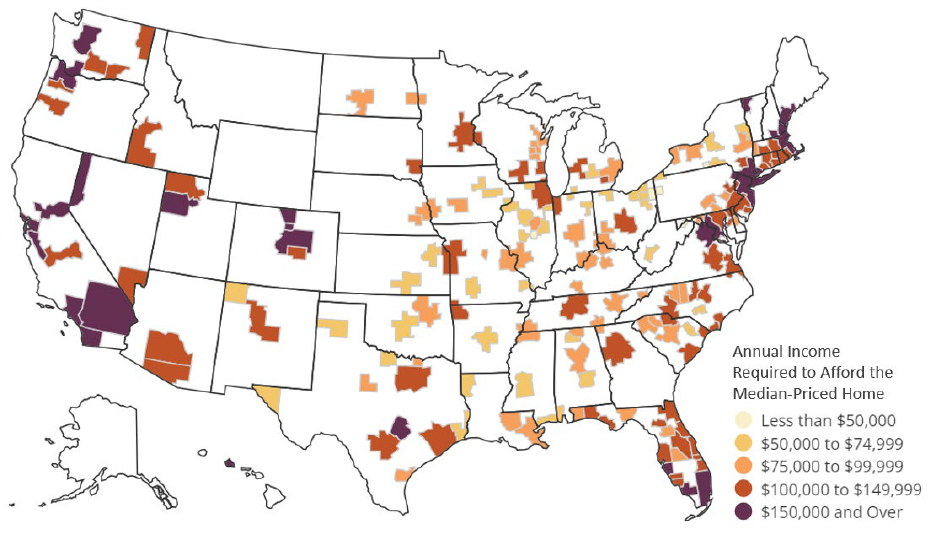

Figure 2. Annual Income Required to Afford the Median-Priced Home, 2021 ................................................................ 11

Figure 3. Rental Households with Cost Burdens, 2021 ..................................................................................................... 12

Figure 4. Low Cost Rentals, California, 2011 vs 2021 ....................................................................................................... 12

Figure 5. Total Housing Units per 1,000 People, California, 1991-2016 ........................................................................... 13

Figure 6. Insurance Risks and Premiums across the United States, 2023 ........................................................................ 14

Figure 7. Projected Job Openings and Median Wages, San Bernardino County, 2020-2030 ........................................... 15

Figure 8. Annual Increase in the Retired Baby Boomer Population (millions) ................................................................. 17

Figure 9. Percentage of Workers Working Remotely by Industry, United States, 2017-2022 ......................................... 17

Figure 10. First Year of Listing as a Short-term Rental by Region, Unincorporated San Bernardino County ................... 19

Figure 11. Units Listed as Short-term Rentals, Unincorporated San Bernardino County, 2021-2023 ............................. 19

Figure 12. Number of Short-term Rentals by Community, Unincorporated San Bernardino County, 2023 .................... 20

Figure 13. Percentage of Short-term Rental Owners that Live in the Same Region by Community, Unincorporated San

Bernardino County, 2023 .................................................................................................................................................. 20

Figure 14. Percentage of Short-term Rental Sales to LLCs by Region and Select Communities, Unincorporated San

Bernardino County, 2015-2022 ........................................................................................................................................ 20

Figure 15. Increase in Median Home Value, US, CA, and San Bernardino County, 2016 to 2023 .................................... 22

Figure 16. Home Values by Community, US, CA, and San Bernardino County, 2015, 2022, and 2023 ............................ 23

Figure 17. Sales Prices of Short-term Rentals, Unincorporated San Bernardino County, 2018-2022 .............................. 24

Figure 18. Sales Prices of Short-term Rentals, Big Bear City and Joshua Tree, 2018-2022 .............................................. 24

Figure 19. Comparison of Long-term and Short-term Rents, Unincorporated Communities, 2024 ................................ 25

Figure 20. Unincorporated Communities and Year-round Occupancy Trends, 2010 vs 2022 ......................................... 27

Figure 21. Unincorporated Communities with Dynamic Occupancy Trends, 2010 to 2022 ............................................ 28

Figure 22. Joshua Tree National Park, Annual Attendance, 2010 to 2022 ....................................................................... 28

Figure 23. Non-Seasonal Ownership Vacancy Rate Trends, Mountain Region and Countywide, 2010 to 2022 .............. 30

Figure 24. Non-Seasonal Ownership Vacancy Rate Trends, East Desert Region and Countywide, 2010 to 2022 ........... 30

Figure 25. Non-Seasonal Rental Vacancy Rate Trends, Mountain Region and Countywide, 2010 to 2022 ..................... 31

Figure 26. Non-Seasonal Rental Vacancy Rate Trends, East Desert Region and Countywide, 2010 to 2022................... 31

Figure 27. Relationship and Timing of STR Permit to New Construction, Unincorporated Study Area, 2019-2024 ........ 34

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 7 of 37

Background & Purpose

2021–2029 HOUSING ELEMENT

As required by all jurisdictions in Southern California, the County initiated an update to its Housing Element in 2021 to

address existing housing needs and plan for future housing growth. The County adopted the updated Housing Element

in September 2022 and received state certification (by the Department of Housing and Community Development or

HCD) in November 2022. As of October 31, 2023, the County is one of 14 (of the 25) jurisdictions in the county to have

received state certification.

Once the County confirmed its compliance with state law through certification, County staff could initiate the dozens

of implementation programs to be completed through 2029. In response to community concerns, the County designed

a program (Program 4) to conduct a public planning process and study the impacts of short-term rental activity on

renter households and the availability of long-term rental housing in Mountain and Desert unincorporated

communities. Program 4 is shown in its entirety below.

Program 4. Short-term Rentals

The proliferation of short-term, whole-home rentals can reduce the amount of available rental housing (particularly that which is

affordable) for people who work in a seasonal and permanent basis in the Mountain and Desert regions (and drive up the cost of housing

in the Valley region). Short-term rentals may also have a negative impact on local hotel/motel businesses. The County permits private

homes, including ADUs, to serve as short-term rentals in the Mountain and Desert regions (maximum stay of 30 days). In the Valley region,

private homes or ADUs must be rented for a term longer than 30 days.

To increase the availability of long-term housing options, the County will conduct a public planning process and a study to determine if the

County should establish a limit on the number of private homes or ADUs that can be developed and used as short-term rentals in the

Mountain and Desert regions. The study should also evaluate the potential effectiveness of various incentives to encourage long-term

rentals, particularly for local employees and lower income residents, as well as where and how many property owners are changing from

long- to short-term rental patterns, where and how many property owners are developing new housing units explicitly for use as a seasonal

home (by the property owner) and that is being made available to others as a short-term rental, the number of hosted vs. unhosted short-

term rentals, and the degree of displacement that is occurring. Based on the outcomes of the study, establish and implement strategies to

mitigate impacts on the loss of housing stock and affordability such as incentives to encourage long-term rentals and/or limiting the number

of total and/or new short-term rentals that can be permitted in the Mountain and Desert regions.

Objective: Conduct a public planning process and study to determine the current and projected impact of short-term rentals on the housing

supply throughout the unincorporated county and on the motel/hotel businesses in the Mountain and Desert regions. Establish and

implement strategies based on the study’s findings. Update and resubmit 2018 through 2021 annual progress reports (APRs) and ensure

that future reports account for units (ADUs, site-built homes, or manufactured homes) that apply for a short-term rental permit (unhosted

only) and communicate this information to HCD to remove such units from being counted as long-term housing units (at any level of

affordability).

Responsibility: Community Development and Housing, Land Use Services

Funding Source: General Fund

Timeframe: Initiate study in 2022 and complete public outreach and engagement in 2023, with a target completion date no later than

2023. Establish and begin implementation of recommended solutions by 2024 if the study’s conclusions support the establishment of

incentives and/or a limitation (by region and/or for specific unincorporated communities). By March 2023, bring forward an interim cap for

consideration by the Board of Supervisors on the total number of short-term rental permits on an annual basis and/or a percentage of total

housing units within each community planning area in the Mountain and Desert regions. Update 2018-2021 APRs in 2022 and adjust future

APRs annually to remove units used for short-term rentals.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 8 of 37

PROGRAM 4 INITIATION

Consistent with the stated timeframe in the Housing Element, the County initiated Program 4 in November 2022 and

contracted with Granicus and PlaceWorks to provide research, analysis, and outreach services. The County and Granicus

initiated a data analysis in late 2022/early 2023 in an attempt to identify any obvious evidence that could support an

interim cap on STR permitting. By February 2023, after reviewing County records, market trends, and Census data, the

County and Granicus concluded that there was insufficient evidence and confirmed a revised schedule with HCD.

County staff presented its interim findings and outline of future activities to the Board of Supervisors on March 28,

2023, which included further analysis and community outreach.

Community Outreach

The County held four public meetings in August and September 2023 in the communities of Big Bear, Crestline, Joshua

Tree, and Twin Peaks. At each meeting, the County shared its findings to date, requested feedback and additional

information from the community, and engaged in an extended discussion of questions and answers submitted by

attendees. In total, approximately 300 people attended the four meetings: Big Bear (50) Crestline (60), Joshua Tree

(130), and Twin Peaks (60). Additionally, the County received nearly 200 questions/comments submitted by email

during the same time period. The largest group of meeting attendees and email commenters represented local

residents, followed by STR owners (some of whom were also local residents), as well as some additional members from

local media outlets and service providers. The following represents a synopsis of the community’s input provided at the

meetings and through email submissions.

Management and operations. The vast majority of comments and questions concerned concerns about the

compatibility of STRs with long-term residential neighborhoods, with residents expressing ongoing problems related to

excessive noise, trash debris, and vehicle parking. Additionally, a number of residents indicated that many of the homes

on their block have turned into active STRs, an experience that is particularly new in the East Desert region. The majority

of residents communicated that they understood the role and benefits of STRs for the local economy, both for local

businesses benefitting from the additional tourism and for property owners benefitting from the income. These

residents welcomed STRs that acted as good neighbors and observed the County’s regulations. However, these same

residents also indicated that the STRs were essentially acting as disaggregated hotels, but without onsite management,

parking facilities, and cleaning staff that hotels provide that ensure tourists’ impacts on nearby residents are minimized

and addressed in a timely manner.

Fees and taxes. STR owners expressed dissatisfaction with the increased permit fees, with many asking how the fees

were spent. County staff informed attendees that the STR permit fees went directly to pay for the administrative costs

of the STR permit program and for increased code enforcement. Some attendees and email correspondents indicated

that they had seen improvements from the increased code enforcement investment (particularly in the Lake Arrowhead

area), while others stated that they had yet to see any improvements. Both STR owners and residents wanted to know

if the transit-occupancy tax (TOT) generated by STRs were going to be used to fund improvements in the communities

within which such funds were collected.

Housing affordability. Community input on the impact of STRs on housing affordability, particularly for long-term rental

housing, varied by region. In the Mountain Region, the input was mixed. Many agreed with the opinion that STRs were

pushing up prices and preventing homes from being rented to long-term tenants, with some citing anecdotal knowledge

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 9 of 37

of neighbors or local workers being pushed out of their rental housing so that the owner (existing or new) could operate

the house as an STR.

A number of others, including but not exclusively STR owners, stated that there was a long history of second-

homeownership and STRs in the region and that the recent increase in STR activity was simply the high point of another

cycle. Many attendees also commented that homes owned as second homes are less likely to ever be available for long-

term renters since the property owners would lose their ability to use the home on a seasonal or periodic basis. Another

common statement referenced STR income as a necessary supplement to pay for the rising costs of insurance premiums

(a hardship for all existing homeowners).

In the East Desert region, the attendees noted their local communities have historically been occupied by long-term

renters and year-round residents, with housing prices and rents that were relatively affordable. A number of meeting

attendees and email commenters, including videos from the Morongo Basin Conservation Association (MBCA), relayed

several stories of individuals and employers who cited the rise in STR activity as a reason for a shortage of affordable

housing.

At meetings in and comments from both regions, people cited recent legislation that made it difficult to evict long-term

tenants that failed to pay rent and/or damaged property, increasing the risk of long-term rentals (especially compared

to STR options). Meeting attendees from both regions suggested additional potential sources of information to evaluate

whether and the degree to which STRs were displacing long-term rental households. This included school districts, Big

Bear Homeless Coalition, and Big Bear Workforce Housing Coalition. For example, County staff followed up on

information cited in MBCA’s videos on the role of STRs in local displacement (Affordable Rentals citing discussions with

51 households in 2021 and the Morongo Unified School District citing calls 3-4 times per week about an eviction).

Unfortunately, attempts to corroborate these statements and clarify the role of STR activity as a direct factor were

unsuccessful, despite attempts to contact or successful communications with these entities. All school districts were

contacted, but no district offered data substantiating cause of homeless children as a result of STR activity.

Additionally, residents and STR owners from both regions urged the County to build more affordable housing, although

all understood the infrastructure limitations when the matter was discussed in more detail.

The County released its draft report on November 9, 2023 and reviewed preliminary results at a virtual outreach

meeting on November 16, 2023. County staff also provided answers to questions submitted in advance of the meeting,

which generally requested more clarification on the study’s preliminary findings and methodology. This meeting was

attended by roughly 80 residents and property owners (excluding County and consultant staff). A full recording of the

meeting was posted online a few days later and generated over 270 views. The County continued to take comments

and questions from the public, including an extensive comment letter (dated December 14, 2023) from the Morongo

Basin Conservation Association (MBCA), which requested additional information at the community level, requests for

a moratorium and cap on STR activity, and documented additional articles and other information to support refinement

of the Study’s analysis, methodology, and findings.

While the initial plan was to present the November 2023 draft report to the County Board of Supervisors in December

2023, County staff opted to postpone its presentation to allow time to review key US Census ACS datasets for year 2022

that were released on December 7, 2023, and to consider additional public input received during the November virtual

outreach meeting and MBCA’s December comment letter. The 2022 ACS datasets revealed distinctly different patterns

compared to prior years for the community of Joshua Tree, leading to additional analysis on all communities and

conclusions that varied from the November 2023 draft report.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 10 of 37

While the County received public comments both during outreach meetings and in email correspondence citing that

displacement is happening, direct communication with property managers, schools, service providers, and other

sources cited by the public yielded no information or confirmations that STR are directly responsible for displacing long-

term renters, serving as a primary cause of an increase in monthly rents, or creating a lack of long-term housing options

throughout the unincorporated Mountain and East Desert communities.

Figure 1. Outreach Materials and Meeting Images (2023)

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 11 of 37

Economic Trends

NATIONAL AND REGIONAL HOUSING TRENDS

Income and Housing Costs

The issue of high housing costs was historically limited to a relatively small portion of the country, notably areas along

the western and eastern coasts. Over the past decades, outward migration, rising rates of remote work, and corporate

expansion into lower cost states and regions increased housing demand in other parts of the country. In 2023, according

to the Harvard Joint Center for Housing Studies, the average household had to earn an annual income of at least

$100,000 to afford the median home price in multiple metropolitan areas across nearly every state in the country.

Additionally, the cost of rental housing, once the fallback for those seeking more affordable housing options, also began

to rise due largely to a combination of a lack of multifamily housing production and rising home sales prices. In 2021,

over a third of rental households spent over 30% of their income for housing in most counties throughout the nation.

When measuring the supply of rental housing stock in 2021 vs 2011 by monthly cost (adjusted for inflation), it becomes

clear that rents have increased substantially, with the majority of units now renting at or above $1,400 per month, and

units renting at or above $2,000 per month representing the largest portion of rental stock. See Figures 2 through 4 for

additional information.

Figure 2. Annual Income Required to Afford the Median-Priced Home, 2021

Source: Source: Harvard Joint Center for Housing Studies, “State of the Nation’s Housing 2023”; as of 9/28/23 prices and interest rates.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 12 of 37

Figure 3. Rental Households with Cost Burdens, 2021

Source: Harvard Joint Center for Housing Studies, “State of the Nation’s Housing 2023”; assuming cost-burdened households pay more than 30% of income

for housing.

Figure 4. Low Cost Rentals, California, 2011 vs 2021

Source: Harvard Joint Center for Housing Studies, “State of the Nation’s Housing 2023”. Includes both vacant and occupied rental units but excludes those

with no cash rent. Contract rents exclude utility costs paid separately. Rents are adjusted for inflation using the CPI-U for All Items Less Shelter.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 13 of 37

Housing Construction Trends

While the construction of new homes was already in a substantial downward trend across the United States since the

30-year peak in 2011, construction activity dropped even more sharply during the COVID-19 Pandemic. California’s

supply of housing units per capita has been on the decline for most of the last 25 years, both statewide and in all the

heavily populated regions. More people are competing for fewer homes, driving up housing prices. The effects of

increased housing demand can be exacerbated in areas with a high percentage of second homes that do not contribute

to the long-term housing supply, often sitting vacant most of the year.

Figure 5 illustrates the total number of housing units (occupied or vacant) compared to the total number of people in

California by region on an annual basis. Even with a trend of decreasing household sizes over the past decade

throughout California (and San Bernardino County), this figure shows that new housing construction is not keeping pace

with population growth.

Figure 5. Total Housing Units per 1,000 People, California, 1991-2016

Source: California State Association of Counties, as charted by Geoff Neill. “Southern Inland” represents San Bernardino, Riverside, and Imperial counties.

Additional contributing factors include the rising rates and costs of natural disasters, which are driving up insurance

premiums throughout much of America. The Mountain region of San Bernardino County is particularly susceptible to

wildfires and has seen rising rates, reducing housing affordability for existing and new residents. This issue was echoed

during the community outreach meetings held in the Mountain communities. Figure 6 compares statewide rates to

cities and communities that are more prone to natural disasters, which adds to the total cost of long-term housing and

reduces affordability for both owners and renters.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 14 of 37

The level of wildfire susceptibility and associated risks to people and property is one of the reasons the County

developed and adopted Policy HZ-1.2 (listed below) in the Hazards Element of the Policy Plan, along with other policies

in its Land Use Element, that would discourage new development in the Mountain region without proper design to

enhance safety and resiliency during time of disaster.

Policy HZ-1.2 New development in environmental hazard areas. We require all new development to be located

outside of the environmental hazard areas listed below. For any lot or parcel that does not have sufficient buildable

area outside of such hazard areas, we require adequate mitigation, including designs that allow occupants to shelter

in place and to have sufficient time to evacuate during times of extreme weather and natural disasters.

• Flood: 100-year flood zone, dam/basin inundation area

• Geologic: Alquist Priolo earthquake fault zone; County-identified fault zone; rockfall/debris-flow hazard area,

medium or high liquefaction area (low to high and localized), existing and County-identified landslide area,

moderate to high landslide susceptibility area)

• Fire: high or very high fire hazard severity zone

Figure 6. Insurance Risks and Premiums across the United States, 2023

Source: Bankrate and NOAA National Centers for Environmental Information, 2023. Notes: Premiums shown are for $250,000 in dwelling coverage. The

erroneous identification of Lake Arrowhead as a “city” is noted but not corrected. Additionally, the rates shown above are averages and may not represent

the lower or higher rates experienced by individuals in each unincorporated community.

Housing Affordability by Occupation

An adequate supply of affordable housing for the local workforce is critical to the County’s economic success and its

residents’ prosperity. Of the top 25 fastest growing occupations in San Bernardino County, as projected through 2030,

only Registered Nurses and Managers have a median annual wage that is adequate to afford the median home sales

price (as of 2023) either as a single- or dual-income household. When looking at the median rents in San Bernardino

County, just over half (14/25) of the fastest growing occupations need dual incomes (totaling at least $76,800) to afford

the median rent for a 2-bedroom unit ($1,920 being the 50

th

percentile rent in San Bernardino County as of 2023

according to the U.S. Department of Housing and Urban Development or HUD). Furthermore, the top two occupations

(Home Health and Personal Care Aides and Fast Food/Counter Workers) need dual incomes (totaling at least $61,320)

to afford the median rent for a 1-bedroom unit ($1,533 being the 50

th

percentile rent in San Bernardino County as of

2023 according to HUD). See Figures 7 for additional information.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 15 of 37

There are a number of occupations that were commonly cited during outreach activities as “backbone” jobs critical to

the basic functions of the community and raising a family. Some, such as primary and secondary school teachers and

Sheriff deputies, are not in the top 25 occupations in terms of job growth and are therefore not shown in Figure 7. The

median wage for both of these occupations, as of 2023 for the San Bernardino County area, was roughly $100,000—a

wage that is adequate to afford the median home sales price and 2-bedroom (or larger) rental units. More localized

salaries for teachers (e.g., Morongo Unified School District 2022-2023 Teacher’s Salary and Big Bear Unified School

District 2023-2024 Teacher’s Salary) indicate a median wage closer to $90,000—still enough to afford the median home

sales and rental costs.

Figure 7. Projected Job Openings and Median Wages, San Bernardino County, 2020-2030

Source: Occupation and wages: California EDD, Top 25 Occupations Ranked by 10-Year Total Projected Job Openings (2020-2030), Median Annual Wage Q1

2023. Home price and affordability: Harvard Joint Center for Housing Studies, as of 9/28/23 prices and interest rates. Median rent: US HUD, Office of Policy

Development and Research, 2023 50

th

Percentile Rent: $1,920 2-bd, $1,533 1-bd; Rent affordability: Harvard Joint Center for Housing Studies.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 16 of 37

SHORT-TERM RENTAL TRENDS

A Brief Timeline of Short-term Rentals in San Bernardino County

Mountain Resort before 1990s. The Mountain region’s resort history started in the late 1800s, with hotels, camps, and

collections of cottages and cabins sprouting up around the various lakes. Through the 1990s, tourist accommodations

remained largely under the operation of hotel and management companies.

STR Companies Emerge in 1995 & 2008. Buoyed by the widespread adoption of the internet and other digital

technologies, two companies emerged that greatly facilitated the ability of individual homeowners to rent out their

property directly to visitors. First, Vrbo (vacation rentals by owner) launched its website in 1995 in Aurora, Colorado,

and allowed users to browse and book vacation rental properties managed by individual owners. While Booking.com

was founded shortly after in 1996 in the Netherlands, the site started as a travel fare aggregator, though it later become

the first hotel booking site to advertise vacation rentals.

As online lodging grew as a business, Airbnb grew as a startup in San Francisco in 2008, and became the first company

to allow guests to book a single room in a host’s home and pay using a credit card over the internet. As of August 2023,

Vrbo has 2 million properties (whole home only) in 190 countries and Airbnb has 7 million places (a combination of

whole home and private rooms) to rent across 191 countries.

County Activities between 2017 and 2020. The County established a formal short-term rental permit system in the

Mountain region in 2017, followed by an expansion into the Desert region in 2019. Also in 2019, the County began

working with T-Mobile to roll out a countywide 5G network, which expanded into rural Mountain and Desert

communities in 2020. The presence of reliable broadband infrastructure facilitated remote work and enhanced the

desirability of long- and short-term stays.

Influential Events and Trends

COVID-19, 2020 to 2022. The COVID-19 Pandemic started in early 2020, growing from an international concern in

January 2020 to a global pandemic in the span of three months. By March, countries began to seal borders, schools

closed for the year, shelter-in-place orders were issued, long-planned events were cancelled, and evictions were halted.

Throughout 2020, Southern California residents look to the Mountain and Desert region communities as safe and

desirable options for remote tourism reachable by car. Some of these residents, already required to work remotely,

begin to see these communities as options for long-term stays or even permanent relocations.

By 2021, a vaccine was developed and travel restrictions began to ease, with statewide tourism restrictions ending in

June 2021 and national tourism restrictions ending in November 2021. By February 2022, the Governor of California

had ended the vast majority of COVD-19 related executive orders. Throughout late 2021 and much of 2022, people

around the state and country travel extensively and surge into destinations located in and around the county’s

Mountain and Desert regions.

Baby Boomer Retirement Patterns, 2020 to 2030. By 2030, all members of the Baby Boomer Generation will be aged

65 or older. While the pace of retirement stayed relatively consistent between 2012 and 2019, with some decline even

as the cost of living forced some to remain in the workforce, the pace of retirement accelerated with the onset of the

Pandemic. Concerns about proximity to other people during the Pandemic, particularly for those of retirement age,

increased the appeal of the remote and rural setting found in Mountain and Desert region communities. Additionally,

Baby Boomer homeowners often purchased their homes many decades in the past and, with housing prices rising ever

higher, were flush with home equity. See Figure 8 for more details.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 17 of 37

Figure 8. Annual Increase in the Retired Baby Boomer Population (millions)

Source: Pew Research Center, 2021.

Remote Work Patterns, 2018 to 2022. Rates of working remotely surged during COVID due to stay-at-home orders and

quick improvements in remote meeting and computer network technology. The US Census reported that the number

of people working remotely tripled during COVID, rising from roughly 6% in 2019 to 18% in 2021. Research by payroll

companies, such as Gusto, found that the communications, technology, and professional services industries are

experiencing the highest rates or remote work, but that all industries are seeing increased rates, even those that are

strongly dependent on in-person work. While some companies have pushed for workers to come back to the office,

rates of remote work are projected to remain high by multiple demographic and occupational research entities. This

“new normal” means many workers are no longer restricted by proximity to their work when choosing a home to rent

or buy. See Figure 9 for more details.

Figure 9. Percentage of Workers Working Remotely by Industry, United States, 2017-2022

Source: Gusto, payroll research data, 2017-2022.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 18 of 37

Short-term Rental Statistics in Unincorporated San Bernardino County

53% of STRs were first listed in 2020 or later. Based on analysis by Granicus of permitted and unpermitted short-term

rentals, over half (53%) of currently active STRs were first listed on any one of over 60 internet platforms in the year

2020 or later. See Figure 10 for more details.

The number of STRs peaked across the entire unincorporated county in July 2022. Following the end of domestic and

international travel restrictions, the number of unique short-term rentals in unincorporated San Bernardino County

peaked at 7,749 units in July 2022. A secondary, though lower, spike occurred in the winter of 2022, followed by a

dramatic drop in the early part of 2023. While a similar seasonal surge took place in 2023, Granicus reported 6,395 STRs

in September 2023, which is nearly 1,400 below the 2022 peak and may indicate a market correction in multiple markets

of the unincorporated county. Additional datasets reported by STR research entities AlltheRooms and AirDNA indicate

that February 2024 listings are relatively consistent with the September 2023 figure, although occupancy rates are

lower both overall and in many of the most popular communities. For example, AirDNA reports occupancy rates were

down 3% in both Lake Arrowhead and Joshua Tree markets when comparing February 2023 and February 2024.

AllTheRooms reports a 4% drop in Lake Arrowhead and an 11% drop in Joshua Tree for the same time period.

Most STRs are in Big Bear City, Lake Arrowhead, and Joshua Tree. Over 3,400 STRs are located in one of three

communities: Big Bear City (1,400) and Lake Arrowhead (951) in the Mountain region, and Joshua Tree (1,082) in the

East Desert region. Three other communities represent much of the remaining balance of STRs: Sugarloaf (428) and

Crestline (278) in the Mountain region and Homestead Valley (295) in the East Desert region. See Figure 12 for more

details (note that not all communities are shown; those that are not shown do not contain a substantial number of

STRs). Additional County data and datasets reported by STR research entities AlltheRooms and AirDNA (as of February

2024) indicate that the number of STR listings has dropped in some communities but increased slightly in Big Bear City,

Lake Arrowhead, and Joshua Tree.

Very few STRs are owned by people who also live in the same area. Overall, roughly 13% of STR owners live within the

same zip code or community planning area as the STR. Roughly 15% of STR owners live within the same region and

could be considered local owners. Another 5% of STR owners live somewhere else in San Bernardino County. Over 93%

of STR owners live somewhere in California and roughly 40% of STR owners live in Los Angeles or Orange County. Only

a handful of properties are associated with international owners.

Only 8% of STR owners in Big Bear City and 7% of STR owners in Lake Arrowhead live locally (somewhere in the Mountain

region). In other Mountain region communities, the percentage of local owners can be much higher, but is only above

20% in places where the total number of STRs is relatively low. In the East Desert region, rates of local ownership are

higher, though still only 22% in Joshua Tree and 25% in Landers. See Figure 13 for more details.

LLCs were active in Joshua Tree but are not prominent elsewhere. While under 10% of all STRs are owned by limited

liability corporations (LLCs), sales to LLCs grew during the first two pandemic years. LLCs were especially active in Joshua

Tree during 2020 and 2021, representing 30% to 40% of all STR sales in those years. LLCs are commonly associated with

a form of corporate activity that can amass a number of STRs to operate as a disaggregated hotel. However, individuals

that only own one STR may still establish ownership through an LLC for matters related to privacy, asset protection, tax

advantages, and other reasons. See Figure 14 for more details.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 19 of 37

Figure 10. First Year of Listing as a Short-term Rental by Region, Unincorporated San Bernardino County

Source: Granicus, using County STR permit database and over 60 internet platforms. Note: Units that first listed prior to 2015 and those in the North Desert

are not shown on the chart.

Figure 11. Units Listed as Short-term Rentals, Unincorporated San Bernardino County, 2021-2023

Source: Granicus, using County STR permit database and over 60 internet platforms. Figures represent unique STR units.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 20 of 37

Figure 12. Number of Short-term Rentals by Community, Unincorporated San Bernardino County, 2023

Source: Granicus, using County STR permit database and over 60 internet platforms. Note: not every unincorporated community shown.

Figure 13. Percentage of Short-term Rental Owners that Live in the Same Region by Community, Unincorporated San

Bernardino County, 2023

Source: Granicus, using County STR permit database and over 60 internet platforms. Note: not every unincorporated community shown.

Figure 14. Percentage of Short-term Rental Sales to LLCs by Region and Select Communities, Unincorporated San

Bernardino County, 2015-2022

Source: Granicus, using County STR permit and Assessor databases and over 60 internet platforms.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 21 of 37

STR Market Evaluation

As STRs grew in popularity, other companies emerged to provide analytics and tools to serve individual and larger

investors evaluate markets both broadly (e.g., throughout California) and specific to individual submarkets or

geographies (e.g., Joshua Tree). The largest of these companies is AirDNA, with AllTheRooms a commonly used

alternative. Both provide a wide range of datasets, including trends on revenue, occupancy, and supply, to help

investors and property owners understand how certain markets are performing. AirDNA offers a market score for each

geographic area benchmarked against other every other market area using five metrics (details below), with values

assigned on a scale of 0 to 100 (with 100 being the best).

- Investability: cost of homes compared to the average short-term rental income of full-time rental properties

- Rental demand: frequency of rental bookings throughout the year

- Revenue growth: change in year-over-year revenue per property

- Seasonality: percentage difference between the minimum and maximum monthly average revenue in the past

year (difference in demand between peak and low seasons)

- Regulation: amount or complexity of regulations

Looking at both AirDNA and AllTheRooms metrics, STR investment value in the Mountain region appears to be on a

downward trend, while STR investment value in the East Desert region remains extremely high. Data from AirDNA and

AllTheRooms indicates that STR activity continues to grow in Joshua Tree and is viewed more favorably as a market for

STR investment compared to other places in the unincorporated county. For example, The STR market in Joshua Tree

is rated by AirDNA as 97/100 or “Great”, while AirDNA ratings for Lake Arrowhead and Big Bear City markets are

substantially lower.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 22 of 37

Housing Cost & Supply

CHANGES IN HOUSING VALUES

Home Values by Community

The change in home values by community was evaluated to identify patterns that could indicate whether short-term

rental activity was driving up housing costs in specific communities. Home values have been steadily increasing over

the past seven years across the country, with prices in California rising faster and to higher values compared to the

national median. See Figure 15 for more details.

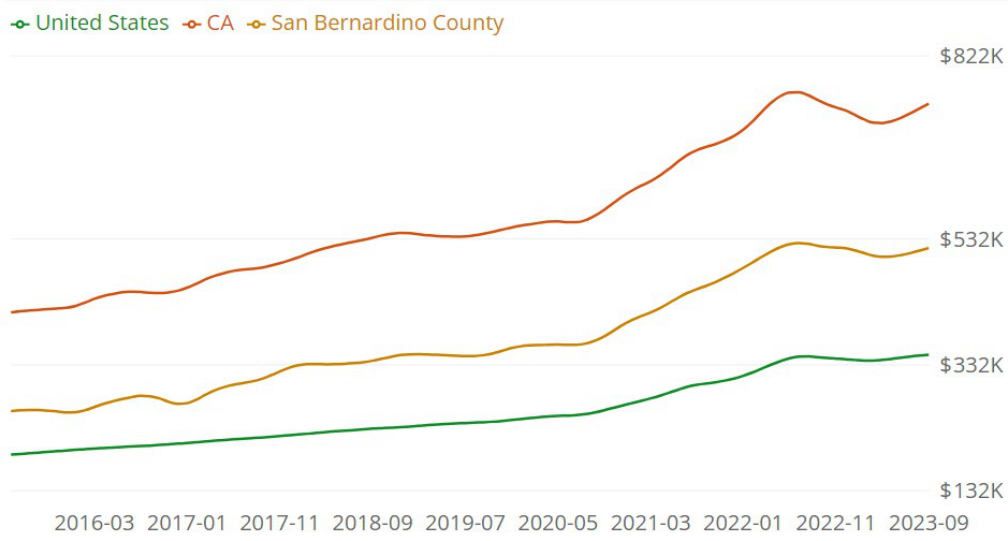

Figure 15. Increase in Median Home Value, US, CA, and San Bernardino County, 2016 to 2023

Source: Zillow Home Value Index, comparing median home values between March 2016 and September 2023.

The rate of increase in the median home value between 2015 and 2023 for unincorporated Mountain and East Desert

communities was compared against the rates for the United States, California, unincorporated Valley region

communities (where STRs are not permitted), unincorporated North Desert communities (where STRs are not

prevalent), and incorporated cities in the Mountain and East Desert regions.

The results indicate that the unincorporated East Desert communities experienced the greatest rate of increase in home

value between 2015 and 2022 (avg. +266%), with the two East Desert incorporated jurisdictions demonstrating a similar

rate of increase (avg.+185%). The communities of Big Bear City and Lake Arrowhead saw comparatively modest rates

of increased home values (avg. +113%), that were only slightly higher than the Valley communities of Bloomington and

Mentone, and roughly the same as the North Desert communities of Phelan and Pinon Hills.

However, the dramatic rise in home values in the East Desert region was influenced by their relatively low home values

in 2015 (avg $124,000). By 2022, home values were $300,000 or more in all unincorporated areas, and many areas were

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 23 of 37

valued closer to $400,000. Home values dropped from their 2022 peak (avg -8%), with steeper declines in places with

the greatest number of STRs (avg -14%), as of September 2023. See Figure 16 for more details.

Figure 16. Home Values by Community, US, CA, and San Bernardino County, 2015, 2022, and 2023

Source: Zillow Home Value Index, comparing median home values in June 2015, July 2022, and September 2023.

Short-term Rentals Sales Prices

The sales prices of short-term rentals were compared to the sales prices of non-STR single-family homes. In tracking

sales prices between 2018 and 2022, the data indicates that STRs were typically sold at higher values compared to other

single-family homes (SFHs). While it may be presumed that STR properties sell for higher prices based on their potential

to generate income, the fact is that any property in the unincorporated Mountain and East Desert region can function

as a STR, and any theoretical value associated with income potential is already incorporated into the market prices of

all housing units. Certainly, a property with an existing track record of generating income as a STR may be easier to sell

(and at a higher price), but the differences in sales prices are at least partially the result of STR properties often being

in better condition, larger in size, and better located. See Figure 17 for more details.

Additional insight can be obtained by comparing sales prices of STR and non-STR SFHs in Big Bear City and Joshua Tree.

STR prices were similar to other SFHs in Big Bear, where STRs already have a long history. Big Bear City’s longer history

with STR activity is likely a big reason for the relatively minimal sales price differential between properties used as STRs

and those that are not. STR prices in Joshua Tree were similar to other SFHs, even after STR permits were allowed in

2019, with the sales price differential actually narrowing between 2019 and 2020. The sales price differential only

diverged once the Pandemic hit. See Figure 18 for more details.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 24 of 37

Figure 17. Sales Prices of Short-term Rentals, Unincorporated San Bernardino County, 2018-2022

Source: Granicus, 2023.

Figure 18. Sales Prices of Short-term Rentals, Big Bear City and Joshua Tree, 2018-2022

Source: Granicus, 2023.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 25 of 37

Short-term and Long-term Rental Values

Although the cost of long-term rental housing is steadily increasing, so too is the nightly price for a short-term rental in

the unincorporated Mountain and East Desert regions. Throughout these regions, as of 2023, STR owners needed only

have their property booked for an average of between six and nine nights per month (72 to 108 nights per year) to

generate the same income as the median monthly rent from a long-term tenant. This can also be portrayed as the ratio

between the two income options (LTR/STR Price Ratio). A lower ratio means that it takes fewer nights of STR activity to

equal a long-term contract. See Figure 19 for more details. Data using average daily rents for STRs and median rents for

long-term rents as of May 2024 indicates that the initial break-even number of nights is between 66 and 76 for the

three biggest STR markets (Big Bear City, Lake Arrowhead, and Joshua Tree).

Additional consideration is given to the potential value associated with an STR-operator being able to use their own

property (which would not be possible with a long-term renter), and the benefit that STR operation bestows by avoiding

risks and lost revenue associated with evicting poor or even non-paying tenants. Based on the initial break-even

numbers and this additional consideration, 60 nights is considered a reasonable threshold when evaluating a potential

property investor's decision to rent as a STR or long-term rental.

STR activity is often seasonal and few properties book up consistently each month and throughout the year. Based on

Granicus’s analysis of an early 2023 sample of over 2,000 STRs throughout the entirety of the unincorporated San

Bernardino County, only about 35% booked more than 60 nights per year and only 22% booked more than 90 nights

per year. Furthermore, only 8% generated income of $25,000 or more per year and just under half (44%) generated

less than $5,000 per year.

However, an examination of the County’s transit occupancy tax data for fiscal year 2022/2023 (July 1, 2022 to June 30,

2023) indicates the East Desert region may contain a larger number and proportion of STRs that rent more than 60

nights per year compared to the Mountain region. For example, approximately 355 STRs reported more than 60 nights

of rentals in Joshua Tree compared to 214 in Big Bear City and 208 in Lake Arrowhead during the referenced timeframe.

In Joshua Tree, these 355 units represent roughly 9% of the entire housing market in Joshua Tree, while the 214 and

208 units in Big Bear City and Lake Arrowhead represent less than 2% of their respective housing markets. The number

of nights rented may be larger given that Airbnb and Vrbo data was not available by community.

Figure 19. Comparison of Long-term and Short-term Rents, Unincorporated Communities, 2024

Community

Long-term Rent (LTR)

Avg Daily Rate

for STR

# STR nights to equal

12-month LTR revenue

Median Rent

12-month Revenue

Big Bear City

$2,095

$25,140

$381

66

Lake Arrowhead

$2,500

$30,000

$427

70

Crestline

$1,950

$23,400

$257

91

Running Springs

$2,000

$24,000

$273

88

Homestead Valley

$2,200

$26,400

$257

103

Morongo Valley

$1,745

$20,940

$309

68

Joshua Tree

$2,000

$24,000

$315

76

Source: Granicus methodology (2023) applied to May 2024 data with median long-term rent from Zillow and average daily rate from AirDNA.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 26 of 37

CHANGES IN OCCUPANCY

Occupancy Rates in Unincorporated Communities

The US Census offers the most complete and authoritative datasets to determine whether short-term rental activity

was displacing long-term renters. The percentage of housing units in 2010

1

and 2022

2

were compared based on the

amount occupied by a property owner, occupied by a long-term renter, or unoccupied and vacant for use as a

vacation/2

nd

home. The term “vacant/2

nd

home” may also be known as “seasonal home” and represent homes that are

used periodically by the property owner and/or as short-term rentals, but are neither occupied by an owner as a primary

residence nor made available for long-term rental occupancy.

Communities with Increased Year-round Occupancy Trends

The housing market in the Mountain region, in terms of occupancy, is relatively similar between 2010 and 2022. Based

on the latest available data, in Big Bear City, the occupancy patterns were almost exactly the same when comparing

2010 and 2022. In Lake Arrowhead, the percentage of vacation/2

nd

homes is lower in 2022 (-7%) compared to 2010

while the percentages of owner- and renter-occupied units are up (+5% and+2%, respectively), indicating that

vacation/2

nd

homes were converted into year-round units. In Crestline, the percentage of vacation/2

nd

homes is much

lower in 2022 (-9%) compared to 2010 and the percentage of owner-occupied units is up (+8%), indicating that a portion

of vacation/2

nd

homes were converted into year-round owner-occupied units. In Running Springs, comparing 2022 and

2010, the percentages of vacation/2

nd

homes and renter-occupied units are nearly the same (-1% and -2%, respectively),

while the percentage of owner-occupied units is up (+6% and higher than any value since before 2010). Additionally, in

the East Desert region, the Morongo Valley community saw increases in rates of year-round occupancy and decreases

in rates of vacation/2

nd

homes. See Figure 20 for more details.

Communities with Dynamic Occupancy Trends

While occupancy patterns in Morongo Valley are similar to unincorporated Mountain communities (decreased seasonal

housing and increased year-round occupancy when comparing 2010 and 2022), occupancy patterns in the Homestead

Valley and Joshua Tree communities are more dynamic (see more details in Figure 21). Between 2010 and 2017,

attendance at Joshua Tree National Park doubled (see Figure 22) and, influenced by a combination of a lack of nearby

hotel accommodations and a decent supply of low cost housing (median home values in Joshua Tree hovered around

$110,000 in 2015), rates of vacation/2

nd

homes and long-term rental occupancy increased substantially. Rates of

vacation/2

nd

homes increased from 5% to 19% in Joshua Tree and from 23% to 33% in Homestead Valley between 2010

and 2017. The majority of these increases appears to have come from the long-term ownership housing stock, with

rates of long-term ownership occupancy decreasing from 61% to 38% in Joshua Tree and from 53% to 48% in

Homestead Valley between 2010 and 2017.

For unknown reasons, the rate of year-round rental occupants in Joshua Tree rose from 31% in 2010 to a historical high

of 45% in 2014. In 2015, this rate began to dip but stabilized at 39% through 2019. During the COVID Pandemic, this

rate dropped to 37% in 2020 and 34% in 2021. However, this rate was still above the rate in 2010 (baseline comparison

year that represents a time that was not influenced by STR activity). For 2022, the rate of year-round rental occupants

dropped to 26%, which is an 8% drop from the previous year, 5% below 2010, and a historic low for Joshua Tree. Rates

1

2010 is used as a base reference as this year represents a time when Airbnb’s service was still relatively unused based on its

lack of presence on Google Trend Index (submitted searches) and the minimal number of listings in the United States.

2

US Census American Community Survey, 2022 5-year data released December 7, 2023 is the latest available data, reflects a

time that was post-Pandemic, and includes data that incorporates the peak of the STR market.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 27 of 37

of year-round owner occupants rose from 40% to 47% between 2020 and 2022, reflecting the surging demand to live

in Joshua Tree during the COVID Pandemic.

Figure 20. Unincorporated Communities and Year-round Occupancy Trends, 2010 vs 2022

Vacation/2nd Homes Year-round Owner Year-round Renter

Unincorporated Mountain Communities

Unincorporated East Desert Communities

Source: US Census 2010 & 2022 5-Year American Community Survey; figures rounded and results subject to margin of error. Data available for census-

designated places. Not shown is the “Other” vacant category, which typically represents 3% to 6% and includes the following categorical reasons for vacancy:

foreclosure, personal/family reasons, legals proceedings, preparing to rent/sell, held for storage of furniture, needs or is currently being repaired/renovated,

intended for year-round occupancy but vacant for 6+ months (extended absence), specific use housing, abandoned or possibly condemned, and unknown.

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 28 of 37

Figure 21. Unincorporated Communities with Dynamic Occupancy Trends, 2010 to 2022

Source: US Census 2010 & 2011 through 2022 5-Year American Community Survey; figures rounded and results subject to margin of error. Data available for

census-designated places. “Other” represents “Vacant for other reasons” and includes the following categorical reasons for vacancy: foreclosure,

personal/family reasons, legals proceedings, preparing to rent/sell, held for storage of furniture, needs or is currently being repaired/renovated, intended for

year-round occupancy but vacant for 6+ months (extended absence), specific use housing, abandoned or possibly condemned, and unknown.

Figure 22. Joshua Tree National Park, Annual Attendance, 2010 to 2022

Source: National Park Service, as of 2022. In 2020, the Park was closed for approximately 2 months due to the COVID Pandemic.

While some of the drop in year-round rental occupancy in Joshua Tree may have come from the increase in ownership

occupancy, the data indicates that the long-term trend of rising rates of vacation/2

nd

homes (coinciding with the

increased numbers of STRs) is likely contributing pressures that reduce the supply of long-term housing. While the rates

of vacation/2

nd

homes only increased from 18% to 21% between 2019 and 2022, the overall year-round occupancy rate

Memo: Housing Element Program 4 | Summary of Short-term Rental Outreach and Study Findings

May 2024 • Page 29 of 37

for Joshua Tree is down from 92% in 2010 and 79% in 2019 to 73% in 2022. Prior to 2010, only 2% to 5% of all housing

units were recorded as vacation/2

nd

homes in the US Census.

In Homestead Valley, the overall year-round occupancy rate is 64% in 2022, which is slightly lower compared to 2019

(67%) and a bit lower than in 2010 (70%). However, the rate of vacation/2

nd

homes in Homestead Valley 2022 (26%) is

essentially unchanged from 2019, is substantially lower than rates between 2014 and 2017 (high of 35%), and is only

marginally higher than rates in 2010 (23%).

CHANGES IN VACANCY

Non-seasonal Vacancy Rates in Unincorporated Communities

US Census data was used to evaluate the long-term trends of housing supply and demand based on the vacancy rate of

ownership and rental housing after excluding vacation/2

nd

(aka seasonal) homes. For example, to determine the non-

seasonal ownership vacancy rate, the number of non-seasonal vacant homes for sale was compared to the overall

supply of units available for long-term ownership occupancy (occupied ownership units plus non-seasonal vacant

homes for sale). Housing units that were vacant because they were vacation/2

nd

homes were excluded from the

equation. While vacation/2

nd

homes are part of the housing market and technically available for purchase or conversion

to long-term rental housing, they are being removed from the equation in this section of the analysis to understand

what the vacancy rate would be if vacation/2

nd

homes were not available to the housing market.

A balanced vacancy rate for a housing market is typically around 4% to 6% for ownership and 5% to 8% for rental units

3

.

Rental tenants tend to move more frequently and so a higher vacancy rate helps the market operate more efficiently.

Vacancy rates within these ranges can indicate that there are enough available properties to meet demand but not so

many that there is an oversupply of units. Vacancy rates that are higher than the top end of the range can indicate that

there is more supply than demand, which may lower housing prices as prospective buyers/renters have multiple options

from which to choose. Vacancy rates that are below the low end of the range can indicate and result in the opposite.

These ranges are general indicators and are most applicable to incorporated cities and towns that are near job markets

and have an abundance of public services and amenities. In areas that lack infrastructure for new development and are

far from job markets and amenities, a vacancy rate closer to the lower end of the range may simply indicate both low

demand and supply. This would only be the case, however, if housing prices and/or rents remained relatively stable. A

vacancy rate closer to or even above the higher end of the range, if accompanied by high prices/rents, can also reflect

a market where property owners are willing to let units sit unsold or vacant in pursuit of prices/rents that are not

affordable to much of the market. Accordingly, trends in vacancy rates are best evaluated as an indicator of housing

conditions in a comparison between communities within a region and between regions within the county.

Regional and Community Comparison

The long-term trend of non-seasonal ownership and rental vacancy rates for various incorporated and unincorporated

communities in San Bernardino County are illustrated in Figures 23 through 26. Comparing rates in the Mountain and

East Desert regions, the Mountain region communities generally display much higher non-seasonal vacancy rates—for