The views expressed in this paper are those of the authors and

do not necessarily represent the U.S. Bureau of Economic Analysis,

or the U.S. Department of Commerce.

BEA Working Paper Series, WP2024-1a

Capitalizing Data: Case Studies of Driving Records

and Vehicle Insurance Claims

Author

Contact

Date

Abstract

Keywords

JEL codes

Rachel Soloveichik, U.S. Bureau of Economic Analysis

April 2024

Early papers on capitalizing data focused on complex digital data that are

stored on supercomputers and managed by highly skilled computer scientists

(Statistics Canada 2019) (Eurostat 2020) (Coyle 2022) (Calderon and Rassier

2022) (Mitchell et al. 2022). This paper studies two very different types of

data: driving records and vehicle insurance claims. Like the tax forms and

individual credit reports studied in a previous paper (Soloveichik 2023), these

types of data are simple text records that can be stored on paper (U.S.

Women’s Bureau 1944) and managed by relatively unskilled workers (U.S.

Bureau of Labor Statistics 2022). Despite their simplicity, these two data

types are expensive to create. This paper estimates that driving records had a

creation cost of $229 billion in 2017 and vehicle insurance claims had a

creation cost of $153 billion in 2017.

Growth during the early 1990s changes noticeably when vehicle insurance

claims are tracked as long-lived intangible assets. Insurers started sharing

their claims data via the Comprehensive Loss Underwriting Exchange

database in 1992. This new data sharing increased the quality of vehicle

insurance claims data substantially and therefore increased real GDP growth

between 1989 and 1994 by 0.2 percentage point per year. Furthermore, the

real capital deepening associated with real data growth in the early 1990s

explains 0.2 percentage point of the 0.4 percentage point acceleration to

measured productivity in the late 1990s.

Data, driving, vehicle, insurance

D14, E01, and G14

2

Introduction

This paper studies two types of driving data: driving records and vehicle insurance claims. Driving

records report underlying risk factors like when an individual obtained their driving license, whether a

vehicle is currently licensed, whether a driver has citations for safety issues like speeding or drunk

driving, and whether their smartphone detects hard stops. In contrast, vehicle insurance claims report

outcomes like accidents or theft. Driving records are created by governments, individuals, lawyers,

insurance companies, and sometime employers, while vehicle insurance claims are only created by

insurance companies. Even though these two types of data are separate, they are often used together in

production. For example, a rideshare company might use both driving records and vehicle insurance

claims, along with other information like vehicle type and non-driving criminal record (Agan et al. 2022),

to decide whether an individual is eligible to drive for the rideshare company.

In recent years, national accountants have discussed including both long-lived purchased and long-lived

own-account data in gross domestic product (GDP) as intangible capital assets (Rassier et al. 2019)

(Eurostat 2020). This inclusion is a broadening of the current recommendation to only include long-lived

purchased data in GDP (United Nations Statistics 2008, sec. 10.112-10.114). Later sections of this paper

show that driving data are long-lived enough to be tracked as intangible assets in the national accounts.

This paper includes government driving data and private driving data (both digital and non-digital) in

GDP using a recently developed national accounting framework for data investment (Eurostat 2020).

At first glance, one might dismiss the driving data studied in this paper as valueless data exhaust. It is

certainly true that neither driving records nor vehicle insurance claims are the primary product of their

respective industries. But measured GDP includes many other products that are not the primary product

of their industries. For example, cow hides are included in GDP even though they are almost always a

byproduct of beef production rather than a primary product. Similarly, one might argue that neither the

driving records nor the vehicle insurance claims studied in this paper count as "data" because neither

are collected by data specialists. But measured GDP includes many other products that are produced by

non-specialists. For example, restaurant meals cooked by waiters who are filling in for absent chefs are

included in GDP together with restaurant meals cooked by trained chefs. Accordingly, this paper’s

inclusion of driving data in the broad category "data capital" is consistent with general national

accounting principles even if it is not consistent with some papers’ narrow focus on data that are

collected by data specialists as a primary product.

Tracking data as capital raises measured GDP because both private business investment and

government consumption of fixed capital are components of final output. In addition, personal

3

consumption expenditures (PCE) by category change when purchased consumer data are tracked

separately from purchases of other insurance industry output. Finally, household production changes

when consumer data creation and consumer durable services are included in the framework outlined in

the U.S. Bureau of Economic Analysis’ (BEA’s) existing household production satellite account (Bridgman

et al. 2022). This paper presents calculations that tracking these two types of data as intangible assets

increases measured GDP in 2017 by $128 billion and measured household production in 2017 by $160

billion. This GDP revision is smaller than the $383 billion GDP increase associated with private software

investment or the $438 billion GDP increase associated with private R&D—but it is not negligible.

Real creation of vehicle insurance claims data grew rapidly during the early 1990s. Before the

Comprehensive Loss and Underwriting Exchange (CLUE) was founded in 1992, claims data were kept in-

house and only used by one insurance company to price vehicle policies. After CLUE was founded, claims

data were shared broadly and used by multiple insurance companies, vehicle dealers (Huang et al.

2021), rideshare platforms (Boyle 2019), and employers (U.S. Department of Transportation 2023). In

other words, insurance claims data quality rose enormously when they switched from an asset with only

one user to an asset with many users. Furthermore, the stock of insurance claims data switched from

being owned by insurance companies to being owned by the driver described. Finally, claims data

services switched from being business asset services that are implicitly included in insurance industry

output to being consumer durable services that can be explicitly included in household production

(Bridgman et al. 2022). This paper demonstrates that this switch has important implications for

measured GDP, measured productivity, and measured household production.

This paper is divided into six sections. Section 1 describes the current and historical system in which

driving data are created, distributed, and used. Section 2 uses BEA’s published spending estimates,

arrest counts from the Federal Bureau of Investigation (FBI) Uniform Crime Report, and academic

research to value the driving records created each year. Section 3 uses industry literature and expert

opinion to value the vehicle insurance claims created each year. Section 4 presents revisions of nominal

GDP and nominal household production when these two types of data are included as intangible capital

assets. Section 5 presents price indexes for data and then uses those price indexes to recalculate overall

GDP prices, overall household production prices, real GDP, and real household production. Finally,

Section 6 presents revisions of private business productivity when both driving records and vehicle

insurance claims are included in the production accounts.

4

1. System of Data Creation, Sharing, and Usage

There are four main entities in the shared data system. First, there is a data creator that records risk

data and submits it to a data platform. Second, there is a data platform that organizes, audits, and

distributes data to a narrow list of specific users for a narrow list of permitted reasons. Third, there are

the data owners who distributed their data to whomever they please for whatever reason they please.

Finally, there is the data user. This section discusses each of the four main entities briefly.

Shared Data Creators

Driving records are created jointly by drivers, police officers, courts, and lawyers. To start out, both

drivers and vehicles require licenses before they are allowed on the road (Sheldon 2021) (Homer 2022).

Once on the road, police officers observe vehicles and decide whether to initiate a traffic stop. During

the traffic stop, the police officer and driver talk, and the police officer decides whether to write a ticket

for a minor safety violation like speeding and whether to make an arrest for a major safety violation like

drunk driving. After a driver is ticketed or arrested, they then face a decision. They can plead guilty

immediately or go to court to contest the ticket or arrest. If they choose to go to court, they may

represent themselves, use a court-appointed lawyer, or hire their own lawyer. Finally, the court decides

whether to convict or acquit the accused.

Driving records are imperfect measures of safety. Some drivers are denied licenses due to non-safety

factors like unpaid child support (Congressional Research Service 2011) or immigration status (Johnson

2004) (Amuedo-Dorantes et al. 2020). Similarly, some vehicles are denied licenses due to non-safety

factors like missing import records (U.S. Customs and Border Protection 2023). Conversely, many unsafe

drivers escape detection because enforcement resources are limited (Becker 1968), because some

police officers choose to be lenient (Goncalves and Mello 2023), or because some vulnerable groups are

disproportionately subject to traffic enforcement (Aggarwal et al. 2022) (Lofstrom et al. 2022). Innocent

people sometimes plead guilty because contesting a ticket or arrest may be too time consuming or too

stressful (Rakoff 2021), and guilty people sometimes have their citations dismissed because the police

officer does not show up in court (Desind 2015) or for other reasons. Nevertheless, meta-analyses find

that negative driving records are correlated with both general accident risk (Barraclough et al 2016) and

fatal accident risk (Slikboer et al. 2020). Because of these correlations, individuals without a valid U.S.

driving license have difficulty getting vehicle insurance (Brady and Glover 2023), and insurers routinely

charge higher premiums to drivers with bad driving records (Chiappori and Salanie 2000).

Vehicle claims data are created by insurers after an accident or theft is reported. Insurance companies

generally differentiate between claims where the insured is at fault and claims where the insured is not

5

at fault (Shuldiner 1968) (ChoicePoint Asset Company 2001). As a result, the exact same payment may

have different implications for future premiums depending on who is judged to be at fault. Conversely,

insurance companies often record a claim even if the assessed damage is below the deductible and

therefore no money is paid out (Mancusi 2018) and may even record a claim when a client asks about

the claim-filing process but does not actually file a claim (Marte 2014).

Insurance customers know that shared vehicle claims data are bundled with other insurance services. To

start out, both insurance applicants and individuals who apply for driving jobs are generally asked

specific questions about their claims data (Megna and Kasperowicz 2023) (Rogers 2023). In addition,

popular financial advisors tell Americans that filing a claim raises future insurance premiums (Shuldiner

1968) (Quinn 2009) and may reduce the likelihood of being hired for jobs that involve driving (Boyle

2019). Based on these facts, shared vehicle claims data are clearly not an externality under the official

guidelines for national accounting (United Nations 2008, sec. 3.92). This paper tracks shared vehicle

claims as purchased data creation services that are bundled together with other insurance services.

Tracking shared data creation does not change total output for insurers. Instead, insurance output is

split into two components: data creation and other insurance services.

Vehicle claims data are sometimes inaccurate. Minor accidents like parking lot scratches are often

handled unofficially without either party reporting the accident to their insurance company (Vallet and

McCormick 2023). Individuals involved in an accident often misreport key facts in the hope of getting a

larger payout (Crocker and Tennyson 2002). Conversely, insurance companies sometimes may

misinterpret their policies to deny potentially legitimate claims (Richmond 1994). Nevertheless, the

same meta-analyses cited earlier to demonstrate that driving records are correlated with accident risk

also find that prior vehicle insurance claims are correlated with accident risk (Barraclough et al 2016)

(Slikboer et al. 2020). This paper calculates a value for the sometimes inaccurate claims data that do

exist rather than a hypothetical value for the perfectly accurate claims data that do not exist.

Shared Data Platforms

Data platforms have four data jobs. First, they organize the scattered data supplied by separate data

creators into a combined file. Second, they audit the combined file for problems that must be resolved.

Third, they store the combined file for future reference. Finally, they distribute the combined file to any

entity with a valid request. In addition to these four data jobs, data platforms sometimes sell additional

services. These additional services may be important sources of revenue—but they are not directly

related to the driving data system.

6

Data platforms are small relative to the value of the data they hold. This paper estimates that the total

budget of all departments of motor vehicles in the United States was only $16 billion in 2017. Similarly,

the global RelX group, which owns CLUE and other data systems, earned only £1.6 billion from their

North American Risk & Business Analytics division in 2017 (RelX 2017). Their small size is possible

because data supplied to data platforms are already formatted by data creators (American Association

of Motor Vehicle Administrators 2023). In addition, data creators are responsible for handling disputes

about potentially inaccurate information (Kasperowicz and Ohman 2022). Because data platforms are so

small and because data creation accounts for only a portion of their output, even a substantial change to

their output has little impact on this paper’s measures of data creation.

Shared Data Owners

Businesses and individuals can generally distribute their data to any entity they choose. In some cases,

the business or individual distributes the data directly. For example, used-car sellers might show a

potential buyer a Carfax report (Huang et al. 2021). In other cases, the business or individual authorizes

a platform to distribute data to a specified user. Direct distribution and authorized distribution have

similar economic impacts, so this paper does not distinguish between them. Because businesses and

individuals have so much control over their data, this paper treats them as the primary data owner.

Governments also distribute data to specific entities for specific uses. Examples of permitted driving-

record distribution include traffic stop investigations (LaFave 2004) and racial bias research (Lofstrom et

al. 2022). Examples of permitted insurance claims data distribution include collection of Medicare liens

for health care related to vehicle accidents (Helland and Kipperman 2011) and state insurance

regulation (Feinman 2015). Because governments have some control over data, this paper treats them

as partial data owners.

Partial ownership by multiple parties likely yields higher social welfare than either complete secrecy or

full sharing. On the one hand, driving data are used for many purposes and total output is higher when

data are distributed broadly. On the other hand, businesses and individuals value privacy and prefer

limited distribution of data (Acquisti et al. 2016). Each business and each individual have their own

desired level of privacy, and so it would be difficult for the government to set a data distribution level

that works for everyone. Governments resolve these contradictory preferences by distributing a

minimum amount of data for purposes that are believed to be important enough to override privacy

preferences. Businesses and individuals who desire less than the maximum amount of privacy can then

decide to distribute their data to any entity they choose.

7

“Free” distribution of data likely yields higher output than either selling data or keeping it in-house. Data

are nonrival and complementary to other data, and so their contribution to output is maximized when

they are shared broadly (Coyle 2022). Furthermore, broad sharing of data requires marginal prices for

data that may be too low to cover the cost of data creation (Coyle and Diepeveen 2022). In this respect,

data are similar to other products whose creation involves high fixed costs and low marginal costs.

Previous researchers have shown that government provision is one method to finance these products

(Samuelson 1954). That method is partially used to finance the creation of driving-record data. But

recent papers have shown that individual ownership is an alternative financing method that can

increase welfare (Jones and Tonetti 2020). That method is partially used to finance the creation of

driving-record data and almost entirely used to finance the creation of vehicle insurance claims data. In

particular, an individual can finance the creation of their own driving data, give those data for “free” to

any entity with a valid reason for its request, and then benefit when that entity uses those data to

provide services or employment to the data owner.

Shared Data Users

Governments use driving records constantly. Courts use driving records to determine whether an

individual should be fined for minor safety violations or imprisoned for major safety violations

(Gershowitz 2011). Departments of motor vehicles use driving records to determine whether an

individual’s driving license should be suspended (Johnston 1951). Finally, policymakers use both driving

records and vehicle insurance claims data to measure current road safety and suggest ways to improve

road safety in the future (Carey et al. 2020). This paper neither studies how each government agency

uses data in its operations nor studies whether government agencies could improve efficiency by using

data better (Harrington et al. 2023). Instead, it simply accepts that driving records are an important

production input. This paper assumes that the government share of data usage equals the government

share of data creation funding. This assumption is equivalent to treating driving records data created by

governments as intangible assets owned by governments.

Private businesses use driving data to make useful predictions (Farboodi and Veldkamp 2022). Insurers

use driving data to predict the likelihood of future insurance claims (Barraclough et al 2016) (Slikboer et

al. 2020), and car buyers use driving data to predict used-car quality (Chapman 2022). Employers are

required to check driving data for workers who regularly drive commercial vehicles on the job (U.S.

Department of Transportation 2023), and many employers also check driving data for other workers

who drive on the job (Rogers 2023). In addition, some employers use drunk-driving records, together

with non-driving criminal records, in their hiring decisions (Agan et al. 2022). Because driving data are

used for fewer purposes than the financial data studied in a previous paper (Soloveichik 2023), the

8

revisions to overall GDP shown in this paper are smaller than the revisions to overall GDP shown in that

paper. Nevertheless, driving data are an important production input, and tracking driving data changes

measured productivity for the insurance industry significantly and changes measured productivity for

other industries noticeably.

This paper assumes businesses that use driving data implicitly purchase those data from their owner.

These implicit data purchases are part of a bundled transaction. For example, a motor vehicle insurer

might offer special discounts to customers who share their insurance claims history, an employer might

offer all job applicants a regular position but also offer those job applicants who consent to have their

driving record checked an opportunity to apply for highly paid traveling sales positions, or an equipment

supplier might offer discounts on truck leases if a small-business owner shares their personal vehicle

insurance claims history. This paper is focused on tracking data, and so it adjusts all bundled

transactions to explicitly track both the value of data given to firms and the value that firms give in

return for those data. For customer data, this paper adjusts the value of purchased products upward

and business intermediate inputs upward to include the value of data provided by customers. In the

example given earlier, the insurance company’s sales would be adjusted upward to include value of the

special discounts given to customers who share their insurance claims history and the insurance

company’s intermediate inputs would be adjusted upward to include the value of data provided by

customers who share their claims history. These two adjustments add precisely the same amount to

output and intermediate inputs so that tracking customer data does not change measured business

value added. Similarly, this paper shifts the value of data provided by workers from labor compensation

to business intermediate inputs without changing measured gross operating surplus. In the example

given earlier, the value of the opportunity to apply for traveling sales positions is considered an implicit

payment for the data provided by job applicants. This implicit payment is shifted from labor

compensation to a payment for data provided by job applicants who consent to have their driving

history checked. Finally, this paper shifts the value of data provided by self-employed individuals from

general proprietors’ income to capital services from data without changing either measured business

value added or measured gross operating surplus. In the example given earlier, the discount on a truck

lease is considered an implicit payment for the data provided by the small-business owner. This implicit

payment is shifted from general proprietors’ income to a payment for the value of data provided by the

small-business owner. To be clear, all of these treatments only apply to data usage. The implicit

payments for data creation by insurers and other businesses were described in an earlier section.

This paper does not study vehicle ownership, driver risk taking, or other indirect behavior changes that

may be impacted by driving data. It is very common for individuals to consider their future insurance

costs when buying a vehicle. Forward-looking individuals may also consider the expected damage to

9

their driving record from speeding or driving drunk. Conversely, governments and insurers may

structure driving-data creation to influence current and future behavior. The combined impact of these

efforts is theoretically ambiguous and difficult to solve without a complete model of the entire

economy. For now, this paper only focuses on the direct impact of driving data.

Unshared Data: Driving Behavior and Vehicle Insurance Claims Before CLUE

The driving-behavior data system is much simpler than the system for shared data. Insurers currently

keep the driving-behavior data they collect in-house and use those data for their own purposes (Jin and

Vasserman 2021). Similarly, employers keep the driving-behavior data they collect in-house and use

those data for their own purposes (Overman 2014). Before CLUE started, vehicle claims were handled

similarly to driving-behavior data. The insurance company kept claims data in-house and used those

data for their own purposes. Unlike shared data, which are owned by the entity described, in-house data

are owned by the entity which holds them. In other words, the four main entities in the shared data

system are all combined in the unshared data system.

Because neither current driving-behavior data nor historical vehicle claims data are shared, they are not

implicitly bundled with other insurance services. Accordingly, including those data in measured GDP

increases measured output for the insurance industry and employers without any adjustment to their

primary output. Similarly, including data services in the production accounts increases measured capital

services for the insurance industry and employers without any adjustment to either output or other

inputs. This paper’s treatment of these in-house data is similar to other national accounting papers’

treatment of other types of in-house data (Coyle and Li 2021) (Mitchell et al. 2022).

Why Did Companies Start Sharing Claims Data?

One might think that data sharing benefits all insurance companies because each insurance company

benefits from access to more claims data. In other words, data are more valuable when they are

combined with other data (Coyle 2022). But the CLUE database is regulated by the 1970 Fair Credit

Reporting Act and individuals can get a copy of their CLUE report without charge (Girardin 2023). So,

insurance companies need not send claims data for their existing customers to access claims data for

new customers. Another possible explanation might be collusion. It is true that an antitrust literature

has argued that data sharing can facilitate collusion when market conditions are uncertain (Vives 1984)

(Raith 1996). However, this particular mechanism does not apply to the insurance industry because

regulators generally allow cooperative insurance rate setting even without data sharing (Eisenach 1985).

The remainder of this subsection will suggest alternative explanations for the existence of CLUE.

10

Data sharing may have benefited insurance companies by reducing customer churn. Expected accident

risk and therefore expected payouts are higher for individuals who have had accidents in the past

(Rubinstein 2023). When claims data are kept in-house , individuals with a recent accident often switch

insurers to avoid a premium increase (Cohen 2005). But when claims data are shared, competing

insurance companies quote a higher premium to individuals who have had an at-fault accident and

therefore decrease the incentive for those individuals to switch insurers. Of course, competing

insurance companies also quote a lower premium to individuals who have not had an at-fault accident

and therefore increase the incentive for those individuals to switch insurers. If individuals are loss

averse, then they will be more interested in switching carriers after a premium increase (Hoffman

2013)—and therefore the net impact of data sharing on customer churn is negative.

It is also possible that the CLUE database benefited insurers by deterring claims. It may be true that the

CLUE database is not widely known (Marte 2014), and therefore it is unlikely that ordinary customers

changed their claim filing behavior when their insurer joined the CLUE database. However, an unknown

but noticeable share of insurance claims are fraudulent (Brenton 1964) and some are even filed by

professionals who specialize in fraudulent claims (Emerson 1992). Those professionals may have quickly

learned about the CLUE and quickly changed their behavior in response.

In practice, the exact reason for the existence of CLUE does not matter to this paper. Instead, this paper

focuses on how CLUE impacts measured GDP and measured productivity. These empirical results are the

same regardless of why insurance companies chose to join CLUE in the early 1990s.

2. Valuing Driving-Record Creation

This paper focuses on data creation costs alone. Accordingly, it measures the cost of creating driving

records rather than the cost of actually learning how to drive. For example, time spent filling out

paperwork at the department of motor vehicles is included but not time spent practicing driving.

Measured investment would be much larger if human capital investment was included together with

data creation, but the qualitative trends shown in this paper would be similar. This paper also does not

study fines, fees, and other payments to the government associated with driving data. Measured

investment would be slightly larger if those payments were tracked as a tax on driving data, but the

qualitative trends shown in this paper would once again be similar.

This paper focuses on driving data, and so it only studies records related to driving. But the general ideas

developed in this section could apply to records related to other activities. For example, a business

11

license could be seen as a data asset owned by a small business. Or a civil citation for loud parties could

be seen as a data asset owned by the rental housing unit. The national accounting impact of those other

records is a topic for future research.

Licenses

Government spending on licenses is assumed to equal the total budgets of all the departments of motor

vehicles in the United States. Each state has its own department of motor vehicles and so government

spending is calculated by summing spending in each state. Information on government spending was

taken from publicly reported state budgets and other online sources. In total, the paper calculates that

governments spent $16 billion on licenses in 2017. This $16 billion includes driver's licenses, vehicle

licenses, and associated services.

Consumer spending on licenses is based on product line detail in the 2017 Economic Census. This paper

assumes that consumers attend drivers’ education courses to get certificates that are required to obtain

or keep a driver's license rather than to learn actual driving skilled. The Economic Census reports that

commercial and vocational schools earned $0.8 billion from drivers’ education courses. This $0.8 billion

includes classes for prospective drivers and also current drivers who are improving their skills.

Information on the revenue earned by public schools from sold drivers’ education courses was not

located. Similarly, information on the revenue earned by driving tutors or other businesses who do not

answer the Economic Census was not located. For now, this paper assumes that those two suppliers are

about equal in size to the businesses tracked in the Economic Census and consumers spent a total of

$1.6 billion on licenses in 2017.

Household production of licenses is based on the time spent obtaining a license. To start out, the initial

learners permit requires a visit to the department of motor vehicles and filling out paperwork. Including

travel time and waiting, this process requires about four hours of time from the prospective driver. Most

states also require a prospective driver to attend drivers’ education courses that involves more

paperwork. Finally, the prospective driver must visit the department of motor vehicles again and fill out

even more paperwork before they are granted a new license. Prospective drivers often fail either the

exam for their initial learner’s permit or the exam for their license, and so may be required to visit the

department of motor vehicles more than twice before they can obtain a new driver license (Greg’s

Driving School 2023). In addition, drivers under eighteen are required to bring a parent to fill out

paperwork at each department of motor vehicles visit and even drivers over eighteen drivers may need

a companion to transport them and the vehicle they will be using for their driving test. For now, this

paper assumes that each new driver’s license requires 80 hours of unpaid time. This paper also assumes

12

that individuals with a current driver’s licenses spend an average of 4 hours per year renewing either

their driver’s license or their vehicle licenses. This paper then multiplies that time by the hourly cost of

tax preparation (Soloveichik 2023) to calculate that household production was $57 billion in 2017.

This paper calculates government spending, consumer spending, and household time costs for every

year from 1929 onwards. Annual data on the number of licensed drivers is available from 1963 onwards

(Federal Highway Administration 2020). Between 1950 and 1963, this paper uses estimates of drivers for

select years and interpolates between those years (Federal Highway Administration 2022). Before 1950,

this paper uses information on the number of registered vehicles (Federal Highway Administration 2000)

and on state laws associated with driving (Federal Highway Administration 1997) to extrapolate the

number of licensed drivers back to 1929.

1

Finally, the paper multiplies that index of licensed drivers by

the cost index that will be developed in a later section to calculate annual data creation for each year.

Criminal Driving Citations

Government spending on criminal driving citations is calculated using a three-step procedure. First,

information on total spending on police, courts, and prisons is taken from NIPA table 3.15.5. Second, the

paper splits total spending between criminal data creation and other government functions. The share

of police time devoted to criminal law enforcement is used as a proxy to split both police and court

costs. In particular, information on the share of police time devoted to criminal law enforcement is

taken from recent studies of select police departments (Asher and Horowitz 2020). Similarly, the share

of prison time devoted to pre-trial detention is used as a proxy to split prison costs. Information on the

share of prison time devoted to pre-trial detention is calculated from 2017 U.S. Bureau of Justice

Statistics information on the share of incarcerated people in jails and the share of jailed individuals who

are in pre-trial detention (Maruschak and Minton 2020) (Zheng 2019). This paper then multiplies police

and court spending by the share of police time devoted to criminal law enforcement and multiplies

prison spending by the share of prison time devoted to pre-trial detention to get an estimate of

government spending on all criminal records. This paper assumes that all criminal records are long-lived

data—and therefore assigns 100 percent of government spending on criminal records to government

data investment. Police and court spending is then multiplied by the ratio of drunk-driving arrests to

total arrests,

2

as reported in the Uniform Crime Reports (U.S. Department of Justice 1933–2022), and

prison spending is then multiplied by the share of unconvicted jail inmates who are held for drunk-

1. States that did not require licenses are assumed to require neither government spending, consumer spending,

nor household production to become a legal driver. States that did not require a driving test are assumed to

require only half the resources to become a licensed driver.

2. Arrests for unspecified crimes that may or may not be driving related are dropped from the sample.

13

driving arrests (Greenfield 1988) (U.S. Department of Justice 1985). In 2017, this paper calculates that

governments created $12 billion of criminal driving citation data.

Consumer spending on criminal driving citations is calculated using a similar three-step process. First,

information on total legal output is taken from BEA’s estimates of gross output by industry. Second,

information on the share of lawyer revenue associated with criminal law services is taken from the

product line detail in the 2017 Economic Census. This criminal law share is then multiplied by legal

output to get an estimate of consumer spending on all criminal records. This estimate is then multiplied

by the same ratio of drunk-driving arrests to total arrests to estimate consumer spending of $2 billion on

legal services associated with criminal driving citations in 2017.

Household production of criminal driving citations is calculated based on time spent. To start out, the

initial arrest process requires an individual to accompany police officers to a station, answer questions,

and cooperate with relevant evidence collection. This process takes at least 2 hours (Devendorf 2021)

and may take longer. Some individuals are released immediately after arrest, and some individuals are

held until they can be bailed out or even until trial. Based on a one-time study of the jail population

(Greenfield 1988), this paper calculates that the average drunk-driving arrest required 16.5 hours in jail.

Finally, individuals are required to appear in court. Court appearances often require careful preparation

ahead of time and long waits on the day of the court appearance. Information on the time associated

with court appearances could not be located. For now, this paper assumes that each individual arrested

for drunk driving spends a total of 80 hours of effort dealing with their arrest. This paper then multiplies

that time by the hourly cost of tax preparation (Soloveichik 2023) to calculate that households spent $4

billion worth of effort managing criminal driving citations. This estimate of household production is

somewhat imprecise. On the one hand, costs would be lower if some of the time associated with an

arrest was considered short-term conflict resolution rather than long-term data creation. On the other

hand, costs would be higher if the paper accounted for the very small but nonzero number of deaths

associated with arrests (Edwards et al. 2019). For simplicity, this paper assumes these two adjustments

cancel out so that the total household creation of criminal driving data is $4 billion.

Noncriminal Driving Records

Government spending on noncriminal driving records is calculated similarly to criminal driving records.

The only difference is that accused individuals are almost never placed in pre-trial detention and

therefore prison costs are irrelevant. This paper calculates police and court spending by multiplying total

police and court spending with an estimate of the share of police time devoted to traffic (National

Highway Traffic Safety Administration 1975) and then subtracting the police time related to criminal

14

driving records that was estimated in an earlier subsection. The time share reported in that early study

is reasonably similar to share of police time devoted to noncriminal driving records in a recent study

(Asher and Horowitz 2020).

3

Between those two years with data, this paper uses the ratio of drunk-

driving arrests to total arrests to interpolate and extrapolate the share of police time devoted to

noncriminal driving records from 1929 to 2020. Based on those assumptions, the paper calculates that

government expenditures on noncriminal driving records were $41 billion in 2017.

Consumer spending on noncriminal driving records is calculated using a similar two-step process. First,

information on total legal output is taken from BEA’s estimates of gross output by industry. Vehicle

accidents account for three-quarters of personal injury legal fees (Anderson et al. 2010). This paper

assumes that lawyer fees are split evenly between plaintiffs and defendants, so that three-eighths of

civil law negligence services are associated with individuals suing insurers for damages associated with

vehicle accidents.

4

Information on the share of lawyer revenue associated with civil negligence law

services is taken from the 2017 Economic Census. This number is then multiplied by total legal output to

calculate that consumer expenditures on noncriminal driving records were $19 billion in 2017.

Household production of noncriminal driving records is calculated based on time spent. Based on a

Bureau of Justice Statistics survey, this paper calculates that Americans in 2017 had approximately 38

million encounters with police associated with noncriminal driving records (Langan et al. 2001).

5

This

paper assumes that each police encounter is associated with 80 hours of driver time. To be clear, the 80

hours of driver time includes much more time than just time spent talking to police offices during a

traffic stop. Drivers spend a lot of time watching for police vehicles and communicating with others on

how to avoid police vehicles (Yawman 1977) (Dube 2021). And drivers who receive documents from the

police must decide how to respond to those documents. This paper then multiplies that time by the

hourly cost of tax preparation to calculate an hourly time cost of $63 billion in 2017.

3. The category “responding to noncriminal calls” includes both driving accident responses and non-driving

responses. For now, this category is assumed to be distributed similarly to other police time.

4. It may be true that non-accident related traffic citations are common. But individuals rarely hire lawyers to fight

those citations. This paper assumes that expenditures on non-accident related traffic citations are only 1 percent

of expenditures on criminal citations.

5. This paper assumes that 10 percent of reports made by crime victims are for vehicle theft or other driving-

related crimes. Individuals who report two or more encounters with a police officer are assumed to have 2.5

encounters.

15

Driving-Behavior Data

Insurers, employers, and other entities started collecting data on driving behavior in the 1990s, and data

collection has grown steadily since then (Karapiperis et al. 2015). For example, rideshare companies

automatically monitor speed (Smialowski 2016) for the self-employed workers associated with their

platforms. Furthermore, modern programmers are using sophisticated techniques to summarize raw

telematics data into risk scores (Gao et al. 2022) that are much more predictive than the mileage based

scores suggested by early theorists (Vickrey 1968). Accordingly, including driving-behavior data has a

noticeable impact on total data creation in recent years but a minimal impact before the 2000s.

Expenditures per monitored driver are estimated from industry literature. Consumer monitoring costs

are taken from a recent academic paper which reported that data collection costs $70 per driver per

year (Jin and Vasserman 2019). On-the-job monitoring costs are taken from a Federal Motor Carrier

Safety Administration publication which estimated that data collection for commercial truck drivers

costs $419 per truck per year (Federal Register 2015). The higher annual cost for on-the-job data

monitoring is likely due to both more hours of data collection and more intensive data collection. To be

clear, the data collection costs shown here only apply to sophisticated electronic monitoring. Non-

electronic monitoring devices like paper logbooks or bumper stickers that ask other drivers to report

driver behavior are assumed to neither cost much nor produce much useful data—and therefore are

ignored. This paper then extrapolates the costs of electronic monitoring forward and backward using

BEA’s pre-existing price index for cellular services (NIPA table 2.4.5U, line 283).

Monitored drivers also suffer a disutility cost from the loss of privacy. The same academic paper that

reported consumer data collection costs of $70 per year also reported a consumer disutility cost of $186

per monitored driver per year (Jin and Vasserman 2019). Precise estimates of the on-the-job disutility

cost of monitoring were not located, but the industry literature suggests that workers who are

monitored on-the-job have a high disutility cost from the monitoring (Premack 2022). For now, this

paper assumes that the ratio of disutility costs to equipment costs is the same for workers as it is for

consumers. This paper also assumes that workers target a fixed level of utility during their work day, and

therefore respond to the disutility of monitored driving by reducing the quantity or quality of other

output (Thiel et al. 2021). In other words, the disutility of worker monitoring is ultimately borne by

businesses. This paper then uses the hourly cost of tax preparation (Soloveichik 2023) to extrapolate

those calculated disutility costs forward and backward.

Total data creation costs are calculated by multiplying monitoring costs with an estimate of the number

of drivers monitored. Information on the number of monitored consumer drivers is taken from a survey

16

which reported that the share of consumers purchasing usage-based insurance doubled from 8 percent

in 2016 to 16 percent in 2020 (JD Power 2022), an industry report which estimated that 1 million U.S.

drivers used Progressive Insurance’s Snapshot policies in 2013 (ABIresearch 2013),

6

and a survey which

reported that awareness of usage-based insurance grew from 10 percent of drivers in 2010 to 36

percent in 2013 (Yao 2018). Accordingly, this paper calculates that 21 million consumer drivers were

monitored in 2017. Information on the number of monitored working drivers was not located, but the

industry literature suggests that driver monitoring has been growing at 10 percent per year (Allied

Market Research 2022). The industry literature also suggests that the government mandate for truckers

to collect data increased monitoring in 2018 (Premack 2022). For now, this paper assumes that the share

of employees monitored on the job was 40 percentage points in 2017, grew to 50 percentage points in

2018, and grew 10 percent per year in all other years. BEA’s published statistics show that the total

number of workers was 160 million in 2017 (NIPA tables 6.5A-D and 6.7A-D) and 11.3 percent of jobs

involve at least some driving (Beede et al. 2017). Accordingly, this paper calculates that a total of 7

million workers were monitored on-the-job in 2017. This paper multiplies these two estimates of

monitored drivers by the cost of consumer driver monitoring and worker monitoring to calculate total

data creation costs of $15 billion in 2017.

3. Valuing Vehicle Insurance Claims

To the best of my knowledge, no academic paper has yet measured either data creation costs or service

flows from vehicle insurance claims alone. But the literature suggests that individuals who have both

driving records and vehicle insurance claims pay lower insurance premiums, sell their used cars quicker,

and earn higher incomes. This paper uses the standard capital formulas (Jorgenson 1963) to calculate

service flows from driving-record data. This paper then assumes that all service flows that are not

accounted as associated with driving-record data are from vehicle insurance claims and uses the

standard capital formulas (Jorgenson 1963) to calculate investment from those service flows.

Lower Insurance Premiums

Newly licensed drivers pay insurance premiums about 40 percent higher than otherwise similar drivers

with at least 5 years of experience (Rosanes 2023). These higher premiums cannot be explained by

driving experience, because recent immigrants are charged higher rates even if they have driving

experience in their prior country of residency (Rosanes 2023). Furthermore, previous research has

6. Progressive was an early leader in usage-based insurance, so they represented a large share of total driver data.

17

shown that new drivers do not have any hidden information about their accident probability (Chiappori

and Salanie 2000) (Cohen 2005) (Spindler et al. 2014). So, the higher premiums cannot be explained by

adverse selection. Instead, this paper assumes that the 40 percent premium discount received by

experienced drivers is an implicit payment for their many years of data. The 2017 Economic Census

reports that drivers paid a total of $263 billion in vehicle insurance premiums. This paper assumes that

the 82 percent of drivers licensed for more than 5 years all received 40 percent discounts for their 5 or

more years of driving data and the remaining 18 percent of drivers licensed received average discounts

of 15 percent for their 0 to 4 years of driving data. Hence, this paper calculates that driving data reduced

premiums by a total of $101 billion in 2017.

Insurers also offer other benefits to individuals with long driving-data histories. Vehicle insurers

sometimes allow parents with a good claims history to get discounts on their children’s insurance

(Chiappori and Salanie 2000) (Quinn 2009). Life insurers also offer discounts to individuals who have

good driving data (Cornelius 2022). Information on the capital services associated with other insurance

data usage was not located. For now, this paper assumes the services associated with parents sharing

their good claims history with their children are 10 percent of the services associated with individual

usage and the services associated with life insurance usage are 10 percent of the services associated

with individual vehicle insurance usage. Based on those assumptions, this paper assumes that driving

records and vehicle insurance claims combined to save drivers a total of $122 billion of insurance

premiums in 2017.

Faster Used-Car Sales

Used-vehicle sellers often use vehicle-history reports, which include both ownership history and any

vehicle insurance claims, to inform potential buyers about a vehicle’s condition (Routhier and Lanctot

2023). A recent academic paper demonstrated that used-vehicle sellers who posted free car history

reports sold their cars 6 days faster (Huang et al. 2021). That paper calculated that those faster sales

increased seller profits by $250 per vehicle.

7

This paper multiplies that $250 estimate by the 39.2 million

used-vehicle transactions that occurred in 2017 (James and Paul 2018) to calculate a total seller profit

increase of $10 billion in 2017.

7. This methodology could underestimate the value of vehicle history reports if some potential car buyers were

able to access vehicle history reports on their own.

18

Higher Worker Earnings

More than 10 percent of jobs involve at least some driving (Beede et al. 2017). Those jobs are often

restricted by law or employer choice to individuals with good driving records. For example, trucking

companies are required to check employee driving records (U.S. Department of Transportation 2023),

and major rideshare platforms require drivers to have held a U.S. license for at least 1 year and have a

good safety record (HyreCar 2020). Previous academic research has shown that undocumented

immigrants who become eligible for driver's licenses due to changes in state law earn around 2 to 3

percent more per year (Amuedo-Dorantes et al. 2020)

8

(Cho 2022).

9

On the one hand, this annual

increase is much smaller than the 9 percent increase in average hours worked for teenagers who

become eligible for driver's licenses due change in the state laws associated with drivers under 18 (Argys

et al. 2019),

10

the 37 percent average earnings increase associated with a taxi license applicant passing

their licensing exam (Kardja and Sundberg 2023), the $12,000 hypothetical earnings loss associated with

suspended licenses (Chien et al. 2022), or the 53 percent hiring rate reported by participants in a

program that helped individuals get their suspended license reinstated (Seidman Research Institute

2017). On the other hand, this annual increase is much larger than either the annual earnings decrease

associated with a suspended license (Pager et al. 2022) (Finlay et al 2023) or the annual cost of restoring

a suspended license (Sweeney et al. 2022).

11

For now, this paper will use the papers focusing on

immigrants because that population seems more representative of the general driving population than

either teenagers, potential taxi drivers, or individuals with suspended licenses. BEA’s published statistics

show that total worker earnings (labor compensation plus proprietors’ income) was $12 trillion in 2017.

Furthermore, U.S. Federal Highway Administration data show that approximately 85 percent of the total

adult population was licensed in 2017 (Federal Highway Administration 2020).

12

Hence, this paper

calculates that the total earnings increase associated with driving data ranges from $203 to $304 billion

[(2 to 3 percent) * ($11,940 billion) * (85 percent)]. This paper then takes the midpoint of that range,

$253 billion, as the earnings increase from driving data.

8. That paper studies the impact on employment, hours worked, and wages per hour separately for both men and

women. This paper combines the coefficients in table 2 to calculate earnings increase for each gender and then

multiplies by the earnings for each gender in table 1 to calculate an average impact.

9. Based on the results after 3 years shown in table A.1

10. Based on the employment decrease shown in table 3 and the hours increase shown in table 4.

11. Based on the $920 million debt and 1.133 million drivers suspended reported on page 5, it would cost $811 to

restore the typical suspended license. That paper does not report a mean length for suspension, but it says that 75

percent last more than 1 year and 33 percent last more than 5 years. Hence the annual cost is well under $800.

12. This 85 percent includes the small but nontrivial portion of licensed drivers who are uninsured (Kluender 2022).

19

At first glance, the $253 billion of higher earnings associated with driving data seem very large. This

paper calculates that reduced business costs from lower on-the-job vehicle insurance premiums

associated with driving data were only $11 billion in 2017. Even when workers' compensation and other

costs are included, total business costs associated with on-the-job accidents were only $39 billion in

2019 (Miller and McKnight 2021). However, accidents are only one cost associated with bad driving. Fuel

efficiency decreases when drivers speed (Friedman et al. 2009) and bad on-the-job driving may damage

a business’s brand (Rossi 2016). In addition, bad driving data can sometime indicate the presence of

conditions like attention deficit hyperactivity disorder (Chang et al. 2015) or alcohol dependence

(Hingson and Winter 2003) that can be associated with non-driving problems at work. Hence, it is quite

plausible that the total costs correlated with bad driving records are sufficiently high that firms are

willing to pay workers $253 billion extra for their driving data.

To be clear, the $253 billion of increased earnings is not a precise measure of the benefits received by

newly licensed drivers. On the one hand, individuals with driving licenses work more hours (Amuedo-

Dorantes et al. 2020) and are more likely to commute to work by car (Cho 2022). These changes all

impose a cost on households that partially offset the increased earnings. On the other hand, some types

of consumption are associated with driving data. For example, people who live far away from a grocery

store may need a driver’s license to obtain fresh fruit (Economic Research Service 2009), and people

who want to rent a vehicle may need good driving data (Murphy 1994). Similarly, some types of

recreation are associated with driving data. For example, older adults who stop driving report higher

levels of social isolation (Qin et al. 2020). For simplicity, this paper assumes that the household costs

associated with higher earnings are equal to the consumption benefits and recreation benefits.

Accordingly, this paper will use the $253 billion figure without adjustment.

Calculating Vehicle Insurance Claim Creation

In total, this paper calculates that driving data yielded $374 billion (122+10+253-11) of benefits to

individuals in 2017. This paper then calculates

13

that driving records yielded $65 billion of shared data

services to governments, $206 billion of shared data services to individuals, $7 billion of in-house data

services to insurers, and $4 billion of in-house data services to businesses. Hence, this paper calculates

that the vehicle insurance claims yielded $168 billion (374–206) of shared data services in 2017.

13. Government capital services are assumed to equal to consumption of fixed capital (BEA 2022), and private

capital services are assumed to consumption of fixed capital plus a return on the capital stock (Jorgenson 1963).

Both government capital and private capital are calculated using the perpetual inventory method and the

depreciation rates that will be discussed in section 5. The rate of return on private capital is also discussed in that

section.

20

This paper then uses the standard capital service formula and a standard 7 percent real rate of return

(Jorda et al. 2019) to calculate that $153 billion of claims data were created in 2017.

At first glance, $153 billion of claims data creation appears implausibly large. After all, NIPA table 2.4.5U

shows that consumers only received $73 billion of vehicle insurance services in 2017. However, those

$73 billion of consumer vehicle insurance services are calculated based on net premiums (gross

premiums less expected insurance claims) (BEA 2022). In other words, the same vehicle insurance claims

that generate the claims data studied in this section are not even included in BEA’s current measures of

insurance industry output. The 2017 Economic Census reports that vehicle insurers collected a total of

$263 billion of gross premiums. This paper tracks those gross premiums as total industry output and also

tracks costs associated with insurance claims (repairs, medical care, and so on) as intermediate inputs.

The increased value of insurance industry output associated with using gross premiums rather than net

is approximately equal to the value of the newly tracked claims data. As a result, this paper does not

change non-data insurance industry output much.

Information on claims data creations costs for years other than 2017 could not be located. For now, this

paper extrapolates costs using incurred losses as a proxy. To be clear, only a portion of incurred losses

create useful data and some data are created without any associated losses. Nevertheless, incurred

losses are generally associated with claims data, and so are a reasonable proxy in the absence of better

information. First the paper collected data on aggregate incurred losses from the Insurance Industry

Factbook (Insurance Information Institute 2008, 2012, 2013, 2015, 2017 and 2021). Consistent

information on aggregate incurred losses before 1997 could not be located. Accordingly, this paper uses

a periodic Illinois government report comparing the state loss ratio with the national loss ratio (Clark

2003) (Shapiro 1999), an academic paper on automobile liability losses (Derrig and Tennyson 2008), a

GAO report giving the average loss ratio for a selected sample of insurers between 1978 and 1987

(Posner 1989), and the Historical Statistics of the United States: Colonial Times to 1970 (U.S. Department

of Commerce 1975). Gross premiums are reported in the Statistical Abstract of the United States (U.S.

Census Bureau 2011, 2005, 2001, 1993, 1986, 1984, 1980, 1977, and 1970) and the Historical Statistics

of the United States: Colonial Times to 1970 (U.S. Department of Commerce 1975). Between years with

information on average losses, the ratio of PCE net vehicle insurance premiums to private passenger

premiums is used as an interpolator.

21

4. Nominal GDP and Nominal Household Production

This section tracks five separate intangible assets: licenses, criminal driving citations, noncriminal driving

citations, driving behavior, and vehicle insurance claims. All five intangible assets combine digital and

non-digital data together. Digital and non-digital data are combined for both practical and theoretical

reasons. Practically, reliable information splitting digital data and non-digital data was not located.

Theoretically, the storage method has little impact on data production, data depreciation, or data usage.

Accordingly, splitting digital driving data and non-digital driving data would add measurement

complexity without changing anything theoretically important. Readers might worry that combining

digital and non-digital data conflicts with the official guidelines' focus on computerized data (United

Nations 2008, sec. 10.109). However, national accountants studying the digital economy routinely

include similar non-digital products in their analysis. For example, BEA’s digital economy satellite

account includes television programs throughout the entire time period studied (Highfill and Surfield

2022) even though television in the United States remained analog for several years after the digital

economy satellite account started (Cole 2009). Similarly, previous BEA research on specific data-related

activities does not distinguish between activities that create digital data and activities that create non-

digital data (Calderon and Rassier 2022) (Soloveichik 2023). Hence, this paper’s treatment of non-digital

driving records and non-digital claims data does not conflict with national accounting practices even if it

is inconsistent with the official guidelines.

Figure 1. Data Creation Relative to Nominal GDP

22

Figure 1 shows that the total ratio of driving-data creation to overall GDP has hovered around 2 percent

from 1980 onward. This ratio is smaller than the 5 percent ratio of data creation to overall GDP found in

an earlier paper that studied financial data (Soloveichik 2023). Nevertheless, it is still a noticeable

amount of data that has the potential to change the economy. The remainder of the paper will discuss

how measured GDP growth, measured household, and measured total factor productivity (TFP) growth

change when driving data are included.

Current Accounting for Data Creation by Sector

Private business expenditures on driving data do not currently impact measures of GDP that are based

on industry value added, because driving data are not considered final output. If data creation services

are purchased from a specialist firm, they are included as output of the producing company and

intermediate input for the purchasing company. This increase to value added for the producing

company is precisely canceled out by the decrease to value added for the purchasing company so that

sales of private business data creation services to businesses have no net impact on total value added

(just as any other intermediate input). In currently published statistics, own-account data creation by

businesses is not included as either output or intermediate input and therefore does not directly impact

any industry’s value added in official BEA statistics. Similarly, private business data do not directly

impact measures of GDP that are based on final demand.

Government and nonprofit expenditures on data creation do impact measures of GDP. For those

sectors, BEA measures output (and implicitly value added) based on costs rather than market revenue.

Wages for workers who create driving data are included in total labor costs and therefore implicitly

included in measured value added of the government or non-profit entity producing data. Furthermore,

a government purchase of driving-data creation services from a private business raises measured value-

added for the private business without lowering measured value-added for the government.

Consumer purchases of insurance data creation services are already included in measured GDP. Driving

schools explicitly sell certificate creation services to consumers, and law firms explicitly sell driving-

record creation services to consumers. In addition, insurance firms implicitly bundle claims data creation

services together with their primary insurance services. As a result, consumer purchases of insurance

data creation services are currently included in PCE. Household data production is not included in

measured GDP.

23

Proposed Accounting for Data Creation and Data Ownership by Sector

This paper proposes to track all data as intangible capital assets. This treatment raises measured

business output by the newly included data investment and raises measured government output by the

newly included depreciation on data capital. Consumer purchases of data are already included in final

output as a component of PCE. To avoid double-counting, this paper shifts those purchases from PCE

services to PCE consumer durables without changing nominal GDP at all. Household data production and

the services from consumer data are included in household production but not in GDP.

The paper assigns initial ownership of data to the sector that funded their creation. Governments

account for a noticeable share of driving record creation, so they are treated as owning a portion of

driving-record data. Consumers own both the portions of driving data created by businesses on behalf of

consumers and the portions of driving data created by consumers themselves. Similarly, businesses own

both the portions of driving data that are created by businesses on behalf of other businesses or by the

businesses themselves. Consumer driving-behavior data are an insurance industry asset, and worker

driving-behavior data are an asset of the firm that hires the workers. Finally, in-house insurance claims

data are treated as an insurance industry asset.

Data are often transferred from consumers to businesses. For example, a young adult might build a

good driving history by using their personal vehicle responsibly and later use that good driving record to

get insurance on their business vehicle. This is treated as a negative purchase of consumer durables and

a positive business investment. The converse situation, where businesses fund the creation of driving

data that are used by consumers, is very rare. Consistent with the asymmetric transfers from consumers

to businesses, insurance industry statistics show the CLUE database was associated with a reduction in

the commercial share of the vehicle insurance industry, from 16 percent in 1990 to 11 percent in 1999

(U.S. Census Bureau 2002). Therefore, neither labor compensation nor proprietors’ income are adjusted

for on-the-job data creation.

24

Revisions to Nominal GDP Associated With Driving Data

Figure 2. Revisions to Nominal GDP From Capitalizing In-House Data

Figure 3. Revisions to Nominal GDP From Capitalizing Shared Data

25

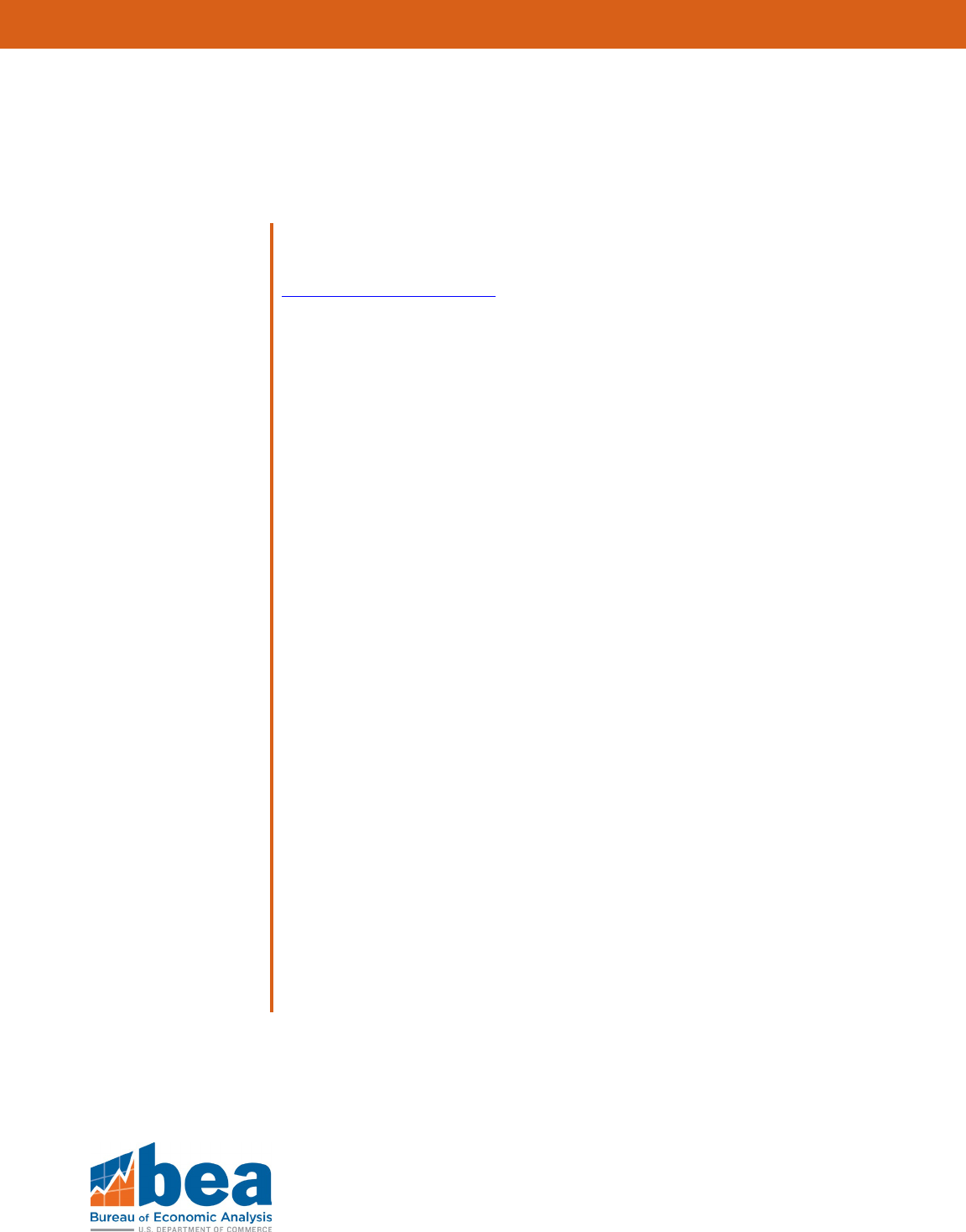

Figures 2 and 3 show that vehicle insurance claims suddenly switched from being in-house data to being

shared data. To remind readers, this switch is due to the introduction of the CLUE system in the early

1990s. Interestingly, in-house claims data have a larger GDP impact than shared claims data. The

difference can be explained by the treatment of claims data associated with consumer vehicle policies.

When claims data are owned by businesses, data creation is included in GDP without any compensating

adjustments. But when claims data are owned by consumers, data creation is exactly offset by a

downward revision to PCE services.

Figures 2 and 3 also show that capitalizing data raises the level of nominal GDP in every year studied. It

may be true that some shared data were already counted in measured personal consumption

expenditures or measured government consumption and were therefore already part of GDP. However,

neither the in-house data shown in figure 2 nor the portion of the shared data shown in figure 3 that are

business assets were ever included in measured consumption. Accordingly, capitalizing driving data

increases private-sector output by the value of business investment in driving data. In addition,

government output increases by the consumption of fixed capital associated with government-owned

driving records.

Depreciation Rates, Capital Stock, and Capital Services Associated With Driving Data

Each type of driving data has its own depreciation rate. Licenses require regular renewal (Insurance

Institute for Highway Safety 2023) but the renewal process is typically straightforward and generally

requires only one visit to the department of motor vehicles (Hawley 2023). This paper assumes that

licenses depreciate at 5 percent per year. Criminal driving citations can impact insurance rates for up to

10 years (Gusner and Tilford 2023), so this paper assumes that they depreciate at 10 percent per year.

The 1970 Fair Credit Reporting Act mandated that noncriminal driving citations (Spencer 2020) and

shared claims data be deleted after 7 years (Masterson and Metz 2022). This paper uses an adjusted

version of the one-hoss shay (Diewert 2004) to calculate an annual depreciation rate of 31 percent for

noncriminal driving citations and shared claims data. To be clear, academic research has shown that

claims data predict accident risk for many years (Rubinstein 2023), and so the 31 percent depreciation

rate used in this paper might decrease noticeably if a longer period before data deletion was allowed.

14

Neither current driving-behavior data nor historical vehicle claims data are regulated by the 1970 Fair

Credit Reporting Act—and therefore they have the potential to last longer than 7 years. However, both

14. Shared claims data were almost nonexistent before 1970, and so the reduced lifespan associated with the Fair

Credit Reporting Act had no impact on measured GDP or productivity. Noncriminal citations did exist before 1970,

but auto insurers then had just started using them to price policies and their initial formulas only looked at the

past three calendar years (Kiplinger 1968). Hence, these data were also unaffected by legal changes in 1970.

26

are kept in-house and therefore lose value whenever a consumer switches insurance carriers or a

worker switches jobs. The industry literature (Bendig 2023) and the academic literature (Cohen 2005)

suggest that consumers switch insurance carriers frequently and therefore data kept in-house

depreciates rapidly. For simplicity, this paper assumes that the reduced depreciation associated with

potential uses after 7 years cancels out the increased depreciation associated with switching so that in-

house data depreciates at the same 31 percent per year as shared claims data.

Government services from insurance data are assumed to equal depreciation (BEA 2022). Based on the

depreciation rates reported above and the assumed rate of return, this paper estimates that

governments receive services equal to 5 percent of their license data stock, 10 percent of their criminal

citation data stock, 31 percent of their noncriminal driving citation stock and 31 percent of their claims

data each year. Both business and consumer services from driving data are assumed to equal

government services plus a 7 percent rate of return based on the average real return for housing and

stocks over the past 150 years (Jorda et al. 2019).

15

However, there is one crucial difference between

business services and household services. When driving data are owned by insurers, data services are

implicitly included in GDP as part of insurance services. But when driving data are owned by consumers,

data services are explicitly included in household production as part of consumer durable services. All

else equal, a switch from in-house claims data to shared claimed data lowers nominal GDP growth.

Conceptually, this decrease in measured GDP is similar to the GDP drop that occurs when cooking or

cleaning time switches from the market sector to the household sector (Coyle 2015) (Bridgman 2023).

Revisions to Nominal Household Production Associated With Driving Data

Total consumer time devoted to driving-data creation was 2.3 billion hours in 2017. It is not obvious how

these 2.3 billion hours are recorded in the American Time Use Survey (U.S. Bureau of Labor Statistics

2023). Time spent helping a teenager obtain a license might be included in the 71 billion hours that

Americans spend on child or adult care. Time spent looking for police while driving or speaking to a

police officer during a traffic stop might be included in the 105 billion hours that American adults spend

in their private vehicles. Time spent paying a ticket might be included in the 2.6 billion hours that

Americans spend on financial management. Time spent obtaining a license for yourself or resolving a

traffic ticket might be included in the 0.1 billion hours that Americans spend obtaining licenses and

paying fines, fees, and taxes. Finally, time spent in police custody or in court might be included in the 0.2

billion hours that Americans spent on civic obligations and government services. Information on the

15. The calculations add general inflation and subtract data inflation to get a specific rate of return for driving data.

27

share of driving-record creation time that is currently included in household production could not be

located. This paper assumes that only 25 percent of driving-data creation time is currently included in

household production. In addition, this paper uses a specialist wage to value data creation time that is

higher than the generalist wage used to value other household production time. As a result, the value of

newly tracked data creation is much larger than the downward revision to other household production.

Figure 4. Revisions to Household Production From Data Creation

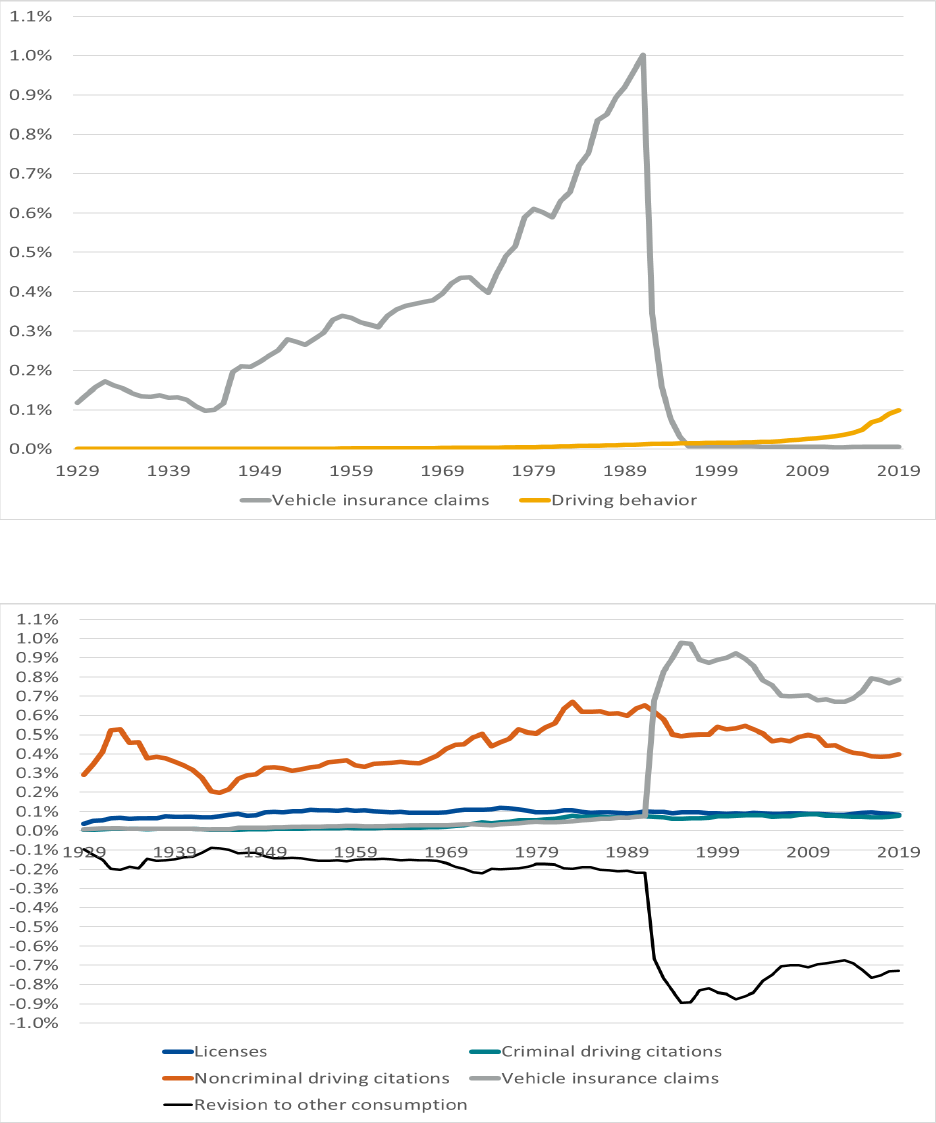

Figures 4 shows that driving data creation accounts for a growing share of household production. A

portion of this relative growth can be explained by growth in the average amount of time spent on

driving-data creation. For example, the number of speeding tickets issued per capita increased between

1946 and 2019. Another portion can be explained by the vehicle insurance claims data switching from a

business asset to a consumer durable in the 1990s. However, the lion’s share of this relative growth can

be explained by a decline in the share of time spent on other household production (Aguiar and Hurst

2007). As a result, a steady amount of time spent at the department of motor vehicles accounts for an

ever-growing share of household production.

28

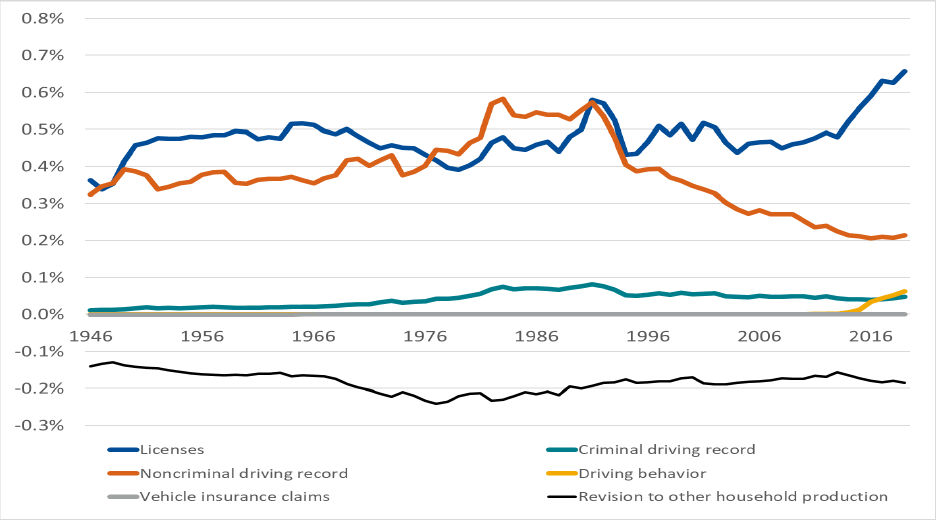

Figure 5. Revisions to Nominal Household Production From Data Services

Figure 5 also shows that driving data services have grown faster than overall household production. To

save space, the remainder of this paper combines household data creation with household data services

and discusses the two together.

5. Data Prices, Real GDP, and Real Household Production

This paper studies five types of driving data: licenses, criminal driving citations, noncriminal driving

citations, driving behavior, and vehicle insurance claims. All of these types except driving behavior can

be created without computers and stored on simple text files. As a result, digitization lowers their cost