NEW YORK CITY

MOBILE SERVICES

STUDY

Research Brief

Julie Menin

Commissioner

Bill de Blasio

Mayor

Consumer

Affairs

Bill de Blasio

Mayor

Julie Menin

Commissioner

© November 2015. New York City Department of Consumer Affairs.

All rights reserved.

The New York City Mobile Services Study was made possible through the collaboration of many partners.

We would like to thank Capital One and MetLife Foundation for their generous support, which allowed

the New York City Department of Consumer Affairs Office of Financial Empowerment (DCA OFE) to

commission this unique and timely research, and for their commitment to identifying how technology can

be used to support the financial empowerment of New Yorkers with low incomes.

Thank you to Anupa Bir and staff members from RTI International for conducting the quantitative and

qualitative research and producing a data visualization tool, which highlights key findings.

We thank the members of DCA OFE’s Mobile Advisory Council for their time, feedback, and vision for

the Study. Members include Lauren Aaronson, Grace Boehm, Daniel Delehanty, Elaine M. Divelbliss,

Keith Ernst, Katherine Hoffman, Phil Kim, Bill Maurer, Aaron Rieke, and Max Schmeiser. Special thanks

to Kathryn Glynn-Broderick.

We thank the Cities for Financial Empowerment (CFE) Fund, in particular staff members Kant Desai and

Katie Plat, for its continued partnership, its assistance with development and dissemination of the

materials, and its commitment to promoting the replication of this Study in other cities.

We would also like to recognize DCA staff members for their contributions to this report and related

materials, including Debra-Ellen Glickstein, Executive Director; Nicole Smith, Executive Deputy Director;

Monica Copeland, Senior Program Officer; and Kimberly Goulart, Senior Program Officer.

Last, we would like to thank the New Yorkers who shared information about their mobile financial

services usage, which provided insights for opportunities in mobile technology to help all New Yorkers.

DCA OFE Department of Consumer Affairs Office of Financial Empowerment

FDIC Federal Deposit Insurance Corporation

RTI RTI International

Mobile banking: Using a mobile phone to access a bank or credit union account. “Access”

includes using a web browser on a mobile phone to visit a bank or credit union web page, text

messaging, or using a mobile application (or “app”) downloaded to a mobile phone. This definition

comes from the Board of Governors of the Federal Reserve System.

Mobile financial management: Using a mobile phone to budget, track expenses, or help make

financial decisions. “Management” includes using a web browser on a mobile phone, text

messaging, or using an app downloaded to a mobile phone.

Mobile payments: Purchases, bill payments, charitable donations, payments to another person, or

any other payment transaction using a mobile phone. “Mobile payments” include using a web

browser on a mobile device to visit a bank or credit union web page, text messaging, or using an

app downloaded to a mobile device. Payments are applied to a phone bill, credit card, deducted

from a prepaid account, or withdrawn directly from a banking account.

As the use of mobile services grows within low-income communities and the disparity in access to

technology between low- and high-income earners (also known as the “digital divide”) closes, the

Department of Consumer Affairs Office of Financial Empowerment (DCA OFE) sought to better

understand the ways in which people use their phones to manage money. In June 2014, in partnership with

the Cities for Financial Empowerment (CFE) Fund and with the generous support of Capital One and the

MetLife Foundation, DCA OFE engaged RTI International, a nonprofit research organization, to design

and conduct a research project based on survey data from interviews with New Yorkers that DCA OFE

could use to help inform financial empowerment programming, product development, and future modes

of communication and engagement, in particular with New Yorkers with low incomes.

The New York City Mobile Services Study (“Study”) is the first attempt, at a local level, to rigorously

examine mobile banking and mobile phone ownership. The purpose of the Study was to analyze the needs,

barriers, and opportunities to increase financial inclusion through mobile financial services use. There is a

growing body of existing research on mobile phone usage for financial services, including several national

studies. For example, research conducted by the Pew Research Center documents consumer behaviors

related to the use of mobile devices to conduct banking activities. A 2013 study found that 51 percent of

adults in the United States bank online, and 32 percent of U.S. adults use their mobile phone

1

for banking

services. The Federal Deposit Insurance Corporation (FDIC) and the Board of Governors of the Federal

Reserve System have also conducted important research on the use of mobile financial services. This

Study, however, specifically examines mobile phone access, mobile banking usage, use of financial

management tools, and perceptions of privacy and data security among New York City residents. This

Study builds on prior research by highlighting some of the current behaviors and attitudes of New York

City residents regarding their mobile phones.

As New York City is a unique marketplace for mobile banking solutions, the Study findings highlight a

number of opportunities to leverage mobile phone platforms in support of financial empowerment goals,

as well as key concerns that New York City residents have when using mobile phones for their financial

transactions. In particular, the Study shows a strong consumer preference for low-risk, passive engagement

with financial accounts through mobile phones. That is, New York City respondents reported being more

comfortable receiving electronic messages and alerts as opposed to accessing an application that would

require entering new or sensitive data. The Study also suggests that if concerns about security can be

credibly addressed, preference for mobile payments may increase, given its convenience.

These insights can be used to facilitate local interventions and solutions targeted to New York City

residents, and can also inform solutions for residents of other cities across the country. Specific

recommendations directed at key stakeholders, such as state and local governments, the tech sector, and

nonprofit service providers are included at the end of the brief. The findings demonstrate there is room to

develop additional public-private partnerships, engage with consumers and help them better understand

mobile phone security, and ensure that consumer preferences and needs are reflected in mobile tools.

1

Pew Research Center, “51% of U.S. Adults Bank Online”:

http://www.pewinternet.org/files/old-media//Files/Reports/2013/PIP_OnlineBanking.pdf

RTI International, with guidance from DCA OFE and its Mobile Advisory Board, developed a survey

instrument to explore patterns of mobile financial service use. The instrument drew from other existing

surveys on the topic conducted recently by the Federal Reserve and the FDIC. The Study included an

online panel survey through GfK Knowledge Networks; 597 individuals submitted responses. To

supplement the sample from the panel and account for populations that were less likely to participate in

online panels, RTI and DCA OFE targeted additional recruitment efforts toward immigrants, those who

use alternative financial services, and older individuals. RTI and DCA OFE collected an additional 195

interviews in person at carefully selected field sites. An email targeted clients of DCA OFE and partner

services; this email sample resulted in 113 respondents. Finally, to probe some of the interesting findings

and add detail and context to the results, RTI conducted 30 qualitative interviews. In total, there were 935

respondents over a four-month data collection period.

Relative to national averages, ownership of mobile phones, including smartphones, was higher among

New York City survey respondents. Nearly all respondents (95.8 percent) reported owning a cell phone,

and 79 percent of cell phone owners had smartphones. In comparison, the Federal Reserve Board’s report

found that approximately 87 percent of American adults own a cell phone and 71 percent have a

smartphone

2

. Rates of smartphone ownership were particularly high among immigrant respondents, those

who are younger, and those with higher incomes, but even those with low incomes ($0/week) also had

high rates of smartphone usage (66.5 percent).

Use of mobile phones also differed between banked and unbanked respondents. Mobile phone and

smartphone ownership varied somewhat by banking status, as individuals without an account at a bank or

credit union (or the “unbanked”

3

) owned both mobile phones generally and smartphones specifically at

lower rates than those with bank accounts. The unbanked were more likely to share their mobile phones

than the banked and underbanked. The way in which respondents reported paying for their mobile phones

also differed across banking status: the banked were much more likely than the underbanked and

unbanked to report having a monthly contract for their phone, while the unbanked and the underbanked

reported using prepaid cell phones at much greater rates than the banked. Banked smartphone users were

more likely to have iPhones, while underbanked and unbanked smartphone users were more likely to have

Android phones.

2

Federal Reserve Board, “Consumers and Mobile Financial Services 2015”:

www.federalreserve.gov/econresdata/consumers-and-mobile-financial-services-report-201503.pdf

3

Someone who is “underbanked” has a bank or credit union account but also uses alternative financial services

such as a check cashing service, money order, payday loan, pawnshop loan, reloadable prepaid debit card, or

payroll card from an employer. Someone who is “banked” has a bank or credit union account (checking, savings,

or money market) and does not use alternative financial services.

Mobile banking is also more common among New York City residents (62.6 percent of respondents

reported using their phone for mobile financial services in the past 12 months).

Use of text and email alerts is greater than that of any other form of mobile financial services, with 69.6

percent of all respondents whose banks offer mobile banking reporting having received a text or email

alert from their bank in the past 12 months. As with mobile banking more broadly, the underbanked were

most likely to use text or email alerts (74.8 percent), and use of text and email alerts decreases as age

increases, ranging from 81.5 percent among those 18-29 to 50.3 percent among those over 60. Similarly,

immigrant respondents (75.4 percent) and those who are unemployed (73.1 percent) were more likely to

use text or email alerts as compared to the total sample average. The most commonly used text or email

alerts included statement available notifications, deposit/payment/withdrawal alerts, low balance alerts,

and fraud alerts.

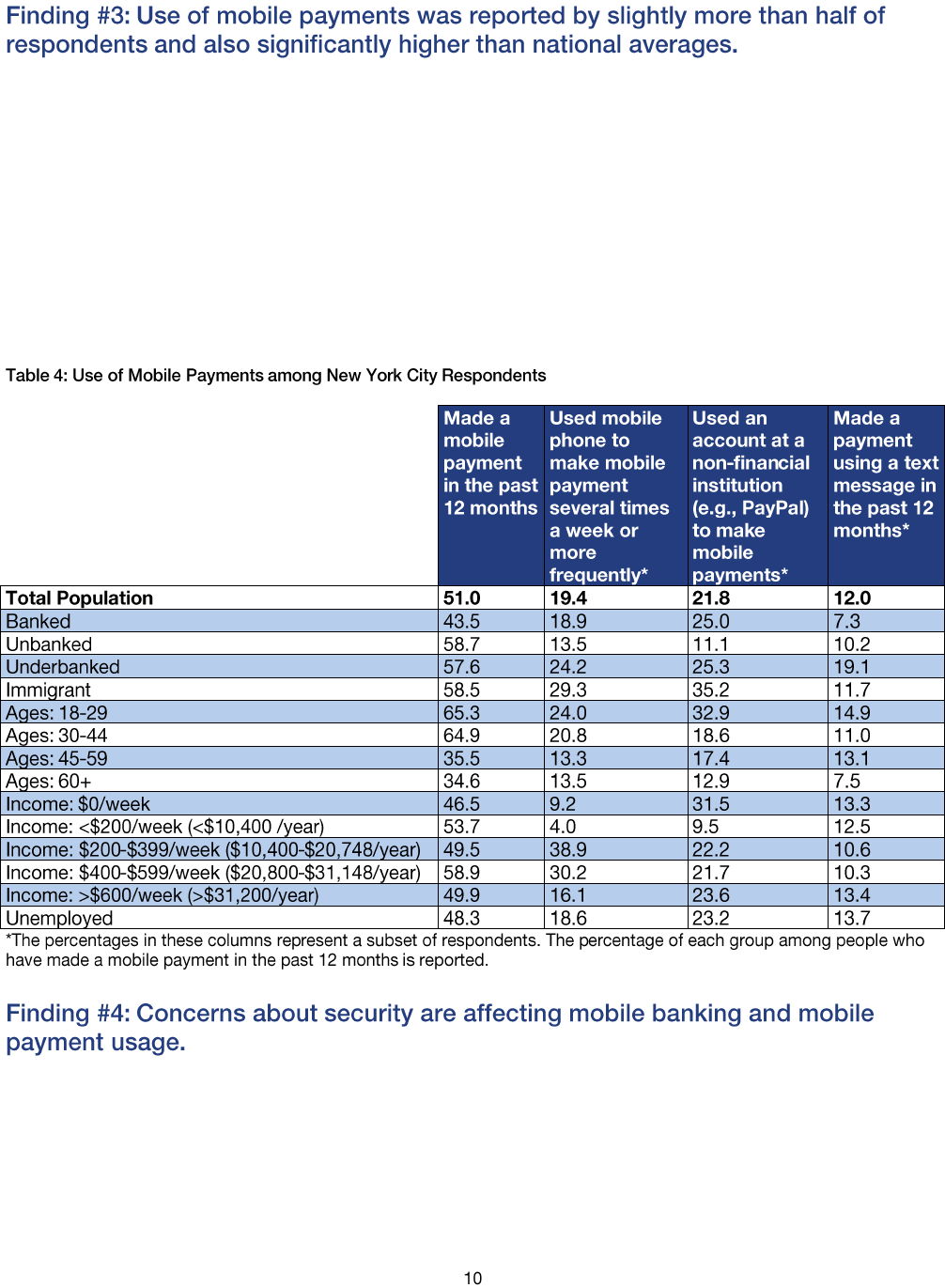

Use of mobile payments—any type of financial transaction using a mobile device drawing from some

established account—was reported by slightly more than half of respondents (51 percent). Again, New

York City proved an outlier against national averages—the rate of mobile payment usage reported in the

Study was more than double the national average found by the Federal Reserve (22 percent). Frequent use

of mobile payments (i.e., making a mobile payment several times a week or more) was less common,

reported by only 19.4 percent of respondents. Rates of frequent mobile payments were highest among the

underbanked (24.2 percent), immigrant respondents (29.3 percent), people ages 18-29 (24 percent), and

those with a weekly income of $200-$399 (38.9 percent). Payment by text was particularly uncommon

among all respondents (12 percent), though the underbanked (19.1 percent) and those ages 18-29

(14.9 percent) more commonly reported use than the overall sample.

The level of concern about the safety of personal information during mobile banking use was particularly

high among the unbanked, with 49.1 percent reporting that they believe personal information is somewhat

unsafe or very unsafe when they use mobile banking. Those ages 45 and older, and those making less than

$200/week, were also more likely to believe that personal information is very unsafe during mobile

banking. Overall, of those who do not use mobile financial services, 55 percent cite concerns about privacy

and data security as a significant barrier to usage and are particularly disinclined to use mobile phones for

payments or other transactions of sensitive data. Those who have adopted mobile banking use are most

likely to report having done so because of the convenience it offers, gaining access to mobile banking by

obtaining a smartphone, or gaining access to mobile banking when their bank began offering it.

As with mobile banking, the perception that mobile payments were not useful and security concerns were

the biggest barriers to mobile payment use. The most common reasons for adopting mobile payment use

were the same as those for adopting mobile banking use: convenience, gaining access to mobile banking by

obtaining a smartphone, or gaining access to mobile banking when their bank began offering it.

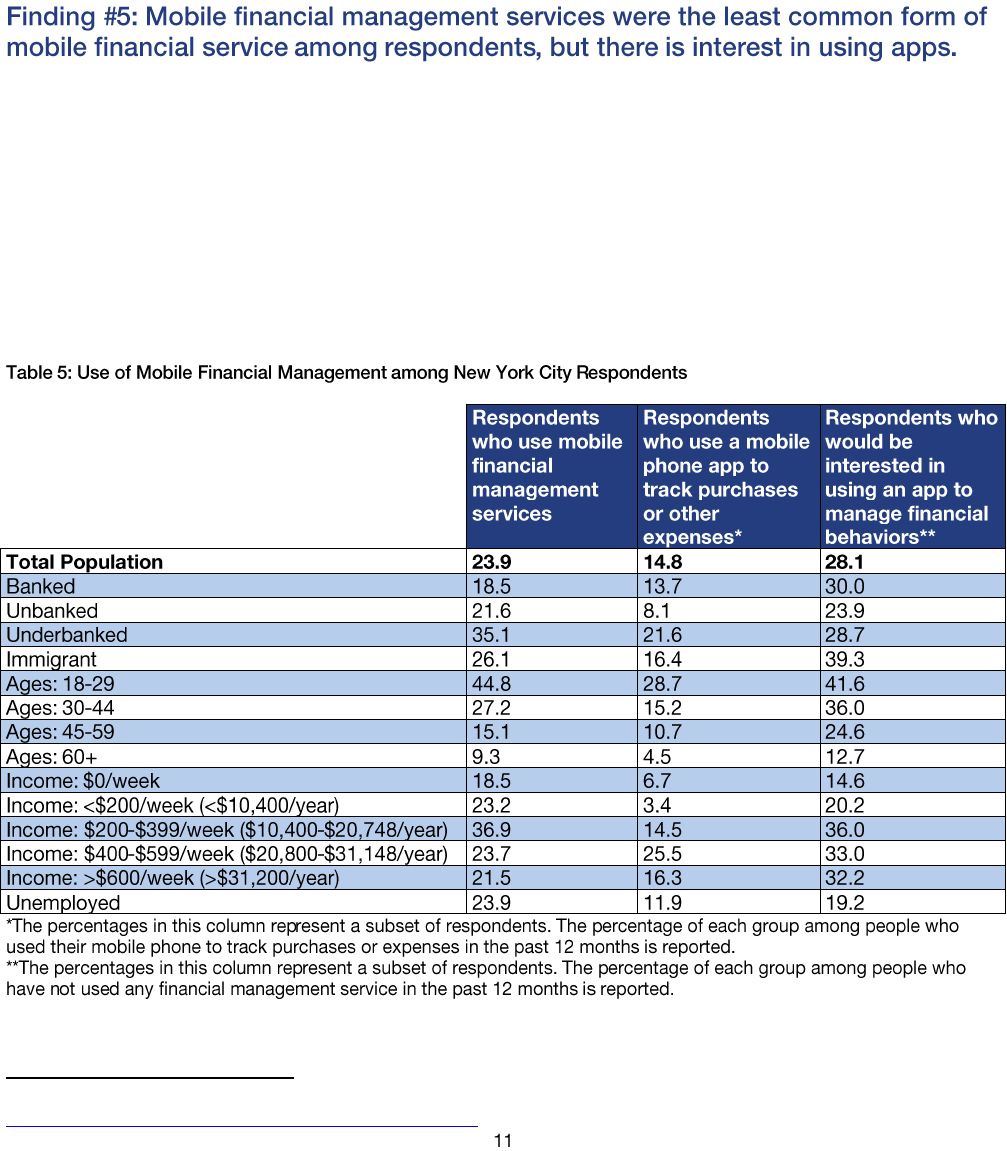

Mobile financial management services—i.e., online services to help consumers budget, track expenses, or

help make financial decisions—were the least common form of mobile financial services respondents

reported using (23.9 percent). This is especially interesting, given that investments in financial technology,

including mobile financial management services, are ballooning—a recent report

4

estimated $12 billion in

investments in 2014 alone. As with other forms of mobile financial services, the underbanked

(35.1 percent) and those ages 18-29 (44.8 percent) were more likely to report use. In spite of the low rates

of mobile financial management service use, stated interest in using an app to manage financial behaviors

was more common (28.1 percent), in particular among immigrant respondents (39.3 percent) and those

ages 18-29 (41.6 percent).

4

Accenture, “The Future of Fintech and Banking: Digitally disrupted or reimagined?”:

https://www.cbinsights.com/blog/fintech-and-banking-accenture/

DCA OFE conducted this Study to understand the potential impact that mobile technology can have on

expanding financial access, to guide programmatic and policy efforts of key New York City stakeholders in

the municipal financial empowerment and asset building fields, and to provide a model for other cities

across the country interested in leveraging mobile technology. With this in mind, the findings from the

Study point to a number of opportunities for local government agencies, nonprofit and community-based

organizations, and the financial and civic technology

5

sector to develop effective ways to engage residents

through mobile phones.

Armed with evidence that New Yorkers value the ability to receive important information via text and

email alerts, government agencies, for example, could focus their efforts on experimenting with different

messaging strategies to inform residents about city services and benefits. Already, the City of New York

uses Notify NYC to deliver information about emergency events and important City services via email,

phone, or Short Message Service/text. Registration is free; however, service providers may charge message

and data rates, so subscribers are encouraged to check with providers. With respect to financial services

and programs, government agencies can develop specific tools and strategies for groups identified with

high levels of mobile financial service engagement, such as younger adults (ages 18-29) or those who

are underbanked.

Government entities could also employ these unique data points to launch and expand public-private

partnerships that result in better products and services for mobile users. For example, DCA OFE might

explore working with developers or civic technology organizations to ensure that consumer preferences

for passive engagement and concerns about security are understood and included as a part of their

technology development. Similarly, government agencies can play an important role in helping consumers

understand mobile phone security and what to look for when sharing sensitive financial information. For

example, governments could develop materials and tip sheets to highlight the kind of security features

consumers should look for and how consumers can avoid mobile-related scams.

Nonprofits and community-based organizations often struggle to keep in touch with their clientele. The

findings, particularly passive engagement strategies, can support efforts to improve financial counseling

and education via mobile phone platforms and applications. Simple mobile interfaces could be developed

to provide appointment reminders or alerts when a client is reaching a spending or savings target. The use

of mobile alerts coupled with financial counseling can improve client engagement and retention, which is

key to improving financial outcomes. However, counselors will need training on increasing clients’

comfort levels with mobile technology and understanding the limits of clients’ mobile and data plans.

Given the relatively limited usage of, but interest in, financial management tools, counselors should work

closely with their clients, especially younger clients, to explore how clients might engage with these tools.

These findings have important implications for the financial technology, or “fintech,” sector. While

investments in fintech are ballooning—a recent report

6

estimated $12 billion in investments in 2014

alone—there has been limited research on specific consumer usage and preferences, especially among low-

income consumers. Although survey responses indicated that mobile financial management tools were not

5

“The emerging field of civic technology, or ‘Civic Tech,’ champions new digital platforms, open data, and collaboration tools for

transforming government service delivery and engagement with citizens.” GovLab, NYU Tandon School of Engineering, “The GovLab

Selected Readings on Civic Innovation: Cities and Civic Technology.” Posted on November 30, 2014:

http://thegovlab.org/civic-innovation-cities-and-civic-tech/

6

Accenture, “The Future of Fintech and Banking: Digitally disrupted or reimagined?”:

https://www.cbinsights.com/blog/fintech-and-banking-accenture/

currently being used at high rates by New Yorkers with low incomes, younger respondents appeared to

express the most interest in using these tools in the future. As this market continues to grow, a key

component of user adoption will be addressing security concerns and engaging target users in app

development to ensure that feature sets are useful and relevant.

This Study sought to establish an understanding of the level of access New Yorkers had to mobile phones

as well as to identify barriers and opportunities for managing money via phones. Survey respondents

reported a high level of mobile and smartphone usage compared to national averages, as well as a high

level of engagement with mobile banking and payments. Respondents demonstrated a strong consumer

preference for low-risk, passive engagement with their financial accounts through mobile phones.

Concerns about privacy and data security are real barriers for mobile financial service use, but if concerns

about security can be credibly addressed, preference for more active mobile engagement may increase,

given its convenience. In order to help increase the adoption of mobile financial service use, public-private

partnerships can be developed to address security and utility concerns.

This Study’s findings reveal the value of understanding the preferences of consumers at a local level and

how research can guide best practices. Other cities around the country can easily use this Study and its

toolkit as a model for how to gather data and to use findings to leverage mobile phone technology in an

optimal way to support goals. Collectively, the Study and toolkit will inform the development of relevant

programs, products, and modes of communication to better meet the needs of low-income consumers,

as well as contribute to current research in the area of mobile financial services.

RTI, with guidance from DCA OFE and its Mobile Advisory Board, developed a survey instrument to

explore patterns of mobile financial service use. The instrument drew from other existing surveys on the

topic conducted recently by the Federal Reserve and the FDIC, both of whom are represented on the

Mobile Advisory Board. English and Spanish versions of the survey were created. To access the

perspectives of a wide range of low- and moderate-income New Yorkers, the Study included an online

panel survey through GfK Knowledge Networks, using the part of their panel that qualified. Responses

were received from 597 of the 861 eligible respondents. To supplement the sample from the panel and

account for populations that were less likely to participate in such panels, RTI and DCA OFE targeted

additional recruitment efforts toward immigrants, the underbanked, and older individuals through the

following recruitment sites: the Consulate General of Mexico in New York City; BedStuy Campaign

Against Hunger food pantry in Brooklyn, NY; the Food Bank for New York City’s food pantry, soup

kitchen, and tax preparation site in Harlem, NY; and Good Shepherd Church food pantry in Inwood, NY.

An additional 195 interviews were collected in person at carefully selected field sites. An additional email

sample targeted clients of DCA OFE and partner services. This email method resulted in 113 (of 3,250)

respondents. Finally, to probe some of the interesting findings and add detail and context to our results,

we conducted 30 qualitative interviews. In total, responses were received from 935 respondents over a

four-month data collection period. These responses were weighted and are representative of the

population of New York City. However, particular attention was paid in this Study on the responses of

low- and moderate-income respondents.

RTI and DCA OFE also looked at other survey sample characteristics and how they compared to

the general population in New York City. For example, 48.7 percent of respondents are banked, meaning

they have a bank or credit union account and do not use alternative financial services;

22 percent of respondents are unbanked; and 29.3 percent of respondents are underbanked, meaning they

have a bank account but also use alternative financial services. Thirty-five (35) percent of respondents

speak a language other than English at home, and 10.2 percent completed the Spanish version of the

survey. The immigrant population in this Study consists of Spanish-speaking Mexican immigrants surveyed

at the Mexican consulate, meaning that this is not a representative sample of immigrants in New York

City.

See Table 6, Demographics of Sample, on page 15.