12703905

1

Consumer Checkpoint

The kids are alright (for now)

11 June 2024

Key takeaways

• Consumer spending momentum continues to appear soft but stable. According to Bank of America internal data, total card

spending per household was up 0.7% year-over-year (YoY) in May, following the 1.0% YoY increase in April.

• The gap between older and younger generations' spending growth has narrowed, which could reflect the fading impact of the

2023 cost-of-living adjustment (COLA) on social security benefits, alongside strong after-tax wage growth for younger cohorts.

• That said, Gen Z and younger Millennials' share of spending on discretionary items is declining potentially due to increasing

spending commitments as they get older. However, higher costs in non-discretionary services is also a headwind, in our view. To

counter these pressures we find some evidence that the younger generations are 'trading down' in grocery shopping and

restaurant decisions.

• The strength in the younger generations' labor market, including wages and salaries growth, has allowed a majority to navigate

these challenges, but there are signs of increased financial pressures for some.

Consumer Checkpoint is a regular publication from Bank of America Institute. It aims to provide a holistic and real-time estimate of US

consumers’ spending and their financial well-being, leveraging the depth and breadth of Bank of America proprietary data. Such data is not

intended to be reflective or indicative of, and should not be relied upon as, the results of operations, financial conditions or performance of

Bank of America.

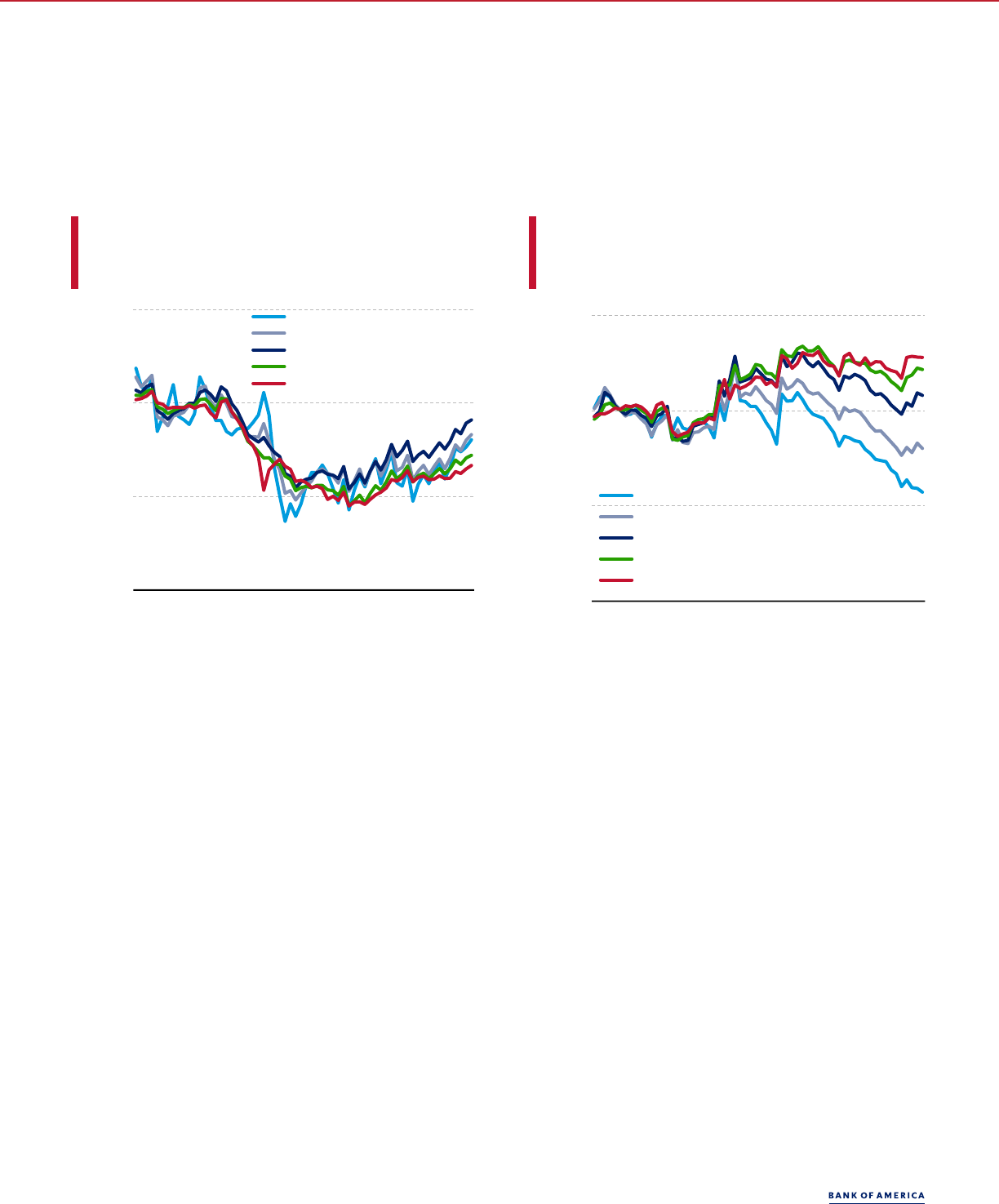

Spending has its generational differences

Bank of America aggregated credit and debit card spending per household rose 0.7% year-over-year (YoY) in May, following the

1.0% YoY rise in April. Exhibit 1 illustrates that overall consumer spending momentum has largely remained stable this year. In

May, retail spending growth, though still negative, reversed course to trend upwards, and while services spending growth eased

back in May, it remained positive. On a monthly seasonally-adjusted (SA) basis, total card spending per household fell 0.9%

month-over-month (MoM) in May, following the 1.3% MoM increase in April.

Exhibit 1: Bank of America credit and debit card spending per

household increased by 0.7% YoY in May

Total credit and debit card spending per household, based on Bank of

America card data (%YoY, monthly)

Source:

Bank of America internal data

BANK OF AMERICA INSTITUTE

Exhibit 2: Gen Z and Millennials account for around 30% of US

total consumer spending and 32% of households in 2022, while

Gen X produces 34% of spend with only 27% of households

Share of annual expenditure and share of households by generation

(2022, %)

Source:

Bureau of Labor Statistics (BLS)

BANK OF AMERICA INSTITUTE

-5%

0%

5%

10%

15%

20%

25%

Jan-22 Jun-22 Nov-22 Apr-23 Sep-23 Feb-24

Total

Services incl restaurants

Retail ex restaurants

Gen Z

Millennials

Gen X

Baby

Boomers

Traditionalist

Outer ring: Share

of spending

Inner ring: Share

of households

I NSTITUTE

Accessible version

2

11 June 2024

I NSTI TUTE

Who drives overall spending? According to data from the Bureau of Labor Statistics (BLS), the ‘younger generations’ – Gen Z and

Millennials together – accounted for around 32% of households and 30% of consumer expenditure as of 2022, while Gen X made

up only 27% of households, but accounted for around a third of spending. ‘Older generations’ – Baby Boomers and

Traditionalists – made up over 40% of households but were around 36% of spending.

Looking at Bank of America aggregated credit and debit card data, it appears there has been some slowdown in older

generations’ spending growth so far this year (Exhibit 3). As we discussed last October, (see:

Will silver spenders continue to

outpace the young?), older generations’ spending growth in 2023 was likely boosted by a large (8.7%) cost-of-living-adjustment

(COLA) in social security benefits. The 2024 COLA adjustment was a much smaller 3.2%, meaning that part of the spending

momentum from this source has likely waned.

Exhibit 3: In the past few months, older generations’ spending growth has begun to cool

Card spending per household by generation (monthly, %YoY)

Source:

Bank of America internal data

BANK OF AMERICA INSTITUTE

Interestingly, Gen X spending growth is not only the weakest of all the generations, but the only generation that saw negative

spending growth in May, which likely reflects both this cohort’s relatively weaker wage growth (Exhibit 5) compared to younger

generations, as well as higher costs in many recurring non-discretionary services, such as property insurance, commonly

associated with Gen X’s current life-stage. Conversely, the spending growth of Gen Z and Millennials appears to have picked up

in May. Their spending growth has tended to be weaker than older generations on services, but stronger in retail (Exhibit 4).

Exhibit 4: Among younger generations, retail spending growth is

beginning to rise while services spending growth is slowing

Card spending per household by generation (monthly, %YoY)

Source:

Bank of America internal data

Note:

Older generations include Traditionalists and

Baby Boomers. Younger generations include Gen Z and Millennials.

BANK OF AMERICA INSTITUTE

Exhibit 5: Millennials and Gen Z have experienced stronger wage

growth than older generations for the last four years

After-tax wage and salary growth by generation (3-month moving

average, %YoY)

Source:

Bank of America internal data

BANK OF AMERICA INSTITUTE

According to Bank of America consumer deposit data, we saw an easing in after-tax wage growth across all age cohorts in May

(Exhibit 5), but it remains to be seen if this is the start of a downward trend or noise; the May Bureau of Labor Statistics (BLS)

data actually showed a pick-up in hourly pay growth to 4.1% YoY from 3.9% YoY in April.

More broadly, the strong labor market has been a particular boon for the young in recent years, reflected in significantly stronger

after-tax wage growth for Gen Z and Millennials compared to other generations. While it does appear the degree of

outperformance of younger generations’ wage growth is past its peak, it remains significant. For example, the after-tax wage

-5%

0%

5%

10%

15%

20%

25%

Feb-22 Aug-22 Feb-23 Aug-23 Feb-24

Gen Z Millennials Gen X Baby Boomers Traditionalists

-10%

0%

10%

20%

30%

Feb-22 Jul-22 Dec-22 May-23 Oct-23 Mar-24

Retail ex restaurants (older)

Retail ex restaurants (younger)

Services incl restaurants (older)

Services incl restaurants (younger)

-5%

0%

5%

10%

15%

20%

25%

30%

Mar-19 Mar-20 Mar-21 Mar-22 Mar-23

Mar-2

Gen Z Millennials

Gen X Baby Boomers

11 June 2024

3

I NSTI TUTE

growth of Millennials was over 5 percentage points (pp) stronger than that of Gen X at the end of 2022, while in May 2024 this

gap was 1.5pp. For Gen Z households, strong wage growth is also partially a life-stage story due to growth from the younger

cohort within this generation entering the full-time labor market.

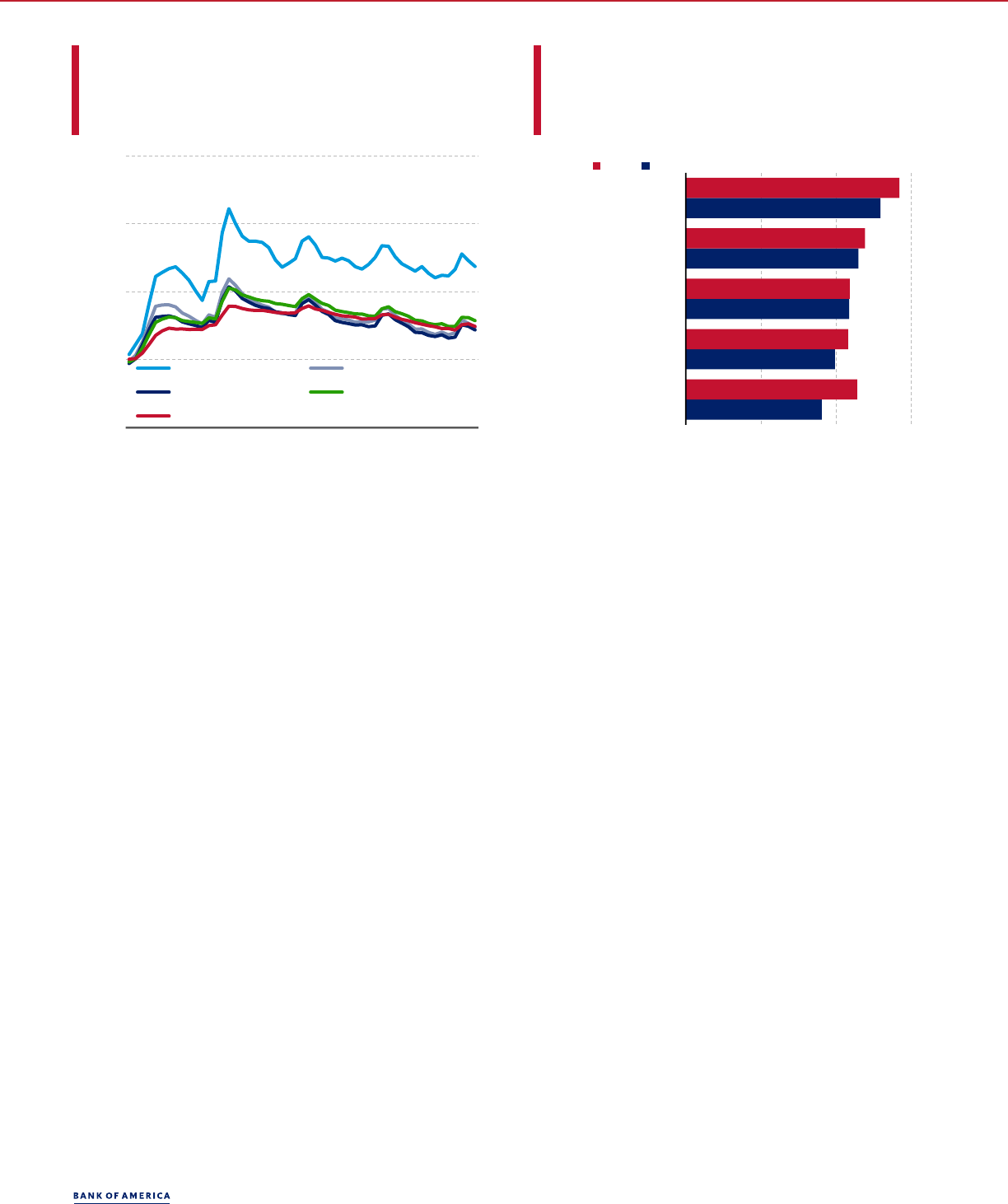

Is “trading down” trending?

While younger generations card spending growth appears to have picked up, we find across a broader range of payment channels

that their share of spending on discretionary spending is declining.

Using Bank of America internal data across payment channels (including ACH, as well as card payments), we construct a broader

measure of necessity spending that includes not only necessity spending on credit and debit cards, but also non-discretionary

services such as insurance and mortgage payments made across broader payment channels.

Exhibit 6 shows that as of May, older Millennials, Gen X, and Baby Boomers have the lowest shares of discretionary spending, at

nearly 50%. However, while Gen Z (61%) and younger Millennials’ (52%) shares of discretionary spending are higher, they are

declining and fast approaching their older counterparts. This is despite their after-tax wage growth being notably ahead of their

credit and debit card spending growth, which indicates these younger households may not be able to dedicate their extra

earnings to discretionary spending.

This convergence is likely part life stage-related, with younger consumers taking on more financial responsibilities such as

buying a house or car. In a recent publication

we noted that younger generations have strong payments growth for housing and

autos.

Gen Z and younger Millennials also face pressure on their necessity spending in the form of rising housing and auto costs.

Further to that point, in another recent piece,

we found that Gen Z and Millennials have recently been “trading down” from

premium or standard-tier grocery stores to value-tier grocers, whereas Gen X and Baby Boomers have long been value shoppers.

Groceries are not the only sector where this is occurring; our data also shows that these generations are also dining out less and

staying in more. Looking at the ratio of average household grocery spending to average household restaurant spending, Exhibit 7

suggests that while Gen Z and Millennials tend to dine out more than Baby Boomers and Gen Xers on a monthly basis, they are

beginning to “trade down” to eating at home more often as well.

Exhibit 6: Older Millennials, Gen X, and Baby Boomers have lower

percentage shares of discretionary spending, but younger

Millennials and Gen Z’s levels are quickly converging with their

older counterparts

Discretionary outflows as a percentage share of total outflows across

payments by age generation (3-month moving average, %)

Source:

Bank of America internal data

BANK OF AMERICA INSTITUTE

Exhibit 7: The ratio of average household grocery spending to

average household restaurant spending is higher for Gen X and

Baby Boomers, but declining, while Gen Z and Millennials’ ratios

have increased

The ratio of average household grocery spending compared to average

household restaurant spending by age generation (Jan-

May, average ratio

in which values > 1 imply more grocery than restaurant spending)

Source:

Bank of America internal data

BANK OF AMERICA INSTITUTE

Signs of credit stress for younger consumers?

Are trade-downs and pressure on discretionary spending, despite strong wage gains, a potential sign of deteriorating financial

health amongst the younger generations? And are some younger generations increasingly using credit to support their spending?

45%

55%

65%

75%

May-18 May-19 May-20 May-21 May-22 May-23

May-

Gen Z Younger Millennials

Older Millennials Gen X

Baby Boomers

0

0.5

1

1.5

2

2.5

Gen Z Millennials Gen X Baby Boomers

2019 2022 2023 2024

4

11 June 2024

I NSTI TUTE

When looking at credit card data, it’s important to distinguish between ‘revolvers’ and ‘transactors.’ While the latter group uses

their cards to make purchases and pays off the full balance each month, revolvers tend to maintain some level of positive card

balance from one month to the next.

Intuitively, revolvers would most likely exhibit signs of being financially stretched, given they are already not paying their balance

in full. Focusing only on this group, Exhibit 8 uses Bank of America internal data to show how the credit card utilization rate has

changed since 2019 across generations for a stable cohort of clients classified as ‘revolvers’ and finds that all generations’

utilization rates are below the level they were in 2019. While Millennials and Gen Z have seen the most significant moves higher

in utilization, these levels do not look particularly elevated.

Exhibit 8: The utilization of younger generation revolvers has risen

most, but remains below the level in 2019

Credit card utilization rates for a stable cohort of clients classified as

‘revolvers’ (average utilization rate in 2019=1, data to April 2024)

Source:

Bank of America internal data

BANK OF AMERICA INSTITUTE

Exhibit 9: Repayment rates have fallen amongst Gen Z and younger

Millennials revolvers, though from relatively high absolute levels

Credit card repayment rates for a stable cohort of clients classified as

‘revolvers’ (average utilization rate in 2019=1, data to April 2024)

Source:

Bank of America internal data

BANK OF AMERICA INSTITUTE

Exhibit 9 shows the credit card repayment rate among the generations – a lower rate means customers are paying off less of

their revolving balances each month.

Interestingly, while the older generations’ repayment rates are above 2019 levels, it appears that Gen Z and younger Millennials

have seen a decline in their repayment rates to below 2019 levels. This could be a sign that these generations are under greater

financial pressure and paying off less of their balances as a result. However, it is hard to abstract from ‘life-cycle’ influences as

these cohorts had the highest repayment rates in 2019 and their current trajectory may simply be a reflection of their behavior

becoming increasingly similar to older generations as they mature and take on more recurring months costs.

When we look at Bank of America internal data on saving and checking balances by all households, we see that all generations,

from Gen Z through to Baby Boomers, have 44% or more deposits than they did pre-pandemic (Exhibit 10).

0.80

0.90

1.00

1.10

Jan-19 Jan-20 Jan-21 Jan-22 Jan-23

Jan-24

Gen Z

Younger Millennials

Older Millennials

Gen X

Boomer/Traditionalist

0.50

0.75

1.00

1.25

Jan-19 Jan-20 Jan-21 Jan-22 Jan-23 Jan-24

Gen Z

Younger Millennials

Older Millennials

Gen X

Boomer/Traditionalist

11 June 2024

5

I NSTI TUTE

Exhibit 10: All generations have raised deposits relative to 2019

Monthly median household savings and checking balances by

generation (2019=100) for a fixed group of households through May

2024

Source:

Bank of America internal data

Note:

Bank of America internal data. Monthly data includes those households that had a

consumer deposit account (checking and/or savings account) for all months from January

2019 through

May 2024.

BANK OF AMERICA INSTITUTE

Exhibit 11: The share of younger clients with deposit inflows less

than 95% of outflows has been rising

The proportion of a stable cohort of clients with a ratio of deposit

account inflows to outflows less than 0.95 by generation (%, six month

average, data to April 2020/2024)

Source:

Bank of America internal data

BANK OF AMERICA INSTITUTE

Are there any signs of stress within these younger generations? Exhibit 11 shows a stable group of Bank of America clients and

looks at the proportion that have seen the inflows to their deposit account fall short of their outflows by 5% or more over a six-

month average. Conceptually, these clients could be relatively more stretched as it appears their incomings have been falling

meaningfully short of their outgoings for an extended period of time.

While the proportion of clients whose inflows are lower than outflows by 5% or more is generally low, it appears Gen Z and

younger Millennials have seen a rise in this share since 2020, while Gen X and older Millennials have seen little change.

Overall, based on our data, it appears that the strength of the labor market and the associated wage growth, as well as elevated

savings deposits, have allowed a majority of younger cohorts to weather any pressures they are seeing from higher necessity

outlays. However, around the edges, some do seem to be feeling more pressure, with some signs of rising credit card utilization

rates and a rising proportion of the younger cohorts finding outflows from their accounts outstripping their inflows by a sizeable

margin.

Monthly data update

Total payment growth across all channels (ACH, Bill Pay, Credit and Debit Card, Wires, Person-to-Person, Cash and Check) rose

1.8% YoY in May. Bank of America total credit and debit card spend, which comprises around 20% of total payments, increased

2.4% YoY in May.

0

100

200

300

400

2020 2021 2022 2023 2024

Gen Z Younger Millennials

Older Millennials Gen X

Baby Boomer

0% 10% 20% 30%

Gen Z

Younger Millennial

Older Millennial

Gen X

Baby Boomer/

Traditionalist

2024 2020

6

11 June 2024

I NSTI TUTE

Methodology

Selected Bank of America transaction data is used to inform the macroeconomic views expressed in this report and should be

considered in the context of other economic indicators and publicly available information. In certain instances, the data may

provide directional and/or predictive value. The data used is not comprehensive; it is based on aggregated and anonymized

selections of Bank of America data and may reflect a degree of selection bias and limitations on the data available.

Any payments data represents aggregated spend from US Retail, Preferred, Small Business and Wealth Management clients with

a deposit account or credit card. Aggregated spend include total credit card, debit card, ACH, wires, bill pay, business/peer-to-

peer, cash, and checks.

Any Small Business payments data represents aggregate spend from Small Business clients with a deposit account or a Small

Business credit card. Payroll payments data include channels such as ACH (automated clearing house), bill pay, checks and wire.

Bank of America per Small Business client data represents activity spending from active Small Business clients with a deposit

account or a Small Business credit card and at least one transaction in each month. Small businesses in this report include

business clients within Bank of America and generally defined as under $5mm in annual sales revenue.

Unless otherwise stated, data is not adjusted for seasonality, processing days or portfolio changes, and may be subject to

periodic revisions.

The differences between the total and per household card spending growth rate can be explained by the following reasons:

1. Overall total card spending growth is partially boosted by the growth in the number of active cardholders in our sample. This

could be due to an increasing customer base or inactive customers using their cards more frequently.

2. Per household card spending growth only looks at households that complete at least five transactions with Bank of America

cards in the month. Per household spending growth isolates impacts from a changing sample size, which could be unrelated to

underlying economic momentum, and potential spending volatility from less active users.

3. Overall total card spending includes small business card spending while per household card spending does not.

4. Differences due to using processing dates (total card spending) versus transaction date (per household card spending).

5. Other differences including household formations due to young adults moving in and out of their parent’s houses during

COVID.

Any household consumer deposit data based on Bank of America internal data is derived by anonymizing and aggregating data

from Bank of America consumer deposit accounts in the US and analyzing that data at a highly aggregated level. Whenever

median household savings and checking balances are quoted, the data is based on a fixed cohort of households that had a

consumer deposit account (checking and/or savings account) for all months from January 2019 through the most current month

of data shown.

Bank of America aggregated credit/debit card spending per household includes spending from active US households only. Only

consumer card holders making a minimum of five transactions a month are included in the dataset. Spending from corporate

cards are excluded. Data regarding merchants who receive payments are identified and classified by the Merchant Categorization

Code (MCC) defined by financial services companies. The data are mapped using proprietary methods from the MCCs to the

North American Industry Classification System (NAICS), which is also used by the Census Bureau, in order to classify spending

data by subsector. Spending data may also be classified by other proprietary methods not using MCCs.

Discretionary spending consists of total payments across credit card, debit card, ACH, wires, bill pay, business/peer-to-peer and

checks. minus necessities (food at home, childcare, housing, autos, etc.) and other outflows (transfers, debt payments, cash, etc.).

The data on inflows and outflows into direct deposit accounts data is based on BAC internal data, it is derived by anonymizing

and aggregating data from Bank of America consumer deposit accounts in the US at a highly aggregated level. Inflows and

outflows are calculated as six-month averages.

Generations, if discussed, are defined as follows:

1. Gen Z, born after 1995

2. Younger Millennials: born between 1989-1995

3. Older Millennials: born between 1978-1988

4. Gen Xers: born between 1965-1977

11 June 2024

7

I NSTI TUTE

5. Baby Boomer: 1946-1964

6. Traditionalists: pre-1946

Any reference to card spending per household on gasoline includes all purchases at gasoline stations and might include

purchases of non-gas items.

Additional information about the methodology used to aggregate the data is available upon request.

Contributors

David Michael Tinsley

Senior Economist, Bank of America Institute

Joe Wadford

Economist, Bank of America Institute

Liz Everett Krisberg

Head of Bank of America Institute

Taylor Bowley

Economist, Bank of America Institute

Vanessa Cook

Content Strategist, Bank of America Institute

Sources

Li Wei

Director, Global Risk Analytics

Kimberly Warren

Director, Global Risk Analytics

Ana Maxim

Senior Vice President, Consumer and Small Business

Jon Kaplan

Senior Vice President, Digital and Data

Mel Roasa

Vice President, Analytics; Data, Digital & Global Marketing

Dale Lin

Quantitative Finance Manager, Global Risk Analytics

8

11 June 2024

I NSTI TUTE

Disclosures

These materials have been prepared by Bank of America Institute and are provided to you for general information purposes only. To the extent these materials reference Bank of

America data, such materials are not intended to be reflective or indicative of, and should not be relied upon as, the results of operations, financial conditions or performance of Bank

of America. Bank of America Institute is a think tank dedicated to uncovering powerful insights that move business and society forward. Drawing on data and resources from across

the bank and the world, the Institute delivers important, original perspectives on the economy, sustainability and global transformation. Unless otherwise specifically stated, any

views or opinions expressed herein are solely those of Bank of America Institute and any individual authors listed, and are not the product of the BofA Global Research department or

any other department of Bank of America Corporation or its affiliates and/or subsidiaries (collectively Bank of America). The views in these materials may differ from the views and

opinions expressed by the BofA Global Research department or other departments or divisions of Bank of America. Information has been obtained from sources believed to be

reliable, but Bank of America does not warrant its completeness or accuracy. These materials do not make any claim regarding the sustainability of any product or service. Any

discussion of sustainability is limited as set out herein. Views and estimates constitute our judgment as of the date of these materials and are subject to change without notice. The

views expressed herein should not be construed as individual investment advice for any particular person and are not intended as recommendations of particular securities, financial

instruments, strategies or banking services for a particular person. This material does not constitute an offer or an invitation by or on behalf of Bank of America to any person to buy

or sell any security or financial instrument or engage in any banking service. Nothing in these materials constitutes investment, legal, accounting or tax advice.

Copyright 2024 Bank of America Corporation. All rights reserved.