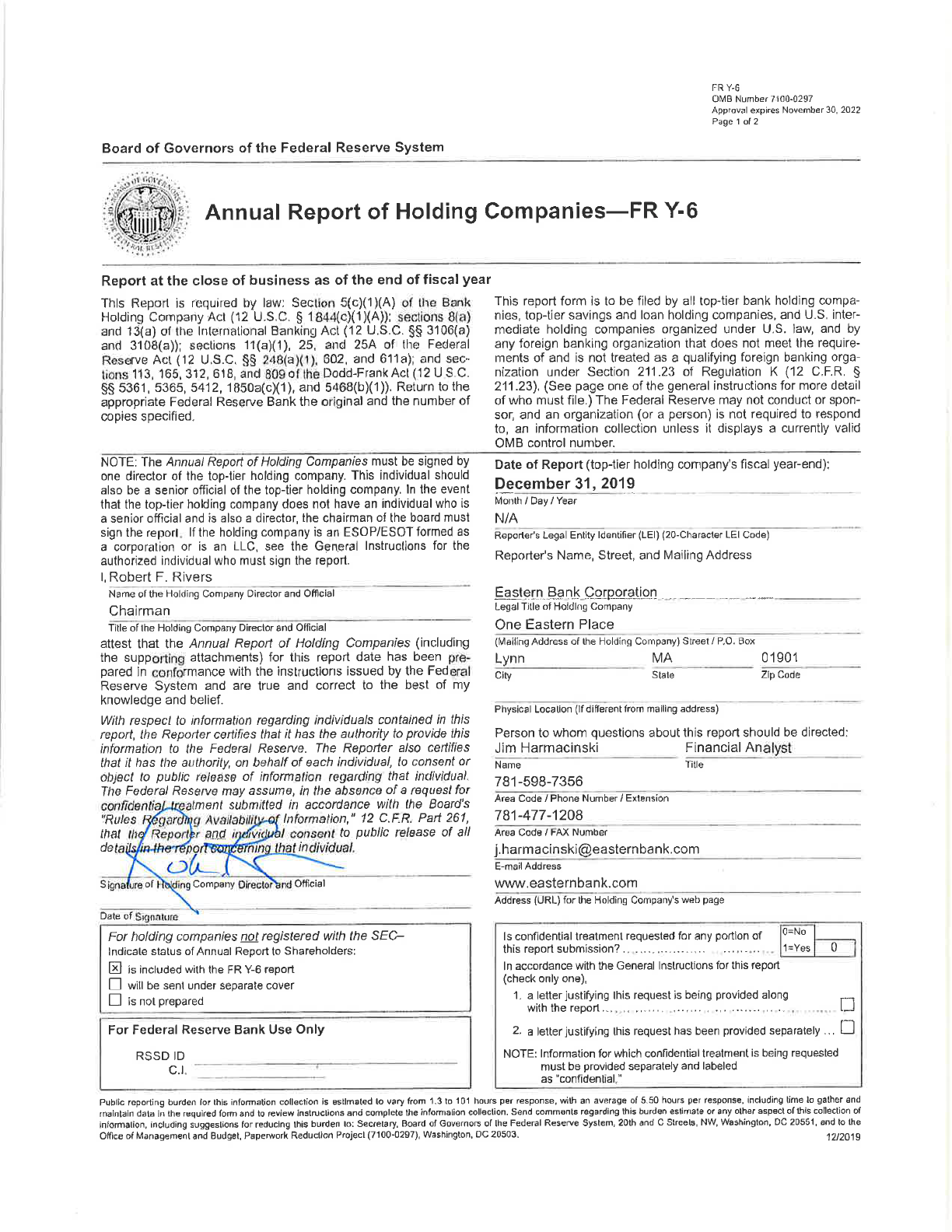

Report Item 1a:

Form 10-K

N/A

Report Item 1b:

Annual Report

Enclosed is the 2019 Consolidated Eastern Bank Corporation Annual Report.

Report Item 2a:

Organization Chart

Attached is an organization chart of Eastern Bank Corporation's direct and indirect ownership

of all its banks and nonbank subsidiaries.

Report Item 2b:

Domestic Branch Listing

Attached is the list of Eastern Bank Corporation's branches

Report Item 3:

Shareholders

Eastern Bank Corporation is a mutually owned holding company with no shareholders.

Report Item 4:

Directors and Officers

Attached is a list of the information requested for Eastern Bank Corporation's Board of Directors

and Executive Officers.

The following list is a reference for the responses submitted to each of the report items

for the 2019 Annual Report FR Y-6 for Eastern Bank Corporation.

Eastern Bank Corporation

2019 Annual Report

Management’s Letter

2019 was another outstanding year for Eastern as we generated our third consecutive year of

record results. Our net income of $135.1 million was an all-time high and exceeded our 2018

results by over 10%. Total assets grew to a record $11.6 billion; and loans, deposits and capital

levels were also new highs. Loans ended 2019 at $8.9 billion or an increase of $124 million

from 2018; deposits were $9.6 billion, up $152 million from 2018; and capital exceeded $1.6

billion, or an increase of $167 million from 2018 levels. Our loan credit quality remained stellar

with very low loan losses of 0.05% of average loans and non-performing loans of 0.49% of total

loans.

Although interest rate levels were lower in 2019 than they had been in 2018, a vibrant local

economy and our strong competitive position helped us generate this performance. The

company’s net interest income (the difference between interest earned on loans and

investments less interest paid on deposits and other funding sources) was $411 million, or 5.4%

above 2018, as higher interest rates on loans and investments exceeded higher costs of

deposits and other funding. Our net interest margin improved to 3.96% from 3.84% in 2018 as

our balance sheet, which we have been positioning to perform well for any direction in interest

rates, paid dividends.

All of our business units performed well in 2019. Our Commercial Banking Group had another

exceptional year as commercial loans increased from $5.9 billion to $6.2 billion, or 5%. Our

commitment to Small Business remained as strong as ever as we were ranked the #1 SBA

lender in New England for the 10th consecutive year. Our retail businesses, both consumer

lending and our branch-based deposit groups, had outstanding years as checking and lending

product sales to our customers were well above prior levels. Eastern Insurance Group had

another outstanding year with more than $91 million in revenues and Eastern Wealth

Management saw revenues increase 3% to just under $20 million.

We leveraged our existing platforms to generate these terrific results with noninterest expenses

of $413 million, less than a 4% increase from 2018. We continue to be very pleased with our

many investments in technology and people and believe our online and mobile platform

upgrades over the last few years have provided a better customer experience and new

opportunities for growth. We will finish the roll out of our commercial and business customers’

online banking upgrades in the first half of 2020 and plan continuous upgrades in our

commercial lending origination platform we implemented several years ago. The process to

create better digital experiences for our customers that make it easy to transact with Eastern,

and to improve our analytical capabilities to better understand our customers, made great

strides in 2019 and we look forward to more in 2020.

Our capital base is critical to our health and future success. We ended 2019 with over $1.6

billion in capital after adding $167 million through the year, primarily due to our earnings. Our

capital ratios far exceed the bank regulatory minimums and we also exceed the “well-

capitalized” standards set by our regulators. In addition, our balance sheet is extremely strong

with excellent loan quality, ample liquidity and robust capital levels.

1

We were very pleased with these record results in 2019 and would like to thank our 1,896

Eastern colleagues for making them happen. We believe we are well positioned for continued

success and look forward to another outstanding year in 2020.

ROBERT F. RIVERS DEBORAH C. JACKSON

Chair and Chief Executive Officer Lead Director

QUINCY L. MILLER JAMES B. FITZGERALD

Vice Chair and President Vice Chair, Chief Financial Officer & Chief Administrative Officer

2

Financial Highlights

(Dollars in thousands) 2019 2018 2017 2016 2015

Balance Sheet Data

Total assets $

11,628,775 $ 11,378,287 $ 10,873,073 $ 9,801,109 $ 9,588,786

Securities and short-term

investments

1,736,296 1,618,802 1,766,213 1,284,080 1,651,562

Residential loans

1,428,630 1,430,764 1,290,461 1,153,735 1,041,072

Consumer loans

1,335,519 1,501,209 1,548,287 1,539,534 1,607,804

Commercial loans

6,222,897 5,924,030 5,388,293 5,011,862 4,482,592

Total loans

8,987,046 8,856,003 8,227,041 7,705,131 7,131,468

Total deposits

9,551,392 9,399,493 8,815,452 8,188,950 8,133,730

Total retained earnings

1,644,000 1,433,141 1,330,514 1,254,927 1,205,014

Average total assets

11,404,110 11,137,370 10,391,796 9,913,145 9,667,907

Average earning assets

10,529,522 10,298,162 9,566,544 9,077,633 8,871,112

Average total deposits

9,365,581 9,161,981 8,684,043 8,416,777 8,031,975

Operating Data

Net interest income $

411,264 $ 390,044 $ 338,514 $ 293,574 $ 274,977

Provision for credit losses

6,300 15,100 5,800 7,900 (325)

Noninterest income

182,299 180,595 197,727 169,128 153,007

Noninterest expense

412,684 397,928 389,413 367,643 333,695

Income before income

taxes

174,579 157,611 141,028 87,159 94,614

Net income

135,098 122,727 86,697 62,714 62,564

Other Data

Return on average assets

1.18% 1.10% 0.83% 0.63% 0.65%

Return on average equity

8.75% 9.02% 6.62% 5.06% 5.33%

Net interest margin (FTE)

(1)

3.96% 3.84% 3.65% 3.33% 3.17%

Equity to assets ratio

13.76% 12.60% 12.24% 12.80% 12.57%

(1) Fully tax equivalent

December 31

3

Average Balance Sheets

The following tables present average balances, interest rates and yields (tax equivalent basis) for

the years indicated:

Average Interest Average

(Dollars in thousands) Balance Income/Expense Yield/Rate

Assets

Loans:

Residential mortgage loans $ 1,439,845 $ 53,736 3.73 %

Commercial loans

(2)

6,089,410 291,055 4.78

Consumer loans 1,419,692 60,009 4.23

Total loans 8,948,947 404,800 4.52

Investment securities

(2)

1,435,719 42,494 2.96

Federal funds sold and other short-term

investments 144,856 2,977 2.06

Total earning assets 10,529,522 450,271 4.28

Noninterest-bearing assets 874,588

Total assets $ 11,404,110

Liabilities and Retained Earnings

Deposits:

Savings accounts $ 991,244 210 0.02

Interest checking accounts

(1)

1,842,993 3,947 0.21

Money market investment

(1)

2,769,934 19,150 0.69

Time accounts 392,035 3,994 1.02

Total interest-bearing deposits 5,996,206 27,301 0.46

Borrowed funds 291,413 6,452 2.21

Total interest-bearing liabilities 6,287,619 33,753 0.54

Demand accounts

(1)

3,369,375

Other noninterest-bearing liabilities 203,925

Retained earnings 1,543,191

Total liabilities and retained earnings $ 11,404,110

Net interest income $ 416,518

Interest spread 3.74 %

Net interest income to earning assets 3.96 %

(1) Balances shown for interest checking accounts, money market investments, and demand accounts do not reflect the

impacts of certain sweep programs designed to manage reserve requirements at the Federal Reserve Bank of Boston.

(2) FTE adjustments to commercial loan and investment security income were $2.7 and $2.5 million, respectively.

2019

4

Average Interest Average

(Dollars in thousands) Balance Income/Expense Yield/Rate

Assets

Loans:

Residential mortgage loans $ 1,358,387 $ 49,840 3.67 %

Commercial loans

(2)

5,653,675 262,234 4.64

Consumer loans 1,554,087 59,669 3.84

Total loans 8,566,149 371,743 4.34

Investment securities

(2)

1,539,901 45,707 2.97

Federal funds sold and other short-term

investments 192,112 3,412 1.78

Total earning assets 10,298,162 420,862 4.09

Noninterest-bearing assets 839,208

Total assets $ 11,137,370

Liabilities and Retained Earnings

Deposits:

Savings accounts $ 1,048,289 229 0.02

Interest checking accounts

(1)

1,821,854 3,325 0.18

Money market investment

(1)

2,422,531 9,988 0.41

Time accounts 452,885 3,843 0.85

Total interest-bearing deposits 5,745,559 17,385 0.30

Borrowed funds 410,312 7,737 1.89

Total interest-bearing liabilities 6,155,871 25,122 0.41

Demand accounts

(1)

3,416,422

Other noninterest-bearing liabilities 204,515

Retained earnings 1,360,562

Total liabilities and retained earnings $ 11,137,370

Net interest income $ 395,740

Interest spread 3.68 %

Net interest income to earning assets 3.84 %

(1) Balances shown for interest checking accounts, money market investments, and demand accounts do not reflect the

impacts of certain sweep programs designed to manage reserve requirements at the Federal Reserve Bank of Boston.

(2) FTE adjustments to commercial loan and investment security income were $2.6 and $3.1 million, respectively.

2018

5

Ernst & Young LLP Tel: +1 617 266 2000

200 Clarendon Street Fax: +1 617 266 5843

Boston, MA 02116 ey.com

Report of Independent Auditors

The Board of Directors

Eastern Bank Corporation

We have audited the accompanying consolidated financial statements of Eastern Bank Corporation,

which comprise the consolidated balance sheets as of December 31, 2019 and 2018, and the related

consolidated statements of income, comprehensive income, changes in retained earnings and cash flows

for the years then ended, and the related notes to the consolidated financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in

conformity with U.S. generally accepted accounting principles; this includes the design,

implementation and maintenance of internal control relevant to the preparation and fair presentation of

financial statements that are free of material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We

conducted our audits in accordance with auditing standards generally accepted in the United States.

Those standards require that we plan and perform the audit to obtain reasonable assurance about

whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures

in the financial statements. The procedures selected depend on the auditor’s judgment, including the

assessment of the risks of material misstatement of the financial statements, whether due to fraud or

error. In making those risk assessments, the auditor considers internal control relevant to the entity’s

preparation and fair presentation of the financial statements in order to design audit procedures that are

appropriate in the circumstances. An audit also includes evaluating the appropriateness of accounting

policies used and the reasonableness of significant accounting estimates made by management, as well

as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for

our audit opinion.

6

Opinion

In our opinion, the financial statements referred to above present fairly, in all material respects, the

consolidated financial position of Eastern Bank Corporation at December 31, 2019 and 2018, and the

consolidated results of its operations and its cash flows for the years then ended in conformity with

U.S. generally accepted accounting principles.

February 28, 2020

7

Eastern Bank Corporation

Consolidated Balance Sheets

Assets

Cash and due from banks $ 135,503 $ 149,703

Other short-term investments 227,099 110,005

Cash and cash equivalents 362,602 259,708

Trading securities 961 52,899

Securities available for sale 1,508,236 1,455,898

Loans held for sale 26 22

Loans and leases, net of allowance for credit losses of

$82,297 in 2019 and $80,655 in 2018 8,899,184 8,774,913

Federal Home Loan Bank stock, at cost 9,027 17,959

Premises and equipment 57,453 66,475

Bank-owned life insurance 77,546 75,434

Goodwill and other intangibles, net 377,734 381,276

Deferred income taxes, net 28,207 37,676

Rabbi trust assets 78,012 64,819

Other assets 229,787 191,208

Total assets $ 11,628,775 $ 11,378,287

Liabilities and retained earnings

Liabilities:

Deposits:

Demand $ 386,446 $ 337,169

Savings 971,119 999,649

Interest checking 214,462 464,352

Money market investment 7,650,226 7,123,375

Time 243,941 277,740

Time - $250,000 and over 85,198 197,208

Total deposits 9,551,392 9,399,493

Borrowed funds 235,395 334,287

Other liabilities 241,835 211,366

Total liabilities 10,028,622 9,945,146

Retained earnings 1,644,000 1,508,902

Accumulated other comprehensive income, net of tax:

Unrealized appreciation (depreciation) on securities 21,798 (19,360)

available for sale

Funded status of defined benefit postretirement plans (81,269) (59,389)

Unrealized appreciation on cash flow hedges 15,624 2,988

Total retained earnings 1,600,153 1,433,141

Total liabilities and retained earnings $ 11,628,775 $ 11,378,287

See accompanying notes.

December 31

2019

2018

(In Thousands)

8

Eastern Bank Corporation

Consolidated Statements of Income

Interest and dividend income:

Loans, including fees $ 402,092 $ 369,148

Trading securities 242 1,033

Taxable securities available for sale 31,400 31,988

Tax-exempt securities available for sale 8,306 9,585

Federal funds sold and other short-term investments 2,977 3,412

Total interest and dividend income

445,017 415,166

Interest expense:

Deposits 27,301 17,384

Borrowed funds 6,452 7,738

Total interest expense

33,753 25,122

Net interest income 411,264 390,044

Provision for allowance for credit losses 6,300 15,100

Net interest income after provision for credit losses

404,964 374,944

Noninterest income:

Insurance commissions 90,587 91,885

Service charges on deposit accounts 27,043 26,897

Trust and investment advisory fees 19,653 19,128

Debit card processing fees 10,452 16,162

Interest rate swap income 4,362 5,012

Income (losses) from investments held in rabbi trusts 9,866 (1,542)

Trading securities gains, net 1,297 2,156

Net gain on sales of mortgage loans held for sale 795 397

Gains on sales of securities available for sale, net 2,016 50

(Losses) gains on sales of other assets (15) 1,989

Other 16,243 18,461

Total noninterest income

182,299 180,595

Noninterest expense:

Salaries and employee benefits 252,238 239,349

Office occupancy and equipment 36,458 35,480

Data processing 45,939 45,260

Professional services 15,958 14,812

Charitable contributions 12,905 13,251

Marketing 9,619 11,100

FDIC insurance 1,878 4,180

Amortization of intangible assets 3,542 3,891

Net periodic benefit cost, excluding service cost (5,335) (6,498)

Other 39,482 37,103

Total noninterest expense

412,684 397,928

Income before income tax expense 174,579 157,611

Income tax expense 39,481 34,884

Net income $

135,098

$

122,727

See accompanying notes.

Year Ended December 31

2019

2018

(In Thousands)

9

Eastern Bank Corporation

Consolidated Statements of Comprehensive Income

Net income $ 135,098 $ 122,727

Other comprehensive income, net of tax:

Unrealized gains (losses) on securities available for sale:

Change in fair value of securities available for sale 42,715 (30,485)

Less: reclassification adjustment for gains

included in net income 1,557 40

Net change in fair value of securities available for sale 41,158 (30,525)

Unrealized gains(losses) on cash flow hedges:

Change in fair value of cash flow hedges 14,576 3,849

Less: reclassification adjustment for income 1,940 861

Net change in fair value of cash flow hedges 12,636 2,988

Defined benefit pension plans:

(Amortization) of actuarial net loss (5,206) (5,479)

Change in actuarial net loss 27,119 (1,926)

(Amortization) of prior service cost (33) (32)

Net change in actuarial net loss 21,880 (7,437)

Total other comprehensive income (loss) 31,914 (20,100)

Comprehensive income $ 167,012 $ 102,627

See accompanying notes.

Year Ended December 31

2019

2018

(In Thousands)

10

Eastern Bank Corporation

Consolidated Statements of Changes in Retained Earnings

Accumulated

Other

Retained Comprehensive

Earnings Income Total

Balance at December 31, 2017 $ 1,379,006 $ (48,492) $ 1,330,514

Opening balance reclassification

(1)

:

Unrealized appreciation on securities available for sale (1,953) 1,953 -

Actuarial net loss of defined benefit pension plans 9,122 (9,122) -

Net income 122,727 - 122,727

Other comprehensive (loss), net of tax - (20,100) (20,100)

Balance at December 31, 2018 1,508,902 (75,761) 1,433,141

Net income 135,098 - 135,098

Other comprehensive income, net of tax - 31,914 31,914

Balance at December 31, 2019 $ 1,644,000 $ (43,847) $ 1,600,153

(1) Opening balance reclassification adjustment, related to the adoption of Accounting Standards Update 2018-02,

to reclassify amounts stranded in other comprehensive income to retained earnings as a result of the Tax Cuts and

Jobs Act.

See accompanying notes.

(In Thousands)

11

Eastern Bank Corporation

Consolidated Statements of Cash Flows

Operating activities

Net income $

135,098

$

122,727

Adjustments to reconcile net income to net cash provided by

operating activities:

Provision for allowance for credit losses

6,300 15,100

Depreciation

15,940 16,177

Amortization of intangible assets

3,542 3,891

Deferred income tax expense (benefit)

1,376 (4,878)

Amortization of premiums, discounts, and fees, net

8,193 4,747

Increase in cash surrender value of bank-owned life insurance

(2,112) (15)

Decrease (increase) in trading securities, net

51,938 (6,108)

Gain on sale of securities available for sale, net

(2,016) (50)

Net gain on sale of mortgage loans held for sale

(795) (397)

Proceeds from sale of loans held for sale

208,658 108,788

Originations of loans held for sale

(207,867) (106,059)

(Increase) decrease in prepaid pension expense

(11,031) 11,237

Other, net

(11,347) 39,849

Net cash provided by operating activities 195,877 205,009

Investing activities

Proceeds from sales of securities available for sale

47,985 11,672

Proceeds from maturities and principal paydowns of securities

available for sale

204,065 162,425

Purchases of securities available for sale

(252,571) (167,584)

Proceeds from sale of Federal Home Loan Bank stock

42,034 18,346

Purchases of Federal Home Loan Bank stock

(33,102) (12,035)

Contributions to low income housing tax credit investments

(6,349) (3,270)

Contributions to other equity investments

(4,545) (146)

Distributions from equity investments

62 226

Proceeds from life insurance policies

- 743

Net increase in outstanding loans

(135,666) (637,518)

Acquisitions, net of cash and cash equivalents acquired

- (11,500)

Proceeds from sale of portion of reporting unit

- 571

Purchased banking premises and equipment, net

(7,187) (9,034)

Net cash used in investing activities (145,274) (647,104)

Financing activities

Net increase in demand, savings, interest checking, and money

market investment deposit accounts

297,708 485,087

Net (decrease) increase in time deposits

(145,809) 98,954

Net decrease in borrowed funds

(98,892) (192,218)

Contingent consideration paid

(716) (1,173)

Net cash provided by financing activities

52,291 390,650

Net increase (decrease) in cash, cash equivalents, and restricted cash

102,894 (51,445)

Cash, cash equivalents, and restricted cash at beginning of year

259,708 311,153

Cash, cash equivalents, and restricted cash at end of year $ 362,602 $ 259,708

See accompanying notes.

Year Ended December 31

2019

2018

(In Thousands)

12

Eastern Bank Corporation

Notes to Consolidated Financial Statements

December 31, 2019

1. Summary of Significant Accounting Policies

Nature of Operations

Eastern Bank Corporation (the Corporation) is a Massachusetts chartered mutual bank holding

company. Through its wholly-owned subsidiaries, Eastern Bank (the Bank) and Eastern Insurance

Group LLC, the Corporation provides a variety of banking, trust and investment, and insurance

services.

The activities of the Corporation are subject to the regulatory supervision of the Federal Reserve

Board. The activities of the Bank are subject to the regulatory supervision of the Federal Deposit

Insurance Corporation (FDIC) and the Consumer Financial Protection Bureau (CFPB). The

Corporation is also subject to various Massachusetts business and banking regulations, and the

Bank is also subject to various Massachusetts and New Hampshire business and banking

regulations.

Basis of Presentation

The consolidated financial statements include the accounts of the Corporation, its wholly-owned

subsidiaries and a consolidated tax credit investment company. All intercompany accounts and

transactions have been eliminated in consolidation. The Corporation consolidates: wholly-owned

subsidiaries; any variable interest entities (VIEs) where the Corporation or one of the

Corporation’s wholly-owned subsidiaries was determined to be the primary beneficiary of the VIE;

and any voting interest entities (VOEs) where either the Corporation or a wholly-owned subsidiary

is determined to have control of the VOE.

Certain previously reported amounts have been reclassified to conform to the current year

presentation.

The accounting and reporting policies of the Corporation conform to accounting principles

generally accepted in the United States (GAAP) and to the general practices of the banking

industry. In preparing the consolidated financial statements, management is required to make

estimates and assumptions that affect the reported amounts of assets and liabilities as of the date

of the balance sheet and revenues and expenses for the period. Actual results could differ from

those estimates.

13

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Material estimates that are particularly susceptible to change relate to the determination of the

allowance for credit losses, valuation and fair value measurements, other-than-temporary

impairment on investment securities, the liabilities for benefit obligations (particularly pensions),

the provision for income taxes and the valuation of goodwill and other intangibles and their

respective analyses of impairment.

The Corporation has evaluated subsequent events through February 28, 2020, which is the date

that the consolidated financial statements were available to be issued.

Business Combinations

Acquisitions of businesses are accounted for using the acquisition method of accounting.

Accordingly, the net assets of the companies acquired are recorded at their fair values at the date

of acquisition. Goodwill represents the excess of purchase price over the fair value of net assets

acquired. Other intangible assets represent acquired assets that lack physical substance but can be

distinguished from goodwill because of contractual or other legal rights, or because the asset is

capable of being sold or exchanged either on its own, or in combination with a related contract,

asset, or liability.

The Corporation evaluates goodwill for impairment at least annually, or more often if warranted.

Other intangible assets are reviewed for impairment whenever there is an indication of impairment,

however, useful lives are evaluated annually. Any impairment losses are charged to earnings. The

Corporation amortizes other intangible assets over their respective estimated useful lives. The

estimated useful life of core deposit identifiable intangible assets fall within a range of seven to

ten years and the estimated useful life of customer lists from insurance agency acquisitions is ten

years. The estimated useful life of non-compete agreements resulting from insurance agency

acquisitions are dependent upon the terms of the agreement. Intangible assets are stated at cost

less accumulated amortization.

Cash and Cash Equivalents

Cash and cash equivalents include cash and due from banks, Federal funds sold, and other short-

term investments including restricted cash pledged, all of which have an original maturity of 90

days or less.

Securities

Debt and equity securities that are bought and held principally for the purpose of resale in the near

terms are classified as trading and fair value net income, respectively, and reported at fair value,

with unrealized gains and losses included in earnings.

14

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Debt securities classified as available for sale are reported at fair value, with unrealized gains and

losses reported as a separate component of other comprehensive income, net of tax.

Management evaluates impaired securities available for sale (e.g., those for which fair value is less

than cost) for other-than-temporary impairment (OTTI) at least on a quarterly basis, and more

frequently when economic or market concerns warrant such evaluation. Consideration is given to

the length of time and the extent to which the fair value has been less than cost, current market

conditions, the financial condition and near-term prospects of the issuer, performance of collateral

underlying the securities, the ratings of the individual securities, the interest rate environment, the

Corporation’s intent to sell the security or whether it is more likely than not that the Corporation

will be required to sell the debt security before its anticipated recovery, as well as other qualitative

factors.

Premiums and discounts on investments and mortgage-backed securities are amortized or accreted

to income using the effective interest rate method. If a decline in fair value below the amortized

cost basis of an investment is judged to be other than temporary, the investment is written down

to fair value. The portion of the impairment related to credit losses is included in earnings, and

the portion of the impairment related to other factors is included in other comprehensive income.

Gains and losses on sales of investments are recognized at the time of sale on the specific-

identification basis.

Loans

Loans are reported at their principal amount outstanding, net of deferred loan fees and any

unearned discount or unamortized premium for acquired loans. Unearned discount and

unamortized premium are accreted and amortized, respectively, to income on a basis that results

in level rates of return over the terms of the loans. Origination fees and related direct incremental

origination costs are offset, and the resulting net amount is deferred and amortized over the life of

the related loans using the interest method, assuming a certain level of prepayments. When loans

are sold or repaid, the unamortized fees and costs are recorded to income.

15

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Interest accruals are generally discontinued when management has determined that the borrower

may be unable to meet contractual obligations and/or when loans are 90 days or more in arrears,

unless management believes that collateral held by the Corporation is clearly sufficient and full

satisfaction of both principal and interest is highly probable or the loan is accounted for as a

purchased credit-impaired loan. When a loan is placed on nonaccrual, all interest previously

accrued but not collected is reversed against current period income and amortization of deferred

loan fees is discontinued. Interest received on nonaccrual loans is either applied against principal

or reported as income according to management’s judgment as to the collectability of principal.

Nonaccrual loans may be returned to an accrual status when principal and interest payments are

no longer delinquent, and the risk characteristics of the loan have improved to the extent that there

no longer exists a concern as to the collectability of principal and interest. Loans are considered

past due based upon the number of days delinquent according to their contractual terms.

Impaired loans consist of all loans for which management has determined it is probable the

Corporation will be unable to collect all amounts due according to the contractual terms of the loan

agreements. Factors considered by management in determining impairment include payment

status, collateral value, and the probability of collecting scheduled principal and interest payments

when due. The Corporation measures impairment of loans using a discounted cash flow method,

the loan’s observable market price, or the fair value of the collateral if the loan is collateral

dependent.

In cases where a borrower experiences financial difficulties and the Corporation makes certain

concessionary modifications to contractual terms, the loan is classified as a troubled debt

restructuring (TDR). Modifications may include adjustments to interest rates, extensions of

maturity, consumer loans where the borrower’s obligations have been effectively discharged

through Chapter 7 Bankruptcy and the borrower has not reaffirmed the debt to the Corporation,

and other actions intended to minimize economic loss and avoid foreclosure or repossession of

collateral. All TDR loans are considered impaired and therefore are subject to a specific review

for impairment loss. The impairment analysis discounts the present value of the anticipated cash

flows by the loan’s contractual rate of interest in effect prior to the loan’s modification or the fair

value of collateral if the loan is collateral dependent. The amount of impairment loss, if any, is

recorded as a specific loss allocation to each individual loan in the allowance for loan losses.

Commercial loans (commercial and industrial, commercial real estate, commercial construction,

and small business loans) and residential loans that have been classified as TDRs and which

subsequently default are reviewed to determine if the loan should be deemed collateral dependent.

In such an instance, any shortfall between the value of the collateral and the book value of the loan

is determined by measuring the recorded investment in the loan against the fair value of the

collateral less costs to sell.

16

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Acquired Loans

All acquired loans are recorded at fair value at the acquisition date with no carryover of the

allowance for loan losses. At acquisition, loans are also reviewed to determine if the loan has

evidence of deterioration in credit quality since origination and for which it is probable, at

acquisition, that all contractually required payments will not be collected. Such loans are deemed

to be purchased credit-impaired (PCI) loans. Under the accounting model for PCI loans, the excess

of cash flows expected to be collected over the carrying amount of the loans, referred to as the

“accretable yield,” is accreted into interest income over the life of the loans using the effective

yield method. Accordingly, PCI loans are not subject to classification as nonaccrual in the same

manner as originated loans. Rather, acquired loans are considered to be accruing loans because

their interest income relates to the accretable yield recognized and not to contractual interest

payments at the loan level. The difference between contractually required principal and interest

payments and the cash flows expected to be collected, referred to as the “nonaccretable difference,”

includes estimates of both the impact of prepayments and future credit losses expected to be

incurred over the life of the loans.

The estimate of cash flows expected to be collected is regularly re-assessed subsequent to

acquisition. These re-assessments involve updates, as necessary, of the key assumptions and

estimates used in the initial estimate of fair value. Generally speaking, expected cash flows are

affected by:

• Changes in the expected principal and interest payments over the estimated life – Changes

in expected cash flows may be driven by the credit outlook and actions taken with

borrowers. Changes in expected future cash flows resulting from loan modifications are

included in the assessment of expected cash flows.

• Change in prepayment assumptions – Prepayments affect the estimated life of the loans,

which may change the amount of interest income expected to be collected.

• Change in interest rate indices for variable rate loans – Expected future cash flows are

based, as applicable, on the variable rates in effect at the time of the assessment of

expected cash flows.

17

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

A decrease in expected cash flows in subsequent periods may indicate that the loan is impaired

which would require the establishment of an allowance for loan losses by a charge to the provision

for loan losses. An increase in expected cash flows in subsequent periods serves, first, to reduce

any previously established allowance for loan losses by the increase in the present value of cash

flows expected to be collected, and results in a recalculation of the amount of accretable yield for

the loan. The adjustment of accretable yield due to an increase in expected cash flows is accounted

for as a change in estimate. The additional cash flows expected to be collected are reclassified

from the nonaccretable difference to the accretable yield, and the amount of periodic accretion is

adjusted accordingly over the remaining life of the loans.

A PCI loan may be resolved either through receipt of payment (in full or in part) from the borrower,

the sale of the loan to a third party, or foreclosure of the collateral. For PCI loans accounted for

on an individual loan basis and resolved directly with the borrower, any amount received from

resolution in excess of the carrying amount of the loan is recognized and reported within interest

income.

A refinancing or modification of a PCI loan accounted for individually is assessed to determine

whether the modification represents a TDR. If the loan is considered to be a TDR, it will be

included in the total impaired loans reported by the Corporation. The loan will continue to

recognize interest income based upon the excess of cash flows expected to be collected over the

carrying amount of the loan.

18

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Allowance for Credit Losses

The allowance for credit losses is established to provide for probable losses incurred in the

Corporation’s loan portfolio at the balance sheet date and is established through a provision for

credit losses charged to earnings. The allowance is based on management’s assessment of many

factors, including the risk characteristics of the loan portfolio, current economic conditions, and

trends in loan delinquencies and charge-offs. Charge-offs, net of recoveries, are charged directly

to the allowance. Commercial and residential loans are charged-off in the period in which they

are deemed uncollectible. Delinquent loans in these product types are subject to ongoing review

and analysis to determine if a charge-off in the current period is appropriate. For consumer finance

loans, policies and procedures exist that require charge-off consideration upon a certain triggering

event depending on the product type. Charge-off triggers include: 120 days delinquent for

automobile, home equity, and other consumer loans with the exception of cash reserve loans for

which the trigger is 150 days delinquent; death of the borrower; or chapter 7 bankruptcy. In

addition to those events, the charge-off determination includes other credit quality indicators, such

as collateral position and adequacy or the presence of other repayment sources.

The allowance for credit losses is evaluated on a regular basis by management. While management

uses current information in establishing the allowance for losses, future adjustments to the

allowance may be necessary if economic conditions or conditions relative to borrowers differ

substantially from the assumptions used in making the evaluation. Management uses a

methodology to systematically estimate the amount of credit loss incurred in the portfolio.

Commercial real estate, commercial and industrial, and business banking loans are evaluated using

a loan rating system, historical losses and other factors which form the basis for estimating incurred

losses. Portfolios of more homogeneous populations of loans, including residential mortgages and

consumer loans, are analyzed as groups taking into account delinquency ratios, historical loss

experience and charge-offs.

19

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

The allowance consists of specific and general components. The specific component consists of

reserves for impaired loans (defined as those where management has determined it is probable it

will not collect all payments when due), typically classified as either doubtful or substandard. For

impaired loans, an allowance is established when the discounted cash flows (or collateral value or

observable market price) of the loan is lower than the carrying value of the loan. The general

component covers non-impaired non-classified loans and is based on historical loss experience

adjusted for qualitative factors. The qualitative factors include internal infrastructure factors,

external macroeconomic factors, and internal portfolio factors, all customized to loan pools that

include loans with similar characteristics. The general reserve rate is then determined as the greater

of the rate arrived at via the qualitative factor methodology or the floor rate. The floors are

determined by adjusting the Corporation’s average loss rates by long run industry average loss

rates for peer institutions, and then multiplying those by the industry loss emergence period.

In the ordinary course of business, the Corporation enters into commitments to extend credit and

standby letters of credit. Such financial instruments are recorded in the financial statements when

they become payable. The credit risk associated with these commitments is evaluated in a manner

similar to the allowance for loan losses. The reserve for unfunded lending commitments is

included in other liabilities in the balance sheet.

Additionally, various regulatory agencies, as an integral part of the Corporation’s examination

process, periodically assess the appropriateness of the allowance for loan losses and may require

the Corporation to increase its provision for loan losses or recognize further loan charge-offs, in

accordance with U.S. GAAP.

Mortgage Banking Activities

Mortgage loans held for sale to the secondary market are carried at the lower of cost or estimated

market value on an individual loan basis. The Corporation enters into commitments to fund

residential mortgage loans with an offsetting forward commitment to sell them in the secondary

markets in order to mitigate interest rate risk. Gains or losses on sales of mortgage loans are

recognized at the time of sale. Interest income is recognized on loans held for sale between the

time the loan is funded and the loan is sold. Direct loan origination costs and fees are deferred

upon origination and are recognized on the date of sale.

20

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Federal Home Loan Bank Stock

The Corporation, as a member of the Federal Home Loan Bank (FHLB) of Boston, is required to

maintain an investment in capital stock of the FHLB. Based on redemption provisions, the stock

has no quoted market value and is carried at cost.

Premises and Equipment Used in Operations

Land is carried at cost. Buildings, leasehold improvements, and equipment are stated at cost less

accumulated depreciation and amortization, computed principally on the straight-line method over

the estimated useful lives of the related assets or the terms of the leases, if shorter.

Premises and Equipment Held for Sale

Banking premises and equipment held for sale are carried at the lower of cost or estimated fair

value less costs to sell.

Retirement Plans

The Corporation provides pension benefits to its employees through various pension plans. At the

measurement date, plan assets are determined based on fair value, generally representing

observable market prices. The actuarial cost method used to compute the pension liabilities and

related expense is the projected unit credit method. The projected benefit obligation is principally

determined based on the present value of the projected benefit distributions at an assumed discount

rate. The discount rate which is utilized is determined using the spot rate approach whereby the

individual spot rates on the Financial Times and Stock Exchange (FTSE) above-median yield

curve are applied to each corresponding year’s projected cash flow used to measure the respective

plan’s service cost and interest cost. Periodic pension expense (or income) includes service costs,

interest costs based on the assumed discount rate, the expected return on plan assets, if applicable,

based on an actuarially derived market-related value and amortization of actuarial gains and losses.

The overfunded or underfunded status of the plans is recorded as an asset or liability on the

consolidated balance sheets, with changes in that status recognized through other comprehensive

income, net of related taxes.

21

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Variable Interest Entities and Voting Interest Entities

The Corporation is involved in the normal course of business with various types of special purpose

entities, some of which meet the definition for VIEs and VOEs. The Corporation is required by

GAAP to consolidate a VIE when the Corporation is deemed to be the primary beneficiary. This

determination is evaluated periodically as facts and circumstances change.

A legal entity is referred to as a VIE if any of the following conditions exist: 1) the total equity

investment at risk is insufficient to permit the legal entity to finance its activities without additional

subordinated financial support from other parties; 2) as a group, the holders of the equity

investment at risk lack any of the characteristics of a controlling financial interest; or 3) the equity

investors’ voting rights are not proportional to the economics, and substantially all of the activities

of the entity either involve or are conducted on behalf of an investor that has disproportionally few

voting rights. The Corporation consolidates entities deemed to be VIEs when either the

Corporation or a wholly-owned subsidiary is determined to be the primary beneficiary. The

primary beneficiary analysis is a qualitative analysis based on power and benefits. An enterprise

has a controlling financial interest in a VIE if it has both power and benefits – that is, it has 1) the

power to direct the activities of a VIE that most significantly impact the VIE’s economic

performance (power); and 2) the obligation to absorb losses of the VIE that potentially could be

significant to the VIE and/or the right to receive benefits from the VIE that potentially could be

significant to the VIE (benefits).

Under GAAP, investments in limited partnerships and similar entities that are not VIEs should be

evaluated for potential consolidation under the voting model. The Corporation consolidates VOEs

when either the Corporation or a wholly-owned subsidiary is determined to have control of the

VOE.

22

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Rabbi Trust VIE

The Corporation established a rabbi trust to meet its obligations under certain executive non-

qualified retirement benefits and deferred compensation plans and to mitigate the expense

volatility of the aforementioned retirement plans. The rabbi trust is considered a VIE as the equity

investment at risk is insufficient to permit the trust to finance its activities without additional

subordinated financial support from the Corporation. The Corporation is considered the primary

beneficiary of the rabbi trust as it has the power to direct the activities of the rabbi trust that

significantly affect the rabbi trust’s economic performance and it has the obligation to absorb

losses of the rabbi trust that could potentially be significant to the rabbi trust by virtue of its

contingent call options on the rabbi trust’s assets in the event of the Corporation’s bankruptcy. As

the primary beneficiary of this VIE, the Corporation consolidates the rabbi trust investments,

executive retirement benefits liabilities and deferred compensation plan liabilities. These rabbi

trust investments consist primarily of cash and cash equivalents, U.S. government agency

obligations, equity securities, mutual funds and other exchange-traded funds, and are recorded at

fair value. Changes in fair value are recorded in noninterest income.

Tax Credit Investment VIE

Through a wholly-owned subsidiary, the Corporation is the sole member of a tax credit investment

company through which it consolidates a community development entity (CDE) that is considered

a VIE. The CDE is considered a VIE because as a group, the holders of the equity investment at

risk lack any of the characteristics of a controlling financial interest. The tax credit investment

company is considered the primary beneficiary of the CDE as it has the power to direct the

activities of a VIE that most significantly impact the VIEs economic performance and the

obligation to absorb losses of and the right to receive benefits from the VIE that potentially could

be significant to the VIE.

23

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Bank Owned Life Insurance

Primarily as a result of mergers and acquisitions, the Corporation holds life insurance on the lives

of certain participating executives. The amount reported as an asset on the balance sheet is the

sum of the cash surrender values reported to the Corporation by the various insurance carriers.

Certain policies are split-dollar life insurance policies whereby the Corporation recognizes a

liability for the postretirement benefit related to the arrangement. This postretirement benefit is

included in other liabilities on the balance sheet.

Income Taxes

The Corporation accounts for income taxes under the asset and liability method. Under this

method, deferred tax assets and liabilities are established for the temporary differences between

the accounting basis and the tax basis of the Corporation’s assets and liabilities at enacted tax rates

expected to be in effect when the amounts related to such temporary differences are realized or

settled. A valuation allowance is established if it is considered more likely than not that all or a

portion of the deferred tax assets will not be realized. Interest and penalties paid on the

underpayment of income taxes are classified as income tax expense.

The Corporation periodically evaluates the potential uncertainty of its tax positions as to whether

it is more likely than not its position would be upheld upon examination by the appropriate taxing

authority. A tax position that meets the more-likely-than-not recognition threshold is measured to

determine the amount of benefit to recognize in the consolidated financial statements. The tax

position is measured at the largest amount of benefit that is greater than 50% likely of being

realized upon settlement.

Low Income Housing Tax Credits and Other Tax Credit Investments

As part of its community reinvestment initiatives, the Corporation invests in qualified affordable

housing projects and other tax credit investment projects. The Corporation receives low-income

housing tax credits, investment tax credits, rehabilitation tax credits, solar tax credits and other tax

credits as a result of its investments in these limited partnership investments.

24

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

The Corporation accounts for its investments in qualified affordable housing projects using the

proportional amortization method and amortizes the initial cost of the investment in proportion to

the tax credits and other tax benefits allocated to the Corporation. The amortization of the excess

of the carrying amount of the investment over its estimated residual value is included as a

component of income tax expense. At investment inception, the Corporation records a liability for

the committed amount of the investment. This liability is reduced as contributions are made.

The Corporation evaluates investments in tax credit investment companies for consolidation based

on the variable or voting interest entity guidance, as appropriate.

Other tax credit investment projects are accounted for using either the cost method or equity

method.

Advertising Costs

All advertising costs are expensed in the period in which they are incurred.

Insurance Commissions

Through Eastern Insurance Group LLC, the Corporation acts as an agent in offering property,

casualty and life and health insurance to both personal and commercial customers. Personal lines

insurance products include life, accident and health, automobile, and property and liability

insurance including fire, condominium, home and tenants, among others. Commercial insurance

products include group life and health, commercial property and liability, surety, and workers

compensation insurance, among others. The Corporation recognizes insurance commission

revenues as performance obligations of underlying agreements are satisfied.

Trust Operations

The Bank is a full-service trust company that provides a wide range of trust services to customers

that includes managing customer investments, safekeeping customer assets, supplying

disbursement services, and providing other fiduciary services. Trust assets held in a fiduciary or

agency capacity for customers are not included in the accompanying consolidated balance sheets

as they are not assets of the Corporation. Revenue from administrative and management activities

associated with these assets is recognized as performance obligations of underlying agreements

are satisfied.

25

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Derivative Financial Instruments

Derivative instruments are carried at fair value in the Corporation’s financial statements. The

accounting for changes in the fair value of a derivative instrument is determined by whether it has

been designated and qualifies as part of a hedging relationship, and further, by the type of hedging

relationship. At the inception of a hedge, the Corporation documents certain items, including, but

not limited to, the following: the relationship between hedging instruments and hedged items, the

Corporation’s risk management objectives, hedging strategies, and the evaluation of hedge

transaction effectiveness. Documentation includes linking all derivatives that are designated as

hedges to specific assets or liabilities on the balance sheet or to specific forecasted transactions.

The Corporation’s derivative instruments that are designated and qualify for hedge accounting are

classified as cash flow hedges (i.e., hedging the exposure to variability in expected future cash

flows associated with a recognized asset or liability, or a forecasted transaction). As such, changes

in the fair value of the designated hedging instrument that is included in the assessment of hedge

effectiveness are recorded in other comprehensive income and reclassified into earnings in the

same period or periods during which the hedged forecasted transaction affects earnings. Such

reclassifications shall be presented in the same income statement line item as the earnings effect

of the hedged item.

The Corporation’s derivative instruments not designated as hedging instruments are recorded at

fair value and changes in fair value are recognized in other noninterest income. Derivative

instruments not designated as hedging instruments include interest rate swaps, foreign exchange

contracts offered to commercial customers to assist them in meeting their financing and investing

objectives for their risk management purposes, and risk participation agreements entered into as

financial guarantees of performance on customer-related interest rate swap derivatives. The

interest rate and foreign exchange risks associated with customer interest rate swaps and foreign

exchange contracts are mitigated by entering into similar derivatives having offsetting terms with

correspondent bank counterparties.

All derivative financial instruments eligible for clearing are cleared through the Chicago

Mercantile Exchange (CME). In accordance with its amended rulebook, CME legally

characterizes variation margin payments made to and received from CME as settlement of

derivatives rather than as collateral against derivatives.

26

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Fair Value Measurements

The Fair Value Measurements and Disclosures Topic of the Financial Accounting Standards Board

(FASB) Accounting Standards Codification (ASC) defines fair value as the price that would be

received to sell an asset or paid to transfer a liability in an orderly transaction between market

participants at the measurement date. This Topic also establishes a fair value hierarchy that

prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the

highest priority to unadjusted quoted prices in active markets for identical assets or liabilities

(Level 1 measurements), and the lowest priority to unobservable inputs (Level 3 measurements).

The three levels of the fair value hierarchy are described below:

Level 1 – Inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities

that the reporting entity has the ability to access at the measurement date.

Level 2 – Valuations based on quoted prices in markets that are not active or for which all

significant inputs are observable, either directly or indirectly.

Level 3 – Prices or valuations that require inputs that are both significant to the fair value

measurement and unobservable.

To the extent that valuation is based on models or inputs that are less observable or unobservable

in the market, the determination of fair value requires more judgment. Accordingly, the degree of

judgment exercised by the Corporation in determining fair value is greatest for instruments

categorized in Level 3. A financial instrument’s level within the fair value hierarchy is based on

the lowest level of any input that is significant to the fair value measurement.

Statements of Cash Flows

Supplemental disclosures of cash flow information for the years ended December 31 follows:

Cash paid for:

Interest $ 34,217 $ 23,732

Income taxes $ 31,308 $ 29,731

2019

2018

(In Thousands)

27

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Recent Accounting Pronouncements

Relevant standards that were recently issued but not yet adopted as of December 31, 2019:

Standard Description

Date of

Adoption

Effects on the financial statements or other significant

matters

ASU 2016-02, Leases (Topic

842) and relevant amendments

The standard represents a wholesale change to lease

accounting and requires all leases, other than short-

term leases, to be reported on balance sheet through

recognition of a right-of-use asset and a corresponding

liability for future lease obligations. The standard also

requires extensive disclosures for assets, expenses, and

cashflows associated with leases, as well as a maturity

analysis of lease liabilities.

January 1, 2020

The Corporation adopted this standard on January1, 2020 and

used the effective date as the date of application and, therefore,

periods prior to January 1, 2020 will not be restated. The

Corporation elected the package of practical expedients which

permit the Corporation not to reassess prior conclusions about

lease identification, lease classification, and initial direct costs

under the new standard. The Corporation also elected the

hindsight practical expedient and, therefore, used hindsight

knowledge as of the effective date when determining lease

terms and impairment. In addition, the Corporation elected the

practical expedient to not separate lease and non-lease

components and, therefore, accounts for each separate lease

component of a contract and its associated non-lease

components as a single lease component. The new standard

also provides a practical expedient for an entity’s ongoing

accounting relating to leases of 12 months or less (short-term

leases). The Corporation has elected the short-term lease

recognition exemption for all leases that qualify, and thus will

not recognize right-of-use assets or lease liabilities for those

leases. The adoption of this standard resulted in the recognition

of right-of-use assets and lease liabilities on the Corporation’s

balance sheet for its real estate and equipment operating leases

of $93.0 million and $96.4 million, respectively. The

Corporation also recognized a transition adjustment to the

opening balance of retained earnings on 1/1/2020 amounting to

$1.1 million, net of tax, related to the incremental accrued rent

adjustment calculated as a result of electing hindsight. The

amount of right-of-use assets were determined based upon the

present value of the remaining minimum rental payments under

current leasing standards for existing operating leases, adjusted

for options that the Corporation is reasonably certain to

exercise, less accrued rent as of 12/31/2019 and the

incremental accrued rent as a result of electing hindsight. The

amount of lease liabilities were determined based upon the

present value of the remaining minimum rental payments under

current leasing standards for existing operating leases, adjusted

for options that the Corporation is reasonably certain to

exercise.

28

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Standard Description

Date of

Adoption

Effects on the financial statements or other significant

matters

ASU 2016-13, Financial

Instruments - Credit Losses

(Topic 326): Measurement of

Credit Losses on Financial

Instruments and relevant

amendments

The standard replaces the existing incurred loss

impairment guidance and requires immediate

recognition of expected credit losses for financial

assets carried at amortized cost, including trade and

other receivables, loans and commitments, held-to-

maturity debt securities and other financial assets, held

at the reporting date to be measured based on

historical experience, current conditions and

reasonable and supportable forecasts. The standard

also amends existing impairment guidance for available-

for-sale securities, and credit losses will be recorded

as an allowance versus a write-down of the amortized

cost basis of the security and will allow for a reversal

of impairment loss when the credit of the issuer

improves. The guidance requires a cumulative effect of

the initial application to be recognized in retained

earnings at the date of initial application.

January 1, 2023,

early adoption

permitted

The Corporation continues to assess the impact of the standard

on its consolidated financial statements. To date, the

Corporation has been assessing the key differences and gaps

between its current allowance methodologies and model with

those it is considering to use upon adoption. This has included

assessing the adequacy ofexisting loss data, developing models

for default and loss estimates, and finalizing vendor selection.

The Corporation expects to validate its models and execute a

parallel run beginning in 2021.

ASU 2018-15, Intangibles -

Goodwill and Other - Internal-

Use Software (Subtopic 350-

40): Customer's Accounting

for Implementation Costs

Incurred in a Cloud

Computing Arrangement That

is a Service Contract

This standard addresses accounting for fees paid by a

customer for implementation, set-up and other upfront

costs incurred in a cloud computing arrangement that is

hosted by the vendor, i.e., a service contract. The new

guidance aligns treatment for capitalization of

implementation costs with guidance on internal-use

software.

January 1, 2021,

early adoption

permitted

The Corporation is currently assessing the impact of the new

standard on the Corporation's consolidated financial statements.

29

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

1. Summary of Significant Accounting Policies (continued)

Relevant standards that were adopted during the year ended December 31, 2019:

The Corporation adopted ASU 2014-09, Revenue from Contracts with Customers (Topic 606),

effective January 1, 2019. The standard provides entities with a single model for recognizing

revenue from contracts with customers. The core principle requires an entity to recognize revenue

to depict the transfer of goods or services to customers in an amount that reflects the consideration

that it expects to be entitled to in exchange for those goods or services. In completing its

assessment of those revenue streams within the scope of the guidance, the Corporation did not

identify any revenue sources for which the timing of recognition needed to change under the new

standard. The adoption of this standard on January 1, 2019 did not have a material impact on the

Corporation’s consolidated financial statements, its current accounting policies and practices, or

the timing or amount of revenue recognized. As a result, no adjustment has been made to retained

earnings. However, where appropriate, the Corporation evaluated necessary changes to business

processes, systems, and internal controls in order to support the recognition, measurement, and

disclosure requirements of the new standard.

Effective January 1, 2016, The Corporation early adopted a provision of ASU 2016-01, Financial

Instruments – Overall (Subtopic 825-10): Recognition and Measurement of Financial Assets and

Financial Liabilities, that eliminated the requirement for entities that are not considered public

business entities to disclose the fair value of financial instruments measured at amortized cost.

The Corporation adopted the remaining provisions of the standard effective January 1, 2019.

Under the new standard, all equity securities will be measured at fair value through earnings with

certain exceptions, including investments accounted for under the equity method of accounting or

where the fair market value of an equity security is not readily available. The adoption of this

standard did not have a material impact on the Corporation’s consolidated financial statements.

The preceding listings of relevant standards are not comprehensive listings of all standards to

which the Corporation is subject. Rather, these represent accounting standards that had or have

the potential for having a material impact on the Corporation’s consolidated financial statements.

30

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

2. Mergers and Acquisitions

In 2018, the Corporation acquired certain assets and assumed certain liabilities from the acquisition

of certain insurance agencies for total consideration of $11.5 million in cash. These acquisitions

were considered to be business combinations to be accounted for using the acquisition method

since the Corporation obtained control through the acquisition of the operating assets. As a result

of these business combinations, the Corporation increased its goodwill and insurance agency

intangible assets by $7.7 million and $5.0 million, respectively. The intangible assets recorded as

part of these acquisitions consisted of a $4.4 million customer list intangible asset and a $0.6

million non-compete intangible asset. For tax purposes, the transactions were considered asset

acquisitions and as such, the amortization of goodwill and intangible assets is deductible for tax

purposes. Included in the determination of goodwill was $1.2 million of contingent consideration

based upon a percentage of revenues retained over a period of time after the acquisition dates. The

amount of contingent consideration included in goodwill was based upon management’s best

estimate of possible outcomes. According to the purchase agreements, the contingent

consideration payouts may range from $0 to $1.4 million. Acquisition-related legal and

professional fee costs associated with these agency acquisitions of $0.2 million were charged to

expense in 2018 and were included in the professional fee line item of the consolidated statement

of income.

In 2018, $0.2 million was charged to expense to adjust the acquisition-related contingent

consideration liabilities.

31

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

3. Securities

Trading Securities:

Trading securities, at fair value, were as follows:

The reduction in the above balance is due to the Corporation’s exit of the Capital Markets business

in 2019.

For the years ended December 31, 2019 and 2018, the net unrealized gains and losses on trading

activities for trading securities still held at the reporting date were $2 thousand and $39 thousand,

respectively.

Debt securities:

Municipal bonds and obligations $ 961 $ 52,899

$ 961 $ 52,899

Year Ended December 31

2019

2018

(In Thousands)

32

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

3. Securities

Securities Available for Sale:

The amortized cost, gross unrealized gains and losses, and fair value of securities available for sale

for the periods below were as follows:

A schedule of the contractual maturities of securities available for sale as of December 31, 2019,

follows:

Amortized Unrealized Unrealized Fair

Cost Gains Losses Value

Debt securities

Government-sponsored residential

mortgage-backed securities $ 1,151,305 $ 17,208 $ (545) $ 1,167,968

U.S. Treasury securities 50,155 265 - 50,420

State and municipal bonds and obligations 272,582 10,959 (3) 283,538

Qualified zone academy bond 6,155 155 - 6,310

$ 1,480,197 $ 28,587 $ (548) $ 1,508,236

Amortized Unrealized Unrealized Fair

Cost Gains Losses Value

Debt securities

Government-sponsored residential

mortgage-backed securities $ 1,153,495 $ 1,919 $ (19,277) $ 1,136,137

State and municipal bonds and obligations 321,184 1,883 (9,351) 313,716

Qualified zone academy bond 6,045 - - 6,045

$ 1,480,724 $ 3,802 $ (28,628) $ 1,455,898

December 31, 2019

December 31, 2018

(In Thousands)

(In Thousands)

Amortized Fair

Cost Value

Maturing in one year or less $ 6,576 $ 6,731

Maturing after one year but within five years 67,145 67,954

Maturing after five years but within ten years 276,655 283,210

Maturing after ten years 1,129,821 1,150,341

$ 1,480,197 $ 1,508,236

(In Thousands)

33

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

3. Securities (continued)

Mortgage-backed securities and callable securities are shown at their contractual maturity dates.

However, both are expected to have shorter average lives due to expected prepayments and callable

features, respectively. Included in the securities available for sale at December 31, 2019, were

$266.4 million of callable securities at fair value.

Gross realized gains from sales of securities available for sale were $2.1 million and $0.2 million

for the years ended December 31, 2019 and 2018, respectively. The Corporation had no significant

gross realized losses from sales of securities available for sale for the years ended December 31,

2019 and 2018, respectively.

Management prepares an estimate of the expected cash flows for investment securities available

for sale that potentially may be deemed to have OTTI. This estimate begins with the contractual

cash flows of the security. This amount is then reduced by an estimate of probable credit losses

associated with the security. When estimating the extent of probable losses on the securities,

management considers the credit quality and the ability to pay of the underlying issuers. Indicators

of diminished credit quality of the issuers include defaults, interest deferrals, or “payments in

kind.” Management also considers those factors listed in the Investments – Debt and Equity

Securities topic of the FASB ASC when estimating the ultimate realizability of the cash flows for

each individual security.

The resulting estimate of cash flows after considering credit is then subject to a present value

computation using a discount rate equal to the current yield used to accrete the beneficial interest

or the effective interest rate implicit in the security at the date of acquisition. If the present value

of the estimated cash flows is less than the current amortized cost basis, an OTTI is considered to

have occurred and the security is written down to the fair value indicated by the cash flow analysis.

As part of the analysis, management considers whether it intends to sell the security or whether it

is more than likely that it would be required to sell the security before the expected recovery of its

amortized cost basis.

34

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

3. Securities (continued)

Information pertaining to securities available for sale with gross unrealized losses at December 31,

2019 and 2018, which the Corporation has not deemed to be OTTI, aggregated by investment

category and length of time that individual securities have been in a continuous loss position,

follows:

Gross Gross

# of Unrealized Fair Unrealized Fair

Holdings Losses Value Losses Value

Government-sponsored residential

mortgage-backed securities 1 $ 545 $ 74,550 $ - $ -

State and municipal bonds and obligations 2 3 850 - -

3 $ 548 $ 75,400 $ - $ -

Gross Gross

# of Unrealized Fair Unrealized Fair

Holdings Losses Value Losses Value

Government-sponsored residential

mortgage-backed securities 17 $ - $ - $ 19,277 $ 925,797

State and municipal bonds and obligations 257 978 47,324 8,373 151,562

274 $ 978 $ 47,324 $ 27,650 $ 1,077,359

(In Thousands)

December 31, 2019

December 31, 2018

Less than 12 Months

12 Months or Longer

Less than 12 Months

12 Months or Longer

(In Thousands)

35

Eastern Bank Corporation

Notes to Consolidated Financial Statements (continued)

3. Securities (continued)

The Corporation does not intend to sell these investments and has determined based upon available

evidence that it is more likely than not that the Corporation will not be required to sell each security

before the expected recovery of its amortized cost basis. As a result, the Corporation does not

consider these investments to be OTTI. The Corporation made this determination by reviewing

various qualitative and quantitative factors regarding each investment category, such as current

market conditions, extent and nature of changes in fair value, issuer rating changes and trends, and

volatility of earnings.

As a result of the Corporation’s review of these qualitative and quantitative factors, the causes of