HSMAI SPECIAL REPORT

Hotel Management

Company

Sales Incentive Plans

Produced in partnership with

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

Table of Contents

02 Introduction

03 Why are incentives so important?

04 Framework for sales incentive plan design

05 Incentives overview

06 Sales compensation design

07 Metrics

08 Plan types

09 Payout curves

12 ZS POV

13 State of incentives in hotel management companies

14 Our participants

15 Hotel management company incentive plan summary

21 Appendix

22 Director of sales incentive plan summary

24 Sales manager incentive plan summary

2

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

By Robert A. Gilbert, CHME, CHBA, President and CEO,

Hospitality Sales & Marketing Association International (HSMAI)

A

t a time when everything about hospitality sales is changing, the potential for

incentive plans to recognize and motivate sales professionals has never been more

important. But what makes for an effective, impactful incentive program?

HSMAI has partnered with ZS Associates on an original study that addresses this very

question for hotel management companies (HMCs). This report — made possible with the

support of HSMAI Organizational Member companies — presents the results of our study.

Drawing on data that ZS collected from 39 HMCs, the report begins with a general outline

of the five guiding principles and three defining traits of a good sales incentive plan as well

as the advantages and disadvantages of different types of plans. Then we share key findings

from the HMCs that ZS surveyed, including the predominant structure, performance

metrics, maximum payouts, and payout frequency of their incentive plans for both

directors of sales and sales managers.

You’ll also find information about the HMCs that generously contributed data to this

study, which we hope is a valuable resource for your organization as you design an

incentive plan that empowers and elevates your sales professionals.

Hospitality Sales & Marketing

Association International (HSMAI)

is the hospitality industry’s leading

advocate for intelligent, sustainable hotel

revenue growth. HSMAI provides hotel

professionals and their partners with tools,

insights, and expertise to fuel sales, inspire

marketing, and optimize revenue through

programs such as HSMAI’s Revenue

Optimization Conference, Digital Marketing

Strategy Conference, Sales Leader

Forum, and Adrian Awards. HSMAI oers

organizational and individual membership,

with more than 7,000 members in four

global regions — the Americas, Asia Pacific,

Europe, and the Middle East. — hsmai.org

ZS is a professional services firm that works

side by side with companies to help develop

and deliver products that drive customer

value and company results. — zs.com

ABOUT HSMAI

ABOUT ZS

introduction

3

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

Why are incentives

so important?

Three entities are impacted by the incentive plan:

Company

Customer

Sales Force

Sales force drives

the top-line

Output is typically

measurable

Need to

acknowledge success

Lack of supervision

why are incentives so important?

4

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

Framework for

sales incentive

plan design

5

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

Incentives Overview

We need to look at the entire sales compensation spectrum

when thinking about a sales compensation program

Compensation Guiding Principles

Strategic | Motivational | Simple | Fair | Fiscally Responsible

Eligibility

Metrics Methods Mechanics

Plan Period

Additional

Elements

Pay Level & Mix

Plan Design

What are

the criteria

for a role to

receive sales

compensation?

ɠ Customer

contact

ɠ Financial

influence

What level of

base and

variable pay is

appropriate?

What should be

the measuring

metric for each

of the identified

components?

ɠ $ sales

ɠ Unit sales

ɠ Orders

ɠ Gross

margin

What plan type

to choose from?

ɠ Commission

ɠ Goal based

ɠ Forced

ranking

ɠ Matrix

ɠ MBOs

ɠ Combination

What will the

payout curve

look like?

ɠ Threshold

ɠ Slopes

ɠ Accelerators

ɠ Kickers

ɠ Caps

How long is the

plan period?

What is the

payout

frequency?

ɠ Monthly

ɠ Quarterly

ɠ Semi-

annually

ɠ Annually

ɠ SPIFs/

contests

ɠ Recognition

program

ɠ Long-term

incentives

$200K

$50K

100%

salary

100%

incentive

6

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

Guiding Principles: A good incentive plan

is strategic, motivational, fair, simple,

and fiscally responsible

Why do so many companies

have diiculties designing

their IC plans?

Sales Compensation Design

Answer: There are tensions

between the guiding principles.

Simple

Controllable

Motivational

Fair

Measurable

Financially

responsible

ɠ Supports sales and marketing objectives

ɠ Focuses on the “right” activities and customers

ɠ Proper emphasis / focus on key products

ɠ Flexible to account for changes in environment

ɠ Sellers with dierent conditions have similar

earning potential

ɠ Does not penalize sellers for forecasting uncertainties

ɠ Simple to understand and communicate to the sales force

ɠ Can be implemented given IC infrastructure/resources

ɠ Total payout is within acceptable range of budget

ɠ Total payout varies appropriately according

to company success

ɠ Substantial eort leads to significant reward

ɠ Keeps most people engaged

ɠ Focus on what matters to salespeople

Aligned with strategy

Motivational

Fair

Simple

Fiscally responsible

7

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

There are many decisions that can

be made with regard to metrics,

and each has an impact on

representative behavior.

Measurement

Level

Point of Comparison

ɠ Revenue

ɠ RevPAR

ɠ Room nights

ɠ Bookings

ɠ Person/territory

ɠ Property

ɠ Account (above property)

ɠ Other team

ɠ Relative to goal

ɠ Change over time (percent, value)

Ideally, sales incentive plan metrics should

be strategic, controllable, and measurable

Metrics

Strategic

Controllable

Measurable

ɠ Supports key strategic goals

ɠ Critical to the business

ɠ Mostly within the control of the salesperson

ɠ Visibility of the link between behavior

and reward

ɠ Metric can be measured at the appropriate

level

ɠ Systems are able to track and report

on the metric

Dimensions

Requiring a Decision

Sales incentive plans should

be limited to 3 metrics, each

weighted at least 20%

3

KEY TAKEAWAY

8

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

Plan Types

Each incentive plan type has relative advantages and disadvantages;

each is appropriate in certain circumstances

Commission Plan Relative Plan Goal Based PlanMatrix Plan MBO Plan

ɠ New products

ɠ Hunters

ɠ Territory potential

must be balanced

ɠ Minimizes

forecasting issues

ɠ Can cause

unhealthy

competition

ɠ Uncommon

ɠ Territory potential

considered

ɠ Requires accurate

national forecast

ɠ Prevalent for AMs

ɠ Used to balance

competing priorities

ɠ Complex

ɠ Uncommon

ɠ Can be subjective

ɠ Little pay

dierentiation

ɠ Administrative

burden

ɠ May not require

sales data

PAY

% OF

SALES

Goal Attainment

Pay

Objective 1 25%

Objective 2 15%

Objective 3 35%

Objective 4 25%

------------------------

Total 100%

HSMAI

© 2019 ZS | CONFIDENTIAL

− 9−

Each incentive plan type has relative advantages and disadvantages;

each is appropriate in certain circumstances

Plan Types

Objective 1 25%

Objective 2 15%

Objective 3 35%

Objective 4 25%

------------------------

Total 100%

Pay 5%

of sales

Goal Attainment

Pay

§ Minimizes

forecasting

issues

§ Can cause

unhealthy

competition

§ Uncommon

§ Used to balance

competing

priorities

§ Complex

§ Uncommon

§ Territory

potential

considered

§ Requires

accurate

national

forecast

§ Prevalent for

AMs

§ New products

§ Hunters

§ Territory

potential must

be balanced

§ Can be

subjective

§ Little pay

differentiation

§ Administrative

burden

§ May not require

sales data

Commission

Plan

Relative

Plan

Matrix

Plan

Goal Based

Plan

MBO

Plan

HSMAI

© 2019 ZS | CONFIDENTIAL

− 9−

Each incentive plan type has relative advantages and disadvantages;

each is appropriate in certain circumstances

Plan Types

Objective 1 25%

Objective 2 15%

Objective 3 35%

Objective 4 25%

------------------------

Total 100%

Pay 5%

of sales

Goal Attainment

Pay

§ Minimizes

forecasting

issues

§ Can cause

unhealthy

competition

§ Uncommon

§ Used to balance

competing

priorities

§ Complex

§ Uncommon

§ Territory

potential

considered

§ Requires

accurate

national

forecast

§ Prevalent for

AMs

§ New products

§ Hunters

§ Territory

potential must

be balanced

§ Can be

subjective

§ Little pay

differentiation

§ Administrative

burden

§ May not require

sales data

Commission

Plan

Relative

Plan

Matrix

Plan

Goal Based

Plan

MBO

Plan

9

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

-7

-4

-2

-13

-17

Payout Curves

Laggards

Bottom 20% Top 20%

Stars

Middle 60%

Core Performers

-10

Percent reduction in revenue seen, by segment, when no overachievement commission rates were present

Percent reduction in revenue seen, by segment, when no quarterly bonuses were present

Research suggests

more frequent

performance period

evaluation drives

higher sales,

particularly for low

performers

Research suggests

that overachievement

commission rates are

critical in driving top

performers

SOURCE: HARVARD BUSINESS REVIEW, JULYAUGUST

What does the research say about payouts?

10

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

Payout Curves

Caps reduce the motivation of your top performers

Improvement in revenue

after caps were removed

from the plan

9%

RESEARCH SETTING

Data were collated from the sales

organization of a large U.S. contact

lens manufacturer

KEY TAKEAWAY

Payout curves can be designed such that the right amount of money is paid to the right population

GUIDING PRINCIPLE OBJECTIVE METRIC REP BENCHMARK

MANAGER

BENCHMARK

Motivating

Engagement rate Percent receiving payout 90-100% 100%

Meaningful engagement rate Percent paid at least 75% of target $ payout 60-80% 60-80%

Pays for performance;

Fiscally responsible

Median % of target payout Percent of target payout received at the median 100% 100%

Average % of target payout Percent of target payout received on average 100-110% 100-110%

Excellence to target ratio Top 10% $ payout vs. target 200-300% 150-200%

Bottom performer vs. target ratio Bottom 10% payout vs. target 10-30% 30-50%

0%

50%

100%

150%

200%

250%

300%

100%0% 200%

% of Target Paid

% of Quota Attained

Uncapped

Capped

11

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

0% 50%25% 100% 125%75% 150% 175%

200%

0%

50%

100%

150%

200%

250%

300%

Payout Curves

An optimal payout curve considers performance in four payout zones

Too many salespeople below threshold can result in:

ɠ Loss of motivation / morale

ɠ Account managers holding back sales until next pay period

ɠ Loss of confidence in sales management

ɠ Note: A high threshold suggests very strong forecasting ability

Too many in the windfall zone can result in:

ɠ Overpayment

ɠ Culture of entitlement

ɠ Low incentive to drive sales (reduced slope)

ɠ Account managers holding back sales until next pay period

Underperformers

Receive no payout

Good performers

Increased payout for

increased sales

Overachiever

Accelerated payout rate

for increased sales

Windfall possibility

Payout may be due

to windfall conditions rather

than performance

Percent of Target Payout

Attainment

Payout

Threshold

Decelerator

Point

Target

Payout

Attainment

Distribution

12

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

ZS POV

Based on our experience, eective quota-setting processes

include a variety of common characteristics

Territory Opportunity Rigorous Methodology Manager Refinement

ɠ Territory potential must

be incorporated

ɠ Can include multiple metrics

related to accounts or geographic

elements

ɠ Typical metrics include account

characteristics and population

demographics

ɠ Accuracy is tested using

historical simulations to check for

correlations to actual sales results

ɠ Fairness is evaluated by

grouping territories with similar

characteristics and observing

any historical biases

ɠ Local knowledge helps refine

quotas to reflect on-the-ground

reality and increases buy-in of

sales managers

ɠ Reasonable limits on the degree

of change should be imposed,

as well as a rigorous process

HSMAI

© 2019 ZS | CONFIDENTIAL

− 16 −

Based on our experience, effective quota-setting processes include a

variety of common characteristics…

ZS POV

§ Territory potential must

be incorporated

§ Can include multiple metrics

related to accounts or

geographic elements

§ Typical metrics include

account characteristics and

population demographics

§ Accuracy is tested using

historical simulations to

check for correlations to

actual sales results

§ Fairness is evaluated by

grouping territories with

similar characteristics and

observing any historical

biases

§ Local knowledge helps refine

quotas to reflect on-the-

ground reality and increases

buy-in of sales managers

§ Reasonable limits on the

degree of change should be

imposed, as well as a

rigorous process

Territory Opportunity Rigorous Methodology Manager Refinement

20

60

100

140

160

Low Medium High

PREVIOUS-YEAR GROWTH

% GOAL ATTAINMENT CURRENT YEAR

40

80

120

20

60

100

140

160

Low Medium High

PREVIOUS-YEAR GROWTH

% GOAL ATTAINMENT CURRENT YEAR

40

80

120

20

60

100

140

160

Low Medium High

PREVIOUS-YEAR GROWTH

% GOAL ATTAINMENT CURRENT YEAR

40

80

120

HSMAI

© 2019 ZS | CONFIDENTIAL

− 16 −

Based on our experience, effective quota-setting processes include a

variety of common characteristics…

ZS POV

§ Territory potential must

be incorporated

§ Can include multiple metrics

related to accounts or

geographic elements

§ Typical metrics include

account characteristics and

population demographics

§ Accuracy is tested using

historical simulations to

check for correlations to

actual sales results

§ Fairness is evaluated by

grouping territories with

similar characteristics and

observing any historical

biases

§ Local knowledge helps refine

quotas to reflect on-the-

ground reality and increases

buy-in of sales managers

§ Reasonable limits on the

degree of change should be

imposed, as well as a

rigorous process

Territory Opportunity Rigorous Methodology Manager Refinement

20

60

100

140

160

Low Medium High

PREVIOUS-YEAR GROWTH

% GOAL ATTAINMENT CURRENT YEAR

40

80

120

20

60

100

140

160

Low Medium High

PREVIOUS-YEAR GROWTH

% GOAL ATTAINMENT CURRENT YEAR

40

80

120

20

60

100

140

160

Low Medium High

PREVIOUS-YEAR GROWTH

% GOAL ATTAINMENT CURRENT YEAR

40

80

120

HSMAI

© 2019 ZS | CONFIDENTIAL

− 16 −

Based on our experience, effective quota-setting processes include a

variety of common characteristics…

ZS POV

§ Territory potential must

be incorporated

§ Can include multiple metrics

related to accounts or

geographic elements

§ Typical metrics include

account characteristics and

population demographics

§ Accuracy is tested using

historical simulations to

check for correlations to

actual sales results

§ Fairness is evaluated by

grouping territories with

similar characteristics and

observing any historical

biases

§ Local knowledge helps refine

quotas to reflect on-the-

ground reality and increases

buy-in of sales managers

§ Reasonable limits on the

degree of change should be

imposed, as well as a

rigorous process

Territory Opportunity Rigorous Methodology Manager Refinement

20

60

100

140

160

Low Medium High

PREVIOUS-YEAR GROWTH

% GOAL ATTAINMENT CURRENT YEAR

40

80

120

20

60

100

140

160

Low Medium High

PREVIOUS-YEAR GROWTH

% GOAL ATTAINMENT CURRENT YEAR

40

80

120

20

60

100

140

160

Low Medium High

PREVIOUS-YEAR GROWTH

% GOAL ATTAINMENT CURRENT YEAR

40

80

120

13

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

State of incentives

in hotel management

companies

14

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

ɠ AMResorts

ɠ Atlific Hotels

ɠ Atrium Hospitality

ɠ Benchmark Global Hospitality

ɠ Charlestowne Hotels

ɠ Commonwealth Hotels

ɠ Crescent Hotels and Resorts

ɠ Donohoe Hospitality Services

ɠ Dow Hotel Company

ɠ Genuine Hospitality

ɠ GF Management

ɠ Growth Properties

Hospitality Management

ɠ HHM Hospitality

ɠ HVMG - Hospitality Ventures

Management Group

ɠ Hostmark

ɠ HVS Hotel Management

ɠ Interstate Hotels

ɠ Kessler Collection

ɠ Lodging Hospitality Management

ɠ M&R Hotel Management

ɠ Marcus Hotels & Resorts

ɠ NCG - North Central Group

ɠ Newport Hospitality Group

ɠ OTO Development

ɠ Outrigger Enterprises Group

ɠ Pacifica Hotels

ɠ Prism Hotels

ɠ Regency Hotel Management

ɠ Remington Hotels

ɠ Sage Hotels

ɠ Salamander Hotels

ɠ Shaner Hotel Group

ɠ Sound Hospitality Management

ɠ StayPineapple

ɠ Two Roads/CoralTree Hospitality

ɠ White Lodging

ɠ Widewaters Hotels

ɠ Windsor Capital Group

(WCG Hotels)

ɠ Wright Investments

our Participants

We collected incentive

plans from 39 hotel

management companies

15

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

Some “Other” responses include Market Share, House Profit, STR & Revenue Based, Overall Hotel Performance, GOP, Shop Evaluation, Customer Service Scores, and Communications.

0%

100%

0%

100%

Hotel management companies use goal-based plans as

the dominant compensation structure

Hotel companies are simplifying

their plans by carrying fewer metrics

Hotel Management Company Incentive Plan Summary

Incentive Compensation Structure

Number of Performance Metrics

Used in Compensation Plan

97%

6%

4% 4%

29%

12%

35%

18%

18%

18%

9%

7%

40%

27%

23%

7%

43%

37%

18%

45%

94%

3%

Goal based

1

MBO

2

Commission

3

Other*

4 5+

3% 3% 3%

6%

Percentage of Respondents

Number of Metrics Used

to Evaluate Incentive Amount

Director of Sales

HSMAI management

company sample

(N=35)

Sales Manager

HSMAI management

company sample

(N=33)

Previous Study Today’s Sample

Director

of Sales

(n=17)

Director

of Sales

(n=35)

Sales

Manager

(n=12)

Sales

Manager

(n=33)

As compared to our previous study, the majority of companies

build their incentive compensation plans using 3 or fewer metrics

16

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

0%

100%

* “Primary” metrics have the highest weight of all performance metrics that contribute to determining the total target incentive payout amount; sample metrics are listed in order of popularity.

Revenue is the primary metric for

both DOS and Sales Managers

Hotel Management Company Incentive Plan Summary

Primary* Performance Metric Used to Determine Incentive Compensation

Revenue: Total Hotel Contribution Revenue: Individual Contribution RevPAR

Percentage of Respondents

Director of Sales (N=35)

Primary Metric

Sales Manager (N=33)

Primary Metric

Management

companies are

mostly aligned with

metrics: hotel/team

revenue for DOS and

individual revenue

for managers, with

differences tied to

budget, targets, and

consumption

Sample

Metrics

Sample

Metrics

23%

81%

11% 12%

66%

8%

RevPAR

ɠ RevPAR Index

ɠ RevPAR vs. Budget

ɠ RevPAR Index YOY

ɠ RevPAR Index vs.

Budget

ɠ Budgeted RevPAR

Penetration

ɠ RevPAR Rank

Revenue: Total

Hotel Contribution

ɠ Total Hotel

Revenue vs. Budget

ɠ Room Revenue vs.

Budget

ɠ Team Consumed

Revenue

ɠ Team Consumed

Rev. vs. Budget

ɠ Team Bookings vs.

Budget

Revenue: Individual

Contribution

ɠ Individual Bookings

vs. Target

ɠ Individual

Consumed

Revenue vs. Target

ɠ Individual

Consumed Reve-

nue vs. Budget

ɠ Individual Revenue

vs. Budget

ɠ Individual Revenue

Consumption vs.

Budget

Sales Managers have metrics

based on individual contributions

far more often than DOS.

17

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

0%

100%

Hotel Management Company Incentive Plan Summary

Some plans also place a lower weight on Gross Overall Profit

and Guest Satisfaction metrics to determine incentive pay

All Performance Metrics Used to Determine Incentive Compensation

Sample Metrics are listed in order of popularity.

Revenue: Total Hotel Contribution Revenue: Individual Contribution RevPAR GOP OtherGuest Satisfaction

% Weight in the Sales Comp Plan

Director of Sales (n=35)

All Metrics

Sales Manager (n=33)

All Metrics

Usage of RevPAR

as performance

metric has remained

constant across

the companies as

compared to the

previous study

Sample

Metrics

Sample

Metrics

18%

22%

7%

7%

4%

42%

19%

5%

3%

3%

42%

27%

Gross Overall Profit

ɠ Gross Overall Profit

ɠ Gross Overall

Profit - Budget

Guest Satisfaction

ɠ Guest Satisfaction

Score

ɠ Guest & Associate

Satisfaction

ɠ Brand Guest

Service Score

18

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

0%

60%

Hotel Management Company Incentive Plan Summary

The majority of plans we collected were capped, and the max payouts

for Sales Manager and DOS have converged at 30% of base

Maximum Incentive Payout (Percentage of Base Salary)

Maximum Payout (Percentage of Base Salary)

Director of Sales

(n=25)

Sales Manager

(n=26)

High performers

for Sales Managers

averaged 28% in

a previous study,

slightly lower than

today’s sample

50%

10%

30%30%

50%

10%

Maximum

Minimum

Average

28% typical

max payout from

previous study

35% typical

max payout

from previous

study

88% 84%

% of Plans That

Have Pay Caps

19

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

60%

80%

100%

120%

140%

160%

180%

200%

220%

Hotel Management Company Incentive Plan Summary

Ranges for minimum and maximum goal attainment to determine incentive

pay vary by company; most sit between 95% and 125% attainment

Companies C – O award a fraction of their incentive

pay if they achieve close to 100% of their goal

Companies P – W award incentive pay

only if they achieve 100% of their goal

Percent Goal Attainment Required for Minimum and Maximum Incentive Pay

Percent of Target Payout

All Companies Using Thresholds and Caps (n=23)

Minimum thresholds for DOS and Sales Managers averaged

98% in a previous study, similar to our current sample

22% currently have

max payout of 100%

35% currently have 100%

as minimum threshold

Range 30%

A

100%

70%

30%

C

120%

90%

30%

I

130%

95%

35%

J

125%

95%

15%

K

115%

95%

10%

D

100%

90%

10%

T

115%

100%

15%

U

110%

100%

15%

V

108%

100%

20%

B

100%

80%

20%

E

111%

91%

20%

G

200%

95%

23%

N

120%

98%

25%

Q

125%

100%

25%

S

115%

100%

21%

R

121%

100%

2%

O

100%

98%

8%

P

125%

100%

8%

W

108%

100%

45%

H

140%

95%

5%

F

200%

95%

105%

L

110%

95%

105%

M

100%

95%

Maximum Payout

(Higher performance will

not increase pay)

Minimum Payout

(Lower performance will

result in no incentive pay)

20

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

0%

100%

*The Performance Period and Incentive Payout Frequency are the same for each company in our sample.

Hotel management companies most commonly pay out

incentives quarterly to both DOS and Sales Managers

Hotel Management Company Incentive Plan Summary

Frequency of Performance Period and Incentive Payout*

Quarterly and Annually Annually Quarterly

Director of Sales

(N=31)

Sales Manager

(N=30)

The distribution of

performance period and

payout frequency is roughly

the same as those reported

in a previous study

23%

21%

9%

68%

79%

For companies that pay quarterly and annually:

Quarterly payments tend to be based on revenue metrics such as RevPAR; annual payments tend to be based on GOP or guest satisfaction metrics.

21

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

Appendix:

Plan component details

22

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

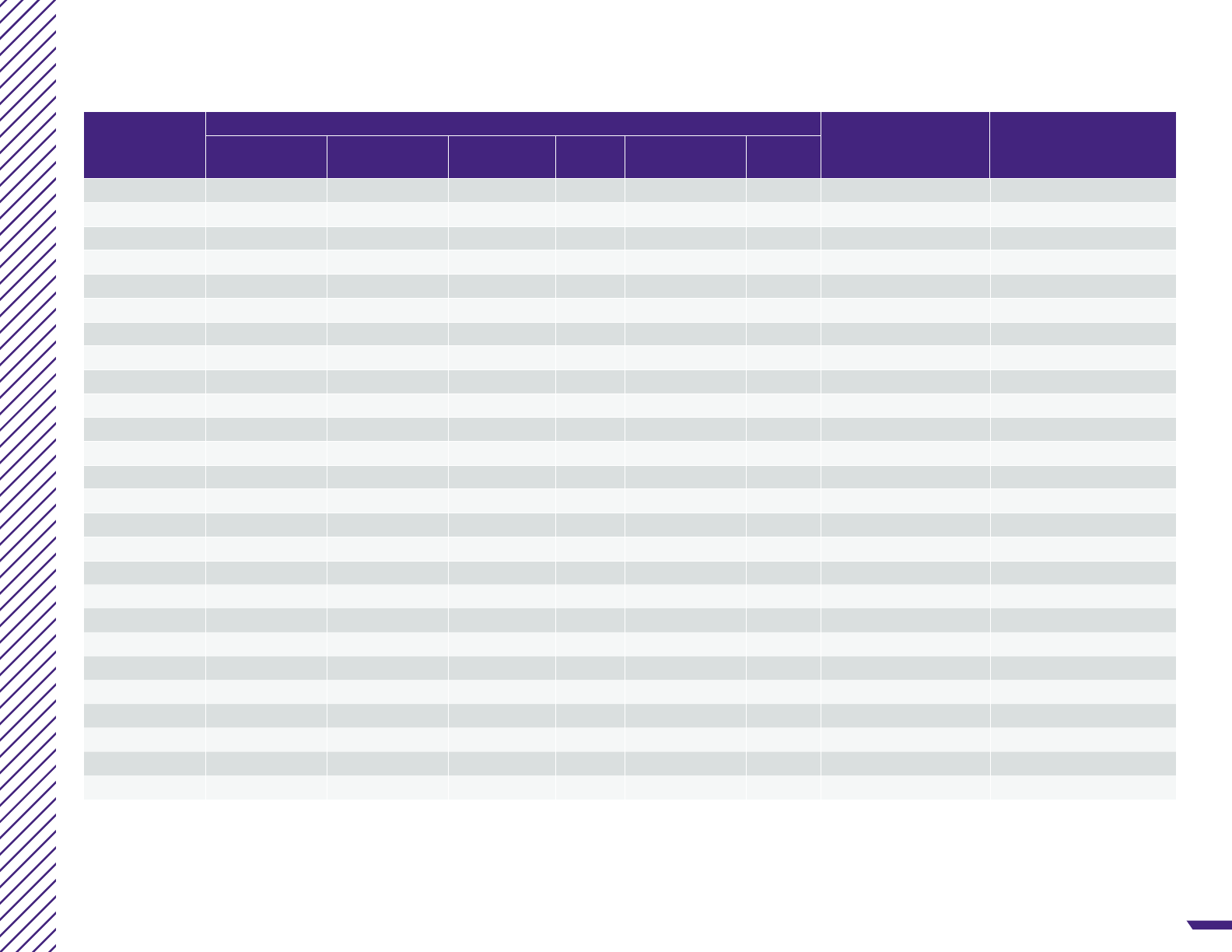

Director of Sales Incentive Plan Summary (1/2)

Sample

Performance Metrics

1

Max Payout

(% of Base)

Payout Frequency

Revenue

Team

Revenue

Indiv.

RevPAR GOP

Revenue to

Budget

Other

2

A X X 25% Annual

B X X X 35% Annual & Quarterly

C X X X Uncapped Quarterly

D X Uncapped Annual & Quarterly

E X X X 40% Quarterly

F X X X 25% Q & 15% A Annual & Quarterly

G X GK GK Uncapped Annual & Quarterly

H X X X 12.5% Quarterly

I X GK X 30% Quarterly

J X GK X X Uncapped Quarterly

K X Uncapped Quarterly

L X X X X Uncapped Annual & Quarterly

M X X X 37% Semi-Annual & Quarterly

N X X X X 30% Annual & Quarterly

O X

X GK X X 30% Annual & Quarterly

P X Uncapped Quarterly

Q X X X X 20% Annual

R X X X Uncapped Quarterly

S X X X X 57% Annual & Quarterly

T X X X 15% Quarterly

U X X 35% Quarterly

V X X X X 20% Quarterly

W X X X 25% Quarterly

X X X X 30% Annual & Quarterly

Y X X X $3,000 Quarterly

Z X X X X 50% Quarterly

1) Performance metrics: “X” indicate category used in incentive plan and “GK” indicates gatekeeper required for incentives to be paid out.

2) “Other” metrics include: sales activities, catering/banquet revenues, employee satisfaction scores, guest scores, physical state of hotel, etc.

23

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

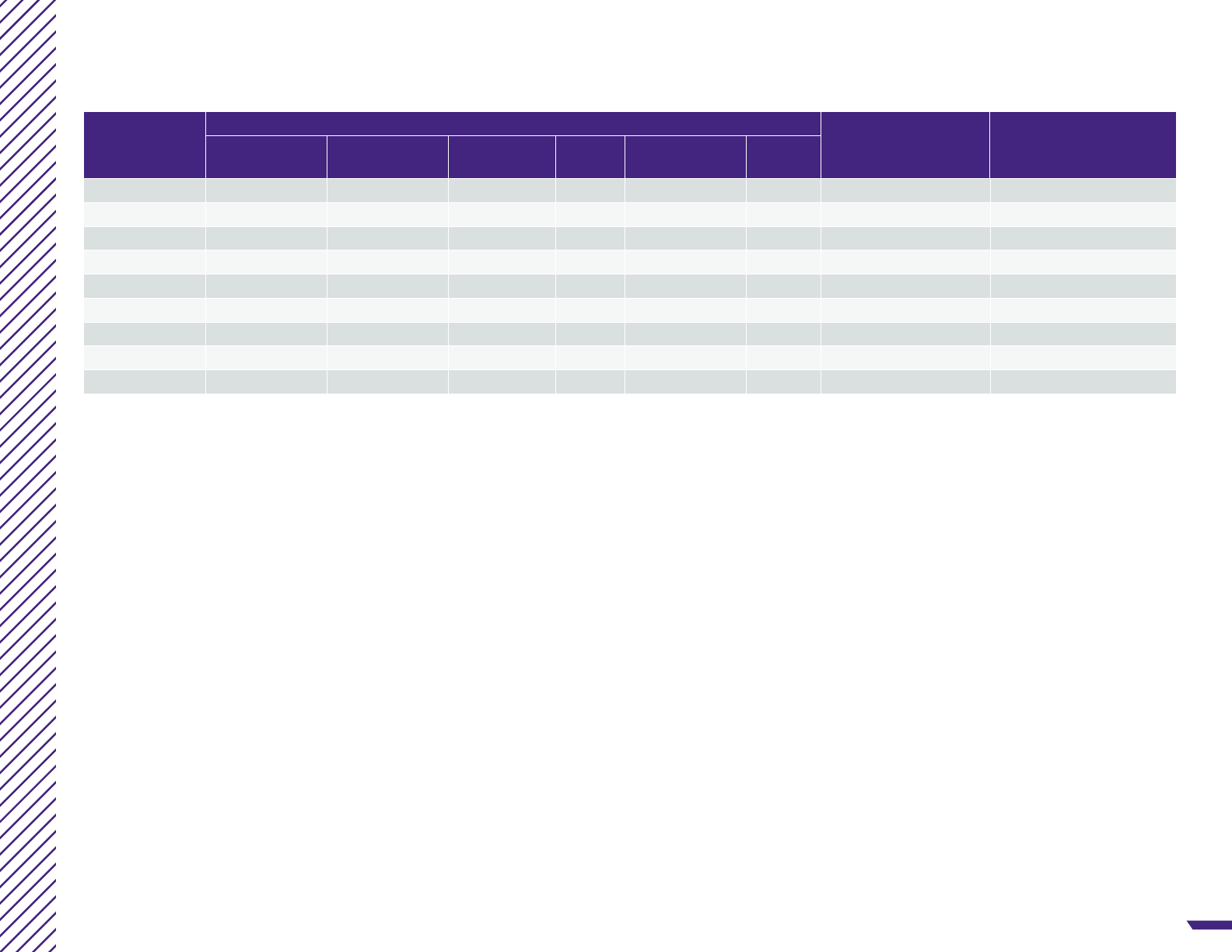

Director of Sales Incentive Plan Summary (2/2)

Sample

Performance Metrics

1

Max Payout

(% of Base)

Payout Frequency

Revenue

Team

Revenue

Indiv.

RevPAR GOP

Revenue to

Budget

Other

2

AA X X X X X X 30% Annual

AB X X GK $17,500 Quarterly

AC X X X 17.5% Annual & Quarterly

AD X X X 35% Annual

AE X X 24% Annual

AF X X X 35% Annual & Quarterly

AG X GK Uncapped Annual & Quarterly

AH GK X X 50% Quarterly

AI X X X 25% Annual & Quarterly

1) Performance metrics: “X” indicate category used in incentive plan and “GK” indicates gatekeeper required for incentives to be paid out.

2) “Other” metrics include: sales activities, catering/banquet revenues, employee satisfaction scores, guest scores, physical state of hotel, etc.

24

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

Sales Manager Incentive Plan Summary (1/2)

Sample

Performance Metrics

1

Max Payout

(% of Base)

Payout Frequency

Revenue

Team

Revenue

Indiv.

RevPAR GOP

Revenue to

Budget

Other

2

A X X X X X 32% Annual & Quarterly

B X X Uncapped Quarterly

C X Uncapped Annual & Quarterly

D X X 35% Quarterly

E X X X X Uncapped Quarterly

F X X GK GK Uncapped Quarterly

G X X 25% Quarterly

H X X GK Uncapped Quarterly

I

X

GK

Uncapped Annual & Quarterly

J X X X Uncapped Annual & Quarterly

K X X X 19% Semi-Annual & Quarterly

L

X

GK

X 30% Quarterly

M

X

GK

Uncapped Annual & Quarterly

N X Uncapped Quarterly

O X X X 20% Annual

P X X X X Uncapped Quarterly

Q

X

X 31% Annual and Quarterly

R

X X X 15% Quarterly

S X X 7% Quarterly

T X X X 20% Quarterly

U X X X X 20% Quarterly

V X X X 50% Annual & Quarterly

W X X X 25% Quarterly

X X X 30% Annual & Quarterly

Y X X 25% Quarterly

Z X X GK $17,500 Quarterly

1) Performance metrics: “X” indicate category used in incentive plan and “GK” indicates gatekeeper required for incentives to be paid out.

2) “Other” metrics include: sales activities, catering/banquet revenues, employee satisfaction scores, guest scores, physical state of hotel, etc.

25

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

Sales Manager Incentive Plan Summary (2/2)

Sample

Performance Metrics

1

Max Payout

(% of Base)

Payout Frequency

Revenue

Team

Revenue

Indiv.

RevPAR GOP

Revenue to

Budget

Other

2

AA X X X 17.5% Annual & Quarterly

AB X X X GK X 25% Annual & Quarterly

AC X X

X

GK

X 30% Annual & Quarterly

AD X $35,000 Annual & Quarterly

AE X GK Uncapped Annual & Quarterly

AF X X GK 40% Quarterly

AG X X 20% Annual & Quarterly

1) Performance metrics: “X” indicate category used in incentive plan and “GK” indicates gatekeeper required for incentives to be paid out.

2) “Other” metrics include: sales activities, catering/banquet revenues, employee satisfaction scores, guest scores, physical state of hotel, etc.

26

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

http://www.seeklogo.net

C=0 M=26 J=56 N=0

C=22 M=42 J=65 N=20

ACCOR

LOGO

Nº dossier : 18J3476

Date : 4/07/18

Validation DA/DC :

Validation Client :

This report is presented with the support of HSMAI’s Organizational Member companies:

Diamond Members

Emerald Members

Sapphire Members

Ruby Members Start-Up Members University Members

Avvio

The Breakers

Cendyn

Cvent

Diamond Resorts

Duetto

Explore St. Louis

GitGo

Google

Host Hotels

Hostmark

IDeaS Revenue Solutions

JD Power

Kessler Collection

Marcus Hotels & Resorts

Marketo,

An Adobe Company

Milestone

MMGY Global

Nor1

OTA Insight

Outrigger Enterprises Group

Rainmaker

Regency Hotel Management

SearchWide

Spire Hospitality

STR

Venetian/Palazzo

Visit Dallas

Visit Tampa Bay

Burgess Crest

CoralTree Hospitality Group

Dragonfly Hospitality

Resources

Hospitality Digital Marketing

IVvy INC.

Kate Burda & Company

Navesink Advisory Group, LLC

Tim Peter & Associates

Cornell University

Johnson & Wales University

Michigan State University

Penn State University

University of Nevada

Las Vegas

Virginia Tech

27

HMC Sales Incentive Plans HSMAI SPECIAL REPORT

hsmai.org