Version 3.0

12 January 2021

PSD2 SCA for Remote

Electronic Transactions

Implementation Guide

January 2021

Version 3.0

12 January 2021

2

Contents

Important Information ............................................................................................................ 4

Using this document ................................................................................................................ 5

1. Introduction: Visa’s guiding principles for PSD2 .......................................................... 8

1.1 Introduction............................................................................................................................................ 8

1.2 Visa’s guiding principles .................................................................................................................... 8

2. The requirements of PSD2 Strong Customer Authentication and Visa’s

interpretation ........................................................................................................................... 9

2.1 The application of SCA and use of factors ................................................................................. 9

2.2 Exemptions .......................................................................................................................................... 12

2.3 Out of scope transactions .............................................................................................................. 13

2.4 Dynamic linking ................................................................................................................................. 16

2.5 Visa PSD2 Solutions and GDPR .................................................................................................... 16

3. Visa’s PSD2 solutions ...................................................................................................... 18

3.1 Solution summary ............................................................................................................................. 18

3.2 Authorization options ...................................................................................................................... 20

3.3 3-D Secure ........................................................................................................................................... 41

3.4 Visa’s PSD2 solutions using Visa Token Service (VTS) ........................................................ 58

3.5 Visa Rules & policies for authentication & authorization under PSD2......................... 62

3.6 Visa Trusted Listing .......................................................................................................................... 63

3.7 Visa Delegated Authentication .................................................................................................... 65

3.8 Visa Pre-dispute products.............................................................................................................. 67

3.9 The Visa MIT Framework ................................................................................................................ 69

3.10 Visa Biometrics ................................................................................................................................... 81

3.11 Visa Consumer Authentication Service ..................................................................................... 81

4. Optimizing the payment experience under PSD2 ....................................................... 82

4.1 Introduction......................................................................................................................................... 82

4.2 Key principles ...................................................................................................................................... 83

4.3 Step by step guide to SCA optimisation ................................................................................ 101

4.4 Liability for fraud-related chargeback ..................................................................................... 109

4.5 Additional guidance on application of the exemptions ................................................... 112

4.6 Challenge Design Best Practice ................................................................................................. 121

4.7 Additional Guidelines for Issuers ............................................................................................. 125

Version 3.0

12 January 2021

3

4.8 EMV 3DS and authorization fall-back options ..................................................................... 132

4.9 Visa Direct and SCA under PSD2 ............................................................................................... 137

4.10 Visa Secure Remote Commerce/Click to Pay ...................................................................... 139

4.11 Visa Secure Authentication Technology and non-Visa Transactions .......................... 139

5. Payment use cases and sector specific guidance for merchants and PSPs ............ 140

6. Bibliography ................................................................................................................. 141

A Appendices ................................................................................................................... 154

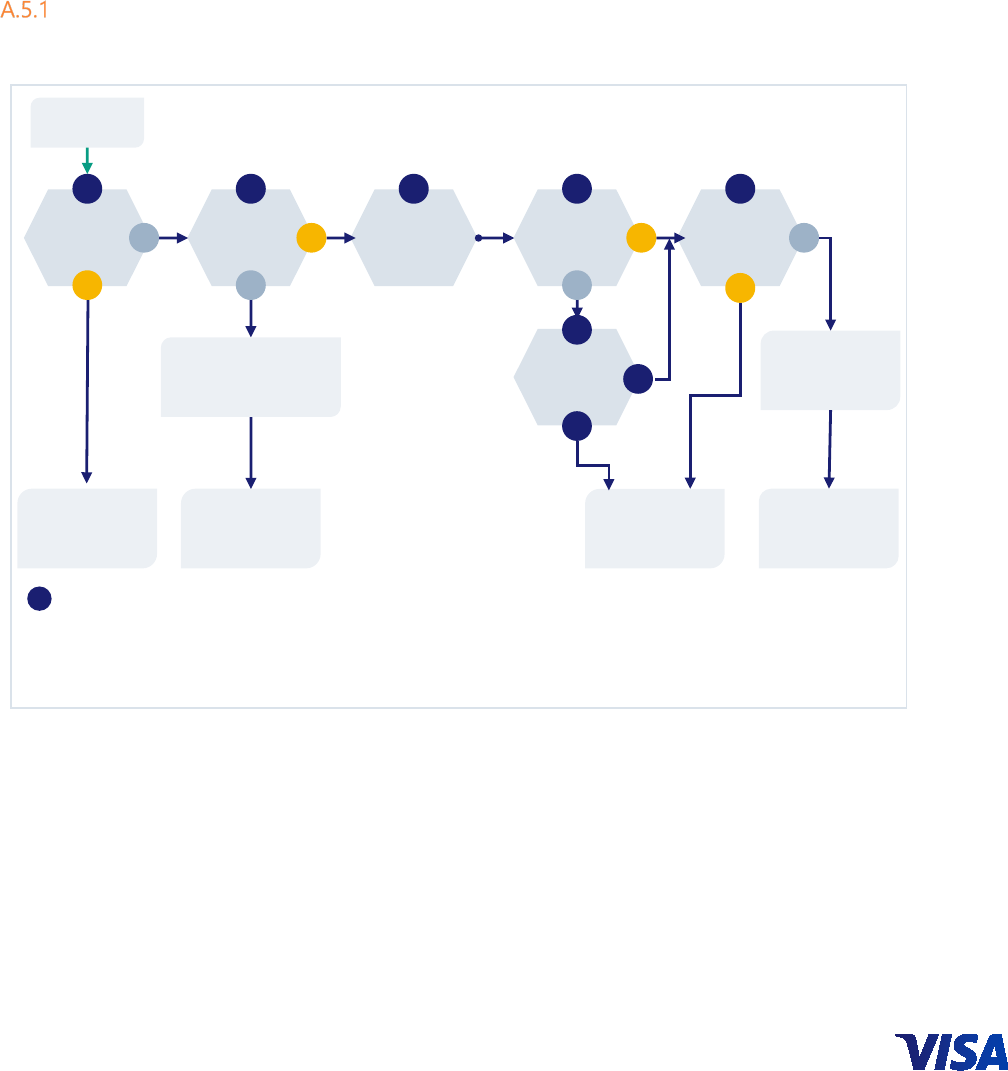

A.1 Appendix 1 The Stored Credential Framework .................................................................... 154

A.2 Appendix 2 STIP SCA Flowchart ................................................................................................ 155

A.3 Appendix 3 Merchant Initiated Transactions ........................................................................ 156

Industry Specific Business Practice MITs ............................................................................... 156

Incremental Authorization Transaction - Reason Code 3900 in Field 63.3—Message

Reason Code .................................................................................................................................... 157

Resubmission Transaction—Reason Code 3901 in Field 63.3—Message Reason

Code .................................................................................................................................................... 157

Delayed Charges Transaction—Reason Code 3902 in Field 63.3—Message Reason

Code .................................................................................................................................................... 158

Reauthorization Transaction—Message Reason Code 3903 in Field 63.3—Message

Reason Code .................................................................................................................................... 158

No Show Transaction—Reason Code 3904 in Field 63.3—Message Reason Code

159

Standing-Instruction MITs .......................................................................................................... 159

Installment Payment Transaction and Prepayment (partial & full) Transaction —

Value “I” in POS Environment Field 126.13 ........................................................................... 160

Recurring Payment Transaction —Value “R” in POS Environment Field 126.13 .... 160

Unscheduled COF Transaction —Value “C” in POS Environment Field 126.13 161

A.4 Appendix 4 EEA Countries in scope of PSD2 SCA .............................................................. 162

A.5 Appendix 5 Transaction assessment decision point considerations ........................... 163

Merchant/Acquirer decision points ......................................................................................... 163

Issuer decision points ................................................................................................................... 170

Version 3.0

12 January 2021

4

Important Information

© 2019 Visa. All Rights Reserved.

The trademarks, logos, trade names and service marks, whether registered or unregistered

(collectively the “Trademarks”) are Trademarks owned by Visa. All other trademarks not

attributed to Visa are the property of their respective owners.

Disclaimer: Case studies, comparisons, statistics, research and recommendations are provided

“AS IS” and intended for informational purposes only and should not be relied upon for

operational, marketing, legal, technical, tax, financial or other advice.

As a new regulatory framework in an evolving ecosystem, the requirements for SCA still need

to be refined for some use cases. This paper represents Visa’s evolving thinking, but it should

not be taken as a definitive position or considered as legal advice, and it is subject to change

in light of competent authorities’ guidance and clarifications. Visa reserves the right to revise

this guide pending further regulatory developments. We encourage clients to contact Visa if

they experience challenges due to conflicting guidance from local regulators. Where it makes

sense, Visa will proactively engage with regulators to try and resolve such issues.

This guide is also not intended to ensure or guarantee compliance with regulatory

requirements. Payment Service Providers are encouraged to seek the advice of a competent

professional where such advice is required.

This document is not part of the Visa Rules. In the event of any conflict between any content

in this document, any document referenced herein, any exhibit to this document, or any

communications concerning this document, and any content in the Visa Rules, the Visa Rules

shall govern and control.

References to liability protection, when used in this context throughout this guide, refer to

protection from fraud-related chargeback liability under the Visa Rules.

Note on references to EMV 3DS, 3-D Secure 2.0 and 3DS 2.0: When in this document we refer

to 3-D Secure 2.0 or EMV 3DS this is a generic reference to the second generation of 3-D

Secure and does not reference a specific version of the EMVCo specification. Version 2.1.0 of

the specification is referred to as EMV 3DS 2.1 and version 2.2.0 is referred to as EMV 3DS 2.2.

Visa rules do not preclude Issuers and Acquirers agreeing alternative means of performing

SCA.

Examples in this document show transactions processed through VisaNet. Visa supports the

use of third party processors. Contact your Visa Representative to learn more.

Version 3.0

12 January 2021

5

Using this document

This guide forms part of a set of Visa guidance documents that are relevant to the

implementation of Strong Customer Authentication under PSD2. The guide is written for

business, technology and payments managers responsible for the planning and

implementation of PSD2 policies and solutions within Issuers, Acquirers, merchants, gateways

and vendors. It aims to provide readers with guidance to support business, process and

infrastructure policy decisions needed to plan for the implementation of SCA. It is supported

by more detailed implementation guides and other documents that are listed in the

bibliography in Section 6.

This guide covers remote electronic payments.

PSD2 SCA also applies to card present payments, including contactless payments and

electronic payments made using devices including mobile handsets and wearables in a “face

to face” environment. Please see Visa Contactless and Card Present PSD2 SCA: A Reference

Guide to Implementation for more details.

This guide is structured as follows:

Section

Title

Description

1

Introduction:

Visa’s guiding

principles for

PSD2

An overview of Visa’s guiding principles for PSD2 and

corresponding focus for SCA

2

The requirements

of PSD2 Strong

Customer

Authentication

and Visa’s

interpretation

Summarizing Visa’s interpretation of the PSD2 SCA requirements

3

Visa’s PSD2 SCA

Solutions

Providing the essential information needed to interpret Section 4

of this document

It details the range of tools and services Visa is making available to

merchants, Issuers and Acquirers to optimize the application of

SCA and allowable exemptions, including EMV 3DS, authentication

and authorization message fields & values and Visa Rules

4

Optimizing the

payment

experience under

PSD2 SCA

Providing information and guidance to help clients set their

policies for application of SCA and exemptions. It describes the:

•

Key principles and considerations that govern

authentication and authorization flows

•

Options available for clients in terms of authenticating

transactions and applying exemptions

Version 3.0

12 January 2021

6

Section

Title

Description

•

Considerations to take into account when deciding how to

handle transactions

Guidance on managing of out of scope transactions and individual

exemptions

5

Payment use

cases and sector

specific guidance

for merchants

and PSPs

This section is currently under review following EBA clarification that

in payment use cases where the final amount is unknown,

transactions must be reauthenticated if the amount increases above

the amount initially authenticated. A short description of what to do

in the meantime is provided.

A revised version of this section will be included the next version

(Version 4.0) of this guide.

6

Bibliography

A list of key additional reference documents

Glossary

A glossary of terms used in the Guide

Appendices

Additional technical detail supporting the main text

Each section, and subsection, has been highlighted to show its relevancy to each client

stakeholder group. The icons used throughout this document are as follows:

Version 3.0

12 January 2021

7

Important Note:

This document provides guidance on the practical application of SCA in a PSD2

environment. Clients should note that this guide should not be taken as legal advice

and the following take precedence over content in this guide:

• Interpretations of the regulation and guidance provided by National

Competent Authorities (NCAs)

• Visa core rules

• Technical information and guidance published in EMVCo specifications, Visa

specifications and Visa Implementation guides listed in the bibliography

Visa recognizes that clients have choices and may wish to use alternative approaches,

tools and services to those referred to in this guide.

Audience

This guide is intended for anyone involved in the initiation, application and processing of e-

commerce transactions in the Visa Europe region. This may include:

• Merchants and their Acquirers and third party agents and vendors looking for

guidance on implementing SCA solutions

• Issuers seeking to ensure that they accurately recognize transactions that are in and

out of scope of SCA so they can maintain security without their cardholders’

experience being unnecessarily disrupted

Who to contact

For further information on any of the topics covered in this guide, Clients in the Visa Europe

region may contact their Visa Representative or email customersu[email protected]

.

Merchants and gateways should contact their Visa Acquirer.

Feedback

We welcome feedback from readers on ways in which future editions of the guide could be

improved. Please send any comments or requests for clarifications to

.

Version 3.0

12 January 2021

8

1. Introduction: Visa’s guiding

principles for PSD2

1.1 Introduction

As the digital economy plays an increasing part in all our lives, it is vital that electronic

payments are secure, convenient and accessible for all. Visa aims to provide innovative and

smart services to Issuers, Acquirers and merchants, so they are able to deliver best in class

payments to all Visa cardholders.

The Payment Services Directive 2 (PSD2) aims to contribute to a more integrated and efficient

European payments market and ensure a level playing field for Payment Service Providers

(PSPs). As such, it introduces enhanced security measures to be implemented by all PSPs.

1.2 Visa’s guiding principles

Visa supports the PSD2 requirements for Strong Customer Authentication (SCA), and Visa

programs and initiatives including 3-D Secure (3DS) and the Visa Token Service (VTS) may

support PSPs to be PSD2 compliant. 3DS, along with our new products, programs and

positions that are outlined in this paper, are in line with Visa’s vision for secure, compliant,

advanced and convenient electronic payments, and aim to deliver a good balance between

security and consumer convenience. This will benefit all participants of the commerce

ecosystem; reduced levels of fraud reduces cost for all parties, while merchants in particular

will benefit from a lower friction payment flow that will increase conversion rates. Consumers

will benefit from a low-friction purchasing experience, even when SCA is required.

Visa’s guiding principles for PSD2 are:

• Innovate to give consumers choice and control to make informed decisions

• Build trust and security into every payment experience

• Expand access to data while keeping it protected

• Foster competition and innovation through open standards

Our Focus for SCA and ensuring that all players in the payment ecosystem are able to

optimize both payment security and user experience are:

• Leadership: Provide clarity and education to the ecosystem

• Products: Build and evolve products and authorization messages

• Programs: Develop new programs and adjust rules as needed

• Compliance: Provide proof between parties to monitor performance

Version 3.0

12 January 2021

9

2. The requirements of PSD2 Strong

Customer Authentication and

Visa’s interpretation

This section provides a brief summary of Visa’s interpretation of the PSD2 Strong Customer

Authentication (SCA) requirements.

PSD2 requires that SCA is applied to all electronic payments - including proximity and remote

within the European Economic Area (EEA

1

); equivalent requirements apply in the UK.

2

The SCA

mandate is complemented by some limited exemptions that aim to support a frictionless

customer experience when a transaction risk is low. In addition, some transaction types are

out of scope of SCA.

The requirement to apply SCA came into force on 14 September 2019. In relation to e-

commerce, the European Banking Authority (EBA) has recognised the need for a delay in

enforcement to allow time for all parties in the payments ecosystem to fully implement SCA

and has set a deadline of 31 December 2020 by which time the period of supervisory flexibility

should end. The migration plans of PSPs, including the implementation and testing by

merchants should also be completed by 31 December 2020. While the majority of National

Competent Authorities (NCAs) will align with the EBA’s guidance, PSPs should ensure they act

in accordance with guidance or additional conditions imposed by local regulators. The UK’s

Financial Conduct Authority (FCA) will start to enforce the regulation which transposes PSD2

into UK law from 14 September 2021 (subject to compliance with phased implementation

plans). The Banque de France has also announced a gradual enforcement of SCA based on

increasing use of soft declines, to 31 March 2021 with potential for further gradual

implementation to 31 June 2021.

Merchants and PSPs should check with NCAs for enforcement timescales in their respective

markets.

2.1 The application of SCA and use of factors

SCA requires that the payer is authenticated by a PSP through at least two factors, each of

which must be from a different category. These are summarized in Table 1.

1

For more information on the territories the requirement applies to please see Appendix A.4.

2

After the end of the Brexit implementation period (from 1 January 2021) SCA requirements are

expected to remain in force and will be defined in accordance with relevant technical instruments

published by the FCA.

Version 3.0

12 January 2021

10

Table 1: Strong Customer Authentication Factors

Category

Description

Example

Knowledge

Something only the payer knows

A PIN code

Possession

Something only the payer has

A preregistered mobile phone, card reader or

key generation device

Inherence

Something the payer is

A biometric (facial recognition, fingerprint,

voice recognition, behavioral biometric)

Factors must be independent such that if one factor is compromised the reliability of the other

factor is not compromised.

While the PSD2 regulation allows for any combination of at least two factors, in Visa’s view,

the most practical SCA solutions will make use of:

• Possession as the first factor, and

• Inherence as the preferred second factor, or

• Knowledge as an alternative compliant, but much less satisfactory, factor

The EBA Opinion published 21

st

Jun 2019

3

makes clear that:

• Static card details and security codes printed on a card cannot be used as either a

possession or a knowledge element and the opinion advises competent authorities

to closely monitor their application

• Dynamic card security codes may be used to provide evidence of possession and

card security codes that are not printed on the card but sent separately to a customer

could constitute a knowledge element

• An OTP cannot be used as a knowledge element but may be used to prove evidence

of possession

• Inherence includes both biological and behavioural biometrics, where behavioural

biometrics includes examples such as keystroke dynamics (typing and swiping

patterns) and the angle at which the consumer holds the device.

The EBA also confirmed via their Q&A tool on 12 July 2020

4

that tokenised card details can be

used to provide evidence of possession where the process of tokenisation binds the cardholder

and the token to a preregistered device. Visa proposes - and has been engaging with

regulators on - an SCA Authentication Factor Strategy that provides staged compliance and

consumer choice by providing two primary, recommended authentication methods:

3

Opinion of the European Banking Authority on the elements of strong customer authentication under

PSD2 21 June 2019.

4

https://eba.europa.eu/single-rule-book-qa/-/qna/view/publicId/2019_4827

Version 3.0

12 January 2021

11

2.1.1 Biometric plus device possession

Biometric authentication can be SCA compliant and a single device can provide both the

possession factor (i.e. indicating possession of the device where the biometric is stored) and

an inherence factor (the verification of the biometric captured). This approach has the

additional advantages that:

• Consumers are getting more comfortable using biometrics

• Both Visa and MasterCard have requirements for Issuers to support biometrics

• The industry is aligned on this, and progress is underway

This method, also known as Out of Band (OOB) app plus biometric authentication uses a

registered smart phone capable of supporting a relevant biometric (for example fingerprint or

facial recognition) in conjunction with a mobile banking or other authentication app. The

technology provides for two distinct and independent authentication factors, possession and

inherence, both of which are facilitated using a biometric.

2.1.2 SMS OTP plus behavioural biometric

Behavioural biometrics can be used as a second factor (proving inherence) alongside OTP

(proving possession) to provide an SCA solution that is significantly easier for customers to

use and far more secure than OTP combined with a knowledge factor. This provides a

potentially compliant evolution solution for existing single factor SMS OTP solutions that

delivers a familiar and secure customer experience and is relatively straightforward for Issuers

to implement.

Behavioural biometrics uses physical behaviour indicators that are unique to an individual

customer. These can include the angle at which a device is held, the way keystrokes are

entered, gesture analysis and swiping speed. Indicators are analysed and used to build

dynamic user profiles and authenticate users.

The use of behavioural biometrics is in line with the EBA opinion on elements for SCA which

identifies inherence elements such as keystroke dynamics (identifying a user by the way they

type and swipe) and the angle at which the user holds the device.

A challenge solution that uses behavioural biometrics will help Issuers to be compliant with

the regulation, while fraud protection can be maximised by combining the behavioural

biometric indicators with EMV 3DS data, which include device, location and purchase history

data, and provides a proven, accurate basis for assessing fraud risk.

2.1.3 Tactical and Inclusivity solutions

While biometrics based SCA solutions are recommended as the primary SCA solutions for the

majority of customers, alternatives may be considered in the following circumstances:

• It is not possible for an Issuer to deploy one of the recommended solutions to all of

its customers by the enforcement date and a Tactical Solution needs to be employed

• A minority of customers are unable or unwilling to access mobile phone based

solutions and an Inclusivity Solution needs to be deployed

Tactical Solutions will normally use a knowledge element to provide second compliant factor

alongside a possession factor provided either through an SMS OTP or a securely device bound

banking authentication app.

Version 3.0

12 January 2021

12

Issuers need to focus on serving the majority of customers with the recommended SCA

solutions, however Inclusivity Solutions should also be made available for limited deployment

to those customers unable to access or use mobile phones for authentication. A number of

two-factor options are available including card readers and hardware tokens that generate an

OTP to prove possession of the device in response to entry of a knowledge factor such as a

PIN.

2.2 Exemptions

The main exemptions to the application of SCA relevant to Visa e-commerce transactions are

summarized below. It should be noted that not all exemptions are available to all PSPs. For

more detail please refer to Section 4.5.

2.2.1 Transaction risk analysis (TRA)

The TRA exemption allows for certain remote transactions to be exempted from SCA provided

a robust risk analysis is performed (based on the requirements in Article 18 of the SCA RTS),

and the PSPs meet specific fraud thresholds. TRA is key to delivering frictionless payment

experiences for low-risk remote transactions. Issuers and Acquirers can both apply the TRA

exemption so long as they meet certain requirements, including that their fraud to sales rates

are maintained within the specific fraud thresholds for remote card payments, set out in Table

2.

The SCA RTS

5

also lays down minimum requirements for the scope of transaction risk

monitoring that must be carried out by PSPs.

Table 2: Specific fraud thresholds for remote card payments

Transaction value band

PSP Fraud Rate

≤€100

13 bps / 0.13%

€100 ≤ €250

6 bps / 0.06%

€250 ≤ €500

1 bps / 0.01%

2.2.2 Low value transactions

Remote transactions up to and including €30 do not require SCA so long as the cumulative

number of previous remote transactions using the exemption does not exceed five, or the

cumulative value of previous remote transactions using the exemption does not exceed €100,

since the last application of SCA. Issuers should select either the cumulative or consecutive

limit. If Issuers do not select a limit, they must apply both limits on a per transaction basis.

2.2.3 Trusted beneficiaries

Under the trusted beneficiaries exemption, once a customer performs SCA in order to add a

qualifying merchant to their Trusted List, subsequent purchases with that merchant generally

will not require SCA.

5

See Recital 14 and article 2 of the Regulatory Technical Standards.

Version 3.0

12 January 2021

13

2.2.4 Secure corporate payments

Under SCA-RTS Article 17, PSPs are allowed not to apply SCA for payments made by payers

who are both legal persons and not consumers. This is only the case where the payments are

initiated electronically through dedicated payment processes or protocols that are not

available to consumers. Subject to the view of local regulators, these payments may:

• Originate in a secure corporate environment, including for example, corporate

purchasing or travel management systems

• Be initiated by a corporate customer using a virtual, lodged card or Central Travel

Account, such as those used within an access-controlled corporate travel

management or corporate purchasing system

In many cases it will not be possible to authenticate transactions originating in a secure

corporate environment and requesting SCA may result in valid transactions being declined.

In order to apply the exemption, Issuers must ensure that, and NCAs must be satisfied that,

the processes or protocols used guarantee at least equivalent levels of security to those

provided for by PSD2. NCAs may have their own procedures or processes for assessing use of

this exemption.

Issuers are encouraged to demonstrate to NCAs that applicable processes and protocols meet

the requirements of the regulation and Visa recommends that Issuers liaise with NCAs over

the procedure for this as required.

2.2.5 Recurring Transactions

Please note Visa does not support the recurring transactions exemption for Visa card

transactions. Visa’s view is card transactions that would otherwise be covered by the recurring

transaction exemption are typically Merchant Initiated Transactions (MITs) and are therefore

out of scope of SCA.

2.3 Out of scope transactions

2.3.1 Transactions considered out of scope

The following transaction types are out of scope of SCA and do not require the application of

SCA, so long as certain conditions are met:

• Merchant Initiated Transactions (MITs) - Are transactions of a fixed or variable amount

and fixed or variable interval, governed by an agreement between the cardholder and

merchant that, once set up, allows the merchant to initiate subsequent payments from the

card without any direct involvement of the cardholder. As the cardholder is not present

when an MIT is performed, cardholder authentication is not possible. A transaction can

only be an MIT if the cardholder is not available to (I) initiate; or (II) authenticate the

transaction. If the cardholder is available to either initiate or authenticate, the transaction

is not an MIT. An MIT can only be submitted after a previous cardholder initiated

transaction (CIT) has been performed with appropriate authentication to establish the

initial agreement with the cardholder specific to the MIT (even if that CIT is a zero-value

transaction). Subsequent qualifying MITs are out of scope of PSD2 SCA and therefore do

not require authentication.

• Mail Order/Telephone Order (MOTO) - Payments made through Mail Order/Telephone

Order are out of scope and do not require the application of SCA. Note, “voice commerce”

Version 3.0

12 January 2021

14

payments initiated through digital assistants or smart speakers are not classed as MOTO.

In Visa’s view, transactions initiated via telephone through Interactive Voice Response (IVR)

can be considered as telephone initiated and therefore MOTO. If the IVR is internet based,

the transaction cannot be classed as MOTO.

• One-leg-out- It may not be possible to apply SCA to a transaction where either the Issuer

or Acquirer is located outside the EEA

6

or the UK

7

. However, SCA should still be applied to

OLO transactions on a “best-effort” basis. Further text on one-leg-out transactions and

best efforts is provided below. If the Issuer is not technically able to apply SCA, the Issuer

is not obliged to decline. The Issuer should make their own approval decision based on

risk and liability considerations. A transaction at a merchant that is located outside the EEA

or UK but that is acquired from within the EEA or UK is not classed as one-leg-out and is

in scope of SCA.

• Anonymous transactions - Transactions through anonymous payment instruments are

not subject to the SCA mandate, for example anonymous prepaid cards. In the Visa system,

these can include non-reloadable prepaid cards on which no KYC has been done and thus

where the Issuer cannot authenticate the identity of the cardholder.

8

2.3.2 Identifying one-leg-out transactions and understanding use of best efforts to apply

SCA

The EBA has set out that SCA applies on a best-effort basis for one-leg-out transactions. We

set out two scenarios below.

Issuer within the EEA/UK, Acquirer outside the EEA/UK

9

Where a transaction uses a card issued in the EEA or the UK, but is acquired outside of the EEA

or the UK:

• If an Issuer receives a transaction request that does not enable them to apply SCA,

the Issuer is not obliged to decline the transaction.

• The Issuer should make its own approval decision based on risk, customer experience

and liability considerations.

Acquirer within the EEA/UK, Issuer outside the EEA/UK

9

Where a transaction uses a card issued outside of the EEA or the UK, but is acquired within the

EEA or the UK:

• Visa recommends that Acquirers/merchants send transactions for authentication in

an SCA compliant way, for example by submitting the transaction via 3DS, where this

is supported by the non-EEA/UK Issuer.

• If a non-EEA/UK Issuer receives such a transaction request, it is not under any

obligation to apply SCA.

6

Refer to Appendix A.4 for a list of EEA countries.

7

From 14 September 2021 (based on current enforcement plans).

8

The fact that no KYC has been done and/or that it is a non-reloadable prepaid card will not necessarily

mean the card is anonymous in all cases.

9

Equivalent requirements are currently planned to be enforced in the UK from 14 September 2021.

Version 3.0

12 January 2021

15

2.3.3 Considerations arising from different SCA implementation timescales

Different SCA implementation timescales and regulatory enforcement dates between

countries means there is a risk that cross-border transactions may be declined by an Issuer

due to SCA being required in one country but not the other. This situation is effectively a

transitional one-leg-out or one-leg-in scenario.

From 1 January 2021 to 14 September 2021 SCA will be enforced across most of the EEA but

will not be enforced in the UK

10

. During this time, where one of the Issuer or Acquirer is in the

UK and the other is in the EEA, these transactions may be considered one-leg-out and SCA

should be applied on a best efforts basis as described above. However, while EEA Issuers are

not obliged to decline one-leg-out transactions without SCA, there may be a heightened risk

of declines if UK-acquired merchants send transactions to EEA Issuers without SCA.

This may also be a risk if timelines diverge between other EEA member states. For example, as

of December 2020, the Banque de France has announced a gradual enforcement based on

soft declines to 31 March 2021, with a possibility of further gradual implementation to 31 June

2021.

Transitional risks that may arise and how they can be mitigated are set out below. Cross border

transactions between the EEA and the UK are used as an example.

Issuer within the EEA / Acquirer in UK (transitional one-leg-out)

There is a possibility that EEA Issuers may decide to request SCA on UK acquired merchants

from 1 January 2021. In order to minimise the risk of declines, UK acquired merchants with

customers using EEA issued cards may wish to consider implementing SCA and submitting

transactions via 3DS in line with the EEA implementation timelines.

EEA Issuers are not obliged to decline transactions without 3DS (and where SCA is not

otherwise technically feasible to apply) and during the transition period should treat them as

described in section 2.3.2.1

Acquirer within the EEA, Issuer within the UK (transitional one-leg-in)

In this case, prior to enforcement, the UK Issuer is not required to support SCA and the EEA

merchant/Acquirer should consider whether to send transactions for authentication, via 3DS,

only when they know the UK Issuer can accept them

Error! Bookmark not defined.

.

UK merchants acquired in the EEA will need to implement SCA in line with implementation

and enforcement timescales in the Acquirer’s region/market.

In practice, in addition to any regulatory requirements, Visa requires that all EEA and UK Issuers

support EMV 3DS in any event from October 2020 as described in section 3.3.2.

10

From 1 January 2021, pending any further developments, the UK could become a third country for

the purpose of PSD2 SCA. Equivalent requirements to PSD2 SCA for e-commerce are currently planned

to be enforced in the UK from 14 September 2021.

Version 3.0

12 January 2021

16

2.4 Dynamic linking

For electronic remote payment transactions, where PSPs apply SCA, both the amount and the

payee must be clear to the payer when they authenticate a purchase. An authentication code

must be produced but does not need to be visible to the cardholder.

Visa’s programs such as 3DS, and Visa Token Service (VTS), deliver an authentication code -

Cardholder Authentication Verification Value (CAVV) and/or Token Authentication Verification

Value (TAVV) - which can be linked to the transaction. The authentication code accepted by

the PSP that is processing the transaction must correspond to the amount and payee. Visa

systems enable the authentication code to be linked back to the amount and payee.

The regulation requires that the authentication code generated is specific to the amount of

the payment transaction and the payee agreed to by the payer when initiating the transaction

and that any change to the amount or the payee results in the invalidation of the

authentication code generated.

When the final amount is unknown, the EBA has confirmed that the final amount should not

increase above the authenticated amount.

11

Re-authentication is required for any increases

above the authenticated amount. The same does not apply where the final, authorized amount

is lower than the authenticated amount. In these cases, no re-authentication is required.

If the amount is higher, several options exist to handle amount variation. One of them is that

the merchant may wish to set up an MIT to allow incremental amounts to be taken if the

authorized amount is insufficient, rather than seek further authentication from the cardholder.

With regard to variations in merchant name, the EBA has confirmed

12

that the information

included in the authentication code does not necessarily need to be the full or exact merchant

name, and that while the RTS ‘Regulation does not specify how the payee should be identified

for the purpose of the dynamic linking requirements, it can be a unique identifier

corresponding to the identity of the payee agreed to by the payer. The identifier agreed to by

the payee at authentication may differ to the merchant name at authorization. For example:

• When there is a difference in the name used to identify a merchant between

authentication and authorization such as use of a trading name vs. a legal entity

name, use of different abbreviations or acronyms or a combination of the Acquirer

and merchant name vs. the merchant name.

• When a transaction is the result of a booking via an agent who initiates

authentication on behalf of a third party merchant that subsequently requests

authorization, the name in the authentication request may be that of the agent only,

or that of the agent and the merchant, whereas the name in the authorization request

may be that of the merchant.

For additional guidance on managing variations in merchant name and amounts within the

constraints of these requirements please see section 4.2.2

2.5 Visa PSD2 Solutions and GDPR

Visa’s PSD2 solutions process data elements that are considered to be personal data under

the GDPR. Merchants, Issuers and Acquirers should seek legal advice when considering the

11

Response to EBA Q&A 2020_5133.

12

Response to EBA Q&A 2019_4556.

Version 3.0

12 January 2021

17

GDPR consequences of providing and processing data that may be considered to be personal

information.

Specific principles to consider include:

• Lawful basis for processing: Merchants, Issuers and Acquirers should ensure they can

rely on a lawful basis under the GDPR to process personal data in the context of

Visa’s PSD2 solutions. For most of these solutions, Merchants, Issuers and Acquirers

may rely on legal bases other than consent including legal obligation, contract and

legitimate interest for using personal data for fraud prevention purposes.

• Purpose limitation: Data provided by merchants for 3DS authentication must not be

used for any purpose other than authentication and fraud prevention. Specifically,

this data should not be used for sales, marketing or other purposes.

• Data storage and security: Merchants, Issuers and Acquirers should ensure that the

requirements for data storage, security and international transfers under GDPR are

applied to any personal data that is collected for Visa’s PSD2 solutions.

• Transparency and Individual Rights: Issuers, Acquirers and Merchants should ensure

that Terms and Conditions, Privacy Policies and Privacy Notices reflect the capturing

and processing of data for fraud prevention purposes in the context of Visa’s PSD2

solutions. This includes information on purposes for processing their personal data,

the retention periods for that personal data, and who it will be shared with. In

addition, Issuers, Acquirers and Merchants should ensure that they can respond to

individuals’ requests under the GDPR.

Version 3.0

12 January 2021

18

3. Visa’s PSD2 solutions

3.1 Solution summary

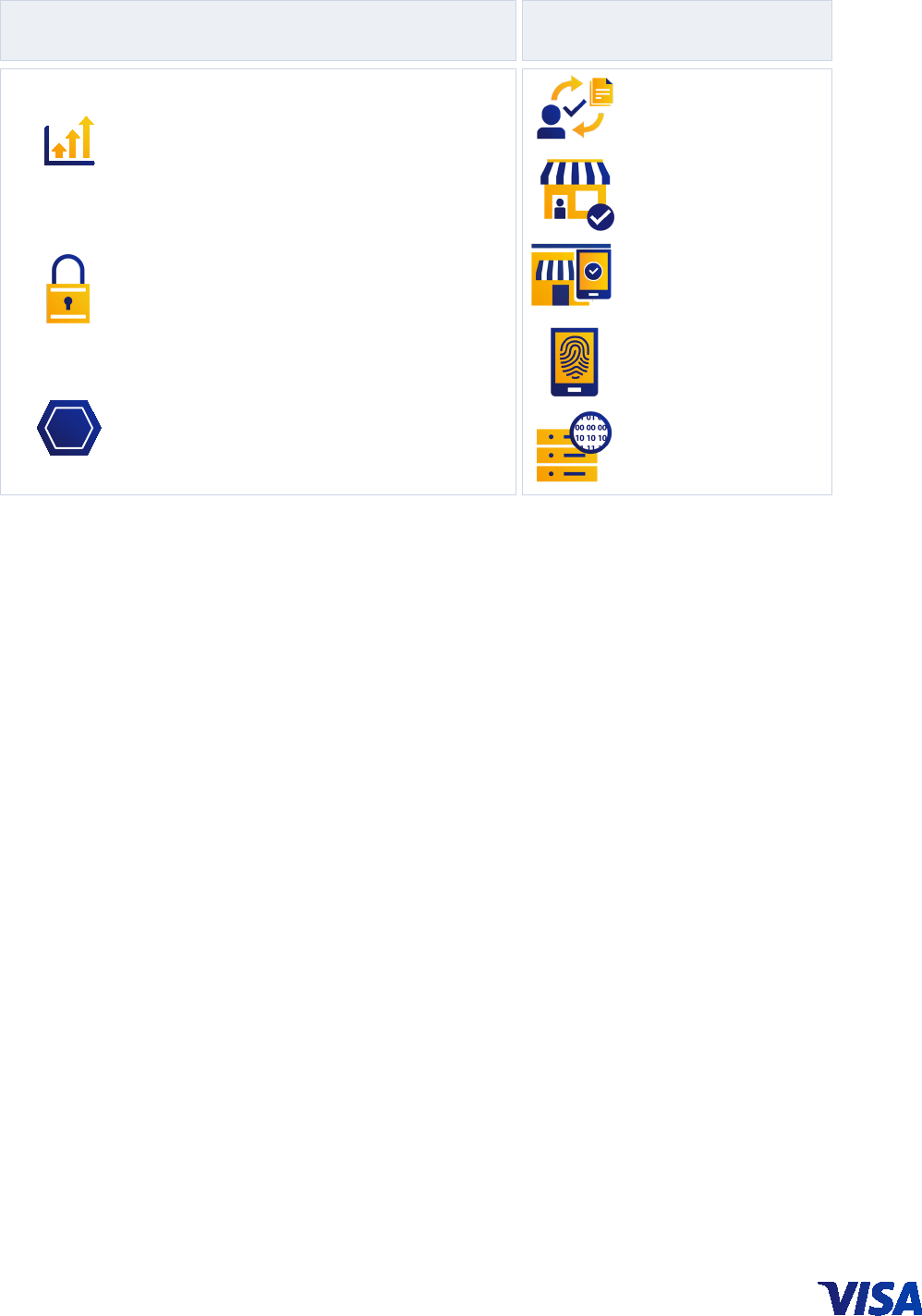

Visa is implementing a portfolio of solutions to help support the application of SCA and

exemptions. These comprise a combination of technology solutions, enhanced rules and

policies which are summarized in Figure 1 below.

Figure 1: Summary of Visa’s PSD2 solutions

The technology-based solutions include a suite of new products and programs that will

support the application of SCA and exemptions. These are all based on a core set of

foundational security technologies, illustrated in Figure 2 below.

STIP Policy

PSD2 Payment Policy

PSD2 Regulatory Guidance

Guidelines on common e-

commerce payment use cases

EMV 3DS 2.2 Exemption Flags

Authorization Flags

SCA Decline Code

Visa Token Service

Visa Trusted Listing

Visa Authenticator App

Visa Pre-dispute products

VCAS

Visa Attempts Server

STIP

Abandonment Rates

Authorization rates

Risk Based Authentication

Minimum Data Requirements

Biometrics Mandate

Visa Delegated Authentication

Program

Technology Rules Policies

Version 3.0

12 January 2021

19

Figure 2: The foundational and SCA products & programs

The application of SCA and the approval of transactions depends on two processes:

• Authentication: Allows the Issuer to verify the identity of the cardholder or the

validity of the use of the card, including the use of the cardholder’s personalized

security credentials. Where authentication is required, it takes place before

authorization, using the Issuer’s selected authentication method, which in most cases

is facilitated through 3-D Secure.

• Authorization: Is a separate process used by a card Issuer to approve or decline a

Visa payment transaction submitted by a merchant/Acquirer or other card acceptor.

In a standard flow, merchants will submit a transaction for authentication, in some cases with

an indicator requesting an exemption from SCA requirements. If the authentication is

successful, the result will be returned along with a cryptogram (CAVV), and the merchant will

submit the transaction to authorization along with the cryptogram and the correct indicators.

Visa also supports the option for transactions to be submitted direct to authorization, with an

appropriate indicator. This may occur when:

• A transaction is out of scope of SCA

• An Acquirer applies an exemption such as TRA

• A qualified delegate has undertaken authentication under the terms of the Visa

Delegated Authentication Program

• A merchant and the Issuer participate in the Visa Trusted Listing Program, the

merchant is on the customer’s Trusted List, and the transaction qualifies for the

trusted beneficiaries exemption

Factors to consider when selecting the appropriate option are summarized in section 4.3.

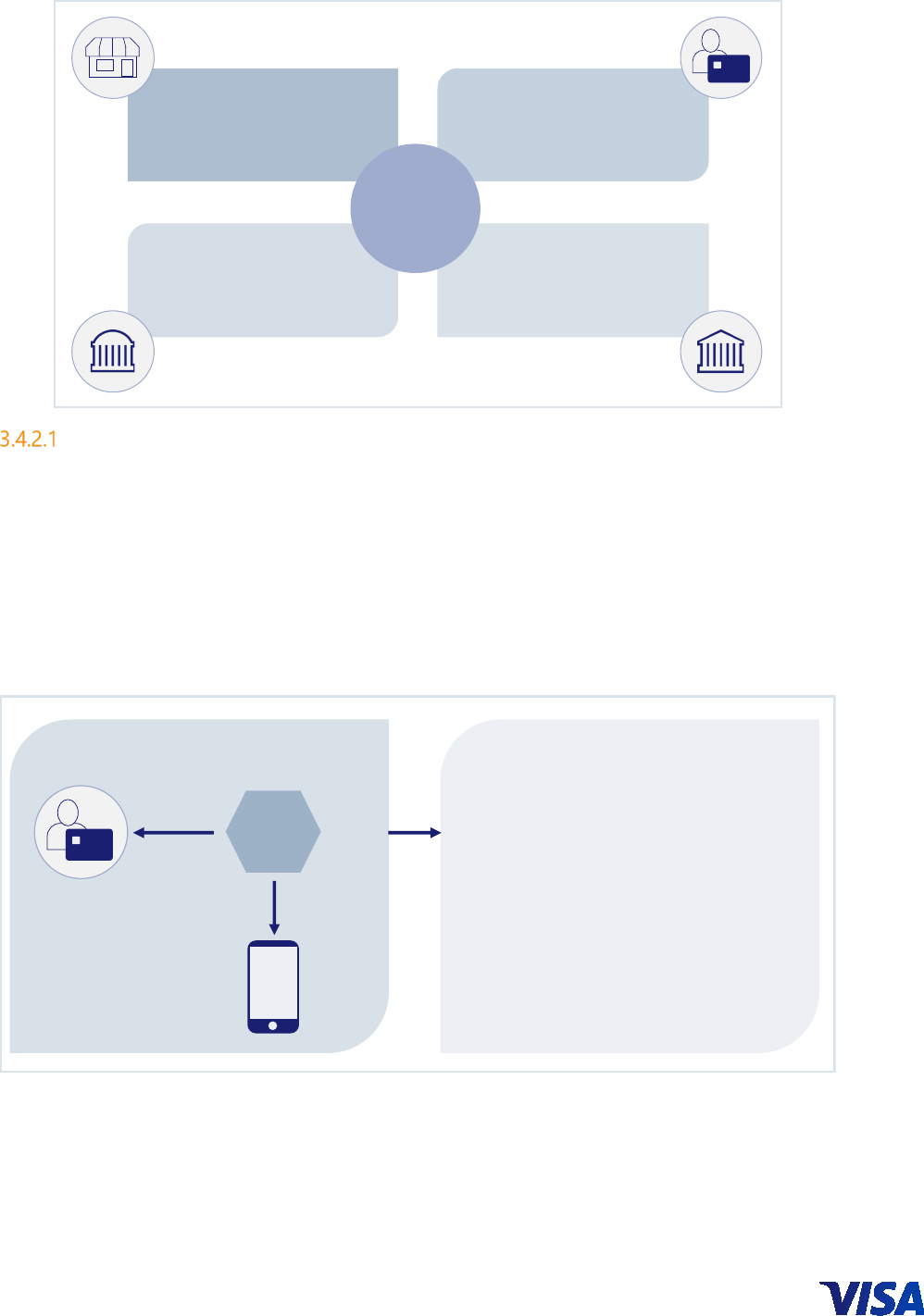

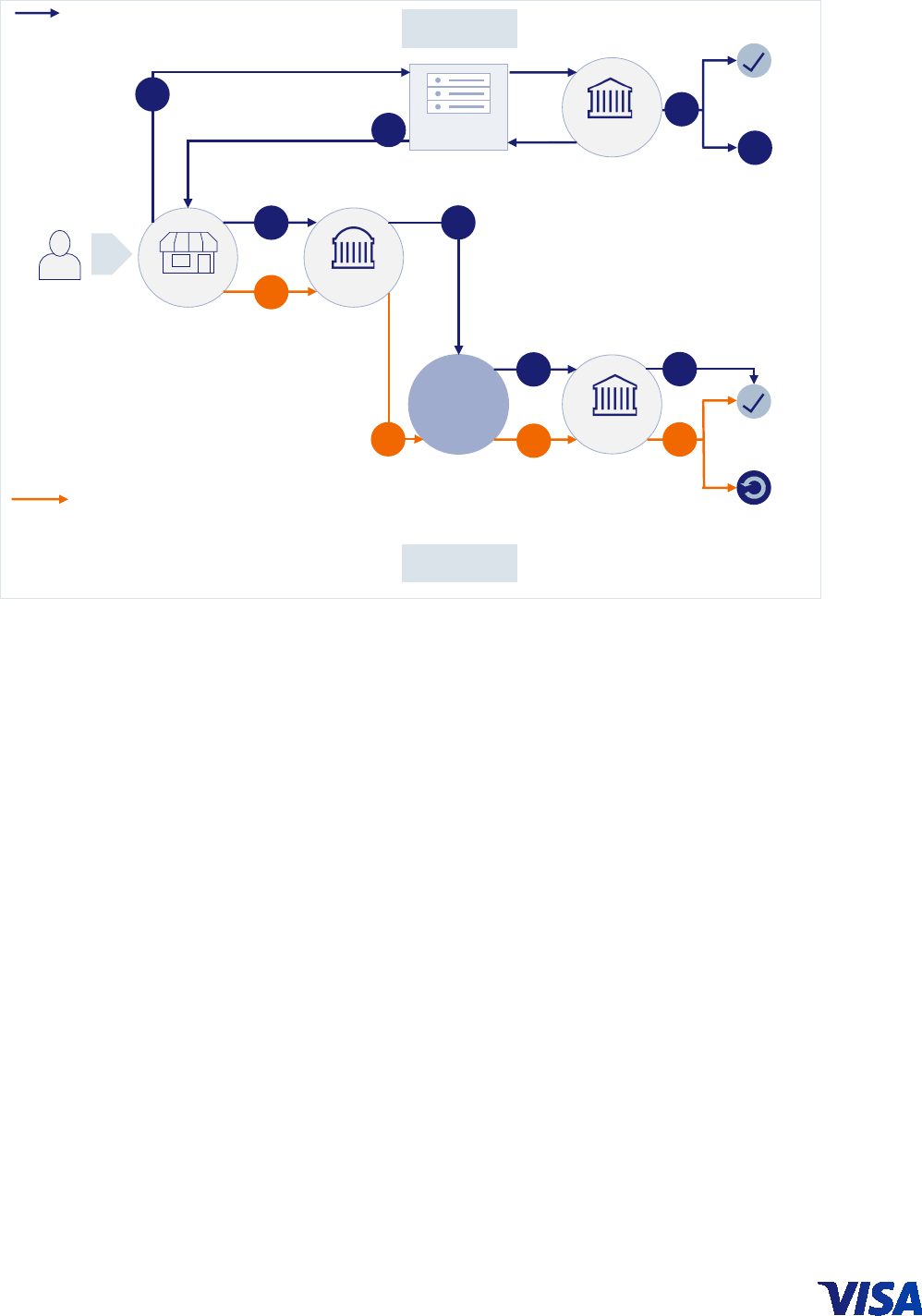

These basic flows are summarized in Figure 3 below:

T

Foundational products and programs SCA products and programs

Predictive analysis

• Dynamic modelling based on current fraud

trends, geographies and segments to effectively

manage risk

• Models built and maintained by Visa and

refreshed every 12 months

3-D Secure

• Industry standard for authentication

• EMV 3DS has an enhanced user experience,

expanded device usage, greater data sharing

and is regulatory smart

Tokenization

• Protecting payment data by replacing

traditional card account numbers with a unique

token that can be restricted by device,

merchant or channel

Visa Trusted

Listing

Visa Delegated

Authentication

Visa Consumer

Authentication

Service (VCAS)

Visa Pre-dispute

Products

Visa Authenticator

App

Version 3.0

12 January 2021

20

Figure 3: Simplified summary of authentication and authorization flows

The following sections describe the authorization and authentication technologies and

indicators offered by Visa.

3.2 Authorization options

3.2.1 Overview

Indicators in the authorization request message will be used by Issuers to identify:

• Transactions that are identified by merchants as being out of scope

• Acquirer exemptions (TRA and low value)

• Issuer applied exemptions that can be indicated by the merchant or Acquirer (trusted

beneficiaries and secure corporate payments)

• That authentication has been applied under the Visa Delegated Authentication

Program

• That authentication was not possible due to an outage in the acceptance domain

• There was no connectivity at the time of authorization

If a merchant would like to indicate that an Acquirer exemption is to be applied, an exemption

indicator should be submitted in the authorization request. If the transaction is out of scope,

the merchant must also ensure that the correct data is used to identify that it is out of scope.

Issuer ACS

Visa

3-D Secure DS

Authentication Response

with CAVV & ECI value

Authorization Request with CAVV, ECI

value & exemption indicator (if applicable)

Authentication

Flow

Standard flow: authentication

followed by authorization

Direct to authorization

flow

Authorization Request with

exemption/out of scope indicator

1

Authentication request

2

Authorization

Flow

VisaNet

Issuer HostMerchant

Customer

Acquirer

1

3

4

2

5

Authorization Response

3

Version 3.0

12 January 2021

21

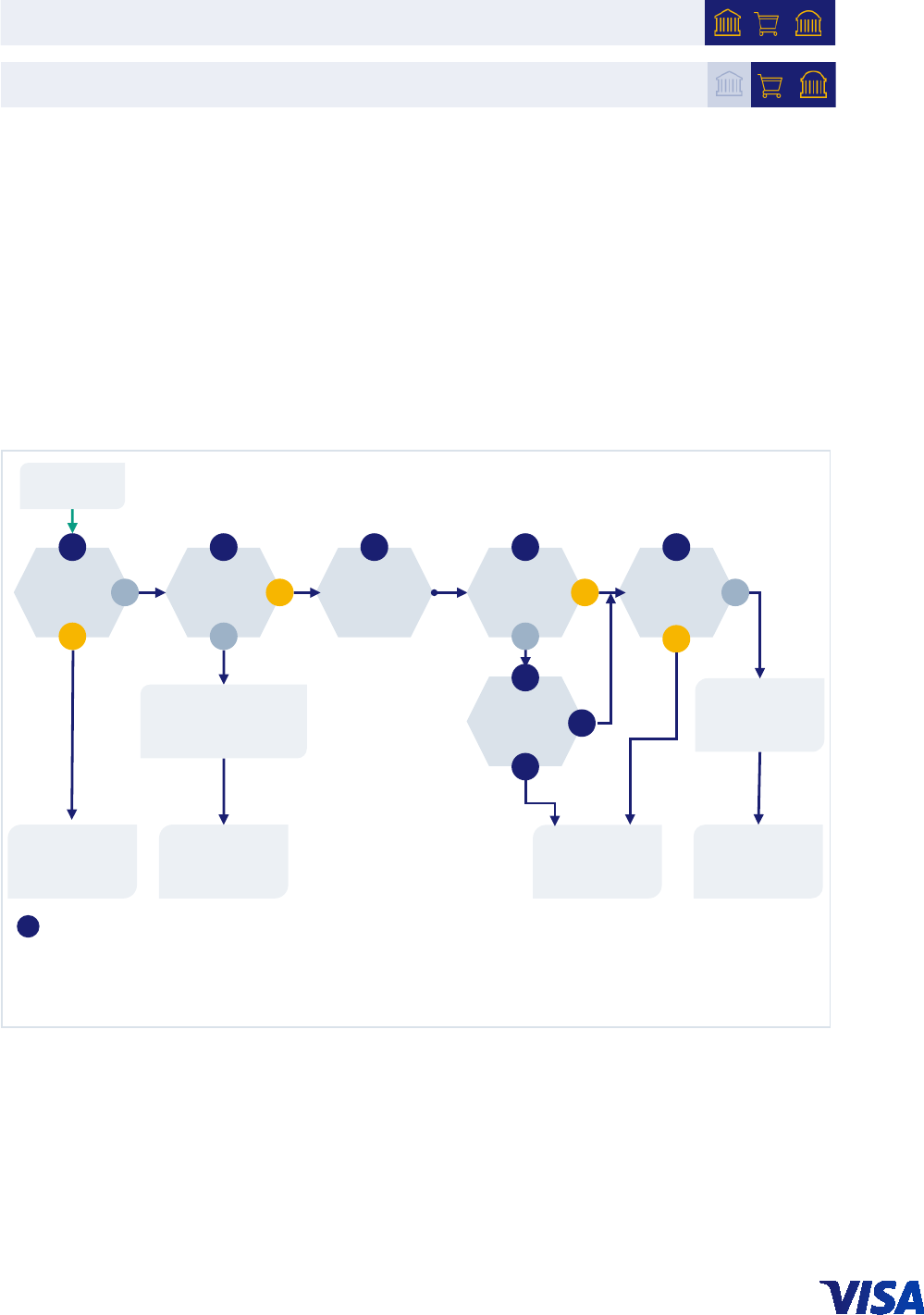

This section describes the Visa authorization message flows and fields and how these are used

to support the application of exemptions and management of out of scope transactions.

3.2.2 Authorization message flows and fields

The main messages in the authorization flow are the Authorization Request and the

Authorization Response messages. These enable merchants and Acquirers to request

transaction authorization and Issuers to respond with the authorization result. The Electronic

Commerce Indicator (ECI) value and CAVV (or TAVV if using the Visa Token Service (VTS)

13

)

cryptograms are used to communicate the authentication status of the transaction. The

messages work as summarized in Figures 4 and 5:

Figure 4: Authorization request message (transaction authenticated via 3DS)

* Note: when an Acquirer TRA exemption request is accepted by the Issuer’s ACS without the application of SCA by

the Issuer the transaction will proceed as ECI 07 with a CAVV present.

13

For more information about the Cloud Token Framework see Section 3.4.2; about Visa Delegated

Authentication Program see Section 3.7; and about authentication data if using 3-D Secure see Section

3.3.8.

Key Point

Indicators in the authorization request message can be used by merchants to

indicate certain out of scope transactions and exemptions. Merchants must

ensure that the correct mechanism and indicators are used to identify

exemptions being requested and transactions that are out of scope of SCA.

VisaNetAcquirer / Acquirer Processor

• Creates the authorization request including:

• The ECI, CAVV and/or TAVV

• MIT indicators if the transaction is an MIT

• Using appropriate MOTO indicating data if

transaction is MOTO

• Exemption flag if exemption is being used

• Forwards the authorization request to the Issuer

through VisaNet

• Recognises ECI 05 and 06 as EMV 3DS transactions

and where a CAVV is present (for ECI 05, 06 and

sometimes present for 07*), - either:

• VisaNet verifies the CAVV and send the issuer the

CAVV verification results, or

• VisaNet forwards the CAVV to the Issuer to verify

• Includes the 3DS Indicator to the Issuer in the

authorization request, if the Issuer has elected to

receive it

• Verifies the TAVV and sends the issuer the TAVV

verification results

• Forwards the authorization request to the Issuer

Host for processing

Version 3.0

12 January 2021

22

Figure 5: Authorization response message (transaction authenticated via 3DS)

Table 3 summarizes the key relevant ECI values returned by 3DS. The format and role of the

CAVV is summarized in more detail in Section 3.2.7.

Table 3: ECI values

ECI Value

Authentication Status

Liability

ECI 05

Cardholder authenticated by the Issuer

Issuer

ECI 06

Merchant attempted to authenticate the cardholder but either the

cardholder or Issuer is not participating in 3DS or the Issuer’s ACS

is currently unavailable

Issuer

ECI 07

Payment authentication has not been performed

Acquirer

Table 4 summarizes the key relevant message fields in the authorization message flow.

It should be noted that some transaction status indicators must be flagged by Issuers and

some by Acquirers. It is key that merchants use MIT indicators for MIT transactions and the

correct MOTO information for MOTO transactions.

Issuer Host VisaNet

Acquirer /

Acquirer Processor

Merchant

• Receives the ECI,

CAVV, and CAVV

Results (if signed up

for the Visa CAVV

Verification Service) in

the authorization

message

• Verifies the CAVV and

updates the CAVV

Results field (if issuer

performs CAVV

verification)

• Completes their

authorization decision

• Returns the

authorization

response (approve or

decline) to the

acquirer via VisaNet.

• Includes the 3DS

indicator to the

Acquirer in the

authorization request

• Forwards the

authorization response

to the Acquirer for

processing

• Forwards the

authorization decision

to the merchant

• Provides authorization

response to cardholder

Version 3.0

12 January 2021

23

Table 4: Summary of authorization fields and messages used to communicate SCA and

authorization status

Field

Set by

Function

Field Value/Indicator

F19 Acquirer

Populated with the Acquiring Institution

Country Code allowing the I

ssuer to

determine whether the transaction is in or

out of scope of SCA

Acquiring Institution Country Code

F25 Acquirer

Point-of-Service Condition Code – required

for CAVV processing which in addition can

be used to indicate MOTO transactions

Existing values as defined in the Visa technical

specification

14

F34 Acquirer

Allows Acquirer to indicate that

authorization is being requested without

the application of SCA because one of the

following exemptions applies:

• Trusted Beneficiary

• Low Value

• Secure Corporate Payments

• Transaction Risk Analysis

or that the transaction has been

authenticated under the terms of the Visa

Delegated Authentication Program allows

Visa to indicate to Issuers that a

transaction is an MIT out of scope of SCA

Allows Acquirers to indicate that there is

an outage in the acceptance environment

and it is not possible to authenticate.

The following tags are used to carry the SCA

exemption indicators in the new TLV Field 34 Dataset

ID Hex 4A:

• Tag 84 - Trusted Merchant Exemption Indicator.

Possible values:

• 0 (Trusted merchant exemption not

claimed/requested)

• 1 (Trusted merchant exemption

claimed/requested)

• 2 (Trusted merchant exemption

validated/honored)

• 3 (Trusted merchant exemption failed

validation/not honored)

NOTE:

If the trusted merchant exemption

does not apply to

the transaction,

the value of 0 is optional and the tag

may be omitted entirely.

• Tag 87 - Low Value Exemption Indicator

Possible Values

• 0 (Low value exemption does not apply to the

transaction)

• 1 (Transaction exempt from SCA as the

merchant/Acquirer has determined it to be a

low value payment)

NOTE:

If the low value exemption does not apply to the

transaction, the value of 0 is optional and the tag

may be omitted entirely.

• Tag 88 - Secure Corporate Payment (SCP) Indicator

Possible Values:

• 0 (SCA exemption does not apply to the

transaction)

• 1 (Transaction exempt from SCA as the

merchant/Acquirer has determined it as a secure

corporate payment)

NOTE:

If the SCP exemption does not apply to the transaction,

the value of 0

is optional and the tag may be omitted

entirely.

• Tag 89 - Transaction Risk Analysis (TRA) Exemption

Indicator

Possible Values:

14

For more details, refer to the V.I.P. Base 1 Technical Specifications, Volume 1 & Volume 2.

Version 3.0

12 January 2021

24

Field

Set by

Function

Field Value/Indicator

•

0 (Transaction risk analysis exemption not

claimed/requested.)

• 1 (Transaction risk analysis exemption

claimed/requested.)

NOTE:

If the TRA exemption does not

apply to the

transaction, the value of 0 is

optional and the tag

may be omitted entirely

• Tag 8A - Tag indicates that the transaction is using

Visa Delegated Authentication during

authorization; also referred to as the Delegated

Authentication indicator

Possible Values:

• 0

(Delegated authentication does not apply to

the transaction)

• 1 (Issuer has delegated SCA)

NOTE:

If the delegated authentication does not apply to the

transaction, the value of 0 is optional and the tag may

be omitted entirely

Apart from the exemption tags present in Dataset ID

Hex 4A, two additional tags are present in Dataset ID

Hex 02:

• Initiating Party Indicator – Tag 80

This is used to indicate to the Issuer that this

transaction was flagged as an MIT. This field

cannot be populated by an Acquirer. Visa net will

populate this value if the Acquirer has indicated

the transaction is an MIT using

the MIT

Framework.

Possible Values:

• 1 (Populated by Visa if Acquirer indicated this

transaction as Merchant Initiated)

• Acceptance Outage Indicator – Tag 87

The indicator means that authentication was

attempted for a transaction but there was an

authentication outage in the authentication flow

between the merchant, gateway 3-D Secure (3DS)

server, and directory server, which means an

authentication request was not possible and an

authentication response could not be received.

(This indicator cannot be used to indicate an

outage in the Issuer processing domain, including

agents acting on behalf of the Issuer).

Possible Values:

• 0 (No authentication outage)

• 1 (Authentication outage)

If there is no Authentication outage, the value of 0 is

optional and the tag may be omitted entirely.

In Dataset ID 01, there is T

ag 86 called ‘Authentication

data’. This will include the 3-

D Secure Protocol version

number and is populated by Visa. Values:

• 1.x.x (3DS 1.x.x)

Version 3.0

12 January 2021

25

Field

Set by

Function

Field Value/Indicator

•

2.x.x (EMV 3DS 2.x.x)

• 2.2.x (EMV 3DS 2.2.x)

• UNKNOWN (Unknown 3DS

protocol version

number)

F39 Issuer

Response to F34 exemption request

indicating additional customer

authentication required

Response code 1A – SCA Decline Code

F44.13 Acquirer CAVV /TAVV Results Code

One-character code indicating classification of the

CAVV / TAVV and the pass/fail result. For token

transactions, if no CAVV, the TAVV result code can be

populated here. If both are present, then the CAVV

Result Code is in this field and the TAVV Result Code

is in field 123

F60.8 Acquirer

Mail/Phone/Electronic Commerce and

Payment Indicator indicating the ECI Value

Existing values as defined in the Visa technical

specification

14

F60.10 Acquirer

Indicates a transaction performed with an

estimated amount

2 or 3

F62.2

Acquirer –

when

submitting

an MIT

(otherwise

set by Visa

on every

single

transaction)

May be used by Acquirers to indicate a

transaction is an MIT: Acquirers may

indicate the Tran ID of the initial CIT (or in

some instances of a previous MIT)

associated with the current MIT in either

F62.2 or F125. Visa forwards this

information to Issuers only in F125

The Tran ID seen by Issuers in F62.2 is that

of the current MIT, as sent by Visa, and not

that of the initial CIT

This is a 16 digit value

F63.3 Acquirer

Indicates if the transaction is an out of

scope MIT of the following type:

• Incremental

• Delayed Charges

• No Show

• Resubmission

• Reauthorization

Indicates the transaction is deferred.

Values 3900 to 3904 indicate MITs

Value 5206 indicates the transaction is deferred, i.e.

that it could not be submitted at the time of the

Transaction due to no connectivity, system issue or

other limitations.

F123 VisaNet

Contains additional data relating to a token

transaction

Includes the TAVV Results Code in Dataset 67, tag 08.

F125 Acquirer

Acquirers may indicate the Tran ID of the

initial CIT

(or in some instances of a

previous MIT) transaction associated with

the current MIT in either F62.2 or F125. Visa

forwards this information to Issuers only in

F125

For Issuers in an MIT transaction, the Tran ID

associated with the initial CIT (or in some limited

instances the with a previous MIT) where agreement

was set up (and SCA performed) see Section 3.9.2.1 for

more details

F126.13 Acquirer

Used to indicate (with F125 or F62.2) if the

transaction is a Recurring,

Value R, I or C

Version 3.0

12 January 2021

26

Field

Set by

Function

Field Value/Indicator

Installments/Prepayment or Unscheduled

Credential on File out of scope MIT

F126.20 VisaNet

3DS Indicator: optional field that identifies

the authentication method used by the

Issuer ACS (e.g. Risk Based Authentication).

For more details see below

Values 0 to F – see Table 5 in Section 3.2.6

F126.8 Acquirer TAVV Data

If CAVV and TAVV are present, then TAVV Data is in

this field. If only TAVV is present, then Acquirer can

populate in this field of field 126.9

F126.9 Acquirer CAVV / TAVV Data

Usage Field 3 supported for EMV 3DS

If CAVV is present, this field contains the CAVV. For

token transactions without a CAVV, the TAVV can

optionally be delivered in this field

The function of each of these fields and the values/tags is described in more detail below.

Figure 6: Main message flows for a simple e-commerce transaction

Authorization

response

Authorization

request

ECI Value (F60.8)

CAVV Data (F126.9) (where available)

Exemption Indicator (F34)

ECI Value (F60.8)

CAVV Data (F126.9) (where available)

CAVV Validation Results (F44.13)

Exemption / Out of Scope Indicator (F34)

3DS Indicator (F126.20) (where available)

CAVV Validation results (F44.13)

3DS Indicator (F126.20) (where available)

VisaNet

Acquirer

Issuer

ECI – Electronic Commerce Indicator

CAVV

– Cardholder Authentication Verification Value

Authorization

request

Authorization

response

CAVV Validation results (F44.13)

Version 3.0

12 January 2021

27

3.2.3 VisaNet Field 34 & SCA decline code (Response Code 1A) in Field 39

Visa has implemented Field 34 to support PSD2 SCA requirements by indicating an Acquirer

applied exemption. Additionally, an SCA decline code (Response Code 1A) in Field 39 is

available to Issuers to indicate that the transaction cannot be approved until SCA is applied.

Acquirers can use Field 34 to submit e-commerce transactions that may include one of the

SCA exemption indicators in order to communicate to the Issuer why SCA was not performed

on an e-commerce transaction. However, Acquirers should specify only one SCA exemption

indicator per transaction message. In the event that the Acquirer specifies multiple SCA

exemption indicators, V.I.P. will pass all the SCA exemption indicators available in the

transaction to the Issuer, however this may have an adverse impact on Issuers’ approval rates.

Issuers are required to consider SCA exemption indicators and out of scope information when

deciding whether or not to approve an authorization request.

The tags listed in Table 4 above, are used to carry the SCA exemption indicators in the Field

34 Dataset ID 4A. These tags are ISO specification compliant and are no longer Visa specific.

Field 34 Dataset ID 56 also supports the addition of optional supplemental data through two

new tags. These carry the consumer device IP address and the Visa Consumer Authentication

Service (VCAS) score, for Issuers using VCAS. This supplementary information aims to help

Issuers improve their approval rates.

Issuers and Acquirers in Europe are mandated to support all SCA tags in Field 34 Dataset

Hex4A. The Tags in Dataset 02, i.e. the MIT Tag in Tag 80 is optional if Issuers choose to

recognise MITs via the MIT framework. Additionally the Acceptance Outage Indicator in Tag

87 is also optional as of the upcoming release (Oct 2020, Jan 2021). The right to apply and/or

accept the exemptions indicated in Field 34 remains that of the Acquirer and Issuer, and all

parties must be technically capable of sending and receiving these fields.

Issuers must complete VisaNet Certification Management Service (VCMS) certification before

the field is activated.

Table 22 in section 1094.4 provides a simple summary of the indicators for the key exemptions

along with the liability for fraud related chargebacks.

Impact for Acquirers

Acquirers in the Europe region must be able to:

Requirement

Acquirers should specify only one SCA exemption indicator per authorization

request.

If an Acquirer requests an exemption in the authentication process, it must be

mirrored during authorization. The Acquirer is responsible for this monitoring

activity and ensuring that the correct indicator is used throughout the

authorization process.

Issuers are required to consider SCA exemption indicators and out of scope

information when deciding whether or not to approve an authorization request.

Version 3.0

12 January 2021

28

1. Support Field 34—Electronic Commerce Data, Dataset ID 4A—Supplemental Data in TLV

format with tags to indicate whether an e-commerce transaction is exempt from the

PSD2/RTS SCA mandate

2. Receive the SCA decline code in existing Field 39

SCA decline code will be converted to 05 (Do not honor) in Field 39 if the non-EEA Acquirer’s

parameter is not activated in VisaNet to receive the SCA decline code.

Certification is required for Acquirers to support TLV Field 34, which contains the new SCA

exemption indicators in Dataset ID 4A. Additional certification is not required for Acquirers to

receive the SCA decline code in existing Field 39.

Impact for Issuers

Issuers in the Europe region must:

1. Be able to receive TLV Field 34—Electronic Commerce Data

2. Use the SCA decline code when a transaction has been declined due to the

absence of SCA

3. Not use the SCA decline code for a transaction that is out of scope of SCA

Issuers may respond with the SCA decline code for both e-commerce and card present

contactless point of sale (POS) transactions.

Issuers that choose to receive the supplemental data must be able to receive the new Field 34

- Electronic Commerce Data, Dataset ID 56 - Supplemental Data in TLV format with new tags

and must be aware of new processing rules to support the new supplemental data.

Issuers must not use SCA decline code for all transactions out of scope of SCA or not requiring

SCA.

transactions that are deemed out of scope of SCA from a regulatory perspective,

specifically:

a. MOTO transactions

b. Merchant Initiated Transactions

c. Transactions performed with an anonymous payment instrument (e.g. an

anonymous prepaid card)

d. Transactions from a merchant acquired by an Acquirer located outside the EEA

(one-leg-out transactions). These merchants are asked to perform SCA on a

best effort basis. If the Issuer is not technically able to impose SCA, the Issuer

is not obliged to decline. The Issuer should make their own approval decision

based on risk and liability considerations

Other transactions that do not contain a valid CAVV where SCA is not required, specifically:

a. Zero value authorization/account verification requests

b. Original Credit Transactions

c. Refunds

Version 3.0

12 January 2021

29

For more information on Visa Rules governing the use of the SCA decline code please see

PSD2 Strong Customer Authentication for Remote Electronic Commerce Transactions – European

Economic Area: Visa Supplemental Requirements. For information on identification of

transactions that do not require SCA see sections 3.2.9 and 4.2.4.2.

Use of SCA decline codes in cross border transactions

From the relevant regulatory enforcement dates for e-commerce, Issuers within the EEA and

the UK will be required to request that any transaction submitted without SCA or without a

correct out of scope or exemption indicator is responded to with a request to resubmit with

SCA or the transaction will be declined. Under managed migration programs being

implemented in some markets the so called “soft decline" (SCA decline code) will be applied

progressively by Issuers ahead of the enforcement date.

As enforcement dates may vary between markets, notably between the EEA and the UK, there

will be a period when there is a heightened risk of declines if EEA Issuers respond to cross

border transactions at, for example, UK acquired merchants with an SCA decline code while

UK merchants are still unable to respond to the code and submit the transaction for

authentication. This may result in merchants that are unable to respond losing transactions.

Subject to any further developments, the UK could become a third country for the purposes

of PSD2 from 1 January 2021. The UK currently plans to enforce equivalent requirements to

SCA for e-commerce in the UK from 14 September 2021, but until this point the UK may be

considered ‘one-leg-out’.

Therefore, during this time, relevant PSPs may need to apply SCA on a best efforts basis which

may in some circumstances mean Issuers choose not to decline transactions without SCA. The

Issuer should make their own approval decision based on risk, customer experience and

liability considerations. On this basis:

• EEA Issuers should not use SCA decline codes for UK acquired transactions during

the period 01 January to 14 September 2021. If an Issuer decides that they do not

want to approve the transaction, they should decline with another appropriate

response code.

• EEA and UK Issuers can and should use SCA decline codes for EEA/UK cross border

transactions from 14 September 2021

For guidance, on the recognition of one-leg-out transactions please see sections 2.3.2, 2.3.3

and 3.2.9.

3.2.4 MIT out of scope indicator for Issuers in Field 34

Visa has introduced a new indicator

15

to help Issuers to identify a transaction that is an MIT

and out of scope of SCA. The indicator is a value of “1” in Field 34 (Tag 80, Dataset ID 02) i.e.

the same field Issuers use to check for exemptions to SCA.

15

See Article 9.1.4 Changes to Identify Merchant-Initiated Transaction as Out of Scope for Strong Customer

Authentication, Oct 19 for more details.

Version 3.0

12 January 2021

30

Visa will automatically populate the value of “1” in TLV Field F34, Tag 80, Dataset ID 02 when

receiving a transaction indicated as an MIT by the Acquirer using the MIT Framework. Refer to

section 3.9 for more details.

An Issuer activated to receive F34 will automatically receive this value when the Acquirer has

indicated the transaction as merchant-initiated using the MIT Framework.

This enables Issuers to recognize a transaction as an out of scope MIT by simply looking for

the value of “1” in that tag. Issuers may alternatively decide to recognize an MIT out of scope

by looking at the indicators from the MIT Framework. See section 3.9 for more details.

An Issuer must not use an SCA decline code in a transaction legitimately indicated as an MIT

as the cardholder is not available to be authenticated.

An Acquirer cannot use Field 34, Tag 80, Dataset ID 02 to indicate an MIT out of scope.

3.2.5 New acceptance environment outage indicator in Field 34

Effective 22 January 2021, Visa is introducing a new indicator in Field 34 that will enable

Acquirers to flag that it is not possible to authenticate a transaction due to an outage in the

acceptance environment.

More specifically, the indicator means that authentication was attempted for a transaction but

there was an authentication outage in the authentication flow between the merchant, gateway

3-D Secure (3DS) server, and Directory Server, which means an authentication request was not

possible and an authentication response could not be received (this indicator should not be

used to indicate an outage in the Issuer processing domain, including agents acting on behalf

of the Issuer).

Issuer impact

Using this indicator is optional for Acquirers. Receiving this field is mandated for Issuers from

the April 2021 Business release. Acting on this indicator is however optional for Issuers. Both

Acquirers and Issuers need to consider regulatory requirements and resilience imperatives

before deciding to use this indicator. While transactions containing this indicator do not

represent transactions that can be considered exempt or out of scope of the SCA regulation,

the presence of the indicator enables the Issuer to understand that this is a transaction where

an authentication is expected but could not be performed due to an outage. This provides

Issuers with the ability to explain to a regulator why they may have decided to authorize an

in-scope transaction without authentication, on an exception basis, to support resilience.

Approving transactions with this flag and without authentication is at the Issuer’s discretion. It

is recommended that in deciding their authorization policies with respect to this indicator,

Issuers:

• Consider regulatory requirements balanced with the intent to support

resilience/business continuity/cardholder experience. Issuers could for example

decide to support the indicator every time it is sent or could decide to authorize

flagged transactions only when the outage is major/longer than unusual. Each Issuer

needs to determine its own policies

Version 3.0

12 January 2021

31

• Perform risk based analysis on each transaction and decline if the transaction is high

risk

• Ensure that reasons to decline other than lack of authentication are considered first

as usual (e.g. declines for insufficient funds, block card or similar that would inform

the merchant there is no opportunity for an approval)

Considering that authentication is not available due to an outage, European Issuers are

recommended to carefully consider whether use of an SCA decline code is appropriate. An

SCA decline code may indicate to the merchant that if the option is available to resubmit with

authentication once the 3DS environment is accessible, the Issuer may reconsider the response

if authentication is provided. Issuers should note however that authentication may not be

possible if the customer is no longer available.

Acquirer impact

The use of the indicator is optional for Acquirers. Acquirers need to consider regulatory

requirements and resilience imperatives before deciding to use this indicator. Acquirers must

be aware of additional conditions that will apply for their merchants to be permitted to use

this indicator, including Acquirer monitoring requirements

16

.

3.2.6 Deferred authorization indicator in F63.3