Clean Energy

Investment for

Development in

Africa

Status and opportunities

The IEA examines the

full spectrum

of energy issues

including oil, gas and

coal supply and

demand, renewable

energy technologies,

electricity markets,

energy efficiency,

access to energy,

demand side

management and

much more. Through

its work, the IEA

advocates policies that

will enhance the

reliability, affordability

and sustainability of

energy in its

31 member countries,

13 association

countries and beyond.

This publication and any

map included herein are

without prejudice to the

status of or sovereignty over

any territory, to the

delimitation of international

frontiers and boundaries and

to the name of any territory,

city or area.

Source: IEA.

International Energy Agency

Website: www.iea.org

IEA member

countries:

Australia

Austria

Belgium

Canada

Czech Republic

Denmark

Estonia

Finland

France

Germany

Greece

Hungary

Ireland

Italy

Japan

Korea

Lithuania

Luxembourg

Mexico

Netherlands

New Zealand

Norway

Poland

Portugal

Slovak Republic

Spain

Sweden

Switzerland

Republic of Türkiye

United Kingdom

United States

The European

Commission also

participates in the

work of the IEA

IEA association

countries:

Argentina

Brazil

China

Egypt

India

Indonesia

Kenya

Morocco

Senegal

Singapore

South Africa

Thailand

Ukraine

INTERNATIONAL ENERGY

AGENCY

Clean energy investment for development in Africa Abstract

PAGE | 3

IEA. CC BY 4.0.

Abstract

This report on financing clean energy investments in Africa was requested by the

Italian presidency of the Group of Seven (G7) to support the presidency’s new

Energy for Growth in Africa initiative. This initiative builds upon existing G7 efforts

to promote energy and climate investment in Africa and seeks to develop bankable

clean energy projects, attract public and private capital, encourage concessional

finance, and overcome investment barriers across Africa. This report aims to

inform the G7 initiative by providing an overview of the energy-related investments

needed to achieve all African energy and climate-related goals, including universal

energy access and its nationally determined contributions, by 2030. It then

explores how clean energy projects can best be financed, focusing on three key

investment pillars: household access to modern energy; the electricity sector; and

emerging industries. Finally, it identifies the main types of initiatives needed to

develop human and institutional skills and capabilities across Africa, without which

the financing of clean energy will remain a challenge in many countries. With

energy vital to Africa’s long-term prosperity and the need for investment in clean

energy technologies in Africa never being more urgent, this report comes at a

critical time and lays the foundations for coordinated financing efforts between

governments of African countries and developed nations, international financial

institutions, and development organisations.

Clean energy investment for development in Africa Table of contents

PAGE | 4

IEA. CC BY 4.0.

Acknowledgements, contributors

and credits

This study was prepared by the Directorate of Sustainability, Technology and

Outlooks in co‐operation with other directorates and offices of the International

Energy Agency (IEA). Daniel Wetzel, Head of the Tracking Sustainable

Transitions Unit and Carlo Starace co-ordinated the production of the report.

Trevor Morgan provided writing support to the report and carried editorial

responsibility.

Key IEA contributors to the report include: Nouhoun Diarra, Darlain Edeme, Emma

Gordon, Martin Kueppers, Isabella Notarpietro, Carlo Starace, and Gianluca

Tonolo. Sylvia Beyer, Yunyou Chen, Roland Gladushenko, Luca Lo Re, Vera

O’Riordan and Nikolaos Papastefanakis provided essential support.

Other valuable contributions were made by Araceli Fernandez Pales and Uwe

Remme.

Erin Crum was the copyeditor.

Valuable comments and feedback were provided by other senior management

and numerous colleagues within the IEA, in particular, Laura Cozzi.

Thanks go to the IEA’s Communications and Digital Office for their help in

producing the report and website materials, particularly Poeli Bojorquez, Curtis

Brainard, Astrid Dumond, Liv Gaunt, Grace Gordon, Julia Horowitz, Oliver Joy,

Jethro Mullen, Clara Valois and Therese Walsh.

The work was commissioned by the 2024 Group of Seven (G7) Presidency of Italy.

The work reflects the views of the International Energy Agency Secretariat but

does not necessarily reflect those of individual IEA member countries or of any

particular funder, supporter, or collaborator. None of the IEA or any funder,

supporter or collaborator that contributed to this work makes any representation

or warranty, express or implied, in respect of the work’s contents (including its

completeness or accuracy) and shall not be responsible for any use of, or reliance

on, the work.

Clean energy investment for development in Africa Table of contents

PAGE | 5

IEA. CC BY 4.0.

Table of contents

Executive summary .................................................................................................................. 6

Introduction ............................................................................................................................. 10

Chapter 1. The outlook .......................................................................................................... 12

The Sustainable Africa Scenario ................................................................................................. 12

Hurdles to ramping up clean energy investment ......................................................................... 17

Chapter 2. Access to energy ................................................................................................. 20

Key targets and investment needs .............................................................................................. 20

Financing vehicles and instruments ............................................................................................. 22

Chapter 3. The electricity sector ........................................................................................... 26

Key targets and investment needs .............................................................................................. 26

Financing vehicles and instruments ............................................................................................. 28

Chapter 4. Emerging industries ............................................................................................ 34

Key targets and investment needs .............................................................................................. 34

Critical minerals ........................................................................................................................... 34

Financing vehicles and mechanisms ........................................................................................... 41

Chapter 5. Mobilising investment ......................................................................................... 43

Creating a conducive investment ecosystem .............................................................................. 43

Better leveraging public funds to attract private capital ............................................................... 44

Integrating cross-cutting developmental objectives ..................................................................... 52

Required capacity-building initiatives ........................................................................................... 55

Annexes ................................................................................................................................... 58

Annex A – Abbreviations and acronyms ...................................................................................... 58

Annex B – Units of measure ........................................................................................................ 60

Clean energy investment for development in Africa Executive summary

PAGE | 6

IEA. CC BY 4.0.

Executive summary

Increasing energy investment is at the heart of enabling

African prosperity

Africa’s aspirations for greater economic and social development depend

on access to affordable, reliable, modern and sustainable energy. Despite

immense energy resources, Africa remains energy poor. Today, around

600 million Africans still lack access to electricity and more than 1 billion still cook

their meals over open fires and traditional stoves using wood, charcoal, kerosene,

coal and animal waste. The consequences are dire in terms of health, education,

climate, and economic and social development, with many of these impacts

disproportionally affecting women and children. A lack of reliable and affordable

energy restrains Africa’s farmers from higher productivity; hinders industry, where

energy prices and affordability remain key determinants in competitiveness; and

limits the ability of countries to attract and cultivate new sectors of their economies.

Enhancing Africa’s energy systems can address these issues, but

mobilising more investment remains challenging. Today, Africa accounts for

around 20% of the world’s population but attracts less than 3% of spending on

energy. Energy investment on the continent has been falling since its peak in 2014

and is down by 34%. Increasing investment in domestic energy systems faces

hurdles, notably a shortage of bankable projects and the high cost of capital, which

can be two to three times higher for renewable projects in Africa than in advanced

economies. Overlapping crises have also raised the bar for attracting new capital

to Africa. Currently, 21 African countries are in or are at high risk of being in debt

distress, weighing heavily on public balance sheets and those of state-owned

enterprises (SOEs). At the same time, higher interest rates have increased the

expectations on returns in commercial markets. For clean energy projects in

emerging market and developing economies, this has resulted in an increase in

expected returns greater than those in advanced economies.

Meeting growing energy demand from African countries requires a more

than doubling of annual energy investment by 2030, of which three-quarters

is in clean energy. The IEA’s Sustainable Africa Scenario lays out a pathway in

which Africa achieves all its energy-related goals in full and on time, including its

pledges on climate and access to electricity and clean cooking, and aligns with

the goals of the African Union’s Agenda 2063: The Africa We Want

. In this

scenario, energy investment in Africa grows to almost USD 240 billion annually by

2030. This report – commissioned by Italy’s G7 Presidency in support of its new

initiative: Energy for Growth in Africa – lays out key areas for investment that are

Clean energy investment for development in Africa Executive summary

PAGE | 7

IEA. CC BY 4.0.

consistent with the objectives set by countries in Africa and supports the

realisation of the Dubai Consensus’s objectives of tripling renewable capacity and

doubling energy efficiency by 2030. The report also highlights financing

mechanisms best suited to ensure these investments materialise in a timely

manner.

Investments in energy access and the power sector

remain the top priority for new energy infrastructure

Extending access to electricity and clean cooking remains the most

important lever for growth and development, and is central to a just energy

transition. From 2023 to 2030, around USD 22 billion per year is required to

connect all African homes and businesses to electricity, while USD 4 billion per

year is needed to provide them with clean cooking solutions. In total, the needed

annual investments in access for Africa equate to less than 1% of current energy

investment worldwide. There are also affordability challenges to consider; only half

of households without electricity access today would be able to afford basic energy

services without additional financial support, and even fewer would be able to

afford modern cooking solutions. A number of private companies based in Africa,

many of which are small and medium-sized enterprises, are offering innovative

solutions beyond traditional public-sector-led approaches but scaling them

requires more financing and specialised incentives to reach rural areas. Recent

multilateral efforts are attracting greater political attention to energy access and

bringing in new concessional and commercial funding, including the USD

2.2 billion in new financing mobilised at the Summit for Clean Cooking in Africa.

Around half of the energy investment required in Africa to 2030 is needed in

electricity, where policies play a key role in attracting more investment. Total

electricity sector investment increases from just under USD 30 billion in 2022 to

more than USD 120 billion in 2030 in the Sustainable Africa Scenario, with around

50% going towards renewable generation alone. Africa is home to some of the

most cost-competitive renewable resources in the world, with 60% of the best solar

resources globally, and many countries are home to high-potential resources for

hydropower, geothermal, and wind. Utility-scale renewable power projects, often

based on power purchase agreements, have found a foothold in markets with

access to commercial finance in Africa, where around 80% of clean power projects

by volume have reached investment decisions in the last five years. However, less

developed markets, where three-quarters of African people live today, face greater

perceived investment risks, especially where utilities are not seen as a credible

off-taker. Authorising the use of concessional agreements or other regulatory

carve‐outs for private investors can help attract new capital to debt-distressed

utilities, as can tariff reform, though such approaches need to guard against the

real risks of offering terms that are ultimately costly to consumers and

governments.

Clean energy investment for development in Africa Executive summary

PAGE | 8

IEA. CC BY 4.0.

New industries, including those related to clean energy

technologies, can support Africa’s growing energy

sector

Developing industry goes hand-in-hand with the expansion of Africa’s

energy system. By 2030, Africa is projected to build more floor area than exists

in Japan and Korea today. Accordingly, demand for steel and cement is set to

grow considerably from today’s levels, alongside rising demand for irrigation

pumps, cold chains, data centres and mining. Productive uses – which include

industry, agriculture, freight, and public and commercial buildings – make up

nearly half of the growth in electricity demand in Africa over the last ten years.

These are often large and reliable customers that can financially encourage the

development of new energy infrastructure. Based on today’s prices, these uses

cover two-thirds of Africa’s electricity expenditure, despite only representing just

over half of Africa’s electricity demand. If structured well, development financing

support for African industries can play a dual role: creating reliable off-takers for

new energy projects, while also providing the right incentives to install the efficient

equipment that will underpin the energy systems of the future. This is increasingly

important for new steel plants, with some countries currently electing to use coal-

based technologies instead of hydrogen-ready, natural gas-based technologies

which are cost-competitive for countries with easy access to natural gas.

Critical minerals and the manufacturing of clean energy technologies

present practical opportunities to cultivate a growing industrial base.

Revenues from the production of copper and key battery metals in Africa are

already estimated to be more than USD 20 billion annually. The current pipeline

implies a 65% increase in market value is possible by 2030, with significant

potential for further growth given that investment in mineral exploration is on the

rise again. New manufacturing plants for clean energy technologies and solutions

to improve energy access are being developed across the continent as well,

including some backed by the development finance institutions of G7 members.

Additionally, low-emissions hydrogen production from announced electrolyser

projects in Africa could reach 2 Mt by 2030 if all projects come to fruition.

Investments in these fast-growing sectors can help diversify global supply chains

and reduce import burdens for Africa. If well-designed, these projects could also

be powered by energy investments that serve Africa’s wider domestic energy

needs, and ensure their development creates jobs, supports local communities,

and meets important health, safety, and labour criteria.

Boosting energy investment relies on private sector

participation, which concessional finance can help

unlock

Private sector spending needs to grow 2.5 times between 2022 and 2030 to

meet Africa’s energy investment needs. In the Sustainable Africa Scenario,

USD 190 billion of private capital is required by 2030, growing from around

Clean energy investment for development in Africa Executive summary

PAGE | 9

IEA. CC BY 4.0.

USD 75 billion today. Concessional capital from international sources will play a

key role in mobilising this increase, with an estimated USD 30 billion per year for

clean energy projects required to mobilise commercial funding over the 2023-2030

period.

Blended finance, a proven tool, can attract commercial financing that is up

to seven times the level of concessional funding from donors. Blended

finance – whereby donors, development finance institutions (DFIs) and

philanthropies use their funds to improve the risk-return profile of projects and

attract private capital to a project – will be crucial to achieving the level of

investment needed in the Sustainable Africa Scenario. The number of deals using

blended finance in Africa has grown since 2014, with the volume doubling from

2019 levels to reach more than USD 3 billion in 2021. Other instruments have also

demonstrated their ability to improve the risk-return profile of energy investments,

including green, social, sustainable and sustainability-linked (GSSS) bonds;

carbon credits and voluntary carbon markets; syndication platforms and pooled

investment vehicles, and instruments to address currency risk.

Connecting concessional finance with the right projects

remains a barrier but can be addressed

Ongoing initiatives within the G7 can be reinforced with targeted technical

assistance and improved coordination. G7 countries have reiterated their

commitment to mobilise more energy and climate investment in Africa in the

Climate, Energy and Environment Ministers’ Meeting Communiqué

, including

reinforcing capacity building efforts. Over the past 10 years, advanced economies

have provided, on average, USD 2.4 billion of development assistance to Africa’s

energy sector annually. Our tracking shows that G7 members have programmes

operating in nearly every country in sub-Saharan Africa with the aim of delivering

greater energy and climate-oriented investments. These include Global Gateway,

Just Energy Transition Partnerships, and the Partnership for Global Infrastructure

and Investment. Many of these initiatives face similar challenges, notably

developing a pipeline of bankable projects and guiding them through the higher-

risk development and construction phases. A survey of ongoing activities,

however, highlights several effective approaches that can help to address these

gaps – notably capacity building with African governments and small and medium-

sized enterprises (SMEs), and developing new financing vehicles that absorb

early-stage development risk. Scaling these efforts will be key to unlocking more

finance for Africa’s energy sector, and to ensuring these investments realise the

full suite of economic, development, energy security, health and climate benefits.

Clean energy investment for development in Africa Introduction

PAGE | 10

IEA. CC BY 4.0.

Introduction

Energy is vital to Africa’s long-term prosperity. It can unlock sustainable economic

growth, improve human well-being, and enable healthier and more productive

lives. The recent energy crisis, following on the heels of the Covid-19 pandemic

and ensuing global economic disruption, has hit many African countries hard.

Access to modern energy services remains a pressing concern, primarily in sub-

Saharan countries, where half the population still lacks electricity, and four out of

five people do not have access to clean and healthy cooking methods. Soaring

energy prices and the financial difficulties of electricity utilities have recently

reversed the progress that had been made in expanding energy access. There

has never been a more urgent need for a concerted push for investment in clean

energy technologies to ensure universal access to modern energy, drive economic

and social development, and eradicate the poverty that persists across much of

Africa.

This investment will not happen on a sufficiently large scale without strong

interventions by the governments of African countries and the assistance of

developed nations, international financial institutions and development

organisations. Financing Africa’s energy development is a massive undertaking

and must overcome several hurdles – notably the high cost of capital faced by

investors in energy projects and a lack of bankable projects. Evidence of this can

be seen in Africa’s ability to attract financing to its energy sector: while Africa

accounts for around 20% of the world’s population, it attracts less than 3% of its

spending on energy, and energy investment in the continent has been falling in

recent years. Mobilising international funding, notably concessional finance, will

be crucial.

This report aims to provide an overview of the energy-related investments that are

needed to meet the targets set out by African countries in their nationally

determined contributions (NDCs) under the Paris Agreement, their net zero goals,

the United Nations Sustainable Development Goal 7

(SDG 7) on access to

affordable and clean energy, and the 2023 Nairobi Declaration on climate change.

The report also analyses how clean energy projects would need to be financed

and the supporting policies and measures required to make that happen, focusing

on three key investment pillars: household access to modern energy; the electricity

sector; and emerging industries, including manufacturing of clean energy

technologies, hydrogen and related fuels, and critical minerals. Finally, the report

identifies the main types of initiatives needed to build human and institutional skills

and capabilities in Africa, without which the financing of clean energy will remain

constrained in many countries.

Clean energy investment for development in Africa Introduction

PAGE | 11

IEA. CC BY 4.0.

This report on financing clean energy investments in Africa was requested by the

Italian Presidency of the Group of Seven (G7). African development is a major

focus of Italy’s G7 agenda, exemplified by the Italy-Africa Summit held in January

2024, which was attended by high-level representatives from 46 African countries,

major international organisations – including the IEA – international financial and

development institutions, multilateral development banks, and leaders of the

European Union.

The Italian G7 Presidency's new initiative, Energy for Growth in Africa, aims to

build upon existing G7 efforts to promote sustainable energy in Africa by

leveraging programmes from advanced economies, such as the Mattei Plan, to

direct development and climate funding towards financing vehicles that could

attract further private capital. Announced at the Climate, Energy and Environment

Ministers' Meeting on 29-30 April 2024 and launched at the G7 Summit on

13-15 June 2024, with the IEA as a knowledge partner and the United Nations

Development Programme (UNDP) as the implementation partner, this initiative

seeks to develop bankable clean energy projects, attract public and private capital,

encourage concessional finance, and overcome investment barriers across Africa.

This report aims to inform the G7 initiative by providing an overview of the energy-

related investments needed in the IEA’s Sustainable Africa Scenario (SAS). The

SAS is a pathway developed by the IEA that envisions the continent achieving all

its energy and climate-related goals, including universal energy access and its

NDCs, by 2030.

Clean energy investment for development in Africa Chapter 1: The outlook

PAGE | 12

IEA. CC BY 4.0.

Chapter 1. The outlook

The Sustainable Africa Scenario

Energy and investment trends

The Sustainable Africa Scenario (SAS), first set out in the IEA’s Africa Energy

Outlook 2022, describes a realistic pathway for the continent to achieve the

energy-related goals set out in Sustainable Development Goal 7, including

universal access to modern energy by 2030, as well as fulfilling all announced

climate pledges, including conditional NDCs, in full and on time.

1

This requires a

steep increase in investment, a shift away from export-oriented projects towards

clean energy projects predicated on local demand, and enabling a greater role for

decentralised systems. This hinges on tapping into a range of new capital sources

and financing approaches.

Providing modern energy services to the 600 million Africans still lacking electricity

and the more than 1 billion without access to

clean cooking remains the priority of

the SAS. Economic growth across the region also drives higher demand for

modern energy from industry, transport and agriculture in this scenario. Modern

primary energy supply rises to 2030, an increase that is propelled mainly by

renewables accounting for more than four-fifths of the total, though oil use also

rises sharply, primarily due to strong growth in transport demand.

In the SAS, electricity use grows across all end-use sectors, with households

contributing more than half of the growth. In total, demand surges by more than

60% between 2022 and 2030 to 1 160 TWh, driven largely by more than a

doubling of household use of air conditioners, fans and refrigerators. The share of

electricity in total final energy consumption jumps from 10% to 20%. Renewable

energy generation, mainly from solar PV, accounts for most generating capacity

additions as declining costs drive rapid global uptake. By 2030, solar and wind

together provide 27% of the continent’s power generation, compared with barely

5% in 2022.

Energy trends to 2030 are very different across Africa. Although modern

renewables grow fastest everywhere, oil and gas continue to dominate energy

1

In the rest of the world, it is assumed that all announced global commitments to reach net zero emissions are fully

implemented, as per the Announced Policies Scenario. See the latest edition of the IEA’s World Energy Outlook

(WEO) for

further details.

Clean energy investment for development in Africa Chapter 1: The outlook

PAGE | 13

IEA. CC BY 4.0.

supply in North Africa and coal in South Africa, while renewables become the

dominant fuel category in sub‐Saharan Africa.

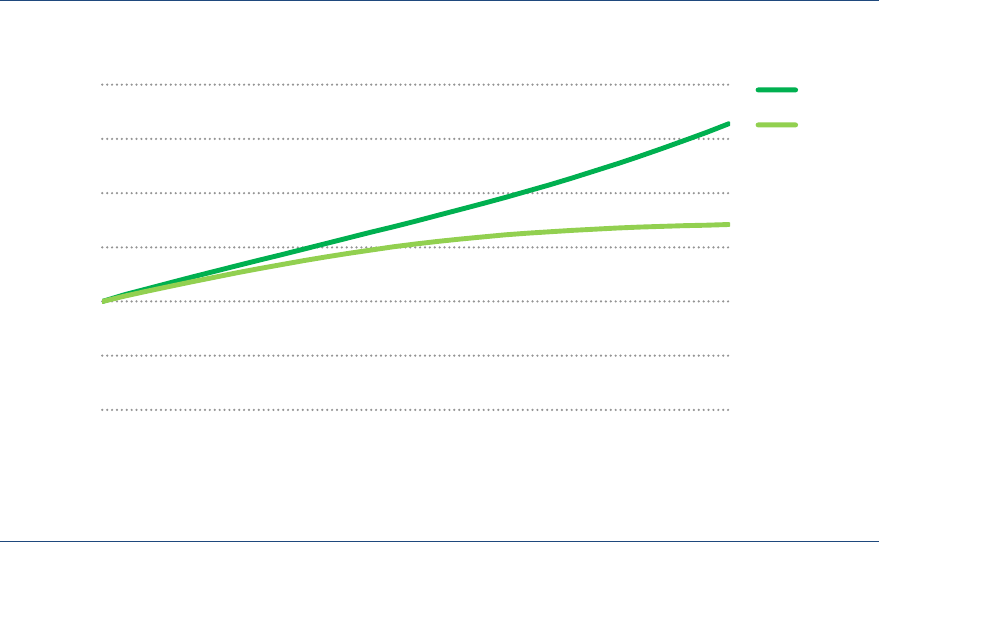

Tot

al energy investment in Africa was already declining prior to the Covid-19

pandemic (Figure 1.1). Historically, fossil fuel supply – primarily oil and gas

production – has dominated energy investment in Africa, and a sharp fall in

upstream investment explains most of the fall in overall capital spending since

2015. Investment fell even lower in 2020, and while it has been increasing slightly

year-on-year since then, in 2022 the almost USD 90 billion invested in energy was

equal to around 3.5% of Africa’s GDP, well below percentages seen in the decade

prior.

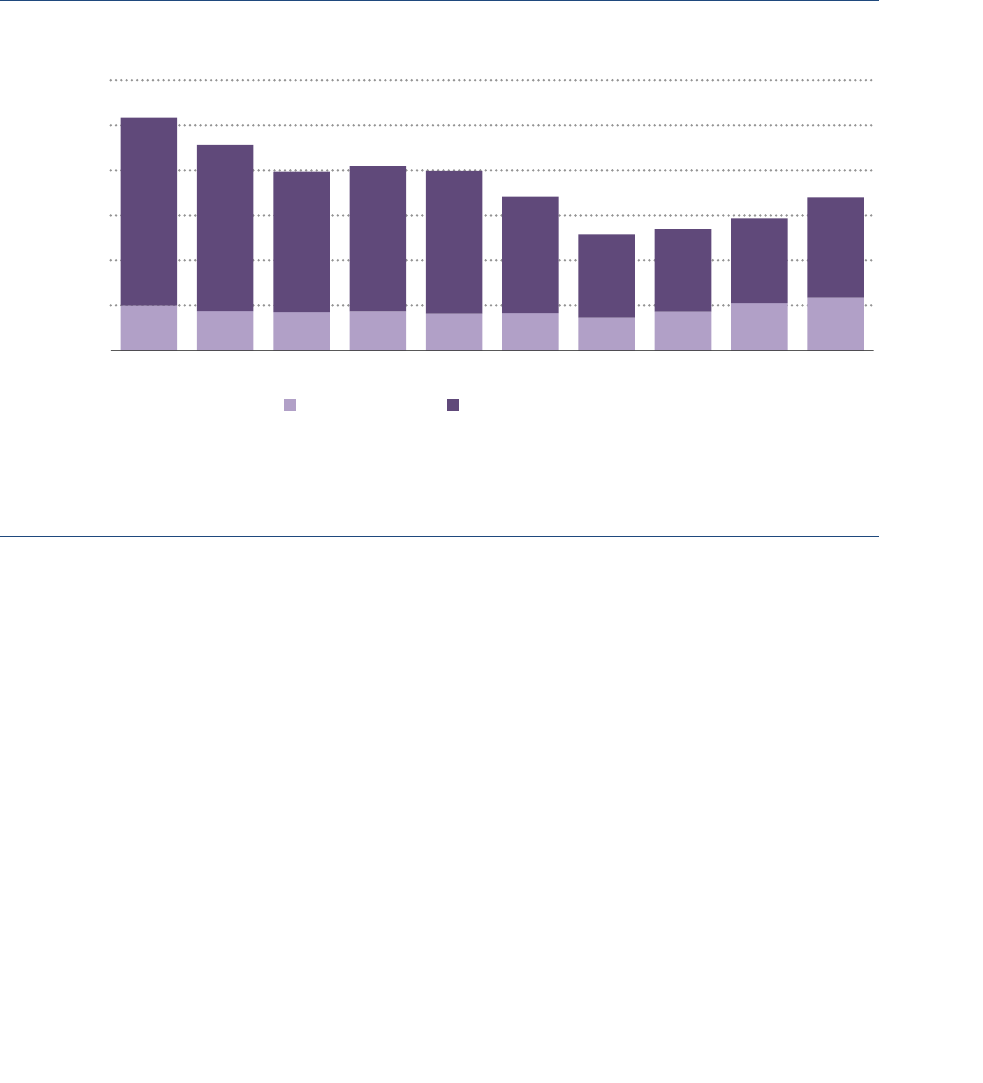

Figure 1.1 Energy investment in Africa by type, 2014-2023

IEA. CC BY 4.0.

Overall energy investments in Africa were on a downward trend in the 2015-2020 period,

although they have begun most recently to pick up

In the SAS, energy investment in Africa picks up in the period to 2030, driven by

a surge in clean energy spending (Figure 1.2). Clean energy investment rises to

reach nearly three-quarters of energy investment by the end of this decade. Still,

around 30% of total spending goes to fossil fuel supply over the 2022-2030 period.

Total annual investments in renewables and power grids see a substantial climb,

jumping from almost USD 39 billion in 2023 to an average of USD 172 billion in

2028-2030.

30

60

90

120

150

180

2014 2015 2016 2017 2018 2019 2020 2021 2022 2023

Clean energy Fossil fuel-related

Billion USD (2022, MER)

Clean energy investment for development in Africa Chapter 1: The outlook

PAGE | 14

IEA. CC BY 4.0.

Figure 1.2 Average annual energy investment in Africa by sector and share by type of

energy and investor in the Sustainable Africa Scenario

IEA. CC BY 4.0.

Annual capital spending on energy grows more than double, reaching an average of

USD 225 billion in 2028-2030, with three-quarters of the investment in clean energy

Renewable generation and power grids together account for close to 70% of the

clean energy investment needed over 2023-30 in the SAS and over 80% of all

new power generation capacity added over 2023-30. Solar remains the largest

growing source, as Africa is home to 60% of the best solar resources

globally, yet

only 1% of installed solar PV capacity today. By 2030, solar PV – already the

cheapest source of power in many parts of the continent – outcompetes all other

generating technologies continent-wide. These capacity additions call for large

investments in grid infrastructure, both to expand network capacity and to upgrade

grids to provide adequate flexibility and support the integration of renewables,

including through the installation of digital technologies (see Chapter 3). Regional

interconnections need to be strengthened and their operations better integrated to

effectively manage the impact of intermittency of renewable power generation on

the stability and reliability of national power systems. Dispatchable power

providers such as hydropower, natural gas, battery and pumped-hydro storage

are also needed to provide flexibility.

Investment to reach the goal of universal access to modern energy averages

USD 26 billion per year over 2022-30 in the SAS, accounting for around 15% of

total African energy investment. Of this investment, USD 22 billion per year goes

to electricity access, while around USD 4 billion is channelled to provide

individuals with clean cooking devices. Mobilising this level of investment is

contingent on a major policy push for access projects, involving the establishment

of national targets and action plans that clearly lay out the role of different energy

access solutions and providers, coupled with new financing solutions to support

2028-30

2025-27

2023

50 100 150 200 250

3% 4% 5% 6% 7%

Billion USD (2022, MER)

Share of GDP

Fuel supply

Power

End use

Share of GDP

Investment by sector and share of GDP

Shares by type of energy

Investment

Fossil fuel-related

Clean energy

Energy share

Clean energy investment for development in Africa Chapter 1: The outlook

PAGE | 15

IEA. CC BY 4.0.

the effective use of public funds and attract private capital where possible (see

Chapter 2). Investment is also needed to drive the switch to electric two- and three-

wheelers, as well as green public transport such as electric buses and urban rail

systems, and the use of renewables in buildings and industry for heating and

cooling.

Sources of finance

In the SAS, private investment increases 2.5 times between 2022 and 2030 in

absolute terms, buoyed by policy reforms and the use of concessional capital from

development finance institutions (DFIs) to de-risk projects. Concessional financing

takes many forms but typically involves several broad instruments including grants

that do not need to be repaid, loans with very favourable interest rates or

guarantees whereby a third party agrees to cover losses in case repayments

cannot be made. DFIs

2

play the dual role of investing their own capital, both in

projects via debt and equity and in early-stage development financing, while also

using their concessional funds to mobilise private capital (Figure 1.3). Finance for

energy projects in Africa from DFIs in advanced economies has largely been

stable at around USD 11 billion annually, while Chinese DFI activity boomed in

the middle of last decade at USD 14 billion but has fallen back substantially in

recent years (Box 1.1). In total, an average of around USD 30 billion per year of

concessional finance is required in the SAS between now and 2030 to help attract

the USD 190 billion of private capital for energy projects in 2030 needed in that

same scenario.

Today, DFI finance plays a particularly prominent role in renewable power

generation, including that related to electricity and clean cooking access projects,

and emerging technologies (such as low-emissions hydrogen). State-owned

enterprises (SOEs) retain a key role in grids and storage, although achieving the

necessary level of investment relies on improving their financial health, which has

deteriorated in many cases

in recent years, most likely requiring grants and other

forms of concessional support from DFIs and donors.

2

Multilateral development banks (MDBs), other international and regional financial institutions, national development banks

and export credit agencies.

Clean energy investment for development in Africa Chapter 1: The outlook

PAGE | 16

IEA. CC BY 4.0.

Figure 1.3 Sources of finance for clean energy investments in Africa by sector,

provider and instrument in the Sustainable Africa Scenario, 2030

IEA. CC BY 4.0.

The private sector plays the main role in all energy investment categories except grids

by 2030, with equity remaining important for new technologies and end-use sectors

Note: SAS = Sustainable Africa Scenario; DFI = development finance institution.

Source: IEA (2023), Financing Clean Energy in Africa

.

Scaling up investment in energy hinges on mobilising capital providers and

financing instruments to match the capital structure of energy companies and

assets. As with most project finance investments, debt plays a large role in most

clean energy developments. Commercial debt in Africa can be expensive and in

short supply since debt markets are small outside South Africa, while public debt

has become increasingly unsustainable in many economies. Currently, 21 African

countries are in or are at high risk of being in debt distress, weighing heavily on

public balance sheets and those of SOEs. At the same time, higher interest rates

have increased the expectations of returns in commercial markets. For clean

energy projects in emerging market and developing economies this has resulted

in an increase in expected returns greater than those in advanced economies.

However, alternative financing approaches exist, each utilising different debt-to-

equity ratios according to the stage of the project. While the role of debt increases

in the SAS, equity remains essential where risks are higher, such as in new

markets and for novel technologies. Equity capital is limited in most African

countries, with many of the equity funds which currently finance energy projects

funded by DFIs. Other sources of equity include corporate balance sheets and –

for start-ups and small and medium-sized enterprises – private equity and venture

capital firms.

50% 100%

Low-emissions fuels

Other end use

Efficiency

Grids and storage

Renewable power

Private

DFIs

Public

Debt

Equity

By provider

50% 100%

By instrument

Clean energy investment for development in Africa Chapter 1: The outlook

PAGE | 17

IEA. CC BY 4.0.

Hurdles to ramping up clean energy

investment

Improving access to affordable finance is key to achieving the huge increase in

investment in clean energy projects required to put Africa on a sustainable

development path. At present, there are several hurdles to financing such projects,

reflected in the high cost of capital relative to other parts of the world; the

weighted

average cost of capital for renewable generation projects in Africa is currently at

least two to three times higher than in the advanced economies and China (see

Figure 1.4). This is due to the greater risks, real or perceived, of investing in Africa.

Box 1.1. Chinese investment in Africa’s energy sector

The involvement of the People’s Republic of China (hereafter “China”) in African

economies took off in the early 2000s, and the country became the continent’s

largest trading partner in 2009. China is now the fourth‐largest investor in Africa

and accounts for about one‐fifth of all lending, much of which goes to energy and

infrastructure projects. China committed to USD 150 billion in loans to Africa

between 2000 and 2018, roughly a quarter of which were in the energy sector.

However, lending to African power projects fell from its peak of almost

USD 14 billion in 2016 to USD 2 billion in 2019 as China’s policy banks focused

more on domestic projects.

Financing from China has primarily been in the form of large low-cost loans from

development banks and energy- or construction-oriented SOEs. The level of

lending has led to concerns around the sustainability of debt, particularly as

Chinese loans are generally exempt from the restructuring arrangement of the

Paris Club – a group of officials from major creditor countries whose role is to

develop co‐ordinated solutions to address payment difficulties in debtor countries.

Several African countries have been forced to renegotiate repayment terms,

notably in the case of loans to railways in Kenya and Ethiopia. Default risks on the

continent are rising due to the combination of increased debt since the Covid‐19

pandemic and inflationary pressures.

Changing dynamics point to a shift in China’s dealings with Africa. At the Forum on

China Africa Cooperation in November 2021, China’s president announced a one‐

third reduction in public financing to Africa and emphasised the growing role of

Chinese private investment, although no specific targets have been announced.

Together with China’s move away from funding coal plants abroad, this is likely to

result in more emphasis on renewable energy projects by Chinese developers.

Source: IEA (2022), Africa Energy Outlook 2022

Clean energy investment for development in Africa Chapter 1: The outlook

PAGE | 18

IEA. CC BY 4.0.

Figure 1.4 Cost of capital ranges for solar PV and storage projects taking final

investment decision in 2022

IEA. CC BY 4.0.

The cost of capital for solar PV and storage projects in EMDE is at least twice the value

in advanced economies, despite relatively larger interest rate hikes in advanced

economies

Notes: Values are expressed in nominal, post-tax and local currency. WACCs for solar PV projects represent responses for

a 100-megawatt (MW) project and for utility-scale batteries a 40 MW project. Values represent average medians across

countries. Advanced economies represent values in the United States and Europe.

Source: IEA (2024), World Energy Investment 2024; IEA (2024), Cost of Capital Observatory

.

Higher costs of capital act as a brake on private sector involvement as they make

projects either unaffordable or unviable for the investor. They can also leave

countries trapped in a loop of higher risks, higher costs, energy deficits and

deepened reliance on fossil fuels, which typically require less upfront investment.

A high cost of capital has a particularly large impact on capital-intensive

investments such as renewable power projects, including off-grid solutions. As a

result, it raises overall power generation costs, which are either passed on to

customers or absorbed by governments as subsidies.

The cost of capital largely reflects two sets of risks: those associated with the

country (the base rate) and those associated with the sector, project or company

(the premium). These risks vary considerably across the continent; some

countries have investment-grade credit ratings and/or a well-developed energy

sector, while others are plagued by social and political conflict or instability and

low economic growth, and thus struggle to attract investment. Costs also vary by

capital provider and currency, depending on whether the provider is taking on

currency risk, their familiarity with the local market and the base rate in their

country of origin, as well as according to the company or project that is seeking to

raise capital. Larger international companies are able to tap into concessional

finance from DFIs and donors or cheaper capital in international markets more

3%

6%

9%

12%

15%

Solar PV

Storage

Emerging market and

developing economies

Advanced economies

Clean energy investment for development in Africa Chapter 1: The outlook

PAGE | 19

IEA. CC BY 4.0.

easily. Meanwhile, local companies more reliant on domestic capital markets can

struggle to access both early-stage financing to make projects bankable and

sufficient affordable capital to develop projects.

Certain investment risks originate from outside the energy sector, but there are

financial tools, policy measures and technical assistance that can help mitigate

project-specific risks and help ensure more projects reach financial close. The

main energy sector-specific factors driving higher costs of capital for clean energy

projects according to a survey of investors

are regulatory risk (e.g. changing

regulations, government renegotiations of contract terms), off-taker risk (e.g. no

credible buyer, utility financial distress), land acquisition risks, and transmission

risks (e.g. delays in interconnection or not being able to reliable deliver energy to

the grid due to network issues). Addressing these risks will be key to the focus of

the new G7 initiative, Energy for Growth in Africa.

Clean energy investment for development in Africa Chapter 2: Access to modern energy services

PAGE | 20

IEA. CC BY 4.0.

Chapter 2. Access to energy

Key targets and investment needs

Ensuring that everyone has access to modern energy services remains the

primary developmental goal for Africa. According to IEA data, around 600 million

Africans lack access to electricity and more than 1 billion Africans – roughly two-

thirds of the population – still cook their meals over open fires and traditional

stoves, using wood, charcoal, kerosene, coal and animal waste. Most of these

people are in sub-Saharan Africa, concentrated in just five countries: Democratic

Republic of the Congo, Ethiopia, Nigeria, Tanzania and Uganda.

The consequences of such “energy poverty” are dire. A lack of electricity

undermines public health, education and communication and holds back

economic and social development. Poor air quality due to cooking indoors using

traditional fuels is the second-leading cause of premature deaths across the

continent. Women suffer the most, both directly from the pollution and from

forgoing opportunities to pursue schooling, employment and revenue-generating

economic activities as they spend five hours a day on average gathering fuel and

tending to cooking fires. A lack of clean cooking

also contributes to deforestation,

environmental degradation and climate change.

Africa was already well off track to reach the Sustainable Development Goal 7

(SDG 7) target, set in 2015, of universal access to modern energy by 2030 at the

beginning of 2020 and the Covid‐

19

pandemic. The recent energy crisis has set

back progress even more, despite a modest tick upward during 2023. Current

government policies fall far short of what is required to meet that goal, and without

additional measures, 550 million people will still be without access to electricity

and around 1 billion still without access to clean cooking even in 2030. Political

momentum is growing to resolve these issues, notably for clean cooking, with

renewed focus within the G7, G20, and Conference of the Parties (COP), and

USD 2.2 billion of new financial commitments

announced at the Summit on Clean

Cooking in Africa, convened in Paris on 14 May 2024. Still more is required to get

Africa on track to achieve universal access to modern energy services by 2030 –

a central pillar of the Sustainable Africa Scenario (SAS).

For every African to have access to electricity by 2030 (SDG 7.1), almost

70 million people, or 5% of the current total population, including 60 million from

rural areas, would need to gain access each year on average from 2023. In rural

areas, where more than 80% of Africans without electricity access live today,

progress needs to be even faster. Rural customers predominantly gain access

Clean energy investment for development in Africa Chapter 2: Access to modern energy services

PAGE | 21

IEA. CC BY 4.0.

through stand‐alone and mini‐grid systems, which can provide first access quickly

and represent roughly two‐thirds of new connections by 2030 in the SAS

(Figure 2.1).

Figure 2.1 Africans gaining access to modern energy by type and technology in the

Sustainable Africa Scenario, 2023-2030

IEA. CC BY 4.0.

Universal access to electricity is achieved largely through off-grid solutions, while

access to clean cooking comes mainly through improved cookstoves and LPG

Note: LPG = liquefied petroleum gas.

Source: IEA (2022), Africa Energy Outlook

2022.

Achieving universal access to clean cooking fuels and technologies by 2030

(SDG 7.2) in Africa requires an abrupt reversal of current trends; the population

without access has been climbing continuously. In the SAS, 130 million Africans

(including 80 million in rural areas) gain access to clean cooking each year

between 2023 and 2030 – roughly 10% of Africa’s current population each year.

Around 40% of the people gaining first‐time access to clean cooking by 2030 do

so with the use of solid biomass in improved biomass cookstoves, which is

generally the cheapest and most practical means of providing clean cooking in

rural areas. One‐third of the people gain access via LPG, 10% via electricity, 10%

via biogas from biodigesters and 6% via ethanol. In urban areas, LPG represents

a practical, quickly deployable clean cooking solution; however, more African

households adopt electric cooking after 2030 as electricity becomes more reliable

and connections are strengthened.

On average, around USD 22 billion per year in investment is required to connect

Africans to electricity sources and USD 4 billion per year to provide them with

clean cooking devices over 2023-30 in the SAS. These are modest sums – less

than 1% of current energy investment globally – and would bring enormous

42%

31%

27%

Electricity:

Grid

Mini-grid

Stand-alone

Clean cooking:

Improved cookstoves

LPG

Electricity

Biogas

Ethanol

Electricity

90 million

people

gaining

access per

year

41%

33%

10%

10%

6%

Clean cooking

130 million

people

gaining

access per

year

Electricity

Clean cooking

Clean energy investment for development in Africa Chapter 2: Access to modern energy services

PAGE | 22

IEA. CC BY 4.0.

benefits, such as better health, improved conditions for women and children, and

general economic development. However, mobilising this investment represents

a massive undertaking for the poorest African countries in view of the limited public

funds and local private capital at their disposal. Current investment falls far short

of these levels: in 2019, it amounted to just 10% of the average needs for

2023-2030 in the case of electricity and 3% for clean cooking (Figure 2.2). In the

case of electricity access, the bulk of investment to 2030 is needed for

decentralised mini-grids and stand-alone systems, mostly solar photovoltaic (PV)

based. For clean cooking, end-use equipment requires the most finance, with

infrastructure in fuel supply, delivery and supply chains needing about 40% of the

annual investment.

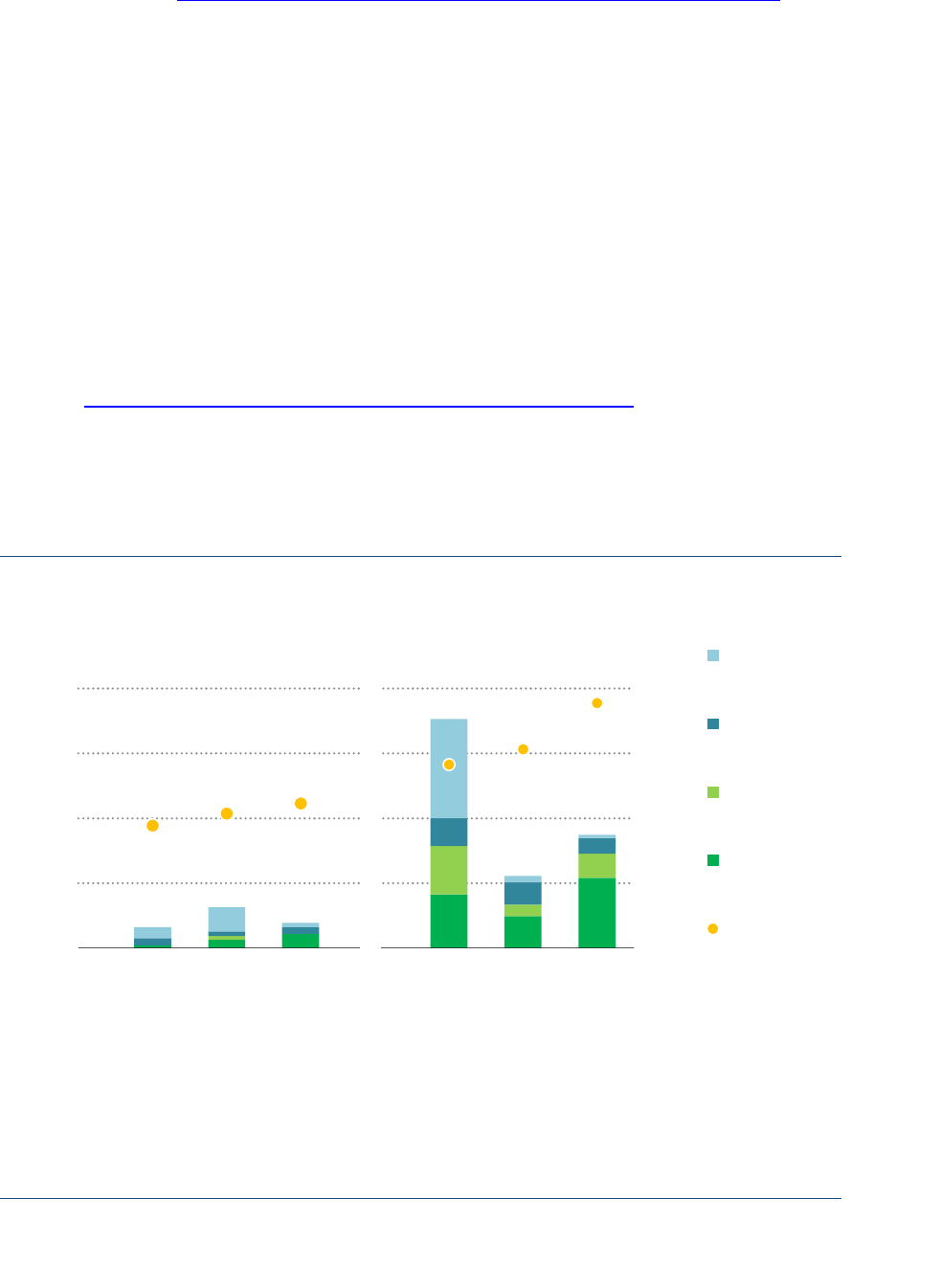

Figure 2.2 Annual investment in and people gaining access to electricity and clean

cooking in Africa in the Sustainable Africa Scenario, 2019 and 2023-2030

IEA. CC BY 4.0.

To achieve universal access, investment in electricity access infrastructure needs to

increase sevenfold and investment in clean cooking over twenty-fold

Note: Historical data for investment in access to electricity comprise not only first access projects, but also investment aimed

at improving the level of access for households already with access.

Sources: IEA (2023), A Vision for Clean Cooking Access for All

; IEA analysis based on SE4All and Climate Policy Initiative

(2021), Energizing Finance: Understanding the Landscape.

Financing vehicles and instruments

There is a range of financing vehicles and instruments available for energy access

projects, but in general, a high share of it would need to be concessional to

address the affordability gap that many African households face. While

accompanying infrastructure for grids and fuel distribution rely on a wider set of

30

60

90

10

20

30

2019 2023-2030

Billion USD (MER, 2022)

Historic Grid

Infrastructure Mini-grids

Stand-alone End-use equipment

People gaining access (right axis)

60

120

180

2

4

6

2019 2023-2030

Million people

Electricity

Clean cooking

Clean energy investment for development in Africa Chapter 2: Access to modern energy services

PAGE | 23

IEA. CC BY 4.0.

financing approaches and tools, they can also benefit from any measures that

improve end-user payment reliability (Table 2.1).

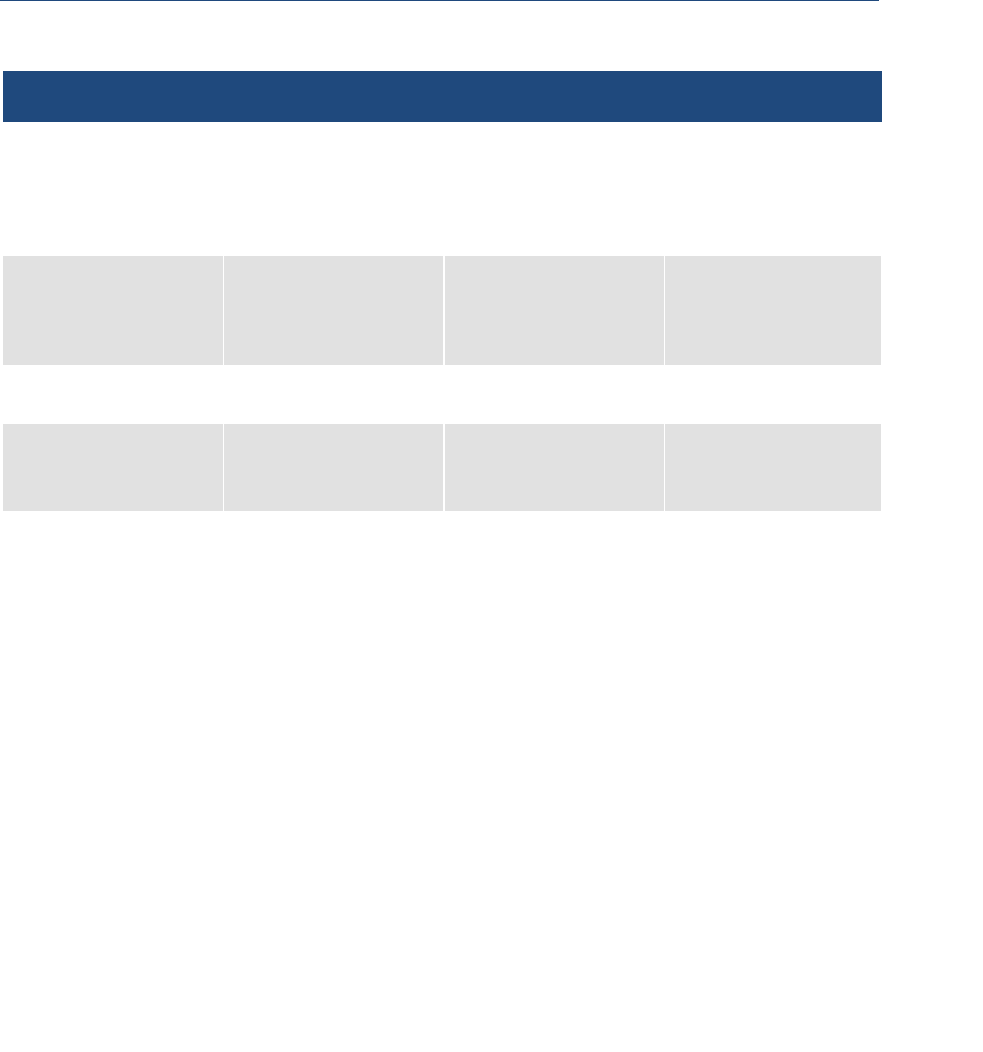

Table 2.1 Common financing instruments by type of energy access project and

project stage

Project type Development Operation

Grids

Grants

Concessional equity and debt

Corporate cash flow

Viability gap funding

Corporate bonds (if credit rating

allows)

Mini-grids

Grants

Concessional equity and debt

Commercial debt

Viability gap funding

Private equity (PE)/venture capital

(VC)

Commercial debt

Results-based finance

Aggregation/securitisation

Corporate (growth) equity and, where

possible, public listing

Stand-alone solar

Technical assistance and grants

Concessional equity and debt

Corporate equity (PE/VC)

Concessional or commercial debt

Results-based finance

Aggregation/securitisation

Corporate (growth) equity and, where

possible, public listing

Carbon markets

Clean cooking

Technical assistance and grants

Concessional equity and debt

Corporate equity (PE/VC)

Carbon markets

Results-based finance

Aggregation/securitisation

Notes: Equity can be concessional if it is provided in a subordinated or first-loss capacity, or if it has lower return expectations

or a longer time period to exit. Aggregation and securitisation refer to the pooling of assets and selling the cash flows to

investors to raise capital, generally via an asset-backed security or a bond. Viability gap funding refers to the practice of

providing grants or concessional short-term loans to projects that are economically beneficial but not financially viable.

Results-based financing refers to approaches where payments are made, usually by governments, donors or development

finance institutions (DFIs) to the private sector, on the achievement of predefined results.

Source: IEA (2023), Financing Clean Energy in Africa

.

The primary hurdle to attracting finance for expanding energy access is

affordability, especially in rural areas. As a result, government affordability support

and concessional financing are essential if all households are to gain access by

2030. It is estimated that due to affordability constraints, only around half of the

new electricity access connections providing the most basic energy services

3

in

the SAS are likely to be commercially viable without incentives such as reduced

connection charges, lower tariffs and subsidised electrical appliances. The

situation is similar for clean cooking access projects where the upfront cost of

stoves and the cost of fuels, such as electricity, LPG and charcoal, undermine

adoption. For example, LPG is one of the key solutions to closing the access gap,

3

The basic bundle includes more than one light point providing task lighting, phone charging and a radio. For further

information on these definitions see Guidebook for Improved Electricity Access Statistics

.

Clean energy investment for development in Africa Chapter 2: Access to modern energy services

PAGE | 24

IEA. CC BY 4.0.

yet only one-fifth of the population without access could afford to switch to LPG at

current tariffs if they were given access to affordable credit to purchase the LPG

stove and cylinder. Excluding current affordability support, only 5% of those

without access today could afford LPG cooking.

Making electricity affordable requires a combination of well-targeted government

incentives covering grid and off-grid solutions (potentially involving cross-

subsidisation), de-risking instruments such as grants, existence of productive uses

as anchor loads and tariff reforms. Traditionally, many African countries have

subsidised domestic energy by setting prices at below-market levels, but this has

often led to electricity utilities and other energy companies – usually state-owned

enterprises (SOEs) – failing to recover their costs, resulting in rising debt, falling

investment and an inability to expand new connections fast enough. Making clean

cooking affordable on the other hand typically requires the upfront costs of

acquiring the equipment to be subsidised. Solutions based on “PayGo” models

,

where families pay as they use gas, or models based on smaller gas cylinders that

reduce the cost of each refill, have proven successful in some markets, including

Kenya and South Africa, but usually need to go together with subsidised prices.

Adequately funded national access programmes, involving transparent subsidy

mechanisms, are an important prerequisite. Currently, only 41% of the people

without access to electricity in Africa and 55% of those without access to clean

cooking are in countries with programmes that provide affordability assistance to

consumers for access. Developing integrated energy strategies is a fundamental

building block to attract supporting investment by providing greater certainty to

investors.

Governments also have a major role to play in funding access projects. Grid

extensions are generally the responsibility of SOEs, so are indirectly publicly

funded. This is expected to remain the case in the medium term: roughly four-fifths

of grid investments are carried out by public utilities in 2030 in the SAS (see

Chapter 3). Private sector financing is set to take on a larger role, though this is

likely to be limited to countries that have relatively well-developed power systems

and a stable regulatory environment. It also requires governments to make private

involvement legally viable by authorising the use of concessional agreements or

other regulatory carve‐outs for private sector investment and ownership, and as a

matter of best practice should be accompanied by auctions and competitive

tenders.

Some successful grid extension programmes have combined central government

and local community financing, ensuring local engagement. For example, in 2020,

Ghana introduced the Self-Help Electrification Scheme

, which allowed

communities to be connected to the grid earlier if they could provide poles for low-

voltage lines and guarantee that at least 30% of the households in the community

Clean energy investment for development in Africa Chapter 2: Access to modern energy services

PAGE | 25

IEA. CC BY 4.0.

were ready to start using the electricity provided. Some countries, such as

Côte d’Ivoire, have implemented the option of on-bill repayment of connection

costs, reducing the upfront burden and permitting many households to connect to

the grid legally.

Mini-grid projects also typically depend on public sector assistance to support the

relatively high upfront costs and to ensure a tariff structure that is both cost-

reflective and sensitive to what end users can afford. When it comes to stand-

alone systems providing electricity, their inherent small scale often poses a barrier

to finance. Traditional channels of energy financing are not well adapted to support

these smaller, higher-risk projects, or to finance small and medium-sized

enterprises and local start-ups. These companies often struggle to access DFI

capital or other international sources of finance and, therefore, rely more on local

commercial banks. As a result, many of them operate as retail businesses, which

can attract more private capital but need to focus on the most profitable projects.

There will need to be an increase in patient equity and affordable local currency

debt, as well as an emphasis on early-stage financing, to support the development

of bankable projects. An alternative approach would be an

energy-as-a-service

model via public-private partnership, whereby the government leverages DFI

capital to buy the solar home systems from a private developer, and the

households pay affordable tariffs for the use of energy (and providing for

equipment maintenance) under a long-term contract.

In view of the constraints on public spending and the difficulties facing SOEs,

especially electricity utilities, international concessional capital from DFIs and

private donors will need to continue to play a critical role in de-risking access

projects and leveraging private sector finance, especially for projects aimed at the

poorest households in the most remote regions that would otherwise struggle to

attract investment. Concessional financing needs to be focused on projects where

their presence can crowd in commercial financing. In the case of clean cooking

projects, the share of private capital in international financial flows to Africa has

been growing in recent years, in part thanks to the leveraging effect of

concessional capital from DFIs and growing funds from carbon markets.

Given the limited availability of concessional finance and the large amounts of

capital needed to expand access projects, it is vital that concessional funds from

DFIs and philanthropies are used in such a way as to mobilise the maximum

amount of private capital by improving the risk-return profile of projects and

lowering the cost of capital. A number of so-called blended finance instruments

can be used to stimulate private investment in access projects, including

guarantees or other risk-sharing and liquidity support to mitigate risks, or providing

grants to support project preparation and project structuring (see Chapter 5).

Clean energy investment for development in Africa Chapter 3: The electricity sector

PAGE | 26

IEA. CC BY 4.0.

Chapter 3. The electricity sector

Key targets and investment needs

The electricity sector lies at the heart of the energy transition and is central to

achieving universal access to modern energy services. In many African countries

today, the sector is suffering from years of under-investment and poor operational

and financial performance, including large network losses, low collection rates,

widespread under-recovery of costs and unmet demand. Major reforms and new

sources of finance will be needed to bring about a step increase in investment in

generating capacity, transmission and distribution.

Ensuring universal access to reliable electricity for all households, schools,

hospitals, companies and businesses, together with an underlying shift towards

the electrification of energy end uses, means electricity becomes the fastest-

growing component of final demand in Africa in the Sustainable Africa Scenario

(SAS). Electricity demand surges by around 60% this decade from a little over

700 TWh in 2022 to more than 1 160 TWh in 2030, driven by both households

gaining access and greater use of electricity in industry and other productive uses.

The majority of this increase in demand is met by increased generation from

renewables – primarily hydropower (160 TWh to 312 TWh in 2022-30), solar PV

(16 TWh to 215 TWh) and wind (25 TWh to 156 TWh). This shift towards

renewables is driven by falling costs and policies promoting low-emissions energy,

capitalising on Africa's abundant resources. By 2030, solar PV and wind combined

contribute 38% to total power generation – eight times more than in 2022.

Installed power generation capacity in Africa doubles in the SAS, from 278 GW in

2022 to 510 GW in 2030, with a profound shift in the type of power plants built

across the continent. Renewables account for 80% of the generating capacity

additions. Solar PV leads the way, with 120 GW of capacity added between 2022

and 2030 – over 40% of the total increase in capacity. It overtakes hydropower

before 2030 and approaches natural gas as the largest source of power

generation capacity (Figure 3.1). Wind power capacity also expands rapidly,

especially in North and East Africa, where resources are located close to demand

centres. Hydropower also remains a cornerstone, with several large‐scale projects

currently under development to provide affordable and dispatchable electricity.

Natural gas-fired capacity continues to grow, but more slowly than in recent years.

The relative stability of the oil-fired plant fleet hides different regional dynamics,

with an increase in capacity related to expanded access in sub‐Saharan Africa

offset by a decline in North Africa.

Clean energy investment for development in Africa Chapter 3: The electricity sector

PAGE | 27

IEA. CC BY 4.0.

Figure 3.1 Installed power generation capacity in Africa by source in the Sustainable

Africa Scenario, 2010-2030

IEA. CC BY 4.0.

Solar PV, hydropower and wind capacity surpass that of coal and oil this decade, while

the dominant position of natural gas is overturned in the 2030s

Source: IEA (2022), Africa Energy Outlook 2022.

The rapid growth in the share of intermittent renewables has implications for the

operation of power systems, which must be managed in conjunction with efforts

to shore up electricity reliability. A range of assets and measures are developed

to improve reliability and improve system flexibility in the SAS from now to 2030,

including hydropower facilities (including pumped storage), gas-fired power plants,

geothermal plants and energy storage. Improvements in grid operation in terms of

scheduling and dispatch are also needed to make the most of these dispatchable

resources. Battery storage deployment remains modest to 2030, but accelerates

quickly thereafter, mainly to provide short‐duration flexibility and provide stable

power supply in both on-grid and off-grid applications.

Electricity sector investment accounts for around half of all energy investment by

2030 in the SAS (Figure 3.2). Total electricity sector investment rises from an

estimated USD 30 billion in 2022 to USD 120 billion in 2030, with renewables

accounting for over half of this amount. Solar PV accounts for the bulk of this

investment.

30

60

90

120

150

2010 2015 2020 2025 2030

GW

Natural gas

Solar PV

Hydro

Wind

Coal

Oil

Other renewables

Bioenergy

Nuclear

Clean energy investment for development in Africa Chapter 3: The electricity sector

PAGE | 28

IEA. CC BY 4.0.

Figure 3.2 Electricity sector investment by sector in Africa in the Sustainable Africa

Scenario, 2022-2030

IEA. CC BY 4.0.

Reaching the continent's Sustainable Development Goals, including energy access and

climate targets, will require nearly a fivefold increase in electricity sector investment by

2030. This increase is driven mainly by clean energy and infrastructure

Note: STEPS = Stated Policies Scenario; SAS = Sustainable Africa Scenario. Grid investment excludes that related to

extending electricity access.

Supporting these capacity additions requires large-scale investments in grid

infrastructure, not just to expand networks to meet the needs of newly connected

customers and rising demand from existing ones, but also to upgrade them to

provide adequate flexibility, support the integration of digital technologies to

improve real-time awareness of the situation on the grid and improve the ability

for dispatchers to operate the grid. The achievement of universal access to

electricity by 2030 is a significant driver of electricity sector investment, accounting

for 13% of the total over 2023-2030, compared with barely 4% in 2019-2022.

Maintenance and modernisation of existing infrastructure

represents almost a

quarter of total capital spending on grids to 2030, helping to reduce network losses

in 2030 by 30% compared with 2022. The financial difficulties experienced by

many utilities over several years have hampered investment in new transmission

and distribution assets as well as the maintenance of existing ones, resulting in a

deterioration in operational performance, including increasing network losses.

Most utilities report losses of at least 10%, with an average of 15% across the

continent in 2020 – more than double the global average of 7%.

Financing vehicles and instruments

The way electricity sector investment in Africa is financed must evolve to support

the near-tripling of investment by 2030 and a shift towards renewables and

networks in the SAS. The types of financing instruments typically used for power

and network projects vary markedly according to the type of projects, the

technology involved, the maturity of the market and the project stage (Table 3.1).

50

100

150

2022 2030

Billion USD (2022)

Other

Grids and storage

Access

Fossil fuel generation

Renewables:

Wind

Hydro

Solar

Other Renewables

Clean energy investment for development in Africa Chapter 3: The electricity sector

PAGE | 29

IEA. CC BY 4.0.

For instance, solar PV and wind projects can benefit from technical assistance in

early development stages and concessional equity and debt during their

development, but once they are operational with a proven performance, they can

be refinanced on commercial capital. Arrangements for private investments are

also an important factor. Several models to facilitate private sector participation in

the power sector are in operation across the continent, including long-term

concessions; build, own, operate and transfer (BOOT) projects; merchant plants,

long-term power purchase agreements facilitated by auctions, and transmission

lines; and dedicated lines for independent power projects.

Table 3.1 Common financing instruments for power generation and networks by

technology and project stage

Technology Development Construction Operation

Solar PV/wind – nascent

market

Technical assistance

grants; seed grants

Concessional equity

Corporate cash flow

Concessional debt

Viability gap funding

Corporate equity (private

equity [PE]/venture

capital [VC])

Commercial debt

Aggregation;

securitisation

Solar PV/wind –

developed market

Corporate cash flow

Equity

Project finance

Commercial debt

Corporate equity

(PE/VC)

Commercial debt

Refinance via corporate

bond (if credit rating

allows; on local markets

ideally)

Geothermal and hydro

Technical assistance

grants in new markets,

such as resource

potential assessment

Equity

Funding from state-

owned enterprises

(SOEs)

Project finance

Concessional debt

Corporate equity

(PE/VC)

Commercial debt

Refinance via corporate

bond

Transmission and

distribution

Grants

Corporate cash flow

Concessional equity

Grants

Viability gap funding

Concessional debt and

equity

Corporate bond (if credit

rating allows; on local

markets ideally)

Notes: Equity can be concessional if it is provided in a subordinated or first-loss capacity, or if it has lower return expectations

or a longer time period to exit. Viability gap funding can take several forms but refers to the practice of providing grants or

concessional short-term loans to projects that are economically significant but not financially viable. Aggregation and

securitisation refer to the pooling of assets and selling the cash flows to investors to raise capital, generally via an asset-

backed security or a bond. Viability gap funding refers to the practice of providing grants or concessional short-term loans to

projects that are economically beneficial but not financially viable.

Source: IEA (2023), Financing Clean Energy in Africa

.

Utility-scale renewable power projects

Utility-scale renewable power projects, especially in less mature markets, are

often hard to finance due to higher risks in the development and construction

phases. This means that higher levels of equity financing, as well as public

spending and/or concessional support from development finance institutions

(DFIs), are needed. Geothermal and hydropower projects, which have more

specific geological and hydrological requirements for their successful

development, have an additional risk phase during the exploration and scoping

Clean energy investment for development in Africa Chapter 3: The electricity sector

PAGE | 30

IEA. CC BY 4.0.

that is greater than that required for wind and solar. Hydropower projects also

require long due diligence, permitting and environmental licensing procedures.

This can present a major hurdle, particularly for large projects such as the

proposed Grand Inga Dam project in the Democratic Republic of the Congo,

which

has been stalled for years due to its large scale (40 GW) and the associated need

for both transmission works and cross-border agreements, as well as ongoing

discussions regarding its potential environmental impact.

Many African countries still rely on concessional support for the development of

their large renewable projects. As a result of the limited availability of concessional

finance, investment in such projects has so far been concentrated in countries with

access to commercial capital due to their broader access to finance (Figure 3.3).

There is a need to increase the amount of funding to lower-income countries,

accompanied by support to strengthen the regulatory environment and build

institutional and technical capacity within these countries. There are signs of

progress here; for example, lower-income countries are seeing a shift from

licensed schemes to competitive bidding, which accounted for 20% of renewables

projects in 2017-2018, rising to 90% in 2019-2021. Programmes such as the

African Development Bank (AfDB) Desert to Power Initiative

, which began working

with five countries in the Sahel and is now entering a second phase in East Africa,

demonstrate the value of a co-ordinated approach that includes working with

governments on national sector roadmaps, as well as supporting individual

projects through viability gap funding.

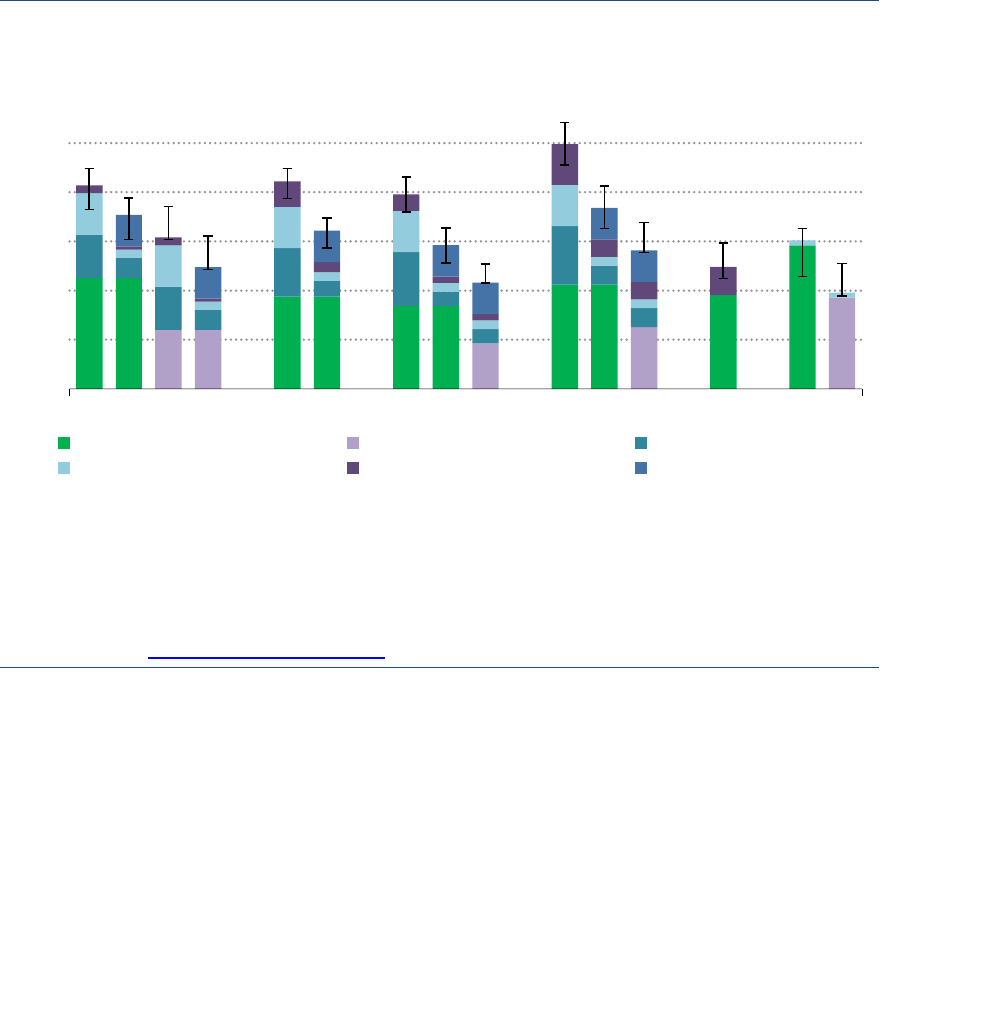

Figure 3.3 Clean power project financing by ability to access commercial capital in

Africa, 2017-2022

IEA. CC BY 4.0.

Renewable power investments are concentrated in larger economies with greater access

to commercial capital, with poorer countries forced to rely on limited concessional

capital finance

Note: MER = market exchange rate; PV = photovoltaics.

Sources: IEA analysis based on IJ Global and WB PPI.

10

20

30

40

5

10

15

20

2017-

2018

2019-

2020

2021-

2022

2017-

2018

2019-

2020

2021-

2022

Hydropower

Grids and

storage

Wind

Solar PV

Renewables

capacity

(right axis)

Billion USD (2022, MER)

Countries reliant on

concessional capital

Countries with access to

commerical finance

GW

Clean energy investment for development in Africa Chapter 3: The electricity sector

PAGE | 31

IEA. CC BY 4.0.

In more developed African countries, especially those with strong renewables-

related regulations and existing projects, a major barrier to their widespread

adoption is concern over non-payment of offtake agreements (electricity supply

contracts). Aside from cultivating a reliable, paying customer base to buy this

energy, other measures can help overcome this risk. These include measures that

ensure utilities are not over-contracted for energy that will not get used, such as

the creation of realistic integrated resource plans with clear capacity targets by

technology type. It can also be improved through contract structures that assume

some of the offtake risk, which includes introducing independent power producer