For use at 10:00 a.m., EDT

Wednesday

July 18, 2007

Board of Governors of the Federal Reserve System

Monetary Policy Report to the Congress

July 18, 2007

Board of Governors of the Federal Reserve System

Monetary Policy Report to the Congress

Submitted pursuant to section 2B of the Federal Reserve Act

July 18, 2007

Letter of Transmittal

BOARD OF GOVERNORS OF THE

FEDERAL RESERVE SYSTEM

Washington, D.C., July 18, 2007

THE PRESIDENT OF THE SENATE

THE SPEAKER OF THE HOUSE OF REPRESENTATIVES

The Board of Governors is pleased to submit its Monetary Policy Report to the Congress

pursuant to section 2B of the Federal Reserve Act.

Sincerely,

Ben Bernanke, Chairman

Contents

Page

Monetary Policy and the Economic Outlook 1

Economic and Financial Developments in 2007 4

Board of Governors of the Federal Reserve System 1

Monetary Policy Report to the Congress

Report submitted to the Congress on July 18, 2007,

pursuant to section 2B of the Federal Reserve Act

MONETARY POLICY AND THE ECONOMIC OUTLOOK

The U.S. economy generally performed well in the fi rst

half of 2007. Activity continued to increase moderately,

on average, over the period; businesses added jobs at

a steady pace; and the unemployment rate remained at

4½ percent. Overall infl ation, however, picked up as a

result of sizable increases in energy and food prices. At

the same time, core infl ation (which excludes the direct

effects of movements in energy and food prices) held at

about the same rate as in 2006; this measure smoothes

through some of the volatility in the high-frequency data

and thus is generally a better gauge of underlying infl a-

tion trends.

Although real gross domestic product appears to have

expanded at about the same average rate thus far this year

as it did in the second half of 2006, the pace of expansion

has been uneven. In the fi rst quarter, consumer expen-

ditures and business fi xed investment, taken together,

posted a solid gain. However, homebuilding continued to

contract, and manufacturing fi rms adjusted production to

address stock imbalances in that sector that had emerged

over the course of 2006. In the second quarter, housing

activity declined further in response to the continued

softness in home sales and still-elevated inventories of

unsold new homes; personal consumption expenditures

(PCE) also slowed. Even so, the available data point to

solid gains overall in other components of fi nal sales, and

with manufacturing inventory imbalances signifi cantly

reduced, growth in real GDP apparently sped up.

Job growth in the fi rst half of 2007 was driven by

sizable increases in service-producing industries. In the

goods-producing sector, manufacturing employment con-

tracted, especially at fi rms closely tied to the construction

industry and at producers of motor vehicles and parts.

Employment in residential construction, which had turned

down in mid-2006, decreased only modestly further over

the fi rst half of 2007 despite the substantial decline in

homebuilding.

Real hourly compensation increased over the year end-

ing in the fi rst quarter, the most recent period for which

complete data are available. In the second quarter, howev-

er, gains in real compensation were probably curtailed by a

steep, energy-driven rise in consumer prices. Employment

continued to rise apace in the fi rst half of 2007 in the face

of moderate growth in output. As a consequence, growth

in labor productivity—which had slowed in 2006 from the

rapid rate observed earlier in the decade—appears to have

remained modest. The cooling of productivity growth in

recent quarters likely refl ects cyclical or other temporary

factors, but the underlying pace of productivity gains may

also have slowed somewhat.

Financial market conditions have continued to be

generally supportive of economic expansion thus far

in 2007, though there was a notable repricing in the

subprime-mortgage sector. In recent weeks, the deterio-

ration in that sector has been particularly marked, and

markets for lower-quality corporate credits have also

experienced some strains. Nonetheless, spreads on such

corporate credits have remained narrow on the whole,

and business borrowing has continued to be fairly brisk.

On balance, equity markets posted sizable gains through

mid-July, in part because of continued robust corporate

profi ts and an upward revision to investors’ outlook for the

economy. The improved outlook led market participants

to mark up their anticipated path for the federal funds

rate, and intermediate- and long-term interest rates rose

signifi cantly. The foreign exchange value of the dollar has

declined moderately this year as the pace of economic

activity abroad has strengthened.

Overall consumer price infl ation, as measured by the

PCE price index, picked up noticeably in the fi rst half

of 2007, largely because of a sharp increase in energy

prices. After moving down over the second half of 2006,

the prices households pay for energy subsequently turned

up and by May were 14 percent (not at an annual rate)

above their level at the end of last year. Food prices also

contributed to the step-up in overall infl ation this year.

The faster rate of increase in overall prices has had only

a modest effect on infl ation expectations: Surveys suggest

that near-term infl ation expectations have risen somewhat

in recent months, but measures of long-term infl ation

expectations have remained within the range of recent

years.

The rate of increase in the core PCE price index ticked

down from 2.1 percent over the twelve months of 2006 to

an annual rate of 2.0 percent over the fi rst fi ve months of

2007, primarily accounted for by more-favorable readings

between March and May. Although higher energy prices

this year added to the cost of producing a wide variety

2 Monetary Policy Report to the Congress July 2007

of goods and services that are included in the core index,

these effects were offset by other factors—most notably,

a slowdown in the rate of increase in shelter costs from

the very high rates seen in 2006.

The U.S. economy seems likely to continue to expand

at a moderate pace in the second half of 2007 and in 2008.

The current contraction in residential construction will

likely restrain overall activity for a while longer, but as

stocks of unsold new homes are brought down to more

comfortable levels, that restraint should begin to abate.

In addition, the inventory correction that damped activity

in the manufacturing sector around the turn of the year

appears largely to have run its course. Thus, stock adjust-

ment is unlikely to be a drag on production in coming

quarters. Consumer spending should also keep moving up.

Employment and real wages are on track to rise further,

and, although the diffi culties in the subprime-mortgage

market have created severe fi nancial problems for some

individuals and families, the household sector is in good

fi nancial shape overall. Businesses are also continuing to

enjoy favorable fi nancial conditions, which, along with

a further expansion in business output, should support

moderate increases in business investment. The positive

outlook for economic activity abroad bodes well for U.S.

exports.

Core infl ation is expected to moderate a bit further over

the next year and a half. Longer-run infl ation expectations

are contained, pressures on resource utilization should

ease slightly in an environment of economic expan-

sion at or just below the rate of increase in the nation’s

potential to produce, and some of the other factors that

boosted infl ation in recent years have already receded

or seem likely to do so. As noted, increases in shelter

costs, which helped push up core infl ation in 2006, have

slowed appreciably this year. In addition, the paths for

the prices of energy and other commodities embedded in

futures markets suggest that the impetus to core infl ation

from these infl uences should diminish. And although unit

labor costs in the nonfarm business sector have been ris-

ing, the average markup of prices over unit labor costs is

still high by historical standards, an indication that fi rms

could potentially absorb higher costs, at least for a time,

through a narrowing of profi t margins.

Nonetheless, the possibility that the expected modera-

tion in infl ation will fail to materialize remains the pre-

dominant risk to the economic outlook. The more-favor-

able readings on core infl ation in recent months partly

refl ect some factors that seem likely to prove transitory.

Moreover, the economy appears to be operating at a high

level of resource utilization, which has the potential to sus-

tain infl ation pressures. In addition, an upward impetus to

costs could emanate from other sources, including higher

prices for energy and other commodities or a slower rate of

increase in structural productivity. Another concern is that

high rates of headline infl ation, if prolonged, could cause

longer-run infl ation expectations to rise and could thus

become another factor sustaining infl ation pressures.

Significant risks also attend the outlook for real

economic activity. On the downside, the fall in housing

construction could intensify or last longer than expected.

In addition, persistent weakness in the housing sector

could spill over to other sectors, especially consump-

tion. But upside risks also exist. For example, consumer

spending appears to be rising less rapidly of late after a

period of large increases that pushed the personal saving

rate into negative territory; increases in consumption

could return to their earlier pace. Exports could also

boost aggregate demand more than anticipated, espe-

cially if economic conditions abroad continue to exceed

expectations.

The Conduct of Monetary Policy

over the First Half of 2007

The Federal Open Market Committee (FOMC) left the

stance of monetary policy unchanged over the fi rst half

of 2007. At the time of the January meeting, available

economic information pointed to a relatively favorable

outlook for both economic growth and infl ation. While

manufacturing activity had softened, the housing sector

had shown tentative signs of stabilizing, and consumer

spending remained strong. Readings on core infl ation had

improved some from the elevated levels reached in 2006,

and infl ation expectations continued to be stable. Never-

theless, the prevailing level of infl ation was uncomfortably

high, and elevated resource utilization had the potential

to sustain infl ation pressures. Against this backdrop, the

Committee decided to leave its target for the federal funds

rate unchanged at 5¼ percent and reiterated in its policy

statement that some infl ation risks remained. The Com-

mittee also explained that the extent and timing of any

additional fi rming would depend on the evolution of the

outlook for both infl ation and economic growth as implied

by incoming information.

When the Committee met in March, data suggested

that the ongoing weakness in the housing market had not

spilled over to consumption spending, and the strains in

the subprime-mortgage market did not appear to be affect-

ing the availability of other types of household or busi-

ness credit. Although investment spending had been soft,

it was expected to pick up, primarily because of strong

corporate balance sheets, continued high profi tability, and

generally favorable fi nancial conditions. Nevertheless,

sluggish business spending and the deterioration in the

subprime-mortgage market suggested that downside risks

to growth had increased. At the same time, readings on

core infl ation had stayed somewhat elevated, and increases

Board of Governors of the Federal Reserve System 3

in the prices of energy and non-energy commodities had

boosted the risk that the expected deceleration in infl ation

would fail to occur. The FOMC decided to leave its target

for the federal funds rate unchanged at 5¼ percent and

noted in the accompanying statement that its predominant

policy concern remained the risk that infl ation would

fail to moderate as expected. In light of the increased

uncertainty about the outlook for both inflation and

growth, the statement indicated that future policy adjust-

ments would depend on the evolution of the outlook

for both infl ation and economic growth as implied by

incoming information—a characterization that has been

repeated in the two postmeeting FOMC statements since

then.

In May, the data in hand indicated that the adjust-

ment in the housing sector was continuing and appeared

likely to persist for longer than previously anticipated.

Moreover, growth in consumer spending seemed to have

slowed in the early spring. Nonetheless, because the prob-

lems in the subprime-mortgage market apparently were

contained and business spending indicators suggested

improving prospects for investment, the economy seemed

likely to expand at a moderate pace over coming quarters.

Despite more-favorable readings for March, core infl ation

remained somewhat elevated from a longer perspective.

Infl ation pressures were expected to moderate over time,

but the high level of resource utilization had the potential

to sustain those pressures. As a result, the FOMC decided

to leave its target for the federal funds rate unchanged at

5¼ percent and repeated in the statement that its predomi-

nant policy concern remained the risk that infl ation would

fail to moderate as expected.

At the June meeting, data appeared to confi rm that

economic growth had strengthened in the second quarter

of 2007 despite the ongoing adjustment in the housing

sector. Business spending on capital equipment, which

had faltered around the turn of the year, fi rmed somewhat

in the spring, and nonresidential construction advanced

briskly. In addition, the inventory correction that had held

down economic activity late last year and early this year

seemed to have mostly run its course. Moreover, defense

spending and net exports appeared poised to rebound

after sagging in the fi rst quarter. These factors more than

offset a slowdown in the growth of consumer spending.

Readings on core infl ation remained favorable in April

and May. Nonetheless, a sustained moderation of infl ation

pressures had yet to be convincingly demonstrated, and

the high level of resource utilization had the potential to

sustain those pressures. Under these circumstances, the

Committee decided to leave its target for the federal funds

rate unchanged at 5¼ percent. In its policy statement, the

Committee repeated that its predominant policy concern

remained the risk that infl ation would fail to moderate as

expected.

At their meetings over the fi rst half of 2007, FOMC

meeting participants continued the discussions they had

formally initiated last year regarding their communica-

tions with the public. The discussions included a review

of the role of the economic projections that are made

twice a year by the members of the Board of Governors

and the Reserve Bank presidents and which are included

in the Board’s Monetary Policy Report to the Congress.

In addition, participants exchanged views on the possible

advantages and disadvantages of specifying a numerical

price objective for monetary policy. They also discussed

the appropriate role of meeting minutes and policy state-

ments. These discussions remain ongoing, as participants

continue to evaluate the best available means for improv-

1

2

3

4

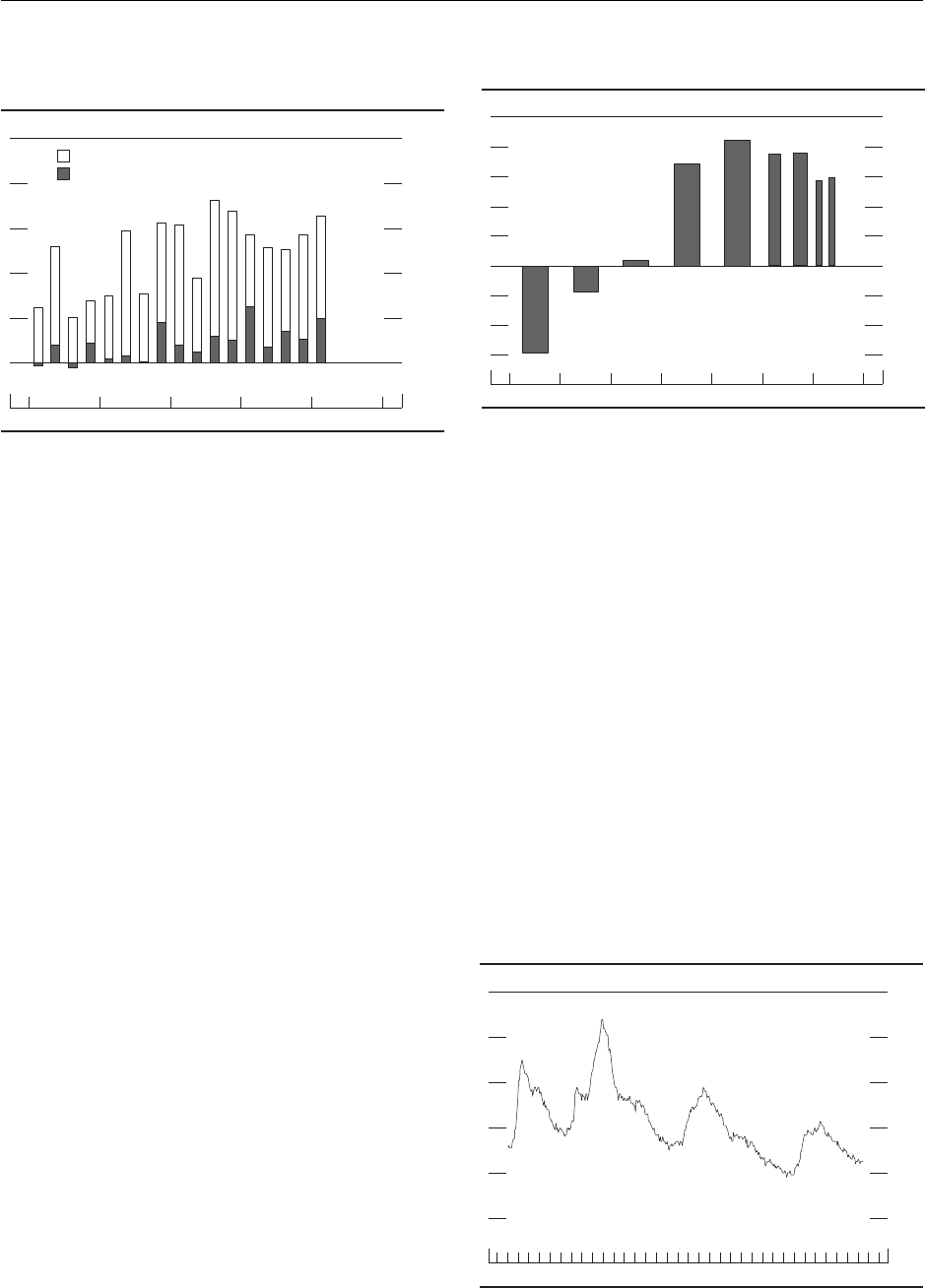

5

Percent

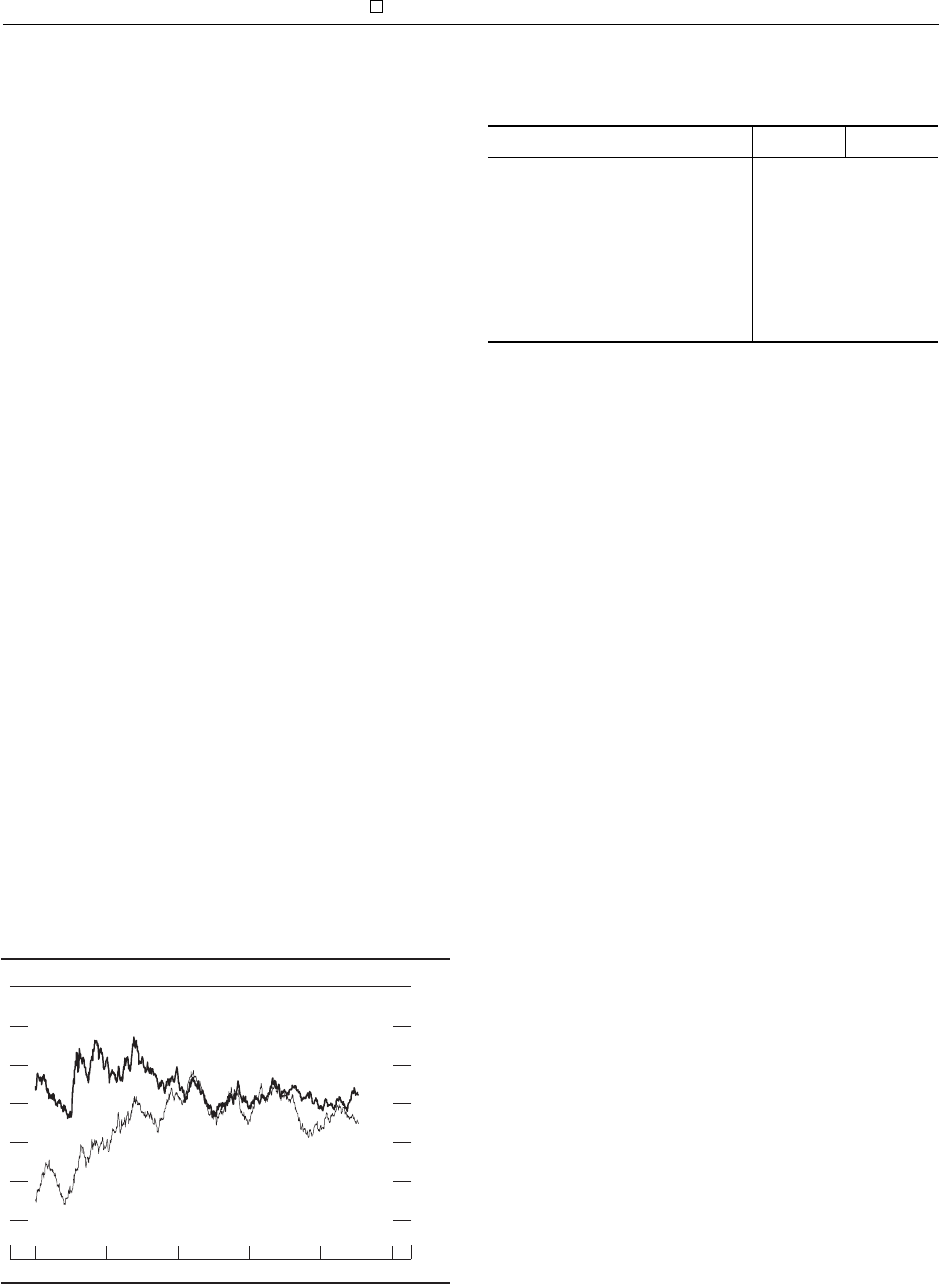

1/28 3/16 5/4 6/30 8/10 9/21 11/10 12/14 2/2 3/22 5/3 6/30 8/9 9/20 11/1 12/13 1/31 3/28 5/10 6/29 8/8 9/20 10/25 12/12 1/31 3/21 5/9 6/28

2007200620052004

Selected interest rates, 2004–07

Target federal funds rate

Ten-year Treasury rate

N

OTE

: The data are daily and extend through July 13, 2007. The ten-year Treasury rate is the constant-maturity yield based on the most actively traded

securities. The dates on the horizontal axis are those of FOMC meetings.

S

OURCE

: Department of the Treasury and the Federal Reserve.

4 Monetary Policy Report to the Congress July 2007

ing communication with the public in furtherance of the

Committee’s dual mandate for both maximum employ-

ment and stable prices.

Economic Projections for 2007 and 2008

In conjunction with the FOMC meeting at the end of June,

the members of the Board of Governors and the Reserve

Bank presidents, all of whom participate in the delibera-

tions of the FOMC, provided economic projections for

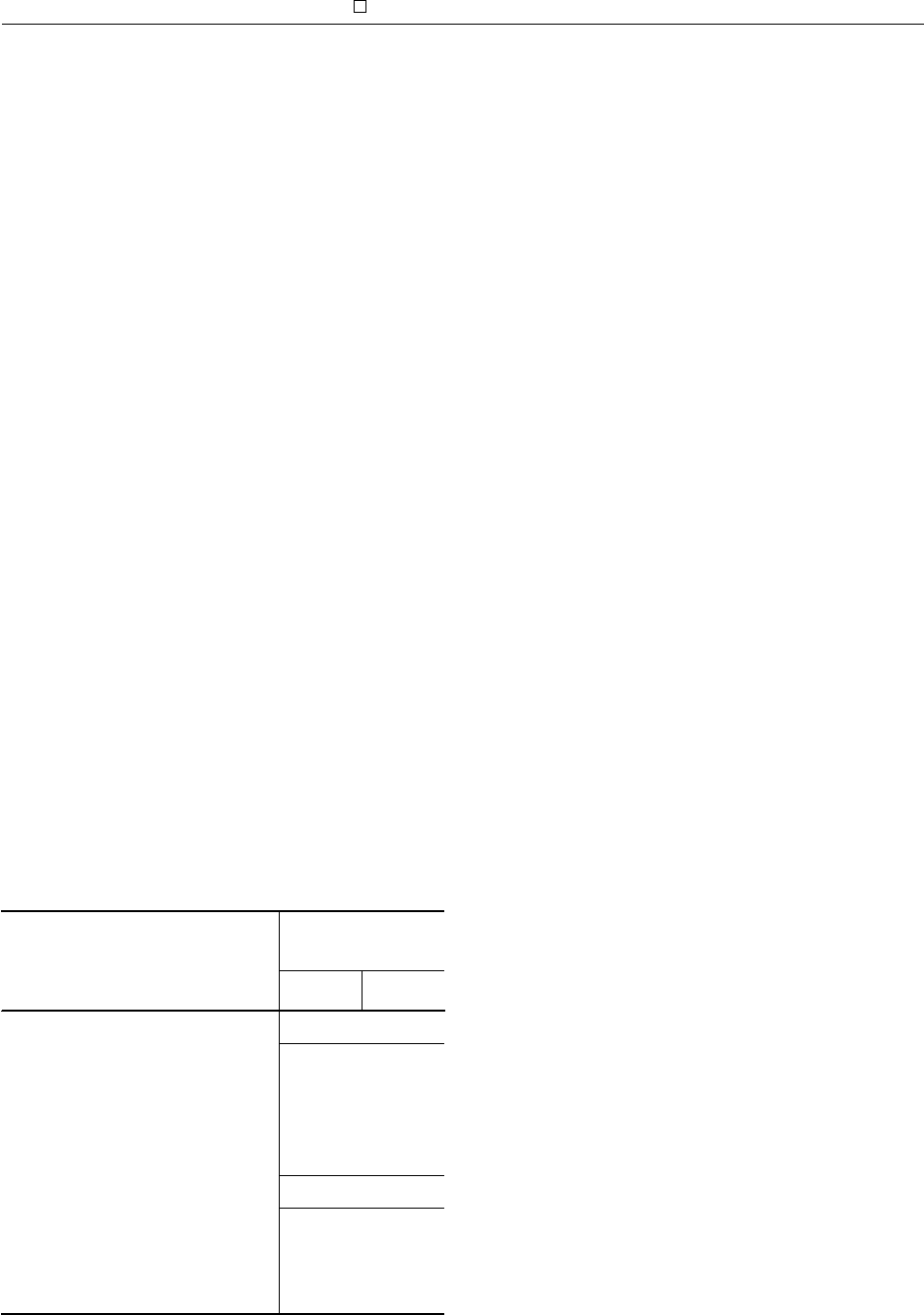

2007 and 2008 for this report. The central tendency of

the FOMC participants’ forecasts for the increase in real

GDP is 2¼ percent to 2½ percent over the four quarters of

2007 and 2½ percent to 2¾ percent in 2008. The civilian

unemployment rate is expected to lie between 4½ percent

and 4¾ percent in the fourth quarter of 2007 and to be

at about the top of that range in 2008. As for infl ation,

FOMC participants expect that the increase in the price

index for personal consumption expenditures excluding

food and energy (core PCE infl ation) will total 2 percent

to 2¼ percent over the four quarters of 2007 and will drift

down to 1¾ percent to 2 percent in 2008.

Economic activity appears poised to expand at a

moderate rate in the second half of 2007, and it should

strengthen gradually into 2008. The ongoing correction in

the housing market seems likely to continue to weigh on

the rate of economic expansion over the near term. But as

that process runs its course, the rate of growth of economic

activity should move up somewhat. The pace of consumer

spending may be restrained in the near term as households

continue to adjust to the latest run-up in energy prices and

to softer house prices; still, household balance sheets are

generally in good shape, and increases in employment

and real wages over the next year and a half should be

suffi cient to sustain further gains in spending. Regarding

business investment, solid gains in real outlays on equip-

ment and software seem likely in light of the anticipated

expansion in business output, continuing strong profi ts,

and generally favorable fi nancial conditions. Opportuni-

ties to realize signifi cant gains in effi ciency by investing

in high-tech equipment should provide ongoing support to

equipment spending as well. Investment in nonresidential

buildings also seems to be expanding briskly. In addition,

prospects are favorable for continued increases in demand

for exports of U.S. goods and services.

FOMC participants generally expect core infl ation to

edge down a bit further over the next year and a half. In

assessing the apparent slowing of core infl ation this spring,

participants recognized that the monthly price data are

volatile and that some of the recent improvement may

prove to have been transitory. Nonetheless, they believe

that the current environment will be conducive to some

further moderation in underlying price pressures. The

participants’ forecasts for real activity imply a slight

easing over the next several quarters of the tightness in

labor and product markets. And although core infl ation

is expected to remain under some upward pressure in the

near term from the pass-through of the increases to date

in the prices of energy and other commodities, those cost

pressures should subsequently wane. Accordingly, with

long-run infl ation expectations contained, diminished

cost pressures should result in some moderation in core

infl ation.

ECONOMIC AND FINANCIAL DEVELOPMENTS

IN 2007

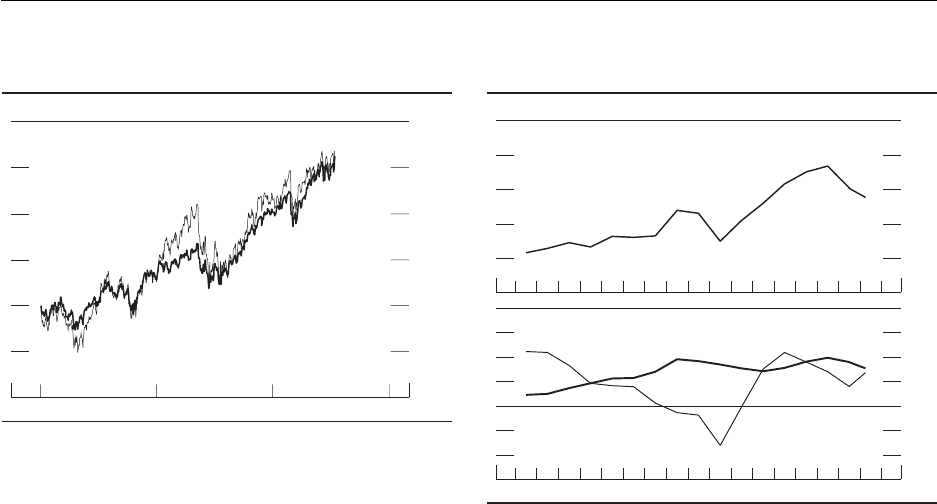

Real GDP increased at an annual rate of 2¼ percent in

the second half of 2006, and it appears to have risen at

roughly that pace, on average, over the fi rst half of 2007.

Although consumer spending and business fi xed invest-

ment posted moderate gains, on balance, during the fi rst

half, the contraction in residential construction exerted

signifi cant restraint on economic activity. The rise in real

GDP in the fi rst quarter was also damped by a downswing

in inventory investment, a dip in defense spending, and an

unusually sharp drop in net exports. The available infor-

mation suggests that GDP growth rebounded in the second

quarter as the drag from inventory investment waned and

as defense expenditures and net exports snapped back

after their fi rst-quarter declines. In the labor market, hir-

ing continued at a steady pace throughout the fi rst half,

Economic projections for 2007 and 2008

Percent

Change, fourth quarter to fourth quarter

1

Nominal GDP ......................................................... 4½ –5½ 4½ – 5

Real GDP ............................................................... 2 –2¾ 2¼ – 2½

PCE price index excluding food and energy .......... 2 – 2¼ 2 – 2¼

Average level, fourth quarter

Civilian unemployment rate ................................... 4½ – 4¾ 4½ – 4¾

Change, fourth quarter to fourth quarter

1

Nominal GDP ......................................................... 4½ – 5½ 4¾ – 5

Real GDP ............................................................... 2½ – 3 2½ – 2¾

PCE price index excluding food and energy .......... 1¾ – 2 1¾ – 2

Average level, fourth quarter

Civilian unemployment rate ................................... 4½ – 5 About 4¾

1. Change from average for fourth quarter of previous year to average for

fourth quarter of year indicated.

Federal Reserve Governors

and

Reserve Bank presidents

Indicator

Range

Central

tendency

2007

2008

Board of Governors of the Federal Reserve System 5

although job gains fell short of those recorded in 2006, and

the unemployment rate remained at 4½ percent. Headline

consumer price infl ation was boosted by a reversal of the

downturn in energy prices in late 2006 and a step-up in

retail food prices, while core infl ation was little changed.

Real hourly labor compensation increased over the year

ending in the fi rst quarter, although gains in the second

quarter were probably eroded by the energy-driven pickup

in overall infl ation. Conditions in fi nancial markets have

remained generally supportive of economic expansion

thus far this year despite deteriorating conditions in the

subprime-mortgage sector. Investors seemed to become

more optimistic about the outlook for the economy: Inter-

est rates rose, credit spreads on corporate bonds stayed

narrow on the whole, and equity markets recorded sizable

gains.

The Household Sector

Consumer Spending

After exhibiting considerable vigor in late 2006, consumer

spending slowed somewhat over the fi rst half of 2007.

Spending continued to be bolstered by the strong labor

market and the lagged effects of earlier increases in house-

hold wealth. However, these positive infl uences were

partly offset by the rise in energy prices this year, which

drained consumers’ purchasing power, and by reduced

home-price appreciation, which limited recent gains in

1

2

3

4

5

Percent, annual rate

2007200620052004200320022001

Change in real GDP, 2001–07

Q1

NOTE: Here and in subsequent figures, except as noted, change for a given

period is measured to its final quarter from the final quarter of the preceding

period.

SOURCE: Department of Commerce, Bureau of Economic Analysis.

1

2

3

4

Percent, annual rate

2007200620052004200320022001

Change in PCE chain-type price index, 2001–07

NOTE: The data are for personal consumption expenditures (PCE).

Through 2006, change is from December to December; for 2007, change is

from December to May.

S

OURCE: Department of Commerce, Bureau of Economic Analysis.

Total

Excluding food and energy

2

4

6

Percent, annual rate

2007200620052004200320022001

Change in real income and consumption, 2001–07

Q1

SOURCE: Department of Commerce, Bureau of Economic Analysis.

Disposable personal income

Personal consumption expenditures

60

80

100

120

140

1966 = 100

60

80

100

120

140

2007200520032001199919971995

Consumer sentiment, 1994–2007

1985 = 100

Reuters/Michigan

Conference Board

N

OTE

: The Conference Board data are monthly and extend through June

2007. The Reuters/University of Michigan data are monthly and extend

through a preliminary estimate for July 2007.

S

OURCE

: The Conference Board and Reuters/University of Michigan Sur-

veys of Consumers.

6 Monetary Policy Report to the Congress July 2007

wealth for many households. Surveys of consumer senti-

ment have remained in a favorable range this year.

Real PCE rose at an annual rate of 4¼ percent in the

fi rst quarter. Spending on light motor vehicles (cars, sport-

utility vehicles, and pickup trucks) got off to a fast start

this year, expenditures on energy services were boosted by

unusually cold weather in February, and outlays for other

goods and services posted sizable gains after a steep run-

up in the fourth quarter. The available data imply a much

slower pace of spending growth in the second quarter, as

sales of light motor vehicles softened and real spending

on goods other than motor vehicles turned lackluster.

Real disposable personal income (DPI)—that is, after-

tax income adjusted for infl ation—also started the year on

a strong note after a large increase in the fourth quarter.

1

Wages and salaries and some other major categories of

personal income continued to rise appreciably in nominal

terms throughout the fi rst half. However, these gains were

eroded in real terms by the energy-related jump in infl ation

in the spring, and, as a result, real DPI rose at an annual

rate of just 1½ percent between the fourth quarter of 2006

and May 2007, compared with an increase of more than

3 percent over the four quarters of 2006.

Even given the sharp deceleration in residential real

estate values, household wealth has remained support-

ive of spending growth. One reason is that the surge

in equity values in recent quarters has allowed overall

household wealth to keep pace with nominal income

despite the softness in home prices. In addition, because

changes in net worth tend to infl uence consumption with

a lag of several quarters, the increases in wealth during

2005 and 2006 are likely still providing a good deal of

impetus to spending. These increases in wealth, which

have provided many households with the resources and

inclination to raise their spending at a rate that exceeds

income growth, have been a factor pushing down the

personal saving rate over the past couple of years even

as interest rates have moved up. After fl uctuating in the

vicinity of 2 percent from 1999 to 2004, the saving rate

subsequently dropped sharply, and it stood at negative

1¼ percent, on average, in April and May of 2007.

Residential Investment

Residential construction activity remained soft in the

fi rst half of 2007, as builders continued to confront weak

demand and an elevated inventory of unsold new homes.

In the single-family sector, new units were started at an

average annual rate of 1.18 million between January and

May—more than 30 percent below the quarterly high

reached in the fi rst quarter of 2006. Starts in the multifam-

ily sector averaged a little less than 300,000 units during

the fi rst fi ve months of 2007, an amount at the lower end of

the range of the past nine years. All told, the contraction in

housing activity subtracted nearly 1 percentage point from

the change in real GDP in the fi rst quarter of 2007—almost

as much as in the second half of 2006—and the drag likely

remained substantial in the second quarter.

1. According to the published data, real DPI rose at an annual

rate of 4¾ percent in the fi rst quarter. However, a substantial part of

the increase occurred because the Bureau of Economic Analysis (BEA)

added $50 billion (annual rate) to its estimate of fi rst-quarter wages and

salaries in response to information that bonus payments and stock option

exercises around the turn of the year were unusually large. Because the

BEA did not assume that these payments carried forward into April,

real DPI fell sharply in that month.

4

5

6

Ratio

200720031999199519911987

Wealth-to-income ratio, 1984–2007

NOTE: The data are quarterly and extend through 2007:Q1. The wealth-

to-income ratio is the ratio of household net worth to disposable personal

income.

S

OURCE: For net worth, Federal Reserve Board, flow of funds data; fo

r

income, Department of Commerce, Bureau of Economic Analysis.

+

_

0

3

6

9

12

Percent

200720031999199519911987

Personal saving rate, 1984–2007

N

OTE

: The data are quarterly and extend through 2007:Q2; the reading fo

r

2007:Q2 is the average for April and May.

S

OURCE

: Department of Commerce, Bureau of Economic Analysis.

Board of Governors of the Federal Reserve System 7

The monthly data on home sales have been erratic this

year. But after smoothing through the ups and downs, the

data suggest that demand has softened further after falling

at a double-digit rate between mid-2005 and mid-2006 and

then holding reasonably steady in the second half of last

year. On average, sales of existing homes over the three

months ending in May 2007 were 4½ percent below their

average level in the second half of last year, while sales of

new homes were down 10 percent over that period. The

further weakening of housing demand this year likely

refl ects, in part, tighter lending standards for mortgages,

and it occurred despite mortgage rates that were relatively

low by longer-run standards. The ongoing slippage in sales

has made it more diffi cult for homebuilders to make much

of a dent in their inventories of new homes for sale. When

evaluated relative to the three-month average pace of sales,

the months’ supply of unsold new homes in May was

more than 60 percent above the high end of the relatively

narrow range it occupied from 1997 to 2005. Moreover,

these published fi gures probably understate the true inven-

tory overhang in this sector to the extent that they do not

account for the surge in canceled sales in the past year;

such cancellations return homes to unsold inventory but

are not incorporated in the offi cial statistics.

The rate of house-price appreciation slowed dramati-

cally in 2006 after nearly a decade of rapid increases, and

prices appear to have moved roughly sideways in the fi rst

half of 2007. The purchase-only version of the repeat-

transactions price index for existing single-family homes

published by the Offi ce of Federal Housing Enterprise

Oversight, which tracks sales prices of the same houses

over time, rose at an annual rate of just 2 percent in the

fi rst quarter of 2007 (the latest available data) and was

up just 3 percent over the year ending in the fi rst quarter,

compared with an increase of 10 percent over the pre-

ceding year. For April and May combined, the average

price of existing single-family homes sold—which does

not control for changes in the mix of houses sold but is

available on a more timely basis—was about 1 percent

below that of a year earlier.

Household Finance

Household debt expanded at an annual rate of 6 percent

in the fi rst quarter of 2007, somewhat below the pace of

.4

.8

1.2

1.6

Millions of units, annual rate

2007200520032001199919971995

Private housing starts, 1994–2007

Single-family

Multifamily

N

OTE: The data are quarterly and extend through 2007:Q2; the readings fo

r

2007:Q2 are the averages for April and May.

S

OURCE: Department of Commerce, Bureau of the Census.

3

4

5

6

7

8

9

Percent

20072005200320011999

Mortgage rates, 1999–2007

Fixed rate

Adjustable rate

N

OTE

: The data, which are weekly and extend through July 11, 2007, are

contract rates on thirty-year mortgages.

S

OURCE

: Federal Home Loan Mortgage Corporation.

2

+

_

0

2

4

6

8

10

12

14

Percent

200720031999199519911987

Change in prices of existing single-family houses,

1984–2007

Average price

Repeat-transactions

index

N

OTE

: The data are quarterly, and changes are from one year earlier. The

repeat-transactions index extends through 2007:Q1. For the years preceding

1991, that index includes appraisals associated with mortgage refinancings;

beginning in 1991, it includes purchase transactions only. The data fo

r

average price extend through 2007:Q2, and the reading for Q2 is the average

for April and May compared with the same period one year earlier.

S

OURCE

: For repeat transactions, Office of Federal Housing Enterprise

Oversight; for average price, National Association of Realtors.

8 Monetary Policy Report to the Congress July 2007

8¾ percent posted in 2006. The deceleration was pri-

marily the result of a signifi cant step-down in the rise

of mortgage debt, which refl ected the sharp slowing of

house-price appreciation and the slower pace of home

sales. Consumer (nonmortgage) debt has remained on a

moderate uptrend this year.

Debt rose a little more slowly than personal income in

the fi rst quarter, so the fi nancial obligations ratio for the

household sector inched down, though it remained only a

bit below its historical high. Most households were able

to meet their debt service obligations, and measures of

household credit quality were generally little changed.

For example, delinquency rates on consumer loans and

prime mortgages—the two main components of total

household debt—stayed low through the spring of 2007,

as did those on subprime fi xed-rate mortgages. In addition,

household bankruptcy fi lings continued to be subdued in

the fi rst half of the year: They ran near the average pace

seen since early 2006, after the bulge that accompanied

the implementation of the new bankruptcy law in October

2005.

Some households, however, have experienced growing

fi nancial strains. Delinquency rates on subprime mort-

gages with variable interest rates, which account for about

9 percent of all fi rst-lien mortgages outstanding, continued

to climb in the fi rst fi ve months of 2007 and reached a level

more than double the recent low for this series, which was

recorded in mid-2005. The rise in delinquencies has begun

to show through to new foreclosures. In the fi rst quarter of

2007, an estimated 325,000 foreclosure proceedings were

initiated, up from an average quarterly rate of 230,000 over

the preceding two years; about half of the foreclosures this

year were on subprime mortgages. The decline in credit

quality in the subprime sector has likely stemmed from a

combination of several factors, including the moderation

in overall economic growth and some regional economic

weakness. In addition, a substantial number of subprime

borrowers with variable-rate mortgages have faced an

upward adjustment of the rates from their initial levels.

When house prices were rising rapidly and rates on new

loans were lower, many of these borrowers qualifi ed to

refi nance into another loan with more-favorable terms.

With house prices having decelerated and rates having

moved higher, however, the scope for refi nancing has

been reduced. Moreover, investor owners may have been

tempted to walk away from properties with little or no

equity. Subprime mortgages originated in late 2005 and

2006 have shown unusually high rates of early delin-

quency, suggesting that some lenders unduly loosened

underwriting standards during that period.

In recent months, credit has become less easily avail-

able in the subprime-mortgage market, as investors in

subprime-mortgage-backed securities reportedly have

scrutinized the underlying subprime loans more carefully

and lenders have tightened underwriting standards. For

example, more than half of the respondents to the ques-

tions on subprime residential mortgages in the Federal

Reserve’s April 2007 Senior Loan Offi cer Opinion Survey

on Bank Lending Practices indicated that they had tight-

ened credit standards on such loans over the previous three

months. In June, the federal fi nancial regulatory agencies

issued a fi nal Statement on Subprime Mortgage Lending to

address issues relating to certain adjustable-rate mortgage

products. Credit spreads on the lower-rated tranches of

new subprime securitizations have increased sharply, on

balance, this year, and issuance of subprime-mortgage-

backed securities has moderated from its vigorous pace

of the past couple of years. However, despite the ongoing

0

1

2

3

4

5

6

7

8

9

10

11

12

Percent

2007200620052004200320022001

Mortgage delinquency rates, 2001–07

Prime, fixed rate

Prime, variable rate

Subprime, fixed rate

Subprime, variable rate

N

OTE

: The data are monthly. Prime-mortgage data extend through April

2007, and subprime-mortgage data extend through May 2007. Delinquency

rate is the percent of loans ninety days or more past due or in foreclosure.

Prime mortgages include near-prime mortgages.

S

OURCE

: First American LoanPerformance.

0

200

400

600

800

Basis points

20072006

Spreads over libor of securities backed by subprime

residential mortgages, 2006–07

BBB-

A

AAA

N

OTE

: The data are weekly and extend through July 6, 2007.

S

OURCE

: Merrill Lynch.

Board of Governors of the Federal Reserve System 9

problems, the subprime market has continued to function,

and new loans are being made.

The Business Sector

Fixed Investment

After having risen sharply over much of 2006, real busi-

ness fi xed investment (BFI) lost some steam in the fourth

quarter and posted a relatively meager gain in the fi rst

quarter of 2007. The slower rise in business output in

recent quarters has likely been a moderating infl uence

on business investment expenditures. But on the whole,

economic and fi nancial conditions still appear to be favor-

able for capital spending: Corporate profi ts remain robust,

businesses have ample liquid assets at their disposal, and

conditions in fi nancial markets remain supportive.

Much of the recent softness in BFI was in spending on

equipment and software (E&S), which rose at an annual

rate of less than 2 percent in real terms in the fi rst quarter

after having fallen nearly 5 percent in the fourth quarter of

2006. Within the major components of E&S, real spend-

ing on high-tech equipment expanded at an annual rate of

more than 20 percent in the fi rst quarter of 2007 because

of both a surge in outlays on computers after the release

of a major new operating system and a spurt in investment

in communications gear. Aircraft purchases also posted

a sizable increase. However, spending on motor vehicles

tumbled, as many fi rms had accelerated their purchases of

medium and heavy trucks into 2005 and 2006 so that they

could take delivery before the Environmental Protection

Agency’s new emissions standards for engines went into

effect this year. Elsewhere, real investment in equipment

other than high-tech and transportation goods dropped at

an annual rate of 10 percent in the fi rst quarter after a fall

of nearly 5 percent in the previous quarter. The weakness

in this category, which accounts for roughly 40 percent

of investment in E&S when measured in nominal terms,

appears to have refl ected, in part, appreciable declines in

spending on equipment disproportionately used by the

construction and motor vehicle industries and was most

pronounced around the turn of the year.

Although the weakness in truck sales apparently

extended through midyear, real E&S outlays apart from

transportation equipment appear to have posted a solid

increase in the second quarter. Incoming information

suggests that high-tech spending continued to move up in

real terms—albeit not as fast as it did in the fi rst quarter.

Moreover, shipments and orders for equipment other than

high-tech and transportation items regained some lost

ground.

Nonresidential construction activity turned up steeply

in 2006 after having been stagnant for several years, and

it continued to exhibit considerable strength in early 2007.

Outlays for offi ce, retail, and industrial buildings are all

running well above year-earlier levels, and—given that

20

40

60

80

Billions of dollars, annual rate

200720062005200420032002

Gross issuance of alt-A and subprime-mortgage-backed

securities, 2002–07

H1

H2

Q1

Q2

N

OTE: Alt-A includes such products as mortgages with limited income

verification and mortgages secured by non-owner-occupied properties.

S

OURCE:

Inside MBS & ABS.

Alt-A

Subprime

10

+

_

0

10

20

Percent, annual rate

Change in real business fixed investment, 2001–07

Q1

Structures

Equipment and software

10

+

_

0

10

20

30

2007200620052004200320022001

Q1

N

OTE

: High-tech equipment consists of computers and peripheral equip-

ment and communications equipment.

S

OURCE

: Department of Commerce, Bureau of Economic Analysis.

High-tech equipment and software

Other equipment excluding transportation

10 Monetary Policy Report to the Congress July 2007

vacancy rates have moved down over the past couple of

years—prospects for further gains in coming quarters are

good. One exception to the recent strength in this sector

is the drilling and mining category, in which real outlays

fell in the fi rst quarter after three years of sizable gains.

The recent softening in this category of investment may

refl ect, in part, reported shortages of specialty equipment

and skilled labor.

Inventory Investment

Inventory investment slowed markedly in the fourth

quarter of 2006 as fi rms acted to stem rising inventory

imbalances, and it turned negative in the fi rst quarter of

2007. The downswing in inventory investment shaved

about 1 percentage point from the change in real GDP in

both the fourth and fi rst quarters, and it appears to have

brought stocks into better alignment with sales. Some of

the inventory correction was in the motor vehicle sector,

in which high gasoline prices have been causing demand

to shift to more-fuel-effi cient models—a trend that, by the

middle of 2006, had left dealers with bloated inventories

of light trucks and sport-utility vehicles. Facing little

prospect of signifi cantly stronger sales of those vehicles

in the near term, the manufacturers instituted sharp cuts

in production starting in the second half of last year. The

production cuts, which in the fi rst quarter of 2007 brought

assemblies of light vehicles to their lowest level in more

than a decade, helped clear out dealers’ lots and thus set the

stage for a step-up in assemblies in the second quarter. The

automakers have scheduled a further rise in assemblies in

the third quarter, in part to get a good start on producing

the new, more-fuel-effi cient models that will be introduced

to the public in coming months.

Excluding motor vehicles, inventories appeared to be

well aligned with sales through much of 2006, but they

too started to look excessive as the growth of aggregate

demand slowed in the latter part of the year. The emerging

imbalances, some—though not all—of which appear to

have been at fi rms that supply the construction and motor

vehicle industries, prompted production adjustments that

reduced non-auto inventory investment to a very modest

rate in the fi rst quarter. According to the limited available

information, the pace of real stockbuilding appears to have

remained low in April and May, and, for the most part,

inventories seem to have moved back into rough alignment

with sales. In fact, businesses surveyed in June by the

Institute for Supply Management reported that their cus-

tomers were mostly comfortable with their current stock

levels, whereas earlier in the year an elevated number of

respondents had characterized these inventory positions

as too high.

Corporate Profi ts and Business Finance

In the fi rst quarter of 2007, growth in corporate profi t-

ability slowed from last year’s pace, but the level of

profi tability remained high. Earnings per share for S&P

500 fi rms decelerated but still came in nearly 10 percent

above their year-earlier level. In the national income

accounts, profi ts of nonfi nancial corporations in the fi rst

quarter were little changed from year-earlier levels after

double-digit gains in 2006; nonetheless, before-tax profi ts

measured as a share of sector GDP were nearly 13 percent,

close to the high levels posted last year.

20

+

_

0

20

40

60

Billions of chained (2000) dollars, annual rate

2007200620052004200320022001

Change in real business inventories, 2001–07

Q1

S

OURCE: Department of Commerce, Bureau of Economic Analysis.

6

8

10

12

14

Percent

20072003199919951991198719831979

Before-tax profits of nonfinancial corporations

as a percent of sector GDP, 1979–2007

N

OTE

: The data are quarterly and extend through 2007:Q1. Profits are from

domestic operations of nonfinancial corporations, with inventory valuation

and capital consumption adjustments.

S

OURCE

: Department of Commerce, Bureau of Economic Analysis.

Board of Governors of the Federal Reserve System 11

Fueled in part by continued heavy merger and acquisi-

tion activity, nonfi nancial business debt expanded at an

annual rate of 9 percent in the fi rst quarter of this year, only

a bit slower than in 2006, and data in hand suggest a robust

pace of expansion again in the second quarter. Net bond

issuance has been solid so far in 2007, and commercial and

industrial lending by banks has remained strong. Although

lower-quality corporate credit markets experienced some

strains, generally narrow credit spreads have encouraged

corporate bond issuance, and the growth of business loans

has been spurred by banks’ accommodative lending pos-

ture. Considerable net fractions of respondents to the April

2007 Senior Loan Offi cer Opinion Survey indicated that

they had eased some terms—especially spreads of loan

rates over their costs of funds, costs of credit lines, and

loan covenants—on commercial and industrial loans over

the previous three months. Banks pointed to more-aggres-

sive competition from other banks or nonbank lenders and

to increased liquidity in the secondary market for these

loans as the most important reasons for having eased

business lending terms. Commercial paper outstanding

was fl at in the fi rst quarter but increased somewhat in the

second quarter.

Gross public issuance of equity by nonfi nancial corpo-

rations has continued to be moderate so far this year, but

private equity issuance has apparently remained strong,

as leveraged buyout activity has continued to climb.

However, given the elevated levels of share repurchases

and equity retirements from cash-fi nanced mergers and

acquisitions in the fi rst quarter, net equity issuance con-

tinued to be deeply negative.

Despite some deceleration in profi ts, the credit quality

of nonfi nancial fi rms has generally continued to be robust.

The six-month trailing bond default rate has stayed near

zero this year, and the delinquency rate on commercial

and industrial loans at banks remained extremely low in

the fi rst quarter. For public fi rms, balance sheet liquid-

ity was still high in the fi rst quarter, whereas corporate

leverage stayed near historical lows despite the large net

retirement of equity. In addition, net interest payments

relative to cash fl ow continued to be near the low end of

the range seen over the past two decades.

Commercial real estate debt expanded briskly in

the fi rst quarter of 2007, albeit not quite so rapidly as

200

+

_

0

200

400

Billions of dollars, annual rate

20072006200520042003

Selected components of net financing

for nonfinancial corporate businesses, 2003–07

Sum of selected

components

N

OTE

: The data for the components except bonds are seasonally adjusted.

The data for the sum of selected components are quarterly. The data for

2007:Q2 are estimated.

S

OURCE

: Federal Reserve Board; Securities Data Company; and Federal

Financial Institutions Examination Council, Consolidated Reports o

f

Condition and Income (Call Report).

Commercial paper

Bonds

Bank loans

600

400

200

+

_

0

Billions of dollars

200720042001199819951992

Net equity issuance at nonfinancial corporations, 1991–2007

NOTE: The data are annual through 2006; for 2007, they are as of Q1. Data

for 2006:Q4 and 2007:Q1 are estimated. Equity issuance includes funds

invested by private equity partnerships and stock option proceeds.

S

OURCE

: Federal Reserve Board, flow of funds data.

0

1

2

3

4

Percent

200720042001199819951992

Default rate on outstanding corporate bonds, 1992–2007

NOTE: The data are monthly and extend through June 2007. The rate for a

given month is the face value of bonds that defaulted in the six months

ending in that month, multiplied by two to annualize the defaults and then

divided by the face value of all bonds outstanding at the end of the calenda

r

quarter immediately preceding the six-month period.

S

OURCE: Moody’s Investors Service.

12 Monetary Policy Report to the Congress July 2007

in 2006, a pattern consistent with the net tightening of

credit standards on commercial real estate loans reported

in the Senior Loan Offi cer Opinion Survey. Spreads

on BBB-rated commercial-mortgage-backed securities

(CMBS) soared in late February and have varied within

an elevated range since then. The increase reportedly came

in response to a reduction in investor interest in collater-

alized debt obligations, sponsors of which traditionally

have purchased many of these securities, and to plans by

the rating agencies to increase the level of credit support

required for such securities. However, because rents on

commercial properties have been increasing and vacancy

rates have remained moderate, credit quality has generally

continued to be good. Delinquency rates on commercial

mortgages held by life insurance companies and on those

backing CMBS have stayed near the bottom of their recent

ranges this year. The delinquency rate on commercial

mortgages held by banks edged up further in the fi rst

quarter in response to a deterioration in the performance

of loans for multifamily properties and for construction

and land development; nevertheless, this delinquency rate

remained low by historical standards.

The Government Sector

Federal Government

The defi cit in the federal unifi ed budget narrowed further

during the past year: Receipts continued to rise at a fairly

rapid rate, while growth in outlays was relatively subdued.

Over the twelve months ending in June, the unifi ed bud-

get recorded a defi cit of $163 billion, $113 billion less

than during the comparable period ending in June 2006.

When measured relative to nominal GDP, the defi cit

has decreased steadily from a recent fi scal year high of

3.6 percent in 2004 to a little more than 1 percent during

the past twelve months.

Nominal federal receipts during the twelve months

ending in June were 8 percent higher than during the

same period a year earlier. This increase was considerably

smaller than the double-digit advances recorded in fi scal

2005 and fi scal 2006. Nonetheless, it was faster than the

increase in income and pushed up the ratio of receipts

to GDP to nearly 19 percent. Individual income tax

receipts continued to outpace the rise in taxable personal

income as measured in the national income and product

accounts (NIPA), likely a result, at least in part, of larger

10

15

20

Percent

20072003199919951991198719831979

Net interest payments of nonfinancial corporations

as a percent of cash flow, 1979–2007

N

OTE

: The data are quarterly and extend through 2007:Q1.

S

OURCE

: Department of Commerce, Bureau of Economic Analysis.

50

100

150

200

250

Basis points

200720052003200119991997

Spreads of ten-year investment-grade commercial-mortgage-

backed securities over swaps, 1997–2007

BBB

AAA

N

OTE: The data are weekly and extend through July 11, 2007.

S

OURCE: Bloomberg.

16

18

20

22

24

Percent of nominal GDP

200720031999199519911987

Federal receipts and expenditures, 1987–2007

Expenditures

Expenditures

excluding net interest

Receipts

N

OTE

: Through 2006, receipts and expenditures are on a unified-budge

t

basis and are for fiscal years (October through September); GDP is for the

four quarters ending in Q3. For 2007, receipts and expenditures are for the

twelve months ending in June, and GDP is the average of 2006:Q4 and

2007:Q1.

S

OURCE

: Office of Management and Budget.

Board of Governors of the Federal Reserve System 13

capital gains realizations (which are excluded from NIPA

income), the effect of some taxpayers moving into higher

tax brackets as their real incomes increased, and perhaps

a further shift in the distribution of income toward high-

income households, which typically face higher tax rates.

Corporate receipts, after rising at an annual rate of nearly

40 percent, on average, over the three years ending in

fi scal 2006, rose 15 percent during the year ending in

June, a rate more in line with the increase in corporate

profi ts.

Nominal federal outlays increased less than 3 percent

during the twelve months ending in June and edged down

to 20 percent of nominal GDP, around the lower end of

the narrow range that has prevailed since 2003. In large

part, the deceleration in outlays refl ected the tapering off

of the temporary bulge in expenditures for fl ood insurance

and disaster relief associated with the 2005 hurricanes.

Meanwhile, spending on health programs continued to

rise briskly, only in part because of the net increment

to spending from the Medicare Part D prescription drug

program, which started in January 2006. Defense spending

was up 5 percent over the period, an increase somewhat

below those recorded in fi scal years 2005 and 2006. Total

federal outlays were also boosted by a sizable rise in net

interest payments as interest rates moved higher, although

the increase in debt service costs was signifi cantly smaller

than that of a year earlier.

As measured in the NIPA, real federal expenditures on

consumption and gross investment—the part of federal

spending that is a direct component of GDP—fell at an

annual rate of nearly 4 percent in the fi rst quarter, as a drop

in defense spending more than offset a moderate increase

in nondefense purchases. Defense expenditures tend to be

erratic from quarter to quarter, and the fi rst-quarter dip

followed a large increase in the fourth quarter. Defense

spending appears to have turned back up in the second

quarter, and, given currently enacted appropriations, it is

likely to increase further in coming quarters.

All else being equal, the signifi cant narrowing of

the unifi ed budget defi cit over the past few years raises

national saving. However, the positive effect on national

saving of the smaller federal defi cit has been largely offset

by a downward drift in nonfederal saving. Although busi-

ness saving has increased substantially over this period,

personal saving has dropped sharply. Accordingly, total

national saving (that is, federal plus nonfederal) has

recovered only a little from the exceptionally low levels

reached between 2003 and 2005; measured net of esti-

mated depreciation, it has fl uctuated between 1½ percent

and 2½ percent of GDP since the start of 2006. If not

boosted over the longer run, persistent low levels of saving

will be associated with either slower capital formation or

continued heavy borrowing from abroad, either of which

would retard the rise in the standard of living of U.S.

residents over time and hamper the ability of the nation

to meet the retirement needs of an aging population.

Federal Borrowing

Federal debt rose at an annual rate of 6¾ percent in the

fi rst quarter of 2007, a bit slower than in the corresponding

quarter of last year. As of the end of the fi rst quarter, the

ratio of federal debt held by the public to nominal GDP

was about 36 percent, a level little changed from that in

recent quarters.

The improvement in the budget position of the federal

government has led the Treasury to scale back issuance

of marketable coupon securities. As part of its reduction

3

+

_

0

3

6

9

12

Percent, annual rate

2007200620052004200320022001

Change in real government expenditures

on consumption and investment, 2001–07

Q1

S

OURCE

: Department of Commerce, Bureau of Economic Analysis.

Federal

State and local

3

+

_

0

3

6

9

Percent of nominal GDP

200720031999199519911987

Net saving, 1987–2007

Nonfederal saving

Federal saving

Total

N

OTE: The data are quarterly and extend through 2007:Q1. Nonfederal

saving is the sum of personal and net business saving and the net saving o

f

state and local governments.

S

OURCE: Department of Commerce, Bureau of Economic Analysis.

14 Monetary Policy Report to the Congress July 2007

in issuance, the Treasury announced in May that it was

discontinuing auctions of three-year nominal notes. This

move had been widely anticipated and elicited little reac-

tion in fi nancial markets.

Overall, foreign purchases of Treasury securities appear

to have increased further this year, thereby bringing the

share of these securities held by foreign investors to a new

high of almost 45 percent at the end of the fi rst quarter.

The proportion of nominal coupon securities purchased at

auctions by foreign investors moved up in late 2006 and

has stayed elevated thus far this year, albeit well off the

peak reached in 2004. Balance of payments data point to

sizable net purchases by foreign private investors between

January and March, whereas such investors sold Treasury

securities, on net, in 2006. In contrast, net purchases by

foreign offi cial investors have declined somewhat this

year. Custody holdings at the Federal Reserve Bank of

New York on behalf of foreign offi cial and international

accounts have only edged up since the end of 2006.

State and Local Government

On the whole, state and local governments continue to

enjoy strong fi scal positions as a consequence of several

years of robust revenue infl ows and a period of appre-

ciable restraint on spending after these governments’

fi scal diffi culties earlier in the decade. Accordingly, over

the past year or so, states and localities in the aggregate

have been able both to raise expenditures and to maintain

healthy balances in their reserve funds. However, revenue

fl ows in many states appear to have slowed a bit of late, a

pattern similar to the one that has emerged at the federal

level. For local governments, property tax receipts are

still being bolstered by the earlier run-up in real estate

values, but the deceleration in house prices over the past

year will likely slow the rise in local revenues down the

road. Moreover, many state and local governments expect

to face signifi cant structural imbalances in their budgets

in coming years as a result of the ongoing pressures from

Medicaid and the need to provide pensions and health

care to an increasing number of retired state and local

government employees.

According to the NIPA, real expenditures on consump-

tion and gross investment by state and local governments

rose at an annual rate of nearly 4 percent in the fi rst quarter,

and they apparently posted a further increase in the second

quarter. Much of the strength in the fi rst half of 2007 was

in construction spending, which has been climbing since

the start of 2006, in part because of very rapid increases in

outlays on highways. Hiring by states and localities also

exhibited considerable vigor during the fi rst half of 2007,

both in the education sector and elsewhere; on average,

state and local government employment rose 30,000 per

month over the six months ending in June, compared with

an average monthly increase of 22,000 over the preceding

ten years.

State and Local Government Borrowing

Borrowing by state and local governments has been strong

thus far in 2007, largely because refundings in advance

of retirements have been elevated as interest rates have

remained relatively low. In contrast, issuance of short-

term debt has been moderate—a development consistent

with the strong budgets of state and local governments.

The credit quality of municipal bonds has remained solid

on the whole, as the number of bond-rating upgrades has

25

35

45

55

Percent of nominal GDP

20071997198719771967

Federal government debt held by the public, 1960–2007

N

OTE

: The final observation is for 2007:Q1. For previous years, the data

for debt are as of year-end, and the corresponding values for GDP are for Q4

at an annual rate. Excludes securities held as investments of federal

government accounts.

S

OURCE

: Federal Reserve Board, flow of funds data.

30

35

40

45

Percent

20072005200320011999

Treasury securities held by foreign investors

as a share of total outstanding, 1998–2007

N

OTE

: The data are quarterly and extend through 2007:Q1.

S

OURCE

: Federal Reserve Board, flow of funds data.

Board of Governors of the Federal Reserve System 15

outpaced the number of downgrades thus far this year. The

ratio of yields on municipal bonds to those on comparable-

maturity Treasury securities has stayed at the low end of

its range of the past decade.

The External Sector

In 2006, U.S. real net exports made a positive contribu-

tion to the full year’s economic growth for the fi rst time

since 1995. The contribution of net exports moved into

negative territory again, however, in the fi rst quarter of

this year, as imports rebounded and exports slowed from

their exceptional pace late last year. Data for April and

May point to a resurgence of exports and a moderation

of imports in the second quarter.

The U.S. nominal current account defi cit widened a bit

in the fi rst quarter of 2007 to $770 billion at an annual rate,

or about 5¾ percent of nominal GDP, from $752 billion

in the fourth quarter of 2006. The larger defi cit was due

to an increase in net unilateral transfers abroad. Although

the fi rst-quarter trade balance deteriorated in real terms,

increases in export prices outpaced those in import prices,

thereby leaving the nominal trade balance unchanged.

Despite the large negative U.S. net international invest-

ment position, the U.S. balance on investment income

remained positive and also was about unchanged in the

fi rst quarter.

International Trade

Despite continued solid foreign economic expansion and

persisting stimulus from earlier declines in the dollar, the

growth of real exports of goods and services slowed to

an annual rate of less than 1 percent in the fi rst quarter

from its exceptionally strong pace of more than 10 per-

cent in the fourth quarter. The slowdown was particularly

evident in sales of capital goods—especially aircraft and

computers—and industrial supplies, which fell in the fi rst

quarter after rising robustly in late 2006. Also contribut-

ing to the slowdown, real exports of services rose only

2 percent in the fi rst quarter after increasing more than

16 percent in the fourth quarter. Available data for nominal

exports in April and May suggest that real export growth

moved up in the second quarter, as increases in exports of

services, automobiles, industrial supplies, and consumer

goods more than offset a further contraction in exports

of capital goods.

Prices of exported goods rose at an annual rate of

4 percent in the fi rst quarter of 2007, up from the pace

of about 2½ percent seen in the second half of 2006.

Prices of non-agricultural industrial supplies, which had

been reduced in the fourth quarter by lower oil prices,

were pushed up in the fi rst quarter by higher prices for

metals and renewed increases in oil prices. In addition,

agricultural prices—especially those of corn, soybeans,

and wheat—have risen briskly over the past several

quarters, in part because of the direct and indirect effects

of the increased demand for ethanol. Monthly data

on trade prices in the second quarter point to further

increases in export prices on the strength of additional

run-ups in the prices of non-agricultural industrial sup-

plies, most notably metals.

After falling at an annual rate of 2½ percent in the

fourth quarter, real imports of goods and services rose

at a 5½ percent rate in the fi rst quarter. A sharp increase

in oil imports, after a fourth-quarter decline, was the

most important contributor to the swing, but imports of

computers, semiconductors, and natural gas also acceler-

ated. Imports of other goods continued to be weak, likely

7

6

5

4

3

2

1

+

_

0

Percent of nominal GDP

200720062005200420032002200120001999

U.S. trade and current account balances, 1999–2007

Trade

Current

account

N

OTE

: The data are quarterly and extend through 2007:Q1.

S

OURCE

: Department of Commerce.

10

5

+

_

0

5

10

15

Percent

200720062005200420032002200120001999

Change in real imports and exports of goods and services,

1999–2007

Q1

SOURCE: Department of Commerce.

Imports

Exports

16 Monetary Policy Report to the Congress July 2007

a result, in part, of slower U.S. growth; imports of autos

and industrial supplies, in particular, contracted sharply.

The growth of real imports of services dropped from

6¼ percent in the fourth quarter to 2¾ percent in the fi rst

quarter. Data for April and May imply some slowing of

overall real imports in the second quarter. In particular,

imports of oil and computers displayed noteworthy

decelerations.

Prices of imported goods excluding oil and natural

gas rose at an annual rate of about 1½ percent in the fi rst

quarter of 2007, as prices of both fi nished and material-

intensive goods recorded higher rates of increase. Monthly

trade price data suggest that import prices accelerated in

the second quarter, partly because of higher metals prices,

which have fl uctuated widely in recent months but are up

substantially, on balance, so far in 2007. More generally,

prices of industrial supplies have been rising briskly,

a movement that may refl ect, in part, a response to the

depreciation of the dollar in recent months. No such effect

of the dollar’s decline is readily apparent in the prices of

fi nished goods.

Oil prices fell at the beginning of 2007, as unusually

mild temperatures reduced oil demand and OPEC mem-

bers appeared less likely to implement fully production

cuts agreed to at the end of 2006. The spot price of West

Texas intermediate (WTI) crude oil, the U.S. benchmark,

fell from an average of $62 per barrel in December to

$54 per barrel in January. Oil prices then rose gradually as

it became apparent that OPEC, led by Saudi Arabia, indeed

would restrain oil production further. Oil prices also have

been supported by solid growth in demand, particularly

in developing countries, and by long-running concerns

about supply disruptions. Ongoing violence has depressed

oil production in Iraq and Nigeria; the Nigerian outage

recently worsened to about one-fourth of the country’s

estimated capacity. Since the start of the year, concerns

have also intensifi ed about a possible future disruption

of oil exports from Iran. The spot price of WTI averaged

$72 per barrel in the fi rst half of July.

Despite its elevated level by historical standards, the spot

price of WTI has not increased as much in recent months

as have the prices of other grades of crude oil because

of high inventories of WTI in the central United States

arising from interruptions for maintenance and unplanned

outages at refi neries. Since early March, the spot price of

Brent crude oil, the European benchmark, has risen about

$5 per barrel more than has the spot price of WTI; the price

of Brent averaged $76 per barrel in the fi rst half of July.

The Financial Account

The U.S. nominal current account defi cit continued to be

fi nanced primarily by foreign purchases of U.S. debt secu-

rities. Driven by purchases of U.S. government securities

by Asian central banks, foreign offi cial infl ows moved up

noticeably in the fi rst quarter. Although demand for U.S.

Treasury securities by foreign offi cial investors eased, it

was more than offset by increased offi cial purchases of

bonds and mortgage-backed securities issued by govern-

ment-sponsored enterprises (GSEs). Preliminary data

indicate that offi cial infl ows remained strong through

April.

Foreign private purchases of U.S. securities maintained

the extraordinary pace set in 2006. Demand for U.S.

Treasury bonds extended its fourth-quarter strength, while

demand for equities picked up from an already robust

level; purchases of corporate bonds moderated slightly,

10

20

30

40

50

60

70

80

Dollars per barrel

80

100

120

140

160

180

200

220

20072006200520042003

Prices of oil and of nonfuel commodities, 2003–07

January 2003 = 100

Oil

Nonfuel

commodities

N

OTE: The data are monthly. The price of nonfuel commodities extends

through June 2007. The last observation for the oil price is the average for

July 1 through July 13, 2007. The oil price is the spot price of West Texas

intermediate crude oil. The price of nonfuel commodities is an index o

f

forty-five primary-commodity prices.

SOURCE: For oil, the Commodity Research Bureau; for nonfuel com-

modities, International Monetary Fund.

+

_

0

50

100

150

200

250

300

Billions of dollars

20072006200520042003

U.S. net financial inflows, 2003–07

N

OTE

: The data are quarterly and extend through 2007:Q1.

S

OURCE

: Department of Commerce.

Official

Private

Board of Governors of the Federal Reserve System 17

and, on net, private foreigners sold debt issued by GSEs.

Foreign direct investment fl ows into the United States

weakened signifi cantly; the rate of infl ows in the fi rst

quarter was roughly half that in 2006.

Net purchases of foreign securities by U.S. residents,

which represent a fi nancial outfl ow, remained strong in

the fi rst quarter of this year. Net acquisitions of bonds

continued at the brisk pace recorded in the second half of

2006, while purchases of foreign stocks, although slowing

slightly, remained elevated. Outfl ows associated with U.S.

direct investment abroad strengthened to a near-record

rate.

The Labor Market

Employment and Unemployment

The demand for labor has been increasing at a moderate

rate this year, somewhat less quickly than in 2006. After

having averaged 190,000 per month in 2006, gains in pay-

roll employment averaged 145,000 per month in the fi rst

half of 2007. The civilian unemployment rate has changed

little since last fall and stood at 4.5 percent in June.

As was the case in 2006, job growth in the fi rst half