knightfrank.co.in/researchH2 2023 Knight Frank’s ultimate guide to the India real estate market performance and

opportunities in the world’s most exciting subcontinent.

India

Real Estate

Residential and Office Market - July - December 2023

www.knightfrank.co.in/research

Mumbai HO

Knight Frank (India) Pvt. Ltd.

Paville House, Near Twin Towers,

Off. Veer Savarkar Marg, Prabhadevi,

Mumbai 400 025, India

Tel: 022 6745 0101 / 4928 0101;

Bengaluru

Knight Frank (India) Pvt. Ltd.

204 & 205, 2nd Floor, Embassy Square,

#148 Infantry Road,

Bengaluru 560001, India

Tel: 080 40732600 / 22385515

Pune

Knight Frank (India) Pvt. Ltd.

Unit No.701, Level 7, Pentagon Towers P4,

Magarpatta City, Hadapsar,

Pune 411 013, India

Tel: 020 67491500 / 30188500;

Chennai

Knight Frank (India) Pvt. Ltd.

1st Floor, Centre block, Sunny Side,

8/17, Shafee Mohammed Road,

Nungambakkam, Chennai 600 006, India

Tel: 044 4296 9000

Gurgaon

Knight Frank (India) Pvt. Ltd.

Office Address: 1505-1508, 15th Floor, Tower B,

Signature Towers South City 1,

Gurgaon 122 001, India

Tel: 0124 4782700;

Hyderabad

Knight Frank (India) Pvt. Ltd.

Western Dallas Centre, 5th floor, Office #3,

Hyderabad Knowledge City,

Survey No. 83/1, Raidurg, Serilingampally Mandal,

Ranga Reddy District, Telangana Hyderabad - 500032

Tel: 040 44554141;

Kolkata

Knight Frank (India) Pvt. Ltd.

PS Srijan Corporate Park

Unit Number – 1202A, 12th Floor,

Block – EP & GP, Plot Number - GP 2,

Sector – V, Salt Lake, Kolkata 700 091, India

Tel: 033 66521000

Ahmedabad

Knight Frank (India) Pvt. Ltd.

Unit Nos. 407 & 408, Block ‘C’, The First,

B/H Keshav Baugh Party Plot,

Vastrapur, Ahmedabad – 380015

Tel: 079 48940259/ 40380259

Contents

All India

Ahmedabad

Bengaluru

Chennai

Hyderabad

Kolkata

Mumbai

NCR

Pune

04

14

22

30

38

46

54

62

70

Foreword

With the pandemic almost completely in the rear-view mirror, 2023 was expected to see the

beginning of a sustained global economic recovery. However, unrest in the geopolitical environment

caused by the conflicts in Eastern Europe and West Asia and the persistently high inflation

continued to weigh on the global economic environment. While the Indian economy has not been

completely insulated from the economic turbulence, timely interventions by the Reserve Bank of

India (RBI) and the Government have ensured that inflation has not spiraled out of control and the

economy has stayed on the growth path.

The 7.6% GDP growth in Q2 2023 (July – September 2023) has exceeded expectations, and the RBI’s

recently upgraded forecast of 7% for FY 2024 ensures that India continues to be a bright spot in a still

uncertain global economic environment. This undercurrent of economic stability and growth is also

reflected in the strong performance of the Indian real estate markets.

The office market, which could have been impacted by the geopolitical challenges, stayed resilient,

recording a stellar performance in 2023, just shy of the peak reached in 2019. Having said that, these

globally impactful events have changed in characteristics of the market. Based on the economic

growth and stability and changes in the attitude of corporations, Global Capability Centres (GCC)

and India facing businesses claimed centerstage to capitalize on the unique and substantial

growth opportunity that the country presents. The rising confidence in the improving economic

fundamentals of the country has spurred occupiers to make longer term commitments in the office

market.

The increasing participation of a more diverse occupier group across various markets marks a

significant milestone in the evolution of the Indian office market. We saw more office markets

reaching and indeed breaching the 10 mn sq ft mark this year. The growth was backed by a

significant improvement in office occupancies which is expected to continue both in India and

globally.

The residential market has continued from strength to strength with demand scaling 10-year highs

while the headline demand numbers convey a story of steady and resilient growth, their underlying

components are changing radically. The significant shift toward premiumization has taken root in

the residential market which can be seen as a concurrent trend across markets.

I invite you to read the 20th edition of Knight Frank India’s flagship half-yearly report – ‘India Real

Estate H2 2023,’ which tracks the ongoing developments that have impacted the residential and

office segments across the top 8 cities. I hope that you will find it insightful and interesting.

Shishir Baijal

Chairman and Managing Director

INDIA REAL ESTATE - INDIA

India

INDIA MARKET SUMMARY

H1 2015

H2 2015

H1 2016

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

H2 2020

H1 2021

H2 2021

H1 2022

H2 2022

H1 2023

H2 2023

Source: Knight Frank Research

Launches (Units) Sales (Units)

Note – 1 square metre (sq m) = 10.764 square feet (sq ft)

Source: Knight Frank Research

Residential Market

20000

38000

56000

74000

92000

110000

128000

146000

164000

182000

200000

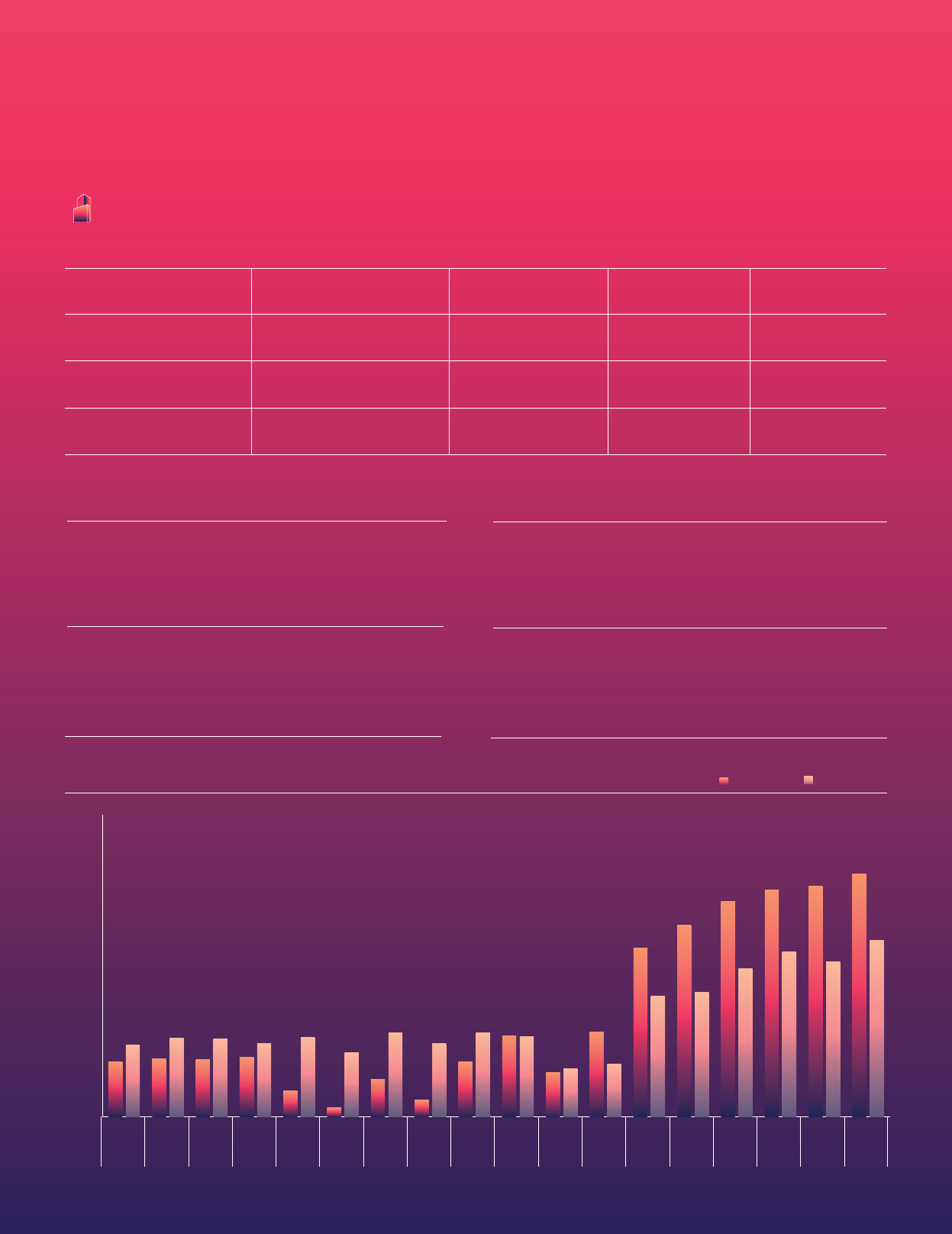

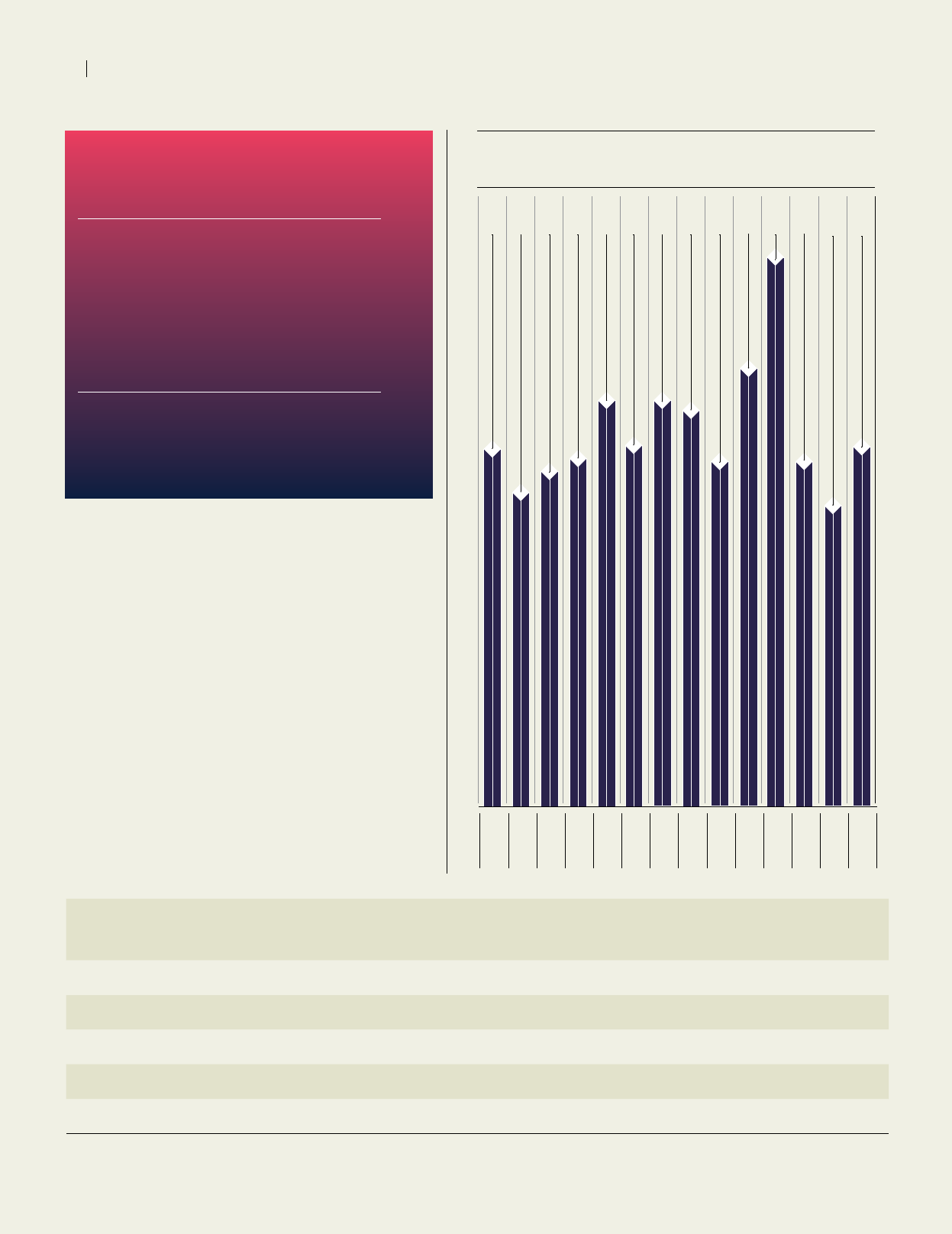

473,511 5.9

Unsold inventory (housing units) H2 2023

Quarters to sell (in quarters) H2 2023

5%

16.1

Change (YoY)

Age of unsold inventory (in quarters) H2 2023

Parameter 2023 2023 Change (YoY) H2 2023 H2 2023 Change (YoY)

Launches

(housing units)

350,746 7% 177,382 6%

Sales

(housing units)

329,097 5% 172,457 15%

LAUNCHES AND SALES TREND NO. OF UNITS

117,200

126,616

126,865

141,341

107,120

135,016

68,702

109,159

62,738

40,832

91,739

89,509

111,175

129,285

112,150

116,576

60,489

59,538

86,139

94,997

103,238

99,416

129,144

133,487

160,806

158,705

167,323

153,952

173,364

156,640

177,382

172,457

120,755

107,316

124,288

118,040

INDIA REAL ESTATE - INDIA

• As we move away from the pandemic, all

categories of real estate assets have undergone a

recovery, with the residential sector experiencing

the swiftest and most significant resurgence.

The heightened need for security and open living

spaces during the pandemic fueled a demand

for homes, bolstered further by exceptionally low

interest rates and comparatively affordable property

prices. 2023 was widely anticipated as a year of

sustained global recovery, with the pandemic in the

rear-view mirror and improving economic growth.

However, unforeseen challenges such as the war in

Ukraine and Israel and their extensive geopolitical

repercussions, coupled with persistent inflation,

posed a threat to global economies, threatening to

derail the strong recovery in the Indian real estate

markets as well.

• As central banks respond to inflationary pressures

by elevating policy rates and causing mortgages

to become more costly, momentum in global

residential markets has moderated following the

initial rebound in 2023. Nevertheless, in contrast

to the Reserve Bank of India’s cumulative increase

of 250 basis points in policy rates between

May 2022 and February 2023, the demand for

residential properties in the country not only

displayed resilience but also surged to a ten-year

high in terms of annual sales in 2023. Incidentally,

H2 2023 also saw the highest sales volumes

generated in a half-yearly period in ten years.

• Increased savings during lockdowns, minimal

income disruptions in mid and high-income

brackets, and a robust economic growth forecast

have fueled demand in the residential real estate

market in India. Besides, a house price growth trend

since 2021 has also created a feel-good factor

for prospective buyers, further helping the cause

of sales. The 0.17 mn units sold during H2 2023

constitute a healthy 12% YoY growth in volume and

was instrumental in pushing the annual sales tally

to a 5% higher level in 2023.

• The resurgence in demand has also put residential

development into overdrive with the half-yearly as

well as annual volume of units launched reaching

ten-year highs. In fact, launch volumes in 2022

and 2023 have exceeded that of sales for the

respective periods and notably, these are just two

of the three years when this has occurred over the

past ten.

• Demand momentum was strong in H2 2023 with

sales growing on a YoY basis across all markets.

Among the larger markets, Pune saw the most

sales growth at 28% YoY while Mumbai, NCR and

Bengaluru constituted 60% of the total sales during

the period.

• The share of annual sales in the <INR 5 mn ticket

size price segment has reduced from 45% in

2020 to 30% in 2023. Conversely, during the same

reference period, the share of sales in the INR 5-10

mn and >10 mn ticket-size categories grew from

35% to 37% and 20% to 34% respectively. The

higher income segments were not as impacted

by income disruptions caused by pandemic

exigencies as was initially expected. Besides, the

high savings rate due to the initial weak sentiments

and lockdown periods played their part in fueling

the current wave of demand.

• The mid and premium categories similarly

outperformed the affordable segment in absolute

sales growth over the past few years. The premium

segment with home prices over INR 10 mn has

been the standout performer with an annual

sales growth of 33% YoY in 2023 and a more

pronounced 49% YoY growth in H2 2023. While

sales growth in the mid segment was close to

market averages in annual and half yearly terms,

that of the affordable segment proved to be the

only drag on the market, falling by 16% YoY in 2023

and by 10% in H2 2023.

• Developers have been ahead of the curve and

judged the shifting preferences of the market by

launching lifestyle-oriented premium products. The

share of the number of units launched in the INR

5-10 mn and >10 mn ticket-size categories grew

from 28% to 37% and 15% to a significant 40%

respectively.

• As discussed earlier, while sales growth has been

strong, the volume of launches has exceeded that

of sales significantly causing unsold inventory

levels to rise by 5% YoY. And as overall market

traction has shifted toward the mid and premium

segments, so has that of the unsold inventory.

Both these segments have seen unsold inventory

levels rise more than the market average, with

the mid segment inventory level rising by 6% YoY

and that of the premium segment increasing by a

substantial 33% YoY.

• While the rising inventory levels can seem like a

matter of concern when viewed in isolation, it must

be seen in conjunction with the sales velocity to

depict a more accurate picture of market health.

The Quarters to Sell (QTS) level is a metric that

enables this by calculating the number of quarters

required by the market to exhaust existing inventory

levels at the sales velocity of the trailing eight

quarters. Generally, a lower QTS level denotes

greater sales traction and better market health.

The QTS level for the eight markets has been

consistently falling despite growing inventory

levels from 8.7 in H2 2020 to the 5.9 quarters (less

than 18 months) in H2 2023 and depicts a market

with improving fundamentals despite increasing

inventory.

• While the overall market remains in good health,

we have gone a level deeper to assess the state

of the market in the ticket-size segments that we

track. While unsold inventory levels in the affordable

category have dropped 8% YoY in H2 2023, the

QTS level is higher than the market average at 7.4

quarters, just shy of two years and still not very high.

And the converse is true for the mid and premium

segments which stand at 5 and 5.3 quarters

respectively, despite the significant increases in

unsold inventory levels for both segments.

• While sales volumes have been robust in H2 2023,

prices have also grown in the range of 4% to 11%

across all markets with Mumbai and Bengaluru

growing by 7% each and the NCR and Pune at 6%

YoY and 5% YoY respectively. This is the fourth

consecutive half-yearly period of price growth

across all markets.

• The residential market continues to move from

strength to strength with market sales volumes

at a ten-year high without any significant impact

on underlying fundamentals. Sales levels were

not materially dented by concerns over growing

inflation, high interest costs or slowing economic

growth. The industry continues to consolidate with

residential developments steadily shifting into the

hands of stronger developers who have been able

to weather the economic storm created by the

pandemic. While ready inventory remains a strong

preference for homebuyers, established developers

with a robust execution record are increasingly

finding a market for their under-construction

inventory. Economic momentum continues to be

strong with the GDP growing at 7.6% YoY in Q2

2023 (Q1 FY 2024) and should sustain homebuyer

sentiment as the market steps into 2024.

INDIA REAL ESTATE - INDIA

H2 2022

H2 2023

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

<5 mn 5-10 mn

>10 mn

35%

37% 28%

37%

35%28%

SALES LAUNCHES

H2 2023 (YoY change) 2023 (YoY change) H2 2023 (YoY change) 2023 (YoY change)

Mumbai 46,073 (12%) 86,871 (2%) 42505 (-1%) 93051 (3%)

NCR 29,888 (2%) 60,002 (3%) 32911 (-5%) 62649 (-1%)

Bengaluru 27,799 (4%) 54,046 (1%) 27584 (24%) 51126 (18%)

Pune 27,596 (28%) 49,266 (13%) 21203 (0%) 42437 (10%)

Hyderabad 17,525 (7%) 32,880 (6%) 24134 (7%) 46985 (7%)

Ahmedabad 8,131 (39%) 16,113 (15%) 11941 (15%) 22497 (8%)

Chennai 7,770 (6%) 14,920 (5%) 8150 (4%) 16272 (6%)

Kolkata 7,675 (32%) 14,999 (16%) 8954 (59%) 15730 (28%)

All India 172,457 (12%) 329,097 (5%) 177382 (6%) 350746 (7%)

RESIDENTIAL LAUNCHES AND SALES

Source: Knight Frank Research

Mid-segment sales

Premium segment sales

H1 2018 H2 2018 H1 2019 H2 2019 H1 2020 H2 2020 H1 2021 H2 2021 H1 2022 H2 2022 H1 2023 H2 2023

70,000

60,000

50,000

40,000

30,000

20,000

10,000

-

INDIA REAL ESTATE - INDIA

Ticket-size

segment

Unsold Inventory (housing units)

(YoY Change)

Quarters-to-sell

(QTS)

0 – 5 mn 199,742 (5%) 7.4

5 – 10 mn 144,458 (6%) 5.0

>10 mn 129,313 (33%) 5.3

Source: Knight Frank Research

329,097

Ten-year high in annual sales in 2023

RESIDENTIAL MARKET HEALTH RESIDENTIAL PRICE MOVEMENT

City

Unsold inventory

(YoY change)

QTS

Mumbai 165,395 (4%) 7. 7

NCR 103,605 (3%) 7.0

Bengaluru 53,479 (-5%) 4.0

Hyderabad 45,505 (45%) 5.7

Pune 39,214 (-15%) 3.4

Ahmedabad 29,361 (28%) 7. 8

Kolkata 21,417 (4%) 6.1

Chennai 15,536 (10%) 4.3

All India 473,513 (5%) 5.9

Source: Knight Frank Research Source: Knight Frank Research

City

H2 2023 in

INR/sq m (INR/sq ft)

12 month change

6 month

change

Mumbai 84,849 (7,883) 7% 4%

NCR 51,226 (4,759) 6% 3%

Bengaluru 63,508 (5,900) 7% 5%

Pune 48,515 (4,507) 5% 3%

Chennai 48,137 (4,472) 4% 3%

Hyderabad 59,740 (5,550) 11% 3%

Kolkata 38,632 (3,589) 7% 5%

Ahmedabad 32,620 (3,031) 4% 1%

INDIA REAL ESTATE - INDIA

The Knight Frank Affordability Index that tracks the EMI (Equated Monthly Instalment) to income ratio for households, has begun to show

some improvement after the brief decline in affordability levels seen in 2022. The better-than-expected economic momentum has

spurred the GDP to rise by 7.6% in the June quarter; and which in concurrence with the inflation levels reined in within the tolerance band

of the central bank, has caused income levels to rise enough to offset the rise in prices and interest rates.

While affordability levels have improved marginally, Mumbai is the only city beyond our affordability threshold of 50%, a level exceeding

which banks rarely underwrite a mortgage. Ahmedabad remains the most affordable housing market in the country with an affordability

ratio of 21% which implies that on an average a household in Ahmedabad needs to spend 21% of its income to pay EMI for a housing

loan. Ahmedabad was followed by Pune and Kolkata at 24% each in 2023.

While marginally better than last year, affordability levels across cities also stand significantly improved than those existing in pre-

pandemic 2019. For instance, in NCR, the affordability index improved from 34% in 2019 to 27% in 2023, while for Bengaluru, it improved

from 32% in 2019 to 26% in 2023. With inflation levels expected to remain at 5.4% in FY 2024 and the GDP growth for the same period

forecasted at 7%, affordability levels are expected to further improve in the following year as the tailwinds of home loan interest rate cuts

help the cause.

Knight Frank

Affordability Index

INDIA REAL ESTATE - INDIA

Mumbai

NCR

Bengaluru

Pune

Chennai

Hyderabad

Kolkata

Ahmedabad

2022

2010

2023

2021

1. Calculated as EMI/INCOME ratio

2. City-wide average affordability statistics cannot highlight disparities in housing costs within sub-markets or across the income spectrum.

Source: MOSPI, Knight Frank Research

METHODOLOGY

The Knight Frank Affordability Index indicates the proportion of income that a household requires to fund the monthly instalment (EMI) of a housing unit in a particular city. So, a

Knight Frank Affordability Index level of 40% for a city implies that on an average, households in that city need to spend 40% of their income to fund the EMI of a housing loan

for a unit. An EMI/ Income ratio of over 50% is considered unaffordable as it is the limit beyond which banks rarely underwrite a mortgage.

ASSUMPTIONS

• EMI, housing unit size and price/sq ft represent city-level averages.

• Loan Tenure – 20 years

• Loan to Value – 80%

• Home Loan Interest Rate – Median MCLR of all scheduled commercial banks with 40 bps spread

• Area of Housing Unit: House sizes are fixed for each city across the years but vary within different cities taking into account the average size preference for each city.

• Housing Price: Median housing price for that city.

93%

52%

53%

51%

53%

28%

29%

27%

48%

26%

27%

26%

39%

24%

25%

24%

24%

51%

27%

25%

47%

28%

30%

30%

45%

25%

25%

24%

46%

20%

22%

21%

INDIA REAL ESTATE - INDIA

India Office Market

INDIA MARKET SUMMARY

Note – 1 square metre (sq m) = 10.764 square feet (sq ft)

Source: Knight Frank Research

Parameter 2023

2023

Change (YoY) H2 2023

H2 2023

Change (YoY)

Completions

in mn sq m (mn sq ft) 3.98 (42.9) -13% 2.31 (24.8) -2%

Transactions

in mn sq m (mn sq ft) 5.53 (59.6) 15% 3.11 (33.4) 27%

85.69 (922.4) 16.1%

2023 Stock mn sq m (mn sq ft)

2023 Vacancy

6%

94

2023 Change (YoY)

2023 Change (YoY)

Basis points decrease

H1 2015

H2 2015

H1 2016

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

H2 2020

H1 2021

H2 2021

H1 2022

H2 2022

H1 2023

H2 2023

Source: Knight Frank Research

Completions Transactions

0.0

0.

5

1.0

1.5

2.

0

2.5

3.

0

3.5

4.

0

INDIA OFFICE MARKET ACTIVITY MN SQ M

1.54

1.75

2.09

2.23

1.87

1.99

1.04

1.94

1.90

1.289

1.70

1.95

2.22

2.55

3.48

3.08

1.71

1.60

1.59

2.06

1.39

1.14

2.20

2.40

2.24

2.35

2.35

2.45

1.67

2.43

2.31

3.1 1

1.81

2.18

2.02

2.40

INDIA REAL ESTATE - INDIA

• With the pandemic almost completely in the

rear-view mirror, 2023 was expected to see

the beginning of a sustained global economic

recovery. However, unrest in the global geopolitical

environment caused by the Russia - Ukraine

and Israel - Palestine wars and persistently high

inflation continued to weigh on the global economic

environment. While the Indian economy has not

been completely insulated from the economic

turbulence, timely interventions by the Central Bank

and the Government have ensured that inflation

has not spiraled out of control and the economy

has stayed on the growth path. The 7.6% GDP

growth in Q2 2023 (Q1 FY 2024) has exceeded

most expectations, and the RBI’s recently upgraded

forecast of 7% for FY 2024 ensures that India

continues to be a bright spot in a still uncertain

global economic environment. This undercurrent

of economic stability and growth is also reflected

in the relatively strong occupier activity seen in the

Indian office market.

• India’s growing stature as the largest democracy

with long term growth prospects of a stable market

for products and services across categories, makes

it one of the most attractive destinations to set up

businesses. The government’s exemplary handling

of the pandemic, the central bank’s success

in controlling inflation while supporting growth

and even the precise execution of the incredibly

complex Chandrayaan mission have been a clarion

call to the world at large that India is one of the

leaders among growth centers across the globe.

• Occupier sentiments have improved steadily in

2023 with cumulative transaction volumes across

the eight markets under our coverage increasing

progressively over the four quarters of the year. The

year ended within striking distance of the historic

highs in terms of annual transacted volumes with

5.53 mn sq m (59.6 mn sq ft) taken up in 2023. The

year ended on a strong note with H2 2023 seeing

transaction volumes of 3.11 mn sq m (33.4 mn sq

ft) which constitutes a healthy 15% growth in YoY

terms and incidentally also marks H2 2023 as

the half-yearly period with the highest transacted

volume since 2012.

• Transaction volumes in all markets grew in YoY

terms except for Bengaluru whose 1.16 mn sq m

(12.5 mn sq ft) tally in 2023 constitutes a 14% YoY

drop. This can be largely attributed to some extent

to the slowdown in demand from the Technology

sector but it must be noted that transaction

volumes during the base year of 2022 were

extraordinarily high and the volumes seen in 2023

are still in line with Bengaluru’s longer term average.

The Chennai market was the biggest outperformer

with 10.8 mn sq ft of office space being transacted

there during the year, a 92% growth in YoY terms.

The surge in demand from Global Capability

Centers (GCC) which accounted for 56% of the

transacted area was the primary driver of this spike

in volumes.

• While the overall transacted volume has been on

a steady uptrend, its underlying constituents have

changed substantially over time. Third party IT

services have been a prominent demand driver of

office space demand previously but India facing

businesses have been anchoring demand in

recent years due to a strategic business need to be

aligned with the growing Indian market. India facing

businesses accounted for 37% of the total volume

transacted during 2023, just shy of the 39% in

2022. The share of third party IT Services has

dropped from 16% to 11% in the same reference

period.

• With business sentiments improving and

uncertainties reducing steadily, occupiers are

more inclined to make longer term commitments

to the workplace by signing long-term leases.

The need for flexibility of tenure is not as intensely

felt as compared to a year ago when flex spaces

accounted for 19% of the total transacted

volumes relative to the current 17% in 2023. This

phenomenon is more visible in H2 2023 where

flex space operators took up just 11% of the total

transacted area compared to twice or 22% in H2

2022. However, it must be noted that H2 2023

is the first half-yearly period in which we have

observed a significant drop in the share of flex

spaces. The premise of a workplace specialist who

enhances employee productivity remains strong

and it needs to be seen if this drop in share is just a

temporary pause as the market consolidates or part

of a longer-term trend reversal.

• While India has always been known for its high

quality and low-cost human resource pool, the

need for friend-shoring and the China+1 trend, has

intensified strategic corporate investments in India.

The nature of work executed out of Indian offices

has also undergone a vast change over the years.

While Third party outsourcing centres were set up

initially to primarily manage processing activities

to capitalise on the cost arbitrage offered by the

Indian markets, Indian operations have now moved

up the value chain and actively contribute to the

organisation’s core business and are an integral

part of its growth strategy. This also reflects in the

nature of office space being demanded, which is of

higher quality and comes with a greater occupier

commitment on lease tenure and investment in the

workspace.

• The increasing confidence in the country’s

economic stability has substantially increased

corporate investments in setting up GCCs in India

and this is reflected in the growing share of GCCs

in the total transacted area. Their share has grown

substantially from 25% in 2022 to 35% in 2023. In

fact, the GCC category is the only one which has

grown in terms of market share among the four

end-use categories tracked by us.

• Completions have been comparatively subdued

as development interest is largely focused on

residential projects due to the relatively steeper

increase in sales and prices in the residential

market. 3.98 mn sq m (42.9 mn sq ft) of office

space were completed in 2023, 2% lower than

a year ago. The second half of the year was

comparatively better with 24.8 mn sq ft getting

delivered, constituting a 7% YoY growth.

• Rent levels have firmed up well across all markets

over the course of the year. This is the third

half-yearly period when rents have either grown

or remained stable across all markets. Despite

not having its best year in terms of transaction

volumes, rent growth has been strong in Bengaluru

at 7%. Among the other large markets, rent levels in

Mumbai, NCR and Chennai have grown at 4%, 2%

and 6% respectively.

• The sustained surge in office demand throughout

2023 despite the volatile global economic

environment underscores the positive business

sentiment that exists in the country today. The

physical occupancy level has also been steadily

increasing across markets and is being reported at

57% - 65% levels in the REIT portfolios, compared

to 47% - 55% last year. Remote working had never

really taken root in the Indian office space market

with some exceptions in Technology dominated

markets and almost all other sectors have reverted

to a full-time office environment, quite unlike the

scenario in most leading markets in the west. Given

that the inflation level is currently well within the

upper tolerance band of the RBI, it is likely that the

central bank will take a more assertive stance to

support growth and consider lowering the repo rate.

Besides, the signals of upcoming interest rate cuts

by the US Fed will pave the way for greater capital

flows to markets like India. These factors should

further galvanise office market fundamentals as the

market steps into 2024.

INDIA REAL ESTATE - INDIA

INDIA OFFICE MARKET VACANCY

H1 2015

H2 2015

H1 2016

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

H2 2020

H1 2021

H2 2021

H1 2022

H2 2022

H1 2023

H2 2023

20%

18%

16%

14%

12%

10%

8%

6%

4%

2%

0

16.7%

15.6%

15.1%

13.4%

12.4%

11.6%

12.9%

13.0%

12.6%

13.1%

14.2%

15.4%

16.6%

17.2%

17.0%

17.1%

16.1%

16.4%

Source: Knight Frank Research

38%

14%

22%

26%

38%

9%

11%

42%

India Facing

Third party

IT Services

Flex

Global Capability

Centres

Source: Knight Frank Research

H2 2022

H2 2023

Notes:

1. India Facing: These refer to such transactions whose lessees/ buyers are busi-

nesses which have an India focused business. I.e: no export or import.

2. Third party IT services: These refer to transactions whose lessees/ buyers are

focused on providing IT and IT enabled services to offshore clients. They service

multiple clients and are not necessarily owned by any of their clientele.

3. Global Capability Center (GCC): These refer to transactions whose lessees/

buyers are focused on providing various services to a single offshore company.

The offshore company has complete ownership of the entity that has transacted

the space.

4. Flex space: These refer to transactions by companies that specialise in providing

comprehensive office space solutions for other businesses along with the

benefits of flexibility of tenure, extent of services provided and the ability to scale

higher or lower as required.

On December 06, 2023, the Union Ministry of Commerce and Industry

amended the Special Economic Zones (SEZ) rules 2006. The new

amended rules now allow the Board of Approval, on request from a

developer of an IT or ITES SEZ, to permit the demarcation of a portion

of the built-up area within an SEZ unit on a floor-by-floor basis as a

non-processing or non-SEZ area. In simple terms, the Government

has allowed SEZs to lease space partially or in terms of floors, allowing

operators of office parks across the country to increase occupancy of

their properties.

If we look at the data, since the time direct tax breaks were removed for

new SEZ units in March 2020, it became less attractive for tenants and

vacancies increased. About 170 mn sq ft of ready IT SEZ office space is

available across the top six cities in India, and around 20% (over 30 mn sq

ft) is still vacant.

This new amendment could lead to an increase in demand for office

spaces in such properties and benefit the developers building IT/

ITES SEZs and it would also allow domestic tariff area suppliers to get

the benefit by being in the same buildings as their SEZ clients. The

Government’s decision to allow the demarcation of non-processing areas

in IT/ITES SEZs is a significant step that will benefit the developers and

create more jobs. The real estate industry has heartily welcomed this

move, and it is expected to have a positive impact on the commercial real

estate sector in India.

INDIA REAL ESTATE - INDIA

Source: Knight Frank Research

Source: Knight Frank Research

OFFICE TRANSACTIONS AND COMPLETIONS

OFFICE TRANSACTIONS

OFFICE COMPLETIONS

H2 2023 2023 H2 2023 2023

Mumbai 0.39 (4.2) (23%) 0.69 (7.4) (16%) 0.16 (1.7) (67%) 0.28 (3.1) (52%)

NCR 0.47 (5) (4%) 0.94 (10.1) (14%) 0.28 (3.1) (-43%) 0.65 (7) (-11%)

Bengaluru 0.51 (5.5) (-19%) 1.16 (12.5) (-14%) 0.65 (7) (-29%) 1.24 (13.4) (-14%)

Pune 0.41 (4.4) (54%) 0.62 (6.7) (9%) 0.1 (1.1) (-36%) 0.34 (3.6) (-46%)

Ahmedabad 0.12 (1.3) (44%) 0.17 (1.8) (-15%) 0.16 (1.7) (1293%) 0.18 (1.9) (34%)

Chennai 0.58 (6.3) (82%) 1 (10.8) (92%) 0.4 (4.3) (212%) 0.61 (6.6) (49%)

Hyderabad 0.55 (5.9) (68%) 0.82 (8.8) (32%) 0.49 (5.3) (-12%) 0.61 (6.5) (-42%)

Kolkata 0.08 (0.8) (45%) 0.13 (1.4) (20%) 0.08 (0.08) (-) 0.08 (0.8) (332%)

Total 3.11 (33.4) (27%) 5.53 (59.6) (15%) 2.31 (24.8) (-2%) 3.98 (42.9) (-13%)

MARKETWISE RENTAL MOVEMENT

Rental value range in H2 2023 in

INR/sq m/month (INR/sq ft/month)

12-month change 6-month change

Mumbai 1,227 (114) 4% 2%

NCR 917 (85) 2% 2%

Bengaluru 930 (86) 7% 4%

Pune 791 (74) 2% 2%

Ahmedabad 450 (42) 4% 1%

Chennai 700 (65) 6% 6%

Hyderabad 705 (66) 1% 0%

Kolkata 414 (39) 11% 1%

INDIA REAL ESTATE - AHMEDABAD

Ahmedabad

AHMEDABAD MARKET SUMMARY

H1 2015

H2 2015

H1 2016

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

H2 2020

H1 2021

H2 2021

H1 2022

H2 2022

H1 2023

H2 2023

Source: Knight Frank Research

Launches (Units) Sales (Units)

Note – 1 square metre (sq m) = 10.764 square feet (sq ft)

Source: Knight Frank Research

Residential Market

0

2,000

4,000

6,000

8,000

1

0,000

12,

000

14,

000

29,361 7.8

Unsold inventory (housing units) 2023

Quarters to sell (in quarters) 2023

28%

7. 3

Change (YoY)

Age of unsold inventory (in quarters) 2023

Parameter 2023 2023 Change (YoY) H2 2023 H2 2023 Change (YoY)

Launches

(housing units)

22,497 8% 11,941 15%

Sales

(housing units)

16,113 15% 8,131 39%

Average price in

INR/sq m (INR/sq ft)

INR 32,620 (INR 3,031) 5% - -

LAUNCHES AND SALES TREND NO. OF UNITS

8,062

7,751

7,491

9,075

8,809

8,556

5,200

7,400

1,874

2,916

1,323

2,844

3,398

8,212

8,089

8,501

2,627

2,520

4,745

3,986

6,226

4,208

8,422

4,703

10,385

8,197

10,424

5,865

10,556

7,982

11,941

8,131

7,941

7,800

8,087

8,101

INDIA REAL ESTATE - AHMEDABAD

• Historically, Ahmedabad has stood out as the

most cost-effective market among the leading

eight cities under our coverage. This distinction

can be largely attributed to the government’s

urban planning efforts aimed at accommodating

the city’s expanding population. Since 2006, the

municipal area of the city has expanded from 186

sq km to its present 466 sq km. This expansion has

played a crucial role in maintaining an equilibrium

between population growth and the city’s built-up

area. Ahmedabad has substantially succeeded in

avoiding the high congestion often seen in the city

centers of other Indian cities, while also steering

clear of low-density sprawl in its outskirts.

• The residential market in Ahmedabad has

rebounded and grown consistently from the lows

experienced during the pandemic as improving

homebuyer sentiments drove sales volumes.

Supply levels have also surged significantly as

developers seized the opportunity to capitalize on

the renewed demand. They aggressively launched

projects featuring larger areas and enhanced

amenities while raising prices, as homebuyer

demand remained strong.

• With the robust recovery in demand and prices

seen over the past two years, it remained to be

seen if market momentum continued in 2023.

Sales levels continued their run with 16,113 units

sold during the year, a healthy 15% higher than

the levels seen a year ago. The Ahmedabad

homebuyer remained resolute despite interest

rates rising to pre-pandemic levels and residential

prices reaching new highs.

• While demand growth has been healthy, developers

have launched new lifestyle-oriented products with

better amenities and larger areas, to tap into this

rich stream of demand. 22,497 units were launched

during 2023 representing an 8% growth over

2022. Just as sales volumes ended the year on a

strong note growing by 39% YoY in H2 2023, the

residential units launched during the second half

of 2023 grew by 15% YoY to 11,941 units during the

period.

• The state government’s encouragement to the

development of skyscrapers by increasing FSI

limits in the city have resulted in an increasing

number of such projects being launched, especially

along the SG Highway. These products are priced

significantly higher than the average residential

project, due to the greater cost of construction and

in equal measure due to the highly elevated prices

at which the land parcels were acquired. This is a

significantly differentiated premium/luxury product

offering compared to what the market has been

used to. The response has been encouraging thus

far and will be tested further in times to come.

• The demand for plotted developments had spiked

in the aftermath of the pandemic as the need for

large open living spaces intensified. This trend has

subsided substantially as we move further away

from the pandemic and normalcy resumes, and

sales conversions occur at prices that offer better

value.

• By virtue of having the lowest per square foot

residential prices among the leading eight markets,

Ahmedabad has always had the bulk of sales occur

in the affordable category of INR 5 mn and below.

This appears to have changed decisively in H2

2023 with the macro trend, of increasing sales in

the mid and premium category catching up with

those in the affordable segment, gaining ground

in Ahmedabad as well. H2 2023 marks the first

half-yearly period in which sales in residential units

priced at INR 5 mn and below constituted less

than half of the total sales. 48% of the sales in H2

2023 occurred in the affordable category while the

share of sales in the mid and premium segments

gained 6 percentage points each compared to H2

2022, to constitute 36% and 16% of the total sales

respectively.

• Market traction in the affordable category has

gradually lost momentum with sales growth

being less than the market average, and fresh

development activity de-growing by 28% YoY in H2

2023. In another first for the market, the share of

the units launched in the affordable category was

eclipsed by that of the mid segment in H2 2023.

• The affordable category currently constitutes over

half of the unsold inventory in the market. While

total unsold inventory levels have increased by

28% YoY, the market still holds less than two years

of inventory, a level which has remained steady

over the past two years. Development activity in

recent periods has been concentrated in the higher

ticket sizes in anticipation of heightened sales and

has exceeded sales in these categories causing

a buildup of inventory levels. This has caused the

QTS levels in the mid and premium segments to

remain elevated, above the market average QTS

level of 7.8 quarters.

• The QTS level is a quantification of the number of

quarters required by the market to absorb existing

inventory at the current rate of sales, and a lower

QTS level signifies a better state of health. While

the QTS in the affordable category is lower than

that of the other segments, this is attributed to the

substantial reduction in inventory in the segment

rather than an actual improvement in market

fundamentals. And, while the QTS levels of the mid

and premium categories are higher, they remain

well under three years of sales and do not signify

signs of weakness.

• The Ahmedabad Municipal Corporation usually

reserves 40% of the total town planning area

for roads, public utilities and other infrastructure.

However, the city civic body’s town planning (TP)

and estate management committee decision to

approve TP Scheme 32 at Shahwadi-Behrampur

with a 25% reduction could set an undesirable

precedent leading to congested development

in the city. Nonetheless, high affordability,

comparatively lower prices per square foot, and

an improving local economic environment remain

compelling drivers for the Ahmedabad residential

real estate market and should help support market

volumes in the following year.

MICROMARKET CLASSIFICATION

Micro market Locations

Central Paldi, Vasna, Navrangpura, Maninagar, Dudheshwar, Ambawadi

East Naroda, Vastral, Nikol, Kathwada Road, Odhav

North Gota, New Ranip, Tragad, Chandkheda, Motera

South Narol, Vatva, Vinzol, Hathijan

West SG Highway, Prahlad Nagar, Bopal, Thaltej, Science City Road

Source: Knight Frank Research

INDIA REAL ESTATE - AHMEDABAD

H2 2022

H2 2023

26% 28%

30% 26%

23% 23%

11% 13%

10% 10%

37% 32%

25% 27%

19% 18%

10% 13%

9% 9%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

AVERAGE RESIDENTIAL PRICE MOVEMENT

INR/SQ M

<5 mn 5-10 mn

H2 2022

H2 2022

>10 mn

H2 2023

H2 2023

H1 2015

H2 2015

H1 2016

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

H2 2020

H1 2021

H2 2021

H1 2022

H2 2022

H1 2023

H2 2023

33,000

32,000

31,000

30,000

29,000

28,000

27,000

26,000

28,376

29,386

29,684

29,816

29,816

30,354

30,354

30,570

30,677

31,173

30,085

30,215

30,161

30,139

31,000

31,216

32,367

32,620

Ticket-size

segment

Unsold Inventory (housing units)

(YoY Change)

Quarters-to-sell

(QTS)

0 – 5 mn 15,258 (6%) 7. 3

5 – 10 mn 9,922 (48%) 8.1

>10 mn 4,182 (118%) 9.3

North North

West West

East East

Central Central

South South

Source: Knight Frank Research

Source: Knight Frank Research

60%

30% 10%

16%

36%48%

29,361

Unsold inventory (housing units) H2 2023

INDIA REAL ESTATE - AHMEDABAD

Source: Knight Frank Research

RESIDENTIAL PRICE MOVEMENT IN SELECT LOCATIONS

Micro Market Location

Price range in H2 2023 in

INR/sq m (INR/sq ft)

12 month Change 6 month Change

Central

Ambavadi 64,000-70,000(5,950-6,500) 5% 1%

Navrangpura 56,000-66,000 (5,200-6,200) 4% 2%

East

Nikol 28,000-35,500 (2,600-3,300) 4% 2%

Vastral 26,000-31,200 (2,400-2,900) 3% 1%

North

Chandkheda 28.000-37,000 (2,600-3,400) 4% 2%

Motera 37,600-45,600(3,500-4,200) 4% 2%

South

Aslali Circle 18,300-21,600 (1,700-2,000) 4% 2%

Vatwa 19,400-24,800(1,800-2,300) 3% 2%

West

Bopal 35,500-44,200 (3,300-4,200) 4% 3%

Prahlad Nagar 59,200-61,500 (5,500-5,800) 5% 1%

MICROMARKET HEALTH

Micro-market Unsold Inventory (housing units) (YoY Change) Quarters-to-sell (QTS)

Central 3,496 (6%) 7.1

East 4,235 (28%) 5.4

North 8,114 (71%) 7.1

South 3,644 (8%) 10.0

West 9,873 (20%) 9.9

Source: Knight Frank Research

INDIA REAL ESTATE - AHMEDABAD

Ahmedabad Office Market

Note – 1 square metre (sq m) = 10.764 square feet (sq ft)

Source: Knight Frank Research

Parameter 2023

2023

Change (YoY) H2 2023

H2 2023

Change (YoY)

Completions

in mn sq m (mn sq ft) 0.18 (1.9) 34% 0.16 (1.7) 1,293%

Transactions

in mn sq m (mn sq ft) 0.17 (1.8) -15% 0.12 (1.3) 44%

Average transacted rent

in INR/sq m/month (INR/sq ft/month) 450 (41.8) 4.2% - -

3.47 (37.4) 41.4%

2023 Stock mn sq m (mn sq ft)

2023 Vacancy

5%

137

2023 Change (YoY)

2023 Change (YoY)

Basis points decrease

H1 2015

H2 2015

H1 2016

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

H2 2020

H1 2021

H2 2021

H1 2022

H2 2022

H1 2023

H2 2023

Source: Knight Frank Research

Completions Transactions

0.00

0.0

5

0.10

0.15

0.

20

0.25

0.

30

AHMEDABAD OFFICE MARKET ACTIVITY MN SQ M

0.06

0.05

0.07

0.03

0.06

0.07

0.10

0.02

0.21

0.06

0.08

0.20

0.25

0.05

0.21

0.09

0.24

0.05

0.23

0.08

0.10

0.04

0.13

0.07

0.12

0.12

0.01

0.08

0.02

0.05

0.16

0.12

0.10

0.03

0.04

0.05

INDIA REAL ESTATE - AHMEDABAD

• Annual transaction volumes in the Ahmedabad

office market had ranged between 1-1.5 mn sq

ft until the pandemic era. However, the past two

years have seen the market achieving significantly

higher volumes. Its increasing stature as a growing

economic hub with the establishment of the

International Financial Services Centres Authority

(IFSCA) in 2020 and the active support received

from the state and central governments are playing

an important role in improving business dynamics

in this budding office market.

• 2023 ended on a strong note with H2 2023

achieving the highest volumes ever seen in a

half yearly period. 0.12 mn sq m (1.3 mn sq ft)

were transacted during H2 2023, a 44% growth

compared to the previous period. While annual

transaction volumes have comfortably exceeded

the levels seen before the pandemic, the 0.17 mn

sq m (1.8 mn sq ft) transacted in 2023 was 15%

lower than the record high for annual transacted

volumes achieved in 2022.

• Despite the substantial vacancy in the Ahmedabad

office market, the dearth of available space in

the highly sought after locations between CG

Road and SG Highway kept transaction levels

suppressed in the first half of the year. The

Ahmedabad office market is also unique in terms

of the high investment interest which does not lead

to occupancy. The vacancy level seems to have

peaked and trended down to the current 41% level

at the end of H2 2023.

• The relative dearth of quality supply in these

locations was addressed substantially in H2 2023

as 0.16 mn sq m (1.7 mn sq ft) of office space

came online on SP Ring Road, Bopal Ambli Road,

Vastrapur and Sindhubhavan. This was a significant

driver for the record volumes seen in the second

half of the year. Most of the area transacted during

the period occurred in Q4 2023 at 0.1 mn sq m (1.1

mn sq ft), which incidentally, was also the highest

quarterly transacted volume achieved by the

market.

• Occupier activity continued to be concentrated in

CBD West with locations like Vastrapur, Prahlad

Nagar, Sindhubhavan and SG Highway accounting

for 87% of the total area transacted during the

period. The comparatively higher grade of office

spaces being developed here along with the

growing infrastructure has continued to attract the

occupiers’ focus in recent times.

• The largest transaction in H2 2023 took place in

Vastrapur in CBD West. This 0.01 mn sq m (0.2 mn

sq ft) lease was inked by BFSI major HDFC.

• India facing businesses continued to drive

volumes in the market and accounted for 81% of

the transacted volume during the year. Occupier

demand in this category was well distributed

across BFSI, IT/ITES, Manufacturing and other

service sectors signifying the broad-based demand

for setting up India facing businesses during the

period.

• The share of flex spaces has grown consistently

in Ahmedabad especially since the pandemic, as

their premise of flexibility presented great value

to occupiers not wanting to make longer term

commitments in a still volatile macro-economic

environment. However, the share of flex space

transactions has fallen significantly from 42% in

H2 2023 to 14% in the current analysis period.

While the improving business environment has

inspired confidence in occupiers to make longer

term commitments, we believe the need for a

workplace specialist remains strong and this fall

in share points more toward a pause in demand

while existing capacities get taken up rather than a

reversal in trend.

• 2023 has ended on a strong note for the

Ahmedabad office market as occupier sentiments

have improved, and their increased willingness

to ink longer term commitments bodes well for

the market. Rents have also grown by 4% YoY in

tandem, pushed by the record volumes seen in H2

2023. The concerted efforts of both the state and

central governments to transform Ahmedabad into

an economic hub, coupled with its affordable real

estate and extensive connectivity infrastructure,

continue to position the city as an appealing choice

for office occupiers.

Business district Micro markets

CBD West Bodakdev, Keshav Baug, Prahladnagar, Satellite, SG Highway, Thaltej

PBD Gandhinagar, GIFT City

CBD Ashram Road, Ellisbridge, Paldi

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

H2 2020

H1 2021

H2 2021

H1 2022

H2 2022

H1 2023

H2 2023

50%

45%

40%

35%

30%

25%

20%

15%

10%

5%

0%

22.2%

23.7%

24.6%

26.4%

34.0%

35.9%

41.7%

45.2%

45.8%

45.9%

45.1%

42.8%

41.8%

41.4%

Source: Knight Frank Research

INDIA REAL ESTATE - AHMEDABAD

AVERAGE DEAL SIZE TREND SQ M

CBD

CBD West

PBD

83%

15%

2%

87%

12%

1%

39%

81%

2,211

1,771

1,039

1,114

1,297

2,024

2,407

2,928

1,135

2,350

3,423

2,292

1,420

2,842

42%

14%

7%

6%

12%

0%

India Facing

Third party

IT Services

Flex

Global Capability

Centres

Source: Knight Frank Research

Source: Knight Frank Research

Source: Knight Frank Research

H2 2022

H2 2022

H2 2023

H2 2023

Rental value range in H2 2023 in INR/

sq m/month (INR/sq ft/month) 12-month change 6-month change

CBD 388-463 (36-43) 3% 2%

CBD West 431-549 (40-51) 5% 3%

PBD 323-441 (30-41) 1% 1%

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

H2 2020

H1 2021

H2 2021

H1 2022

H2 2022

H1 2023

H2 2023

INDIA REAL ESTATE - AHMEDABAD

INDIA REAL ESTATE - BENGALURU

Bengaluru

BENGALURU MARKET SUMMARY

H1 2015

H2 2015

H1 2016

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

H2 2020

H1 2021

H2 2021

H1 2022

H2 2022

H1 2023

H2 2023

Source: Knight Frank Research

Launches (Units) Sales (Units)

Note – 1 square metre (sq m) = 10.764 square feet (sq ft)

Source: Knight Frank Research

Residential Market

0

5000

10000

15000

20000

25000

30000

53,479 4.0

Unsold inventory (housing units) 2023

Quarters to sell (in quarters) 2023

-5%

18.1

Change (YoY)

Age of unsold inventory (in quarters) 2023

Parameter 2023 2023 Change (YoY) H2 2023 H2 2023 Change (YoY)

Launches

(housing units)

51,126 18% 27,584 24%

Sales

(housing units)

54,046 1% 27,799 4%

Average price in

INR/sq m (INR/sq ft)

INR 63,508 (INR 5,900) 7% - -

LAUNCHES AND SALES TREND NO. OF UNITS

21,400

22,234

24,190

27,849

24,281

26,220

13,395

20,309

14,026

8,384

15,556

11,826

20,894

28,225

12,878

19,851

10,806

12,177

9,123

11,402

13,389

14,812

17,218

23,218

21,223

26,677

22,197

26,686

23,542

26,247

27,584

27,799

21,210

13,336

25,802

17,973

INDIA REAL ESTATE - BENGALURU

• Bengaluru’s residential real estate market

continued its growth momentum in 2023 even

though the borrowing costs have significantly

increased since the interest rate upcycle began in

May 2022. The city’s economic prosperity faced

additional headwinds arising from volatility in the

tech sector and the start up eco system, due to

funding winters. A progression in sales, despite the

aforementioned headwinds, indicates continuation

in buyer appetite for home ownership in Bengaluru.

In 2023, Bengaluru registered residential sales

volume of 54,046 units, a nine year high. The strong

sales have boosted developer appetite to launch

large scale projects in the city. In 2023, the city

witnessed new launches of 51,126 units, a multiyear

high. While the Bengaluru centric developers

continue with their launches, the city has also

been gaining interest from non-Bengaluru centric

developers.

• In terms of ticket size, the sales as well as the

launches were concentrated in the mid and the

premium segment. During H2 2023, 49% of the

sales were concentrated in the mid segment (INR

5-10 mn) and 41% of sales were concentrated

in the premium segment (above INR 10 mn), a

significant improvement from 28% of the total

sales during H2 2022. Further bifurcation of figures

reveal that within the premium category, the sale of

houses priced above INR 20 mn have significantly

increased. During H2 2023, housing sales above

INR 20 mn comprised 12% of the total sales in

the city, a significant growth from 5% in H2 2022.

This highlights a growth in the income profile of the

city. While the tech sector primarily dominates the

city’s employment profile, the economic activities

of Bengaluru are diverse. The city hosts many

non-tech industries such as life sciences, defence

and aerospace, educational institutions, consulting

firms etc. which keep the city’s income growth well

balanced, thus driving the consumption demand

including that for real estate.

• Moreover, the consumers are flexible and willing to

pay a premium for larger, more comfortable spaces

with luxurious amenities. In tandem with the sales,

the launches were concentrated in the mid and

luxury segments comprising a share of 46% and

49% respectively during H2 2023. In terms of price,

3,492 units were launched in the price category

of above INR 20 mn, a multifold increase from

297 units launched 5 years ago. Considering the

consumer preference for large, spacious homes,

the average unit size of the new launches in 2023

stood at 1651 sq ft compared to 1450 sq ft in 2019,

pre COVID.

• The traditional South Bengaluru micro-market

continued to dominate sales comprising a share

of 39% of the total sales in the city in 2023. The

micro-market is well connected to the large

employment hubs located in Electronic City, Outer

Ring Road (ORR) etc. and is primarily dominated

by end-use consumers. Additionally, the ongoing

construction of the metro-lines, i.e., Yellow Line on

the Hosur Road and the extension of Purple Line to

Bannerghatta Road, adds impetus to the transport

infrastructure of this micro-market which in turn

will continue to keep afloat the demand for real

estate in this micro-market. While the mid-segment

primarily dominated this market, of late, there has

been a sharp rise in the development of luxury

residential real estate by prominent developers

such as Prestige, Puravankara, Adarsh, Sobha etc.

• In terms of launches, East Bengaluru micro-

market comprised a larger share of 48% of all the

launches in the city. East Bengaluru is a prime IT

hub with the presence of quality Grade A tech parks

in Whitefield, ITPL etc. The operation of 37 kms

of Purple Line metro connecting East Bengaluru

with the other parts of the city gives an additional

boost to the real estate market in East Bengaluru,

both commercial as well residential. Besides end

use, the residential demand in East Bengaluru,

specifically in localities such as Whitefield, is

also led by investment purposes. Thus, due to

its relatively strong economic profile compared

to other micro markets in the city, it encourages

developers to launch high end luxury projects in

this micro-market. East Bengaluru has a presence

of some prominent luxury and ultra-luxury projects

with an average ticket price of above INR 50 mn

by Grade A developers such as Embassy, Prestige,

DivyaSree etc. In terms of sales, the cluster

witnessed 32% of all the residential sales in 2023

with demand expanding to the peripherals of the

region such as Budigere Cross, Hoskote etc.

• The North Bengaluru micro-market is an emerging

and one of the fastest growing clusters in the city.

In 2023, the micro-market witnessed 22% of sales,

with a sharp rise in the absolute volumes. The

growing sales have accelerated developer interest

in this micro-market which comprised 18% of all

launches in the city. To accommodate the growing

population and demand, the development potential

has expanded beyond Hebbal and Yelahanka. The

micro-market is also witnessing one of the fastest

growths in infrastructure development. The Blue

Line metro connecting North Bengaluru via ORR

is one of the fastest developing metro projects

in the city and is expected to be operational from

2026. The operation of Kempegowda International

Airport Terminal 2 has led to massive infrastructure

investment in this region. In recent years, it has

witnessed the development of large commercial

real estate projects such as Aerospace Park,

Devanahalli Business Park and other SEZ and non

SEZ developments. Currently, North Bengaluru

and its peripherals have about 15 mn sq ft of

commercial office stock, and about 8 mn sq ft

is expected to be added by 2025, providing an

opportunity for growth of residential projects in the

region. In addition to the transport infrastructure

development, social infrastructure such as schools,

hospitals etc. is also well established in this cluster.

• Moreover, the developers are taking advantage of

the lush green surroundings in the cluster and have

been launching luxury and ultra-luxury residential

villas with modern exclusive designs, and plotted

developments in North Bengaluru. Such projects

have been attractive to the HNI and UHNI investors

and are being sold out within a very short span of

time from the launch.

• In terms of residential prices, Bengaluru witnessed

a 9% YoY growth with a weighted average price

of INR 63,505/sq m. The price growth is primarily

demand driven as hybrid work structure and

return to office is driving people, especially those

MICROMARKET CLASSIFICATION

Micro market Locations

Central MG Road, Lavelle Road, Langford Town, Vittal Mallya Road, Richmond Road

East Whitefield, Old Airport Road, Old Madras Road, KR Puram, Marathahalli

West Malleshwaram, Rajajinagar, Yeswanthpur, Tumkur Road, Vijayanagar

North Hebbal, Bellary Road, Hennur, Jakkur, Yelahanka, Banaswadi

South Koramangala, Sarjapur Road, Jayanagar, JP Nagar, HSR Layout, Kanakapura Road, Bannerghatta Road

Source: Knight Frank Research

INDIA REAL ESTATE - BENGALURU

0% 0%

31% 33%

13% 13%

46% 46%

10% 08%

0% 0%

55% 32%

20% 22%

21% 39%

04% 07%

AVERAGE RESIDENTIAL PRICE MOVEMENT INR/SQ M

H2 2022

H2 2022

H2 2023

H2 2023

H1 2015

H2 2015

H1 2016

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

H2 2020

H1 2021

H2 2021

H1 2022

H2 2022

H1 2023

H2 2023

70,000

60,000

50,000

40,000

30,000

20,000

10,000

-

50,053

51,452

51,721

52,205

52,001

49,396

50,881

50,386

51,893

53,572

53,605

53,120

52,959

55,435

57,674

59,315

60,739

63,508

Central Central

East East

North North

South South

West West

Source: Knight Frank Research

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

<5 mn 5-10 mn

>10 mn

Ticket-size

segment

Unsold Inventory

(housing units) (YoY Change)

Quarters-to-sell

(QTS)

0 – 5 mn 17,872 (-19%) 6.1

5 – 10 mn 24,744 (-9%) 3.9

>10 mn 10,863 (57%) 2.6

26%

46% 28%

40%

49%11%

H2 2022

H2 2023

employed in the IT to move back to the city. To

accommodate the demand, the residential supply

in the city is scaling upwards too, as witnessed by

the multiyear high launches in 2023. Thus, going

ahead, as supply aligns with demand, the price

growth is likely to moderate in 2024. However, the

real estate market of the city will continue to be

vibrant owing to the growing economic profile of the

city.

• As a result, the quarters-to-sell (QTS) for Bengaluru

has narrowed to 4.1 quarters, which is a historical

low. The age of unsold inventory (AoI) inched up

to 18.1 in 2023. However, the high AoI does not

correlate with the healthy residential demand and

is raised due to the presence of stalled projects in

the city. Some of these projects were launched over

a decade ago and continue to remain on hold for

various reasons.

INDIA REAL ESTATE - BENGALURU

Source: Knight Frank Research

RESIDENTIAL PRICE MOVEMENT IN SELECT LOCATIONS

MICROMARKET HEALTH

Micro-market Unsold Inventory (housing units) (YoY Change) Quarters-to-sell (QTS)

Central 17 (-87%) 0.6

East 15,346 (66%) 3.4

North 9,743 (-25%) 3.7

South 26,241 (-14%) 5.0

West 3,131 (-32%) 3.0

Source: Knight Frank Research

Micro Market Location

Price range in H2 2023 in

INR/sq m (INR/sq ft)

12 month Change 6 month Change

Central

Langford Town 1,61,460-2,36,808 (15,000-22,000) 3.0% 3.0%

Lavelle Road 2,26,044-3,22,920 (21,000-30,000) 3.0% 3.0%

East

KR Puram 43,056-76,424 (4,000-7,100) 5.9% 1.3%

Whitefield 51,129-86,090 (4,750-7,998) 11.1% 5.7%

Marathahalli 45,209-82,883 (4,200-7,700) 7. 3 % 3.8%

North

Hebbal 59,202-1,29,168 (5,500-12,000) 12.2% 6.7%

Yelahanka 45,209-83,959 (4,200-7,800) 10.1% 5.7%

Thanisandra 46,285-95,800 (4,300-8,900) 11.2% 6.4%

Hennur 45,209-96,876 (4,200-9,000) 10.6% 5.0%

South

Sarjapur Road 46,285-91,494 (4,300-8,500) 9.6% 3.9%

Kanakpura Road 45,209-80,730 (4,200-7,500) 8.6% 4.2%

Electronic City 37,674-69,966 (3,500-6,500) 8.7% 4.5%

Bannerghatta Road 45,209-78,039 (4,200-7,250) 8.5% 4.0%

West

Yeshwantpur 64,584-1,17,328 (6,000-10,900) 8.7% 6.8%

Malleswaram 88,265-1,56,078 (8,200-14,500) 7. 9 % 7.9 %

Rajajinagar 89,341-1,71,148 (8,300-15,900) 8.8% 7. 5 %

Tumkur Road 40,365-67,275 (3,750-6,250) 9.7% 6.5%

INDIA REAL ESTATE - BENGALURU

Bengaluru Office Market

Note – 1 square metre (sq m) = 10.764 square feet (sq ft)

Source: Knight Frank Research

Parameter 2023

2023

Change (YoY) H2 2023

H2 2023

Change (YoY)

Completions

in mn sq m (mn sq ft) 1.24 (13.4) -14.4% 0.65 (7.0) -21%

Transactions

in mn sq m (mn sq ft) 1.16 (12.5) -14.3% 0.51 (5.5) -19%

Average transacted rent

in INR/sq m/month (INR/sq ft/month) 929.5 (86.4) 7% - -

20 (215) 15.1%

2023 Stock mn sq m (mn sq ft)

2023 Vacancy (%)

6.6%

100

2023 Change (YoY)

2023 Change (YoY)

basis points increase

H1 2015

H2 2015

H1 2016

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

H2 2020

H1 2021

H2 2021

H1 2022

H2 2022

H1 2023

H2 2023

Source: Knight Frank Research

Completions Transactions

0.0

0.1

0.

2

0.

3

0.

4

0.

5

0.

6

0.7

0.

8

0.

9

1.0

BENGALURU OFFICE MARKET ACTIVITY MN SQ M

0.4

0.6

0.4

0.5

0.6

0.6

0.3

0.5

0.3

0.4

0.3

0.4

0.7

0.8

0.8

0.6

0.4

0.4

0.5

0.7

0.5

0.3

0.6

0.8

0.5

0.7

0.9

0.6

0.6

0.6

0.6

0.5

0.5

0.5

0.6

0.6

INDIA REAL ESTATE - BENGALURU

• Bengaluru continues to be the most favored

market by occupiers in 2023, accounting for

21% of the overall transactions across the top

8 cities. However, within the market, there has

been moderation in the leasing activities due to

moderation in leasing by tech occupiers i.e. third

party IT services, stall in the expansion of start-ups

due to funding winters, and moderation in the

average size of the transactions. Owing to these

factors, Bengaluru registered transaction leasing

volume of 1.16 mn sq m (12.5 mn sq ft) in 2023,

a 14% de-growth when compared to 2022. The

moderation observed does not necessarily signal

a decline in office transactions in Bengaluru. On

the contrary, office leasing in 2023 exceeded the

10-year average of 1.13 mn sq m (12.2 mn sq ft). It

is important to note that the statistical decrease in

growth may be influenced by the high base effect of

2022, which had seen the second-highest volume

of transactions in its recorded history.

• Despite the slowdown in office space leasing by

third-party IT services, which accounted for 15% of

total transactions in Bengaluru in 2023 compared

to 27% in 2022, the leasing landscape in 2023 has

been influenced positively by GCC, flex, and India-

facing occupiers. GCCs players primarily focused

on manufacturing, consulting business and BFSI.

Qualcomm, Deloitte, MUFG etc., were some of the

big-ticket occupiers in 2023.

• Flex tenants emerged as the predominant

occupants of office spaces in Bengaluru in 2023.

The leasing activity by flex occupiers reached 0.35

mn sq m (3.8 mn sq ft) comprising 30.3% of the

overall transaction volume, reflecting a substantial

23% increase compared to 2022. However, the

momentum in flex space leasing that was robust

during H1 2023, tapered off in H2 2023. This shift

suggests a resurgence in occupier inclination

towards long-term leases, signaling a change

in sentiment. The headwinds faced by the tech

sector such as the anticipated slowdown in the US

economy, have diminished and there is a renewed

interest in returning to traditional office setups.

• In 2023, GCCs accounted for 30% of office space

leasing volume in Bengaluru compared to 25% in

2022. According to an EY report, India is currently

home to around 1550 GCCs, and this number is

projected to rise to approximately 2300 by 2030.

This expansion will potentially lead to a growth in

employee headcount to 4.5 mn in 2030, compared

to the current 1.9 mn. Thus, the prospective growth

in the GCC occupiers leasing space is massive

in India. Within India, Bengaluru is an attractive

market for GCC occupiers as the city is already an

established global hub, has a diverse talent pool

and a unique ecosystem comprising technology

penetration, research & development, startups,

academia and more.

• Prospective drivers of office transaction volume

in Bengaluru include tenants associated with

India-facing businesses. In 2023, India-facing

businesses constituted 25% of the total office

leasing volume in Bengaluru. The growth outlook

for businesses operating in India is highly favorable,

given the expanding consumer base, increasing

digitalization, and ongoing economic development

in the country. Notably, the business landscape in

India is experiencing significant advancements,

particularly in technology, e-commerce, healthcare,

renewable energy, and manufacturing. Amidst

this overall development, Bengaluru’s diverse

ecosystem and abundant talent pool are poised to

play a prominent role in attracting occupiers from

India-facing businesses.

• Amongst the business districts, ORR accounted for

the largest share, i.e 41% of the total office space

leasing volume in 2023. ORR continues to be an

attractive micro-market as the business district

consists of established Grade A business parks

with quality space. Owing to its attractiveness to

occupiers, along with the development of new

infrastructure such as the under construction

Blue Line metro connecting Silk Board to Hebbal,

developer sentiment continues to remain strong.

In 2023, ORR witnessed a supply infusion of 0.29

mn sq m (3.1 mn sq ft) primarily in the existing tech

parks backed by prominent Grade A developers.

• PBD East registered 23% of the transactions in

2023. From a mere 10% leasing share in 2017,

the demand for office space in this region has

significantly increased in the last few years. The

recent operation of elevated Purple Line metro

corridor connecting K R Puram and Whitefield

has enhanced connectivity in the micro-market,

boosting occupier interest in this micro-market. To

capitalize on this growing occupier interest, PBD

East witnessed a larger share of supply infusion in

the city, amounting to 0.47 mn sq m (5.1 mn sq ft),

equivalent to 30% of the total new supply infusion

in 2023.

• PBD North stands out as the most rapidly

expanding micro market, demonstrating vigorous

growth to meet the increasing real estate demands

of Bengaluru city. Despite recording 0.09 mn sq

m (1.0 mn sq ft) in office transactions in 2023,

PBD North has attracted considerable leasing

interest from occupiers. Notably, some of the most

substantial transactions in the Bengaluru market

in 2023 were conducted in PBD North, involving

tenants like HDFC Bank, Yenepoya University,

MUFG, and others.

• Large scale infrastructure investment such as the

expansion of Kempegowda International Airport

(KIA), and the construction of phase 2 and 3 Blue

Line metro connecting KIA with the rest of the

city has encouraged developers to acquire large

land banks in the region and develop high scale

tech parks in this cluster. The office stock in this

region has increased from 0.51 mn sq m (5.5 mn

sq ft) in 2019 to 1.4 mn sq m (15 mn sq ft) currently,

with a maximum concentration by the Grade A

developers. The micro market has quality A Grade

office supply developed by prominent developers

such as Brigade Developers, L&T, Bhartiya Urban,

Embassy etc. Additionally, 0.70 mn sq m (8 mn

sq ft) of new office supply is under construction

by developers such as CapitaLand, Prestige,

Salarpuria Sattva etc. to be completed tentatively

by 2025. Improved connectivity, along with quality

workspace, would undoubtedly boost occupier

interest in this micro-market.

• Overall, Bengaluru has witnessed new supply

infusion of 1.24 mn sq m (13.4 mn sq ft) in 2023

with an accumulated stock of 20 mn sq m (215 mn

sq ft). Due to subdued demand, the vacancy level

increased by 100 bps to 15.1% in 2023 compared

to a year ago and the market contains adequate

inventory to fulfill occupier demand in the near

future.

• The average transacted rentals in Bengaluru grew

by 6.6% YoY to INR 930/sq m/month (INR 86.4/

sq ft/month) in 2023. Significant rental growth

was predominantly observed in PBD East and the

ORR micro markets. The development of transport

infrastructure has heightened the occupier’s

interest in both these micro-markets. Although the

demand has been moderate, the growing occupier

interest and the quality supply in Bengaluru has

driven rentals upward in the market. In general,

barring the short-term discrepancies, Bengaluru’s

office market fundamentals remain strong. The

acceleration of return to office by firms and the

growth in India facing businesses along with stable

business inflow from the western developed

markets into India, should support the growth in the

office market demand in the near term.

INDIA REAL ESTATE - BENGALURU

CBD & Off CBD

SBD

PBD East

ORR

PBD South

PBD North

PBD West

04%

04%

33%

38%

15%

05%

0%

07%

07%

09%

45%

16%

15%

01%

27%

17%

27%

31%

19%

37%

27%

15%

India Facing

Third party

IT Services

Flex

Global Capability

Centres

Source: Knight Frank Research

H2 2022

H2 2022

H2 2023

H2 2023

H1 2017

H2 2017

H1 2018

H2 2018

H1 2019

H2 2019

H1 2020

H2 2020

H1 2021

H2 2021

H1 2022

H2 2022

H1 2023

H2 2023

16%

14%

12%

10%

8%

6%

4%

2%

0

INR per sq m

4.0%

3.0%

3.5%

4.0%

4.0%

4.8%

6.5%

9.3%

11.3%

13.0%

12.3%

14.1%

14.5%

15.1%

BUSINESS DISTRICT CLASSIFICATION

Micro market Locations