CORPORATE

INCOME TAX

Most Large Profitable

U.S. Corporations

Paid Tax but Effective

Tax Rates Differed

Significantly from the

Statutory Rate

Report to the Ranking Member,

Committee on the Budget,

U.S. Senate

March 2016

GAO-16-363

United States Government Accountability Office

United States Government Accountability Office

Highlights of GAO-16-363, a report to the

Ranking Member

, Committee on the Budget,

U.S. Senate

March 2016

CORPORATE INCOME TAX

Most Large Profitable U.S. Corporations Paid Tax but

Effective Tax Rates

Differed Significantly from the

Statutory Rate

Why GAO Did This Study

Congress and the administration

continue to express interest in

reforming the U.S. corporate income

tax and the rate at which U.S.

corporations’ income is taxed.

Currently, the top statutory corporate

income tax rate is 35 percent. GAO’s

2013 report on corporate ETRs found

that in tax year 2010, whether for all

large corporate filers or only profitable

ones, the average ETRs were

significantly below the statutory rate.

To provide an update, GAO was asked

to assess the extent to which U.S.

corporations pay federal income tax

and the percentage that had no federal

income tax liability. In this report, GAO

estimates (1) the percentage of all and

large corporations that had no federal

income tax liability and (2) average

ETRs based on financial statement

reporting and tax reporting. To conduct

this work, GAO reviewed economic

literature, analyzed IRS data for tax

years 2006 to 2012 (the most recent

data available), including the financial

and tax information that large

corporations report on Schedule M-3,

and interviewed Internal Revenue

Service (IRS) officials and subject

matter experts.

What GAO Recommends

GAO does not make recommendations

in this report. GAO provided a draft of

this report to IRS for review and

comment. IRS provided technical

comments, which were incorporated,

as appropriate.

What GAO Found

In each year from 2006 to 2012, at least two-thirds of all active corporations had

no federal income tax liability. Larger corporations were more likely to owe tax.

Among large corporations (generally those with at least $10 million in assets)

less than half—42.3 percent—paid no federal income tax in 2012. Of those large

corporations whose financial statements reported a profit, 19.5 percent paid no

federal income tax that year. Reasons why even profitable corporations may

have paid no federal tax in a given year include the use of tax deductions for

losses carried forward from prior years and tax incentives, such as depreciation

allowances that are more generous in the federal tax code than those allowed for

financial accounting purposes. Corporations that did have a federal corporate

income tax liability for tax year 2012 owed $267.5 billion.

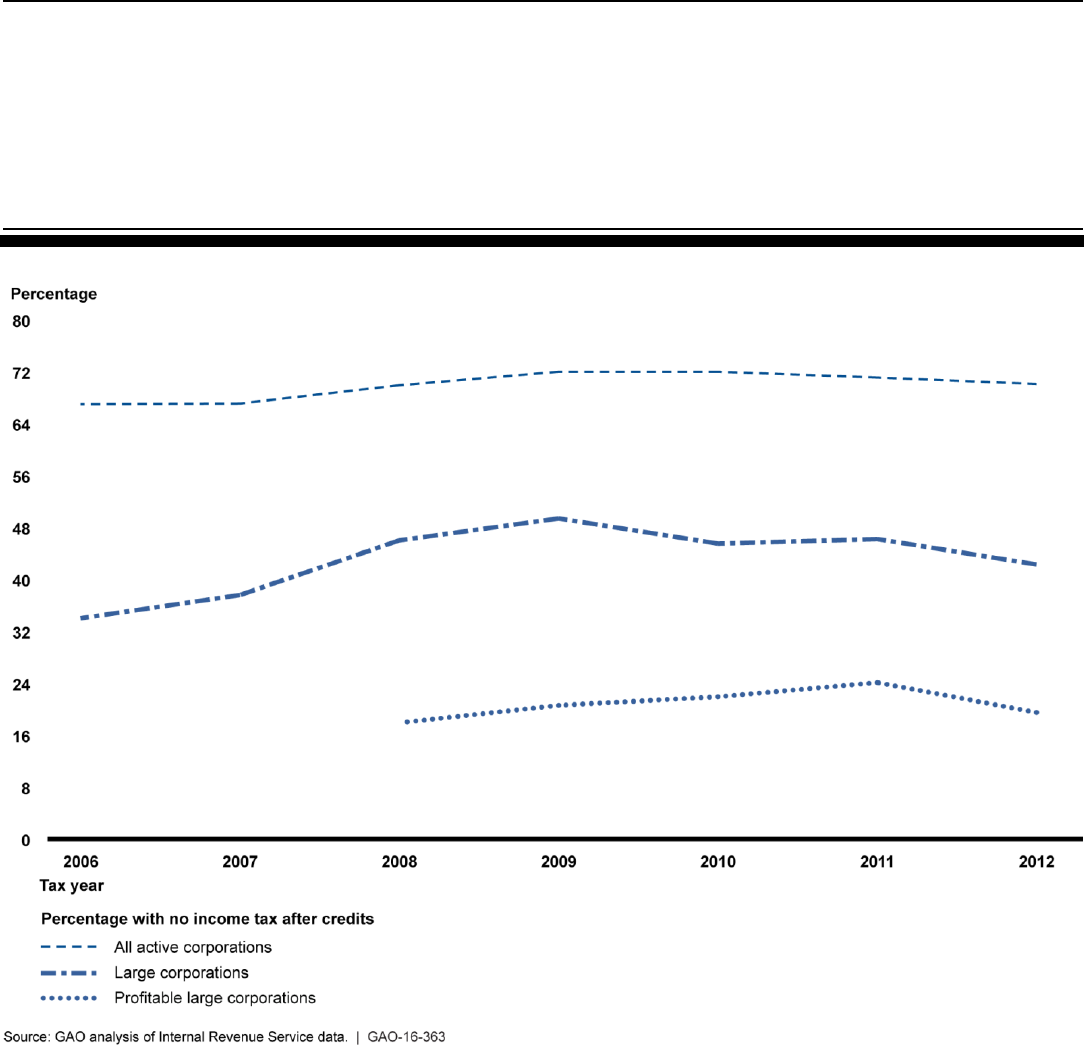

Percentage of Corporations That Reported No Tax Liability after Tax Credits,

Tax Years 2006 to 2012

These reasons also explain why corporate effective tax rates (ETR) can differ

substantially from statutory tax rates. ETRs attempt to measure taxes paid as a

proportion of economic income, while statutory rates indicate the amount of tax

liability (before any credits) relative to taxable income, which is defined by tax law

and reflects tax benefits built into the law. The statutory tax rate on net corporate

income ranges from 15 to 35 percent, depending on the amount of income

earned. For tax years 2008 to 2012, profitable large U.S. corporations paid, on

average, U.S. federal income taxes amounting to about 14 percent of the pretax

net income that they reported in their financial statements (for those entities

included in their tax returns).

When foreign and state and local income taxes are included, the average ETR

across all of those years increases to just over 22 percent. GAO also computed

ETRs that combine large profitable corporations and those large corporations

with current year losses, which pay little if any actual tax. Over tax years 2008 to

2012, all large corporations—profitable and those that reported current year

losses—paid 25.9 percent of their pretax net income in U.S. federal income

taxes, and 40.1 percent when foreign and state and local taxes are included.

Including corporations with losses results in a more comprehensive estimate, but

makes the results difficult to interpret because ETR is not meaningful for a

corporation in a year in which it has a net loss. GAO could not examine the

variation in ETRs across corporations with the aggregated data available,

although GAO’s prior work suggests that ETRs are likely to vary considerably.

View GAO-16-363. For more information,

contact

Jessica Lucas-Judy at (202) 512-

9110

or

LucasJudyJ@gao.gov.

Page i GAO-16-363 Corporate Income Tax

Letter 1

Background 4

In Each Year from 2006 to 2012, Most Corporations Had No

Federal Income Tax Liability, but a Majority of Large

Corporations Did 10

Average ETRs for Large Corporations, Which Differed

Significantly from Their Statutory Rates, Increased Slightly from

2010 to 2012 13

Agency Comments and Our Evaluation 19

Appendix I Selected Issues Relating to the Calculation of Effective Corporate Income

Tax Rates 20

The Inclusion of Corporations with Losses in Effective Tax Rate

Estimates 20

Calculating Worldwide Effective Tax Rates 23

Appendix II Summary of Selected Past Estimates of Average Effective Tax Rates

Based on Financial Statement Data 27

Appendix III Number and Percentage of U.S. Corporations with No Federal Income

Tax Liability from Tax Years 2006 to 2012 31

Appendix IV Average Federal and Worldwide Effective Tax Rates for Varying

Populations of Large Corporations (Schedule M-3 Filers) 33

Appendix V GAO Contact and Staff Acknowledgments 35

Tables

Table 1: Example of How Losses Can Distort Effective Tax Rate

Estimates 21

Table 2: Alternative Calculations of Corporate Effective Tax Rates

for Profitable Large Corporations (Schedule M-3 Filers),

Incorporating Net Operating Loss Deductions (NOLD),

Tax Years 2008 to 2012 22

Contents

Page ii GAO-16-363 Corporate Income Tax

Table 3: Number and Percentage of All Corporations With No Tax

Liability After Credits, Tax Years 2006 through 2012 31

Table 4: Number and Percentage of All and Profitable Large

Corporations (Schedule M-3 filers) with No Federal Tax

Liability After Credits, Tax Years 2006 through 2012 32

Table 5: Average Effective Tax Rates for Profitable Large

Corporations (Schedule M-3 Filers), Tax Years 2008

through 2012 33

Table 6: Average Effective Tax Rates for All Large Corporations

(Schedule M-3 Filers), Tax Years 2006 through 2012 34

Figures

Figure 1: Federal Tax Revenues as a Percentage of Gross

Domestic Product, 1950 to 2014 (2015 to 2020

Projected) 6

Figure 2: Percentage of Corporations That Reported No Tax

Liability after Credits, Tax Years 2006 to 2012 12

Figure 3: Average Federal and Worldwide Effective Tax Rates for

Profitable Large Corporations (Schedule M-3 Filers), Tax

Years 2008 through 2012 15

Figure 4: Average Federal and Worldwide Effective Tax Rates for

All Large Corporations (Schedule M-3 Filers), Tax Years

2006 through 2012 18

Figure 5: Average Effective Tax Rates for Selected Studies on

U.S. Companies, Using Worldwide Pretax Net Book

Income 29

Page iii GAO-16-363 Corporate Income Tax

Abbreviations

ETR Effective Tax Rate

IRC Internal Revenue Code

IRS Internal Revenue Service

NOLD Net Operating Loss Deduction

This is a work of the U.S. government and is not subject to copyright protection in the

United States. The published product may be reproduced and distributed in its entirety

without further permission from GAO. However, because this work may contain

copyrighted images or other material, permission from the copyright holder may be

necessary if you wish to reproduce this material separately.

Page 1 GAO-16-363 Corporate Income Tax

441 G St. N.W.

Washington, DC 20548

March 17, 2016

The Honorable Bernard Sanders

Ranking Member

Committee on the Budget

United States Senate

Dear Senator Sanders:

Congress and the administration continue to debate how to reform the

U.S. corporate income tax. One focus of this discussion is the rate at

which U.S. corporations’ income should be taxed—currently, the top

federal statutory corporate income tax rate is 35 percent. As policymakers

debate this issue, it will be helpful to also have an understanding of the

average effective tax rate (ETR) for corporations, which equals the

amount of income tax corporations pay divided by their pretax income.

ETRs are more appropriate measures of corporate tax burdens than

statutory rates because ETRs reflect the combined effects of exemptions,

deferrals, tax credits, and other tax benefits. Our previous report on

corporate ETRs found that in 2010, whether for all large corporations or

only profitable ones, the average ETRs were significantly below the

statutory rate.

1

As Congress continues discussions on corporate tax reform and what

burden corporations should bear, you asked us to assess the extent to

which U.S. corporations pay federal income tax and the percentage that

had no federal income tax liability. In this report, we estimate (1) the

percent of all corporations and large corporations that had no federal

income tax liability in each year for tax years 2006 to 2012, and (2) the

average corporate effective tax rates for large corporations based on

financial statement reporting and tax reporting for tax years 2006 to

2012.

2

1

GAO, Corporate Income Tax: Effective Tax Rates Can Differ Significantly from the

Statutory Rate, GAO-13-520 (Washington, D.C.: May 30, 2013).

2

For the purposes of this report, we refer to corporations that filed a Schedule M-3 as

large corporations. In general, corporations with $10 million or more in assets are required

to file a Schedule M-3.

Letter

Page 2 GAO-16-363 Corporate Income Tax

To estimate the number and percentage of corporations that had no

federal income tax liability, we analyzed data on the number of

corporations with and without total income tax after credits for all

corporations from the Internal Revenue Service’s (IRS) Corporation

Income Tax Returns Complete Report, as well as for the population of

large corporations that filed Schedules M-3.

3

The Schedule M-3

reconciles income and expense amounts that corporations report for

financial statement purposes with amounts they report for tax purposes,

and is the data source we used for analyzing ETRs, as described below.

We report data for all corporations for tax years 2006 to 2012, for all

Schedule M-3 filers for tax years 2006 to 2012, and for profitable

Schedule M-3 filers for tax years 2008 to 2012. These were the most

recent estimates available at the time of our work and are subject to

sampling errors.

4

To report what available data indicate about the difference between

average effective tax rates based on financial statement reporting versus

those based on tax reporting, we computed a variety of such rates using

income and expense data that large corporations report on the Schedules

M-3 that they file with IRS. These data, which the joint Department of the

Treasury-IRS M-3 First Look Team compiles for a large sample of

taxpayers, allowed us to compare and estimate U.S. and worldwide

effective tax rates on worldwide income of entities included in the federal

income tax return, first using only financial statement data, then using

only data reported for tax purposes, and finally using income data from

financial statements and tax return data for the amount of taxes paid.

3

See IRS Statistics of Income, Corporation Income Tax Returns Complete Report. Data

on all corporations include active corporations filing tax forms 1120 (U.S. Corporation

Income Tax Return), 1120-L (U.S. Life Insurance Company Income Tax Return), 1120-PC

(U.S. Property and Casualty Insurance Company Income Tax Return), and 1120-F (U.S.

Income Tax Return of a Foreign Corporation). Data are not included for certain “pass-

through” entities, which file on forms 1120-REIT (U.S. Income Tax Return for Real Estate

Investment Trusts), 1120-RIC (U.S. Income Tax Return for Regulated Investment

Companies), and 1120S (U.S. Income Tax Return for an S Corporation). The amount for

total income tax after credits includes the following: income tax, personal holding company

tax, recapture and other taxes, alternative minimum tax, branch tax (Form 1120-F), tax

from page 1, line 5 (Form 1120-PC), and adjustments to income tax, and to total tax.

4

Data compiled by IRS Statistics of Income are based on a stratified random sample of

corporate income tax returns. See https://www.irs.gov/uac/SOI-Tax-Stats-Corporation-

Complete-Report. The number of noncertainty corporations in the Schedule M-3 sample is

over 10,000 for each year after 2004.

Page 3 GAO-16-363 Corporate Income Tax

The financial statement data we used from the Schedules M-3 for

worldwide income and tax expenses—including federal, foreign, and U.S.

state and local income taxes—are limited to the entities that are included

in the U.S. taxpayer’s federal tax return. Consequently, the scope of the

corporate entities included in our analysis can differ from the scope of the

entities included in publicly filed financial statements because not all

foreign entities represented in those statements are included in a federal

tax return.

5

In addition, our estimates of effective tax rates remain limited

to corporations with assets of $10 million or more because those are the

ones that filed a Schedule M-3. Our analysis covers all large corporations

for tax years 2006 to 2012 and profitable large corporations (i.e., those

that did not report net losses in their financial statements) for tax years

2008 to 2012.

6

The Schedule M-3 data were available to us in aggregated

form and therefore we were not able to provide any information on the

distribution of ETRs across individual corporations; instead, we estimated

ETRs averaged over the populations of all corporations and profitable

corporations (see appendix I for a detailed discussion of several

limitations of the data for purposes of estimating ETRs).

We also reviewed and summarized the relevant economic and accounting

literature on ETRs since March 2013 (the end date of the literature review

in our previous report).

7

We also discussed our methodology with subject

matter experts from the Congressional Research Service and from the

Department of the Treasury, each of whom has written on effective tax

rates. Based on these discussions, we supplemented our analysis where

we deemed appropriate and possible based on available data.

5

As we discuss in appendix I, this scope limitation, combined with the complexity of U.S.

tax rules pertaining to foreign income, complicates the computation of worldwide ETRs.

6

IRS has compiled data separately for corporations that had nonnegative values for net

income on their financial statements for only tax years 2008 to 2012. The Schedule M-3

data are drawn from IRS’s Statistics of Income division’s annual stratified random samples

of corporate tax returns. The results we present based on these samples are subject to

sampling error. We do not have the detailed information needed to estimate the size of the

sampling error; however, we believe these errors are negligible because a significant

proportion of the returns with Schedules M-3 attached, which are a part of the Schedule

M-3 dataset are sampled at a 100 percent rate and the remaining M-3 filers are sampled

at rates of 27 percent or more. Those returns that were sampled at the 100 percent rate

accounted for 99 percent of the total assets of all returns filed with a Schedule M-3 for tax

year 2012.

7

See appendix II for a summary of past studies that used financial statement data to

estimate average effective tax rates.

Page 4 GAO-16-363 Corporate Income Tax

To assess the reliability of the data and estimates, we reviewed agency

documentation, interviewed agency officials, and reviewed our prior

reports that have used the data and estimates. While there are limitations

to the data provided on the Schedules M-3 and general reporting

problems with tax return data, we determined that the data were

sufficiently reliable to meet our reporting objectives.

We conducted our work from August 2015 to March 2016 in accordance

with all sections of GAO’s Quality Assurance Framework that are relevant

to our objectives. The framework requires that we plan and perform the

engagement to obtain sufficient and appropriate evidence to meet our

stated objectives and to discuss any limitations in our work. We believe

that the information and data obtained, and the analysis conducted,

provide a reasonable basis for any findings and conclusions in this

product.

The base of the federal corporate income tax includes net income from

business operations (receipts, minus the costs of purchased goods, labor,

interest, and other expenses). It also includes net income that

corporations earn in the form of interest, dividends, rent, royalties, and

realized capital gains. The statutory rate of tax on net corporate income

ranges from 15 to 35 percent, depending on the amount of income

earned.

8

The United States taxes the worldwide income of domestic

corporations, regardless of where the income is earned, but allows a

8

26 U.S.C. § 11. In addition, present law imposes an alternative minimum tax on certain

corporations to the extent that their minimum tax liability exceeds their regular tax liability.

26 U.S.C. § 56. In general, the alternative minimum tax applies a lower tax rate to a

broader tax base. Specifically, the regular tax base is increased for alternative minimum

tax purposes by adding back certain items treated as tax preferences and disallowing

certain deductions and credits. Also, marginal rates are higher over limited income ranges

to recapture the benefits of the rates below 35 percent.

Background

Corporate Income Tax

System

Page 5 GAO-16-363 Corporate Income Tax

foreign tax credit for certain taxes paid to other countries.

9

The timing of

the tax liability depends on several factors. For example, income earned

by foreign subsidiaries is generally not taxed until it is distributed—such

as in the form of a dividend—to the U.S. parent corporation.

Another

important element of the U.S. corporate income tax system is the

treatment of losses incurred in a given tax year. If a corporation has a net

operating loss in a particular year, the corporation may carry those losses

forward into future tax years or backward into prior tax years.

10

When

carried back, corporations can deduct those losses from taxable income

and are eligible for a refund equal to the difference between previously

paid taxes and taxes owed after deducting the current year’s loss. Losses

carried forward may be used to reduce future taxable income and tax

liabilities, but cannot be used to reduce taxable income below zero. As a

result, a corporation with a substantial loss in a particular year may claim

deductions stemming from that loss over a number of years in the future.

While corporate income taxes have declined markedly as a share of

gross domestic product since the 1950s, they remain an important source

of federal revenue. In fiscal year 2014, corporate income tax revenue as a

share of gross domestic product was 1.9 percent and totaled $321 billion.

By comparison, revenues from individual income taxes and from social

insurance and retirement receipts (e.g., Medicare) were $1.4 trillion and

$1.02 trillion, respectively, in that year. Corporate income taxes

accounted for 10.6 percent of all federal revenues in 2014, up from 6.6

percent in 2009, but still below their recent high of 14.7 percent in 2006

(see figure 1).

11

9

Taxable income is, in general, total income, including taxable income from foreign

sources, minus deductions such as for salaries and wages, depreciation, and net

operating loss carryovers. The federal income tax owed is determined by multiplying this

income by the applicable tax rate and then subtracting any tax credits, including the

foreign tax credit, for which the taxpayer may be eligible.

10

26 U.S.C. §172. Corporations may carry losses back to two prior years’ taxable income

or forward for up to 20 years.

11

Office of Management and Budget, Historical Tables, Budget of the United States

Government, Fiscal Year 2016 (Washington, D.C.: February 2015).

Page 6 GAO-16-363 Corporate Income Tax

Figure 1: Federal Tax Revenues as a Percentage of Gross Domestic Product, 1950

to 2014 (2015 to 2020 Projected)

Businesses operating as publicly traded corporations in the United States

are required to report the income they earn and the expenses (including

taxes) they incur each year according to two separate standards. First,

corporations must produce financial statements in accordance with

generally accepted accounting principles in order to provide certain

information to investors and creditors. The income and expense items

reported in these statements are commonly known as book items.

Second, U.S. corporations must file corporate income tax returns on

which they report income, expenses, and tax liabilities, according to rules

set out in the Internal Revenue Code (IRC) and associated Department of

the Treasury regulations. While the IRC generally requires that a

corporation’s taxable year and overall method of accounting conform to

those standards used for financial reporting purposes, specific differences

are permitted (and, in some cases, required). These are known as book-

tax differences. One important source of book-tax differences is

incentives for investment and other specific activities that Congress has

chosen to incorporate into the tax code. For example, the bonus

Financial and Tax

Reporting Requirements

for Corporations

Page 7 GAO-16-363 Corporate Income Tax

depreciation allowance permits businesses to depreciate qualified capital

assets much more rapidly than they are permitted to do under financial

accounting. As a result, taxable income will be reduced by a greater

amount than will book income for the year in which the qualified

investment is made. However, in later years (until the asset is completely

depreciated), book income will be reduced by greater amounts than will

taxable income.

Corporations with assets that equal or exceed $10 million are required to

report these book-tax differences to IRS on the Schedule M-3 of their

income tax returns.

12

In tax year 2012, 42,301 corporations filed a

Schedule M-3 return. Of these, 27,546 were profitable according to their

financial statements. By comparison, in that same year, there were

almost 1.62 million active corporations, which include Schedule M-3

filers.

13

A Schedule M-3 filer is required to report the worldwide income of

the entity represented in its financial statements and then follow a well-

defined series of steps—subtracting out income and losses of foreign and

U.S. entities that are included in the financial statements but not in

consolidated tax returns; adding in the income and losses of entities that

are included in consolidated tax returns but not in financial statements;

and making other adjustments to arrive at the book income of entities

included in the federal tax return.

Effective tax rates on corporate income can be defined in several ways,

each of which provides insights into a different issue. This report focuses

on average corporate effective tax rates, which are generally computed

as the ratio of taxes paid or tax liabilities accrued in a given year over the

12

This requirement became effective in December 2004. Prior to 2004, corporations were

required to reconcile their book net income with tax net income reporting on Schedule M-

1. However, concern over the growing difference observed between pretax book net

income and tax net income, as well as the lack of detail available from the Schedule M-1

on the sources of these differences, led to the development of the more extensive

reporting now required on Schedule M-3.

13

IRS Statistics of Income, Corporation Income Tax Returns Complete Report, data on all

active corporations include corporations filing tax forms 1120 (U.S. Corporation Income

Tax Return), 1120-L (U.S. Life Insurance Company Income Tax Return), 1120-PC (U.S.

Property and Casualty Insurance Company Income Tax Return), and 1120-F (U.S.

Income Tax Return of a Foreign Corporation). Schedule M-3 data include only

noninsurance corporations filing tax Form 1120. The Schedule M-3 data are a subset of

the data from the Corporation Income Tax Returns Complete Report.

Effective Tax Rates

Page 8 GAO-16-363 Corporate Income Tax

net income the corporation earned that year.

14

Average effective tax rates

attempt to measure taxes paid as a proportion of economic income. By

contrast, the marginal effective tax rate focuses on the tax burden

associated with a specific investment (usually over the full life of that

investment), and thus is a better measure of the effects that taxes have

on incentives to invest. Meanwhile, statutory rates determine the amount

of tax liability (before any credits) relative to taxable income, which is

defined by tax law and reflects tax benefits and subsidies built into the

law. The highest corporate statutory tax rate of 35 percent applies to most

large U.S. corporations in years that they report positive amounts of

taxable income.

To estimate average effective tax rates, analysts need two components:

1. The measure of tax liabilities to be used as the numerator. Common

measures include

• current book tax expense, including either only federal taxes or

worldwide taxes—federal, foreign, and U.S. state and local income

taxes paid by entities included in the federal tax return,

• total book tax expense, which includes the sum of current and

deferred taxes (again, either federal only or worldwide), and

14

Our average effective tax rates (ETRs) are averages in multiple senses. First, the rate

reflects the average tax paid on every dollar of a corporation’s net income (as opposed to

the tax on the marginal dollar of income earned). Second, given that we had access to

only aggregated IRS data, our ETR estimates represent averages across all of the

corporations in our different populations of analysis (either all Schedule M-3 filers or the

subpopulation of profitable Schedule M-3 filers). Finally, we also compute averages of

these ETRs over a number of years. To do so, we sum the aggregate tax expense and

pretax income amounts over the years reported. For all Schedule M-3 filers, we do so for

tax years 2006 to 2012. For profitable Schedule M-3 filers, we do so for tax years 2008 to

2012. The multiyear averages for profitable large corporations include a population of

corporations for each year for only those which were profitable in that year; they are not

averages for corporations that were profitable in every year.

Page 9 GAO-16-363 Corporate Income Tax

• actual tax paid, which is what corporations report as their income tax

liability after credits.

15

2. The measure of income to be used as the denominator. The typical

measure of income for effective tax rate estimates based on financial

statements has been some variant of pretax net book income, which

we use for all of our ETR estimates.

15

Deferred taxes represent estimated taxes that will be paid (or refunded) in a future year

as timing differences between book and tax reporting reverse themselves and unused

losses and credits that have been carried forward are recognized. Taxes that are reported

as deferred in one tax year are included in current tax expenses in future years (which is

why some studies choose to exclude deferred taxes from their ETR measures). Our

measure of actual worldwide taxes paid by entities included in the federal tax return

equals the sum of total federal income tax after credits, the amount of state and local

income tax deduction claimed on the return, and the foreign tax credit. As explained in

appendix I, we had to estimate the foreign tax credit for certain years.

Page 10 GAO-16-363 Corporate Income Tax

In each tax year from 2006 to 2012 at least two-thirds of active U.S.

corporations had no federal income tax liability after credits (see figure 2).

The percentage of such corporations with no tax liability remained

relatively stable, ranging between 67 and 72 percent during that

timeframe. In tax year 2012, 70.1 percent of the 1.62 million active

corporations had no federal income tax liability with the peak coming in

2009 near the end of the recession.

16

Among large corporations for 2012,

less than half—42.3 percent, or 17,882 returns—had no federal income

tax after accounting for tax credits.

17

Among profitable large corporations,

19.5 percent, or 5,359 returns, had no federal income tax liability in tax

year 2012. Corporations that did have a federal corporate income tax

liability for tax year 2012 owed $267.5 billion.

Corporations may pay no federal income tax for a number of reasons.

One important reason is that in each of the years from 2008 to 2012,

between approximately 49 to 54 percent of all active corporations had

negative net tax income based on federal tax accounting rules. Large

corporations were less likely to have incurred losses. In each year during

that period, between 34.9 percent and 44.2 percent of Schedule M-3 filers

had negative net tax income.

18

A second reason is that other corporations

16

Schedule M-3 filers generally have assets of $10 million or more. These filers are also

included in the top line of figure 2, showing all active corporations. When we subtracted

this subpopulation of Schedule M-3 filers out of that overall population, we found that the

remaining corporations (essentially those with assets of less than $10 million) had almost

the same likelihood of paying tax as the overall population. For example, in tax year 2012,

70.9 percent of corporations excluding Schedule M-3 filers had no federal tax liability after

credits compared to 70.1 percent for all corporations. See appendix III. We also divided

the subpopulation of Schedule M-3 filers into those with assets of less than $50 million

and those with assets of $50 million or more. We found that the group with lower assets

was slightly more likely to have paid no tax than the group with larger assets. For

example, in tax year 2012, 44.9 percent of corporations with total assets between $10

million and $50 million had no federal income tax liability, while 38.7 percent of

corporations with $50 million or more in total assets had no tax liability.

17

For purposes of this report, we refer to corporations which filed a Schedule M-3 as large

corporations. In general, corporations with $10 million or more in assets are required to file

a Schedule M-3. The percent of these corporations that had no federal income tax liability

was similar for all active corporations with at least $10 million in assets.

18

Many of these corporations may have had losses under both book and tax accounting

rules. In other cases, corporations may have been profitable under book accounting rules,

but had no net tax income because tax incentives, such as the bonus depreciation

allowance mentioned earlier, which could eliminate any positive net tax income without

affecting net book income. We are not able to quantify the effect that these incentives had

on the absence of tax liabilities.

In Each Year from

2006 to 2012, Most

Corporations Had No

Federal Income Tax

Liability, but a Majority

of Large Corporations

Did

Page 11 GAO-16-363 Corporate Income Tax

had positive net tax income that was completely offset by net operating

loss deductions (NOLD) carried forward from prior tax years. In each year

from 2008 to 2012, approximately 15 to 19 percent of all active

corporations had their income completely offset in this manner.

19

Similar

percentages of all and profitable large corporations had their income

completely offset by NOLDs from 2008 to 2012. The use of federal tax

credits appears to have had little effect on the number of corporations that

paid no tax in each year (this does not imply that these credits did not

significantly reduce the amount of tax that some corporations paid). For

all active corporations, federal tax credits increased the percentage of

corporations not paying tax by less than one percentage point each year.

Much the same was true for all and profitable large corporations (see

appendix III).

19

Any income remaining after the use of net operating loss deductions is known as taxable

income. Some corporations with no taxable income for regular income tax purposes may,

nevertheless, pay income tax in the form of the alternative minimum tax or one of the

other less common taxes included as part of total federal income tax.

Page 12 GAO-16-363 Corporate Income Tax

Figure 2: Percentage of Corporations That Reported No Tax Liability after Credits, Tax Years 2006 to 2012

Note: IRS Statistics of Income Corporation Income Tax Returns Complete Report data on all active

corporations include corporations filing tax forms 1120 (U.S. Corporation Income Tax Return), 1120-L

(U.S. Life Insurance Company Income Tax Return), 1120-PC (U.S. Property and Casualty Insurance

Company Income Tax Return), and 1120-F (U.S. Income Tax Return of a Foreign Corporation) while

Schedule M-3 data include only noninsurance corporations filing tax Form 1120. The Schedule M-3

data are a subset of the data from the Corporate Complete Report. In general, corporations with $10

million or more in assets are required to file a Schedule M-3.

Page 13 GAO-16-363 Corporate Income Tax

For tax year 2012, the actual U.S. federal income taxes paid by profitable

large corporations amounted to 16.1 percent of the income that those

corporations reported in their financial statements (for those entities

included in their tax returns); this federal effective tax rate averaged 14

percent from tax years 2008 to 2012 (see the first panel of figure 3).

20

This tax rate is slightly lower than the 17.3 percent rate based on the

current federal book tax expense, and the 18.5 percent rate based on

total federal book tax expenses for tax year 2012, which includes current

and deferred federal book tax expenses. Each averaged 15.3 percent and

18.6 percent, respectively, from tax years 2008 to 2012.

21

The subject matter experts with whom we spoke suggested it would be of

interest to estimate what profitable large corporations would have paid in

the current year if one did not take into account the deductions that

corporations are allowed to take for losses carried forward from prior

years. Adjusting for these net operating loss deductions (NOLD) raises

the effective rate of actual U.S. federal taxes paid to 19.5 percent in tax

20

For purposes of this report, we refer to corporations which filed a Schedule M-3 as large

corporations. In general, corporations with $10 million or more in assets are required to file

a Schedule M-3. See appendix IV for all effective tax rates we calculated.

21

For the sake of comparison with our May 2013 report, we also presented actual taxes

paid over taxable income; however, that measure is not a typical effective tax rate

because the income measure is reduced by various tax preferences. See GAO-13-520. All

of the rates we discuss above are significantly lower than the 24.6 percent rate of actual

taxes paid as a percentage of taxable income instead of pretax net book income.

Average ETRs for

Large Corporations,

Which Differed

Significantly from

Their Statutory Rates,

Increased Slightly

from 2010 to 2012

Average ETRs for Large

Profitable Corporations

Were Well Below Statutory

Rates, Even When

Deductions for Prior-Year

Losses Were Excluded

Page 14 GAO-16-363 Corporate Income Tax

year 2012 and averaged 16.5 percent from tax years 2008 to 2012.

22

These rates were 2.6 percentage points higher than the unadjusted rates

(see figure 3).

Even with the adjustment for NOLDs, these ETRs remain well below the

top statutory federal income tax rate of 35 percent for a number of

reasons. First, to the extent that corporations have foreign-source income

on which they have paid tax to foreign governments, their U.S. federal

income tax will be reduced by the foreign tax credit. Also, as noted earlier,

tax incentives, such as the bonus depreciation allowance, will cause

taxable income (on which the actual federal tax is based) to be less than

book income (which is the denominator of the ETR). Other types of

differences between financial statement and tax accounting can have the

same effect.

22

To make this adjustment, we multiplied the highest corporate statutory rate of 35 percent

by the NOLD amount claimed by profitable large corporations (Schedule M-3 filers) and

added that amount to the numerator of our measure. The result shows what the ETR on

current-year income would be if no NOLD had been available to offset any of that income.

Another approach would be to subtract the NOLD from the denominator, which would

show the ETR on the portion of current-year income that was not offset by prior-year

losses. Using this alternative approach, the federal “Actual taxes paid” ETR is 17.8

percent for tax year 2012 and averaged 15.1 percent from tax years 2008 to 2012. No

adjustment is required for losses that are carried backward because the tax return data

that we use do not include deductions for those losses.

Page 15 GAO-16-363 Corporate Income Tax

Figure 3: Average Effective Tax Rates for Profitable Large Corporations (Schedule M-3 Filers), Tax Years 2008 through 2012

Notes: The worldwide effective tax rates are based on the worldwide income and taxes—including

federal, foreign, and U.S. state and local income taxes—of entities included in the federal tax return.

The second panel of figure 3 presents ETRs that incorporate the

worldwide taxes of entities included in the federal tax returns of Schedule

M-3 filers. These worldwide ETRs for profitable large corporations ranged

between 3.5 and 8.7 percentage points higher than comparable federal

ETRs. For example, from tax years 2008 to 2012, the actual worldwide

taxes paid by profitable large corporations averaged 22.2 percent of the

income that those corporations reported in their financial statements (for

those entities included in their tax returns). As was the case with the

federal ETRs for profitable large corporations, the worldwide ETRs have

Page 16 GAO-16-363 Corporate Income Tax

increased somewhat since tax year 2010.

23

These measures do not

include income earned by foreign subsidiaries or the taxes that those

foreign subsidiaries pay, except in the cases where that income is

repatriated to U.S. corporations in the form of dividends or falls into

certain categories of income that are taxed immediately under federal tax

rules.

24

In our May 2013 report and in this report, we present ETR estimates for

all large corporations as well as for the population of profitable Schedule

M-3 filers.

25

Our estimates for profitable large corporations are not

intended to represent the tax burdens of all large corporations; their

purpose is to provide a more accurate picture of the tax burden for the

significant subpopulation of corporations that are profitable in a particular

year without the distortion caused by the losses of other corporations.

26

Profitable large corporations represented between 56 percent and 57

percent of all large corporations from 2008 through 2009; from 2010

through 2012, they represented between 64 percent and 65 percent of all

filers. Some of the past studies we identified in our May 2013 report and

during the course of this report have excluded unprofitable corporations;

others have not (see appendix II).

23

The peak in the effective tax rates based on total book tax in tax year 2011 in both figure

3 and figure 4 is due to a peak in the deferred federal tax expense in that year, which in

turn was likely due to the fact that the benefit of the bonus depreciation allowance peaked

in that year. Corporations had an added incentive to make a qualified investment in 2011,

increasing their deferred federal tax expenses in that year. In addition, investments in

2010 and 2012 were potentially artificially low because investments that might otherwise

have been made in those years would have been shifted into 2011.

24

Appendix I includes a discussion of how the complexity of U.S. tax rules pertaining to

foreign income and the limitations of the data available from Schedules M-3 complicate

the computation of worldwide ETRs.

25

GAO-13-520.

26

Appendix I includes a more detailed discussion of how losses complicate the

computation and interpretation of ETRs.

Page 17 GAO-16-363 Corporate Income Tax

In tax year 2012, all corporate returns with a Schedule M-3, including

those with current-year losses, paid actual U.S. federal income taxes

amounting to 21.2 percent of the income that they reported. Based on

current and total book tax expenses, these corporations had ETRs of 21.8

percent and 22.3 percent, respectively (see the first panel of figure 4). On

average, over tax years 2008 to 2012, all large corporations actually paid

25.9 percent of their pretax net income in U.S. federal income taxes.

The

inclusion of large corporations with losses raises federal ETRs between 3

and 15 percentage points higher than those of large profitable

corporations for years in which ETRs are calculated for both, including tax

years 2009 to 2012. This increase occurs because firms with current year

losses, which pay little if any actual tax, have a negligible effect on the

numerator of the ETR, but their losses can significantly reduce the pretax

net book income in the denominator. For example, in tax year 2009,

profitable large corporations had pretax net book income of $1.187 trillion,

while unprofitable large corporations had net current year losses of $619

billion, netting to a pretax book income of $568 billion. The inclusion of

large corporations with current year losses in that year more than doubles

the ETR based on actual federal taxes paid in comparison to the rate for

only profitable large corporations. In tax year 2008, the losses of

unprofitable large corporations more than completely offset the income of

profitable large corporations, resulting in negative pretax net book

income. Consequently, we were not able to compute ETRs for all large

corporations in that year.

From tax years 2008 to 2012, worldwide ETRs for all large corporations,

which includes federal, foreign, and state and local taxes paid by entities

included in federal tax returns, ranged between almost 5 to more than 16

percentage points greater than comparable federal ETRs for all large

corporations (see figure 4). Over those tax years, ETRs averaged 40

percent when foreign and state and local taxes are included.

The Inclusion of Large

Corporations with Current-

Year Losses Raises the

Average Effective Tax

Rates but Makes Those

Rates Difficult to Interpret

Page 18 GAO-16-363 Corporate Income Tax

Figure 4: Average Effective Tax Rates for All Large Corporations (Schedule M-3 Filers), Tax Years 2006 through 2012

Notes: The worldwide effective tax rates are based on the worldwide income and taxes—including

federal, foreign, and U.S. state and local income taxes—of entities included in the federal tax return.

We did not compute effective tax rates for all corporations for tax year 2008 because aggregate

pretax net book income was negative that year.

Page 19 GAO-16-363 Corporate Income Tax

We provided a draft of this report to the Commissioner of Internal

Revenue for review and comment. IRS provided technical comments,

which were incorporated, as appropriate.

As agreed with your office, unless you publicly announce the contents of

this report earlier, we plan no further distribution until 30 days from the

report date. At that time, we will send copies to the Chairmen and

Ranking Members of other Senate and House committees and

subcommittees that have appropriation, authorization, and oversight

responsibilities for IRS. We will also send copies of the report to the

Commissioner of Internal Revenue and other interested parties. In

addition, this report will be available at no charge on the GAO website at

http://www.gao.gov.

If you or your staff have any questions or wish to discuss the material in

this report further, please contact me at (202) 512-9110 or

[email protected]. Contact points for our Offices of Congressional

Relations and Public Affairs may be found on the last page of this report.

Key contributors to this report are listed in appendix V.

Sincerely Yours

Jessica Lucas-Judy

Acting Director, Tax Issues

Strategic Issues

Agency Comments

and Our Evaluation

Appendix I: Selected Issues Relating to the

Calculation of Effective Corporate Income Tax

Rates

Page 20 GAO-16-363 Corporate Income Tax

In this report, we present effective tax rate (ETR) estimates for both

profitable and all corporations. As we noted, the first set of estimates

provides meaningful information for an important population of firms

without the distortion caused by the losses of other corporations. The

second set of estimates covers a more comprehensive population of

firms; however, an ETR is not meaningful for a corporation in a year in

which it has a net loss. Consequently, it is not clear how to interpret

average ETRs for populations that include some corporations with net

income and others with net losses for a given year. The simplified

example in table 1 demonstrates the nature of this problem. In this

example, Corporation A is profitable in all years, while Corporation B

incurs losses in the first 2 years, which it then offsets against its income in

the third year.

1

A weighted average ETR based on the combined data for

the two corporations for all 3 years provides an accurate representation at

the aggregate level of the tax burden on income earned in those 3 years

(35 percent). However, when the time period is limited so that not all

losses can be used during the period, the estimates do not give an

accurate representation of the longer term rates. The average for the first

2 years (70 percent) overstates the burden because it does not include

the income against which Corporation B’s losses during these 2 years is

actually offset. Instead, those losses offset a completely different

corporation’s income. Conversely, the average for the last 2 years (26.3

percent) understates the burden over the 3-year period because losses

incurred outside of the 2-year period are used to reduce tax payments

during the period. The types of distortions shown in this example arise at

the beginning and end of any finite period of analysis.

1

In order to focus on the effects of loss carryforwards, we assume that there are no

differences between book and taxable income other than these carryforwards, and we

apply a statutory tax rate of 35 percent, ignoring any tax credits. Also in this example, all

losses incurred during this period are used during the period and no losses are carried

into the period from other years.

Appendix I: Selected Issues Relating to the

Calculation of Effective Corporate Income Tax

Rates

The Inclusion of

Corporations with

Losses in Effective

Tax Rate Estimates

Appendix I: Selected Issues Relating to the

Calculation of Effective Corporate Income Tax

Rates

Page 21 GAO-16-363 Corporate Income Tax

Table 1: Example of How Losses Can Distort Effective Tax Rate Estimates

Computation of weighted average effective tax rates

Year 1

Year 2

Year 3

All years

First 2 years

Last 2 years

Corporation A

Current-year net income/loss

$200

200

100

500

400

300

Loss used as a carryforward

-

-

-

-

-

-

Taxable income

200

200

100

500

400

300

Tax at 35 percent rate

70

70

35

175

140

105

A's ETR (tax/ current-year net

income)

35.0 %

35.0 %

35.0 %

35.0 %

35.0 %

35.0 %

Corporation B

Current-year net income/loss

$(100)

(100)

400

200

(200)

300

Loss used as a carryforward

-

-

(200)

-

-

-

Taxable income

-

-

200

200

-

300

Tax at 35 percent rate

-

-

70

70

-

70

B's ETR (tax/ current-year net

income)

not meaningful

not meaningful

17.5 %

35%

not meaningful

23.3 %

Corporation A and B

Aggregate

Current-year net income/loss

$100

100

500

700

200

600

Tax paid

70

70

105

245

140

175

ETR (tax/ current-year net

income)

70.0 %

70.0

21.0

35.0

70.0

29.2

Source: Hypothetical example developed by GAO. I GAO-16-363

Notes: This example and the related discussion originally appeared in an article in Tax Notes. See

James A. Wozny, “GAO Official Defends Agency Report Numbers,” Tax Notes, Nov. 25, 2013. In the

columns where the averages are computed, the losses are counted only once (either as a reduction

in the current-year income/loss line or as a carryforward, not both). For example, Corporation B’s loss

carryforward in year 3 is not included in the last column because only $100 of the losses were

incurred in the last 2 years and that portion has already reduced the current-year net income amount

in that last column.

In this report, the ETRs that we label “actual taxes paid” for profitable

corporations reflect the taxes that those corporations actually reported on

their tax returns in a particular year as a percentage of their net book

income for that year. Alternatively, there are two ways to estimate ETRs

that exclude the effect that prior-year losses have on tax payments. One

approach would be to multiply the amount of prior-year losses that

corporations deducted on their tax returns by the statutory tax rate and

then add that tax amount to the numerator of the ETR. The resulting

estimate would show what the ETR on current-year income would be if no

net operating loss deductions (NOLD) had been available to offset any of

that income. A second alternative for removing the effect of prior-year

Appendix I: Selected Issues Relating to the

Calculation of Effective Corporate Income Tax

Rates

Page 22 GAO-16-363 Corporate Income Tax

losses would be to reduce pretax net book income in the denominator by

the amount of NOLDs used in that year.

2

The estimate that results from

this approach shows the ETRs on the portion of current-year income that

was not offset by prior-year losses. As seen in table 2, compared with our

original actual taxes paid ETRs for profitable corporations, the estimates

that are adjusted for NOLDs are slightly higher. None of these ETRs for

corporations that are profitable in a given year is meant to represent the

tax burden averaged across all corporations (both profitable and

unprofitable ones).

Table 2: Alternative Calculations of Corporate Effective Tax Rates for Profitable Large Corporations (Schedule M-3 Filers),

Incorporating Net Operating Loss Deductions (NOLD), Tax Years 2008 to 2012

Original GAO Estimate of

Effective Tax Rates

Alternative 1: NOLD multiplied by 35

percent added to numerator

Alternative 2:

NOLD subtracted

from denominator

Actual U.S. federal tax paid over book

income

14%

16.5

15.1

Actual worldwide tax paid over book

income

22.2

24.6

23.8

Source: GAO analysis of IRS data for Schedule M-3 filers. I GAO-16-363

Note: The worldwide actual tax paid ETRs for profitable corporations are averages of tax-year 2010 to

2012 values because the foreign tax credit value is not available for tax years 2008 and 2009. The

worldwide effective tax rates are based on the worldwide income and taxes—including federal,

foreign, and U.S. state and local income taxes—of entities included in the federal tax return.

In commenting on our May 2013 report on ETRs, at least one person

stated that ETRs for the full population of corporations are more

appropriate for policymakers.

3

In our view, the choice of which ETR

measure to examine depends on the specific question being considered.

2

The Schedule M-3 data that we had only separate out the NOLD amount between

profitable and loss corporations for tax years 2010 through 2012. For tax years 2008 and

2009, we took the average percentage that profitable NOLD amounts made up of the total

amount reported for all corporations from tax years 2010 to 2012, and multiplied that

average percentage by the total NOLD amount for tax years 2008 and 2009, which we

then used to adjust either the numerator or denominator of our ETR estimates above. The

profitable NOLD amount accounted for 88, 78, and 83 percent of the total NOLD amount

from tax years 2010 to 2012, respectively, and averaged 83 percent over those 3 years.

3

GAO, Corporate Income Tax: Effective Tax Rates Can Differ Significantly from the

Statutory Rate, GAO-13-520 (Washington, D.C.: May 30, 2013); and Andrew B. Lyon,

“Another Look at Corporate Effective Tax Rates, 2004-2010,” Tax Notes (Oct. 21, 2013).

Appendix I: Selected Issues Relating to the

Calculation of Effective Corporate Income Tax

Rates

Page 23 GAO-16-363 Corporate Income Tax

In many cases it is more instructive to examine the distribution of ETRs

across different subpopulations of corporations.

4

With detailed taxpayer-

level data one might track individual corporations from year to year to

address timing issues relating to losses. We did not have access under

the law to such data for this report.

The scope of the data available to us from Schedule M-3 and Form 1120

limited our ability to estimate worldwide ETRs for the large corporations

(Schedule M-3 filers). As noted above, our estimated worldwide ETRs

represent the burden of taxes paid and income received by entities that

are included in federal tax returns. These measures do not include

income earned by foreign subsidiaries or the taxes that those foreign

subsidiaries pay, except in the cases where that income is repatriated to

U.S. corporations in the form of dividends or falls into certain categories

of income that are taxed immediately under federal tax rules. In the

remainder of this section, we compare the data on worldwide taxes

available to us for this report with the data we used for our previous

report.

First, we need to describe some of the relevant U.S. tax rules applying to

foreign-source income. The United States taxes domestic corporations on

their worldwide income, regardless of where it is earned. A U.S.

corporation may directly or indirectly own shares of stock of other

corporations both foreign and domestic; if the U.S. corporation owns all or

a significant number of shares of stock, it may be considered a parent

and the other corporation a subsidiary. In general, a U.S. taxpayer who

owns stock in a corporation is not taxed on income earned by the

corporation when it is earned, but taxed when it is distributed to the

taxpayer, such as in the form of dividends. When the taxpayer is a U.S.

corporation and it owns shares of a foreign corporation in a jurisdiction

with a lower corporate tax rate than that of the United States, this can

4

In an earlier study, we found considerable variation in the U.S. ETR on the domestic

income of large corporations for tax year 2004. At one extreme 32.9 percent of the

taxpayers had ETRs of 10 percent or less, and at the other extreme, 25.6 percent of

taxpayers had ETRs higher than 50 percent. See GAO, U.S. Multinational Corporations:

Effective Tax Rates Are Correlated With Where Income Is Reported, GAO-08-950

(Washington, D.C.: Aug. 12, 2008).

Calculating

Worldwide Effective

Tax Rates

Appendix I: Selected Issues Relating to the

Calculation of Effective Corporate Income Tax

Rates

Page 24 GAO-16-363 Corporate Income Tax

result in what is known as deferral.

5

However, the Internal Revenue Code

(IRC) has antideferral provisions which limit deferral in certain

circumstances. For example, if a foreign entity is a Controlled Foreign

Corporation, as defined in statute, then certain U.S. shareholders, such

as parent corporations, are taxed on their share of certain income earned

by the Controlled Foreign Corporation when it is earned.

6

The income of a

Controlled Foreign Corporation to be included in U.S. shareholders’

income includes the income defined in subpart F (often called Subpart F

income) and earnings of the Controlled Foreign Corporation invested in

U.S. property. Major types of Subpart F income include income from

passive investments, income from transactions with entities related to the

Controlled Foreign Corporation, and insurance income as well as certain

other easily manipulated income, which are ineligible for deferral. When

income is deemed to be received by the U.S. corporation in this way, it

may have already been taxed in the foreign country where it was earned.

The IRC allows U.S. parent corporations to claim a foreign tax credit for

taxes paid to other countries so that foreign source income, such as

repatriated dividends and Subpart F income, is not taxed twice. This

results in U.S. corporations paying federal income tax on foreign-source

income only to the extent that the federal income tax on that income

exceeds the foreign tax credit. Section 78 of the IRC requires U.S.

corporations electing to claim the foreign tax credit to “gross-up” (i.e.,

increase) their dividend income by the amount of creditable foreign

income taxes associated with the dividends they received. Similar

requirements apply to Subpart F income.

7

5

In general, individuals as shareholders get the benefits of deferral when owning shares of

both domestic and foreign corporations. U.S. corporations as shareholders can deduct the

full amount of qualified dividends received from domestic shareholders. So while deferral

exists, it provides limited to no tax benefit in that circumstance.

6

An entity is a Controlled Foreign Corporation if “U.S. shareholders” own more than 50

percent of the total combined voting power of its stock, or more than 50 percent of the

stock’s total value. To be considered a “U.S. shareholder” for the purposes of this

definition, a U.S. person must own at least 10 percent of the total combined voting power

of the corporation’s stock. In calculating ownership, direct, indirect, and constructive

ownership are considered. U.S. persons are deemed to own stock held by their wholly

owned subsidiaries or by certain other related persons. 26 U.S.C. §§ 951, 957.

7

26 U.S.C. § 78. A U.S. corporation that owns at least 10 percent of the voting stock of a

foreign corporation is allowed to take an indirect credit for foreign income taxes associated

with certain dividends it receives from that foreign corporation or is deemed to have

received under Subpart F. 26 U.S.C. §§ 902, 960.

Appendix I: Selected Issues Relating to the

Calculation of Effective Corporate Income Tax

Rates

Page 25 GAO-16-363 Corporate Income Tax

For our prior report we did not have data relating to the amount of foreign

tax credits claimed by our population of profitable large corporations.

8

As

a substitute for the amount of foreign taxes paid, we used the current

foreign tax expenses and foreign withholding tax expenses that the

taxpayers reported in their financial statements. In the case of repatriated

dividends, our measure included foreign taxes paid on the dividends

themselves, but not any foreign tax paid on the subsidiaries’ income out

of which the dividends were paid. In the latest data we obtained from the

Internal Revenue Service (IRS), we do have amounts for the foreign tax

credits claimed in 2012 by the profitable corporations. The new data also

enabled us to make reliable estimates of the foreign tax credits claimed in

2010 and 2011; however, we could not make similar estimates for earlier

years.

9

Although this new measure includes the most comprehensive measure of

foreign taxes available in our database, it does not achieve a perfect

alignment between the taxes included in the numerator and the income

8

GAO-13-520.

9

We estimated the foreign tax credit amount for tax years 2010 and 2011 for profitable

corporations by using IRS data on Tax Before Credits, General Business Credit, and Tax

Less Credits. We know that Tax Less Credits equals Tax Before Credits minus General

Business Credit, Foreign Tax Credit, and Other Tax Credits. In addition, we know the

amount of Other Tax Credits for the full population of Schedule M-3 filers. This amount is

relatively small each year and it represents the maximum potential value of Other Tax

Credits for our population of profitable filers. The minimum potential value is zero. We

used all of this information to determine the upper- and lower-bound potential values of

the amount of Foreign Tax Credit claimed by profitable filers. The gap between these two

bounds is very small and we used the midpoint between the bounds for our estimate. We

could not make similar estimates for tax years 2008 and 2009 because the General

Business Credit data were not available. As a substitute for the Foreign Tax Credit for

those 2 years, we used the sum of the current foreign tax expenses and foreign

withholding tax expenses from financial statements and the section 78 gross-up. For the 3

years for which we had the foreign tax credit data, these two alternative measures had

relatively similar values. The worldwide ETRs based on foreign tax credit data were 21.1

percent, 21.8 percent, and 23 percent in 2010 through 2012 for profitable corporations,

respectively. The comparable ETRs based on the alternative measure of foreign taxes

were 21.1 percent, 21.6 percent, and 23.6 percent, respectively. The foreign tax credit

amount for all corporations included in the Schedule M-3 data was available for tax years

2006 to 2012 and we used these data for this population (in our May 2013 report, for the

sake of consistency, we used only data that were available for both of our populations).

Appendix I: Selected Issues Relating to the

Calculation of Effective Corporate Income Tax

Rates

Page 26 GAO-16-363 Corporate Income Tax

included in the denominator.

10

Nevertheless, after discussions with

analysts from IRS and Department of the Treasury, we concluded that

this new measure represents the closest alignment between income and

the taxes paid thereon that is possible with the aggregated Schedule M-3

data available to us. More importantly, as we mentioned in the body of

our report, regardless of the adjustments we make above, our worldwide

ETR estimates do not represent a comprehensive worldwide ETR. They

do not account for income not repatriated by Controlled Foreign

Corporations and the foreign taxes paid on that income. Data do not exist

to measure both the complete worldwide income of U.S. corporate groups

and the actual taxes that they pay. A truly comprehensive rate could be

either higher or lower than the ones we report. The rate of foreign tax paid

on income that Controlled Foreign Corporations choose to repatriate may

be higher than the rate paid on foreign income that is not repatriated.

Since the U.S. tax system provides a foreign tax credit to U.S.

corporations on foreign taxes paid when income is repatriated, it may

create an incentive for Controlled Foreign Corporations to repatriate

income earned in high tax countries, so that U.S. parent corporations can

claim the full foreign tax credit amount. In contrast, as the foreign tax rate

decreases, the U.S. tax due when the income is repatriated increases,

creating a disincentive to repatriate income earned in low tax countries.

10

The misalignment arises because (1) subpart F income is not included in the net book

income of these Schedule M-3 filers, but some residual federal tax paid on that income is

included in our numerator; and (2) net book income includes some foreign-source

dividends that were subject to federal tax in a previous year, and that tax is not included in

our numerator. These two discrepancies work in opposite directions.

Appendix II: Summary of Selected Past

Estimates of Average Effective Tax Rates

Based on Financial Statement Data

Page 27 GAO-16-363 Corporate Income Tax

We used the criteria in our May 2013 report for selecting studies that

included estimates of corporate effective tax rates (ETR).

1

Specifically, a

study had to have (1) used financial statement data to estimate average

ETRs for U.S. corporations, (2) employed pretax worldwide book income

as the denominator of its ETR calculations, and (3) covered at least one

tax year since 2001. In the previous report, these criteria identified eight

studies.

• PricewaterhouseCoopers LLP, Global Effective Tax Rates. April 14,

2011.

• Markle, Kevin S. and Douglas A. Shackelford (1). “Cross-Country

Comparisons of Corporate Income Taxes.” National Tax Journal, vol.

65, no. 3. 2012: 493-528.

• Costa, Melissa and Jennifer Gravelle, “Taxing Multinational

Corporations: Average Tax Rates.” Symposium on International

Taxation and Competitiveness, 65 Tax L. Rev. 391. 2012.

• Lee, Namryoung and Charles Swenson. “Is It a Level Playing Field?

An Analysis of Effective Tax Rates.” Tax Notes International. May 25,

2009: 685-693.

• Markle, Kevin S. and Douglas Shackelford (2). Do Multinationals or

Domestic Firms Face Higher Effective Tax Rates? National Bureau of

Economic Research, Working Paper 15091. June 2009.

http://www.nber.org/papers/w15091.

• Blouin, Jennifer L. and Irem Tuna. Tax Contingencies: Cushioning the

Blow to Earnings? Working Paper. April 2007.

• Hanlon, Michelle and Edward L. Maydew. “Book-Tax Conformity:

Implications for Multinational Firms.” National Tax Journal, vol. 62, no.

1. March 2009: 127-153.

• Dyreng, Scott D., Michelle Hanlon, and Edward L. Maydew. “Long-

Run Corporate Tax Avoidance,” The Accounting Review, vol. 83, no.

1. 2008: 61-82.

For our report, we searched for studies released after March 2013. Our

search yielded the following seven:

• Dyreng, Scott D., Michelle Hanlon, Edward L. Maydew, and Jacob R.

Thornock. Changes in Corporate Effective Tax Rates Over the Past

Twenty-Five Years. Social Science Research Network. October 2014:

1-58. Accessed October 8, 2015. http://ssrn.com/abstract=2521497.

1

GAO, Corporate Income Tax: Effective Tax Rates Can Differ Significantly from the

Statutory Rate, GAO-13-520 (Washington, D.C.: May 30, 2013).

Appendix II: Summary of Selected Past

Estimates of Average Effective Tax Rates

Based on Financial Statement Data

Appendix II: Summary of Selected Past

Estimates of Average Effective Tax Rates

Based on Financial Statement Data

Page 28 GAO-16-363 Corporate Income Tax

• Blouin, Jennifer. “Defining and Measuring Tax Planning

Aggressiveness.” National Tax Journal, vol. 67, no. 4. 2014:875-900.

• Hope, Ole-Kristan, Mark (Shuai) Ma, and Wayne B. Thomas. “Tax

Avoidance and Geographic Earnings Disclosure.” Journal of

Accounting and Economics, vol. 56. 2013:170-189.

• Jiménez-Angueira, Carlos and Larry Ochoa, “The Determinants and

Market Implications of Long-run Effective Tax Rates.” The Journal of

Theoretical Accounting Research, vol. 9.2. Spring 2014: 58-106.

• Markle, Kevin S. and Douglas A. Shackelford. The Impact of

Headquarter and Subsidiary Locations on Multinationals’ Effective Tax

Rates. National Bureau of Economic Research Working Paper 19621.

November 2013. Accessed October 1, 2015.

http://www.nber.org/papers/w19621.

• Carlos Jiménez-Angueira. “The Effect of Tax Regime Changes on the

Market Valuation of Tax Avoidance?” Journal of Finance and

Accountancy, vol. 15. April 2014: 1-20.

• Crabtree, Aaron D. and Thomas R. Kubick, “Corporate Tax Avoidance

and the Timeliness of Annual Earnings Announcements,” Review of

Quantitative Finance and Accounting, vol. 42. January 2014: 51-67.

As indicated in figure 5, these studies used a variety of measures of

worldwide taxes for their numerator in order to calculate their respective

corporate effective tax rates. Four of the seven studies we identified

excluded corporations with negative book income from their ETR

calculations.

2

It is difficult to make close comparisons between our results

and estimates from those of prior studies based on financial statement

data below because most of the latter estimates are averaged over

multiple years for which we have no data.

2

The four articles are those from Hope, Ma, and Thomas, Crabtree and Kubick, Blouin,

and Dyreng, Hanlon, Maydew, and Thornock. The Blouin article removes firms with

cumulative losses for the period in which effective tax rates are calculated. The Dyreng,

Hanlon, Maydew, and Thornock article removes firms with negative pretax income.

Appendix II: Summary of Selected Past

Estimates of Average Effective Tax Rates

Based on Financial Statement Data

Page 29 GAO-16-363 Corporate Income Tax

Figure 5: Average Effective Tax Rates for Selected Studies on U.S. Companies, Using Worldwide Pretax Net Book Income

Note: The Jiménez-Angueira study excludes 2001 to 2002 from its effective tax rate computations.

The Hope, Ma & Thomas study reports effective tax rates for pre- and post-issuance of Statement of

Financial Accounting Standards No.131. It also breaks out effective tax rates for firms that disclose

their geographic earnings and those that do not. We report the effective tax rate from this study for

Appendix II: Summary of Selected Past

Estimates of Average Effective Tax Rates

Based on Financial Statement Data

Page 30 GAO-16-363 Corporate Income Tax

firms that no longer disclose geographic earnings in the post-period because the sample of these

firms is larger and the effective tax rate calculations are more recent.

Appendix III: Number and Percentage of U.S.

Corporations with No Federal Income Tax

Liability from Tax Years 2006 to 2012

Page 31 GAO-16-363 Corporate Income Tax

The following two tables present data on the number of corporations with

and without federal income tax liability for tax years 2006 to 2012. Data

are presented for all active corporations as well as all and profitable large

corporations that filed a Schedule M-3.

Table 3: Number and Percentage of All Corporations With No Tax Liability After Credits, Tax Years 2006 through 2012

Tax year

All active corporations (in millions)

2006

2007

2008

2009

2010

2011

2012

Number of Corporations

1.96

1.87

1.78

1.72

1.67

1.65

1.62

Number of Corporations with No Total Income Tax After Credits

1.31

1.25

1.25

1.24

1.20

1.17

1.13

Percentage of Corporations with No Total Income Tax After Credits

67.0%

67.1

69.9

72.0

72.0

71.1

70.1

All active corporations excluding Schedule M-3 filers (in millions)

Number of Corporations

1.91

1.82

1.74

1.68

1.63

1.61

1.58

Number of Corporations with No Total Income Tax After Credits

1.30

1.23

1.23

1.22

1.18

1.15

1.12

Percentage of Corporations with No Total Income Tax After Credits

67.7%

67.7

70.4

72.6

72.7

71.8

70.9

Source: GAO analysis of IRS data. l GAO-16-363

Notes: These data include forms1120 (U.S. Corporation Income Tax Return), 1120-L (U.S. Life

Insurance Company Income Tax Return), 1120-PC (U.S. Property and Casualty Insurance Company

Income Tax Return), and 1120-F (U.S. Income Tax Return of a Foreign Corporation). They do not

include certain “pass-through” entities, which file on forms 1120-REIT (U.S. Income Tax Return for

Real Estate Investment Trusts), 1120-RIC (U.S. Income Tax Return for Regulated Investment

Companies), and 1120S (U.S. Income Tax Return for an S Corporation). See

https://www.irs.gov/uac/SOI-Tax-Stats-Corporation-Complete-Report.

Appendix III: Number and Percentage of

U.S. Corporations with No Federal Income

Tax Liability from Tax Years 2006 to 2012

Appendix III: Number and Percentage of U.S.

Corporations with No Federal Income Tax

Liability from Tax Years 2006 to 2012

Page 32 GAO-16-363 Corporate Income Tax

Table 4: Number and Percentage of All and Profitable Large Corporations (Schedule M-3 filers) with No Federal Tax Liability