NBER WORKING PAPER SERIES

WHY DID SO MANY PEOPLE MAKE SO MANY EX POST BAD DECISIONS?

THE CAUSES OF THE FORECLOSURE CRISIS

Christopher L. Foote

Kristopher S. Gerardi

Paul S. Willen

Working Paper 18082

http://www.nber.org/papers/w18082

NATIONAL BUREAU OF ECONOMIC RESEARCH

1050 Massachusetts Avenue

Cambridge, MA 02138

May 2012

This paper was prepared for the conference, “Rethinking Finance: New Perspectives on the Crisis,”

organized by Alan Blinder, Andy Lo and Robert Solow and sponsored by the Russell Sage and Century

Foundations. Thanks to Alberto Bisin, Ryan Bubb, Scott Frame, Jeff Fuhrer, Andreas Fuster, Anil

Kashyap, Andreas Lehnert, and Bob Triest for helpful discussions and comments. The opinions expressed

herein are those of the authors and do not represent the official positions of the Federal Reserve Banks

of Boston or Atlanta, the Federal Reserve System, or the National Bureau of Economic Research.

NBER working papers are circulated for discussion and comment purposes. They have not been peer-

reviewed or been subject to the review by the NBER Board of Directors that accompanies official

NBER publications.

© 2012 by Christopher L. Foote, Kristopher S. Gerardi, and Paul S. Willen. All rights reserved. Short

sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided

that full credit, including © notice, is given to the source.

Why Did So Many People Make So Many Ex Post Bad Decisions? The Causes of the Foreclosure

Crisis

Christopher L. Foote, Kristopher S. Gerardi, and Paul S. Willen

NBER Working Paper No. 18082

May 2012

JEL No. D14,D18,D53,D82,G01,G02,G38

ABSTRACT

We present 12 facts about the mortgage crisis. We argue that the facts refute the popular story that

the crisis resulted from finance industry insiders deceiving uninformed mortgage borrowers and investors.

Instead, we argue that borrowers and investors made decisions that were rational and logical given

their ex post overly optimistic beliefs about house prices. We then show that neither institutional features

of the mortgage market nor financial innovations are any more likely to explain those distorted beliefs

than they are to explain the Dutch tulip bubble 400 years ago. Economists should acknowledge the

limits of our understanding of asset price bubbles and design policies accordingly.

Christopher L. Foote

Federal Reserve Bank of Boston

Research Department, T-8

600 Atlantic Avenue

Boston, MA 02210

Kristopher S. Gerardi

Federal Reserve Bank of Atlanta

1000 Peachtree St. NE

Atlanta, GA 30309

Paul S. Willen

Federal Reserve Bank of Boston

600 Atlantic Avenue

Boston, MA 02210-2204

and NBER

1 Introduction

More than four years after defaults and foreclosures began to rise, economists are still debat-

ing the ultimate origins of the U.S. mortgage crisis. Losses on residential real estate touched

off the largest financial crisis in decades. Why did so many people—including homebuyers

and the purchasers of mortgage-backed securities—make so many decisions that turned out

to be disastrous ex post?

The dominant explanation claims t hat well-informed mortgage insiders used the securi-

tization process to take advantage of uninformed outsiders. The typical narrative follows a

loan fr om a mortgage broker through a series of Wall Street intermediaries to an ultimate

investor. According to this story, depicted graphically in the top panel of Figure 1, deceit

starts with a mortgage broker, who convinces a borrower to take out a mortgage that ini-

tally appears affordable. Unbeknownst to the borrower, the interest rate on the mortgage

will reset to a higher level after a few years, and the higher monthly payment will force the

borrower into default.

The broker knows that the mortgage is hard wired to explode but does not care, because

the securitization process means that he will be passing this mortgage on t o someone else.

Specifically, an investment banker buys the loan for inclusion in a mortgage- backed security.

In constructing this instrument, the banker intentionally uses newfangled, excessively com-

plex financial engineering so that the investor cannot figure out the problematic nature of

the loan. The investment banker knows that the investor is likely to lose money but he does

not care, because it is not his money. When the loa n explodes, the borrower loses his home

and the investor lo ses his money. But the intermediaries who collected substantial fees to set

up the deal have no “skin in the game” and therefore suffer no losses.

This insider/outsider interpretation of the crisis motivated an Academy Award-winning

documentary, appropriately titled Inside Job. It has also motivated policies designed t o

prevent a future crisis, including requirements that mortgage lenders retain some skin in the

game for certain mortgages in the future.

In this paper, we lay out 12 facts about the mortgage market during the boom years

and argue that they refute much of the insider/outsider explanation of the crisis. Borrowers

did get adjustable-rate mortgages but the resets of those mortgages did not cause the wave

of defaults that started the crisis in 2007. Indeed, to a first approximation, “explo ding”

mortgages played no role in the crisis at all. Arguments that deceit by investment bankers

sparked the crisis are also hard to support. Compared to most investments, mortgage-

backed securities were highly transparent and their issuers willingly provided a great deal of

information to potential purchasers. These purchasers could a nd did use this information to

1

measure the amount of risk in mortgage investments and their analysis was accurate, even

ex post. Mortgage intermediaries retained lots of skin in the game. In fact, it was the losses

of these intermediaries—not mortgage outsiders—that nearly brought down the financial

system in late 2008. The biggest winners of the crisis, including hedge fund managers John

Paulson and Michael Burry, had little or no previous experience with mortgage investments

until some strikingly good bets on the future of the U.S. housing market earned them billions

of dollars.

Why then did borrowers and investors make so many bad decisions? We argue that any

story consistent with the 12 facts must have overly o ptimistic beliefs about house prices

at its center. The lower panel of Figure 1 summarizes this view. Rather than drawing

a sharp demarcation between insiders and outsiders, it depicts a “bubble fever” infecting

both bo r r owers and lenders. If both groups believe that house prices would continue to rise

rapidly for the foreseeable future, then it is not surprising to find borr owers stretching to

buy the biggest houses they could and investors lining up to give them the money. Rising

house prices generate large capital gains for home purchasers. They also raise the value of

the collateral backing mortgages, and thus reduce or eliminate credit losses for lenders. In

short, higher house price expectations rationalize the decisions of borrowers, investors, and

intermediaries—their embrace of high leverage when purchasing homes or funding mortgage

investments, their failure to require rigorous documentation of income or assets before mak-

ing loans, and their extension of credit to borrowers with histories of not repaying debt. If

this alternative theory is true, then securitization was not a cause of t he crisis. Ra t her, secu-

ritization merely facilitated transactions that borrowers and investors wanted to undertake

anyway.

The bubble theory therefore explains the foreclosure crisis as a consequence of distorted

beliefs rather than distorted incentives. A growing literature in economics—inspired in part

by the recent financial crisis—is trying to learn precisely how financial market participants

form their beliefs and what can happen when these beliefs become distorted.

1

The idea that

distorted beliefs are responsible for the crisis has also received some attention in the popular

press. In one analysis of the crisis, New York Times columnist Joe Nocera referenced the

famous Dutch tulip bubble of the 1630s to argue that a collective mania about house prices,

rather than individual malfeasance on the part of mortgage industry insiders, may be the

best explanation for why the fo r eclosure crisis occurred:

Had there been a Dutch Tulip Inquiry Commission nearly four centuries ago, it

1

Some examples of this work include Gennaioli and Shleifer (2010), Gennaioli, Shleifer, and Vishny (2011

[online proof]), Barb e ris (2 011), Brunnermeier, Simsek, and Xio ng (2012), Simsek (2012), Fuster, Laibson,

and Mendel (2010 ), Geanakoplos (20 09), and Burns ide, Eichenbaum, and Rebelo (2011).

2

would no doubt have found tulip salesmen who fraudulently persuaded people to

borrow money they could never pay back to buy tulips. It would have criticized

the regulators who looked the o t her way at the sleazy practices of tulip growers.

It would have found speculators trying t o corner the tulip market. But centuries

later, we all understand that the roots of tulipmania were less the actions of

particular Dutchmen than the fact that the entire society was suffering under the

delusion that tulip prices could only go up. That’s what bubbles are: they’re

examples of mass delusions.

Was it really any different this time? In truth, it wasn’t. To have so many people

acting so foolishly required the same kind of delusion, only this time around, it

was about housing prices (Nocera 2011).

In both popular accounts and some academic studies, the inside job explanation and the

bubble theory are often commingled. Analysts often write that misaligned incentives in the

mortgage industry (a key part of the inside job explanation) contributed to an expansion of

mortgage credit that sent house prices higher ( a key part of the bubble explanation). We

believe that the two explanations are conceptually distinct, and that the bubble story is a

far better explanation of what actually happened. To put this another way, according to the

conventional narrative, the bubble was a by-product of misaligned incentives and financial

innovation. As we argue in Section 3, neither the facts nor economic theory draw an obvious

causal link from underwriting and financial innovation to bubbles.

No one doubts that the availability of mortgage credit expanded during the housing

boom. In particular, no one doubts that many borrowers received mortgages for which they

would have never qualified before. The only question is why the credit expansion to ok place.

Economists and policy analysts have blamed a number of potential culprits for the credit

expansion, but we will show that the facts exonerate the usual suspects. As noted above,

some analysts claim that the credit expansion occurred because of improper incentives inher-

ent in the so-called originate-to-distribute model of mortgage lending. Yet mortgage market

participants had been buying and selling U.S. mortgages for more t han a century without

much trouble. In a similar vein, some authors blame the credit expansion on the emergence

of nontraditional mortgages, like option ARMs and reduced documentation loans, but these

products had been around for many years before the housing boom occurred. Other writers

blame the credit expansion on the federal government, which allegedly pushed a too-lax lend-

ing model on the mortgage industry. But government involvement in mortgage lending had

been massive throughout the postwar era without significant problems. In contrast to these

these explanations for the credit expansion, the facts suggest that the expansion occurred

simply because people believed that housing prices would keep going up—the defining char-

3

acteristic of an asset bubble. Bubbles do not need securitization, government involvement, or

nontraditional lending products to get started. Bubbles in many ot her assets have occurred

without any of these things—not only tulips in seventeenth-century Holland, but also shares

of the South Sea Company in eighteenth-century England, U.S. equities and Florida land in

the 1920s, even Beanie Babies and technology stocks in the 1990s.

2

As the housing bubble

inflated it encouraged lenders t o extend credit to borrowers who had been constrained in the

past, since higher house prices would ensure repayment of the loans. Much of this credit was

channeled to subprime bo r r owers by securitized credit markets, but this does not mean that

securitization “caused” the crisis. Instead, expectations of higher house prices made investors

more willing to use both securitized markets and nontraditional mortgage products—because

those markets and products delivered the biggest profits to investors as housing prices rose.

Another reason to keep the two explanations distinct is that they suggest very different

agendas for real-world regulators and academic economists. If the inside jo b story is true,

then prevention of a future crisis r equires regulations to ensure that intermediaries inform

borrowers and investors of relevant facts and that incentives in the securitization process

are properly aligned. But if the problem was some collective self-fulfilling mania, then such

regulations will not work. If house prices are widely expected to rise rapidly, then warning

borrowers that their future payments will rise will have no effect on their decisions. Similarly,

intermediaries will be only too willing to keep some skin in the game if they expect rising

prices to eliminate credit losses. For economists, the bubble theory implies that research

should focus on a more general attempt to understand how beliefs are formed about the

prices of long-lived assets. Gaining this understanding is an enormous challenge for the

economics profession. From tulips to tech stocks, outbreaks of optimism have appeared

repeatedly, but no robust theory has emerged to explain these episo des. As a telling example,

at the peak of the housing boom economic theory could not provide academic researchers

with clear predictions of where prices were go ing or if they were poised to fall. Scientific

ignorance about what causes a sset bubbles implies that policymakers should focus on making

the housing finance system as robust as possible to significant price volatility, rather than

trying to correct potentially misaligned incentives.

The multitude of questions suggested by the financial crisis could never be answered by

one single theory—or in one single paper. Fo r example, as we discuss below, the top-rated

tranches of Wall Street’s mortgage-backed securities p erformed much better t han the top-

rated tranches of its collateralized debt obligations, another type of structured security. This

2

The classic reference on tulipmania is MacKay (2003 [1841]). A c ontrarian view on tulipmania is found

in Garb e r (2000), which reviews data on tulip prices and argues that they can be justified by fundamentals

during this period. The book takes a s imila r stance on other early bubbles, including the South Sea Bubble

(1720) and the Mississippi Bubble (1719-1720).

4

discrepancy occurred even though both types of securities were ultimately collateralized by

subprime mortgages, and even though both types of securities were constructed by the same

investment banks. We do not believe that securitization alone caused the crisis but, by

channeling money from investors to borrowers with ruthless efficiency, it may have allowed

speculation on a scale that would have been impossible to sustain with a less sophisticated

financial system. As economists, we believe that the ultimate a nswers to questions like these

will involve information and incentives. But we also believe that that an examination of the

facts that we present about the mortgage market do rule out the most common informatio n-

and-incentives story invoked to explain the crisis—that poo r incentives caused mort gage

industry insiders to take advantage of misinformed outsiders.

The paper is organized as follows. Section 2 lays out the 12 facts about the U.S. mortgage

market that are critical in rationalizing borrower and lender decisions. Section 3 relates

these facts to various economic theories about the crisis, and Section 4 concludes with some

implications for policy makers.

2 Twelve Facts About the Mortgage Market

Fact 1: Resets of adjustable-rate mortgages did not cause the foreclosure crisis

One theory for why borrowers took out loans t hey could not repay is that their lenders

misled them by granting them loans t hat initially appeared affordable but became unafford-

able later on. In particular, analysts have pointed to t he large number of adjustable-rate

mortgages (ARMs) originated in the years immediately preceding the crisis, attributing the

rise in delinquencies and foreclosures to the “payment shocks” associated with ARM-rate

adjustments. Borrowers, they argued, had either not realized that their payments would

rise or had been assured that they could refinance t o lower-rate mortgag es when the resets

occurred.

The “exploding ARM” theory has played a central role in narratives about t he crisis

since 2007 , when problems with subprime mortgages first gained national attention. In April

2007, Sheila Bair, then the chair of the Federal Deposit Insurance Corporation, testified to

Congress that “ ‘[m]any subprime borrowers could avoid foreclosure if they were offered more

traditional products such as 30 -year fixed-rate mortgages’ ” (Bair 2007).

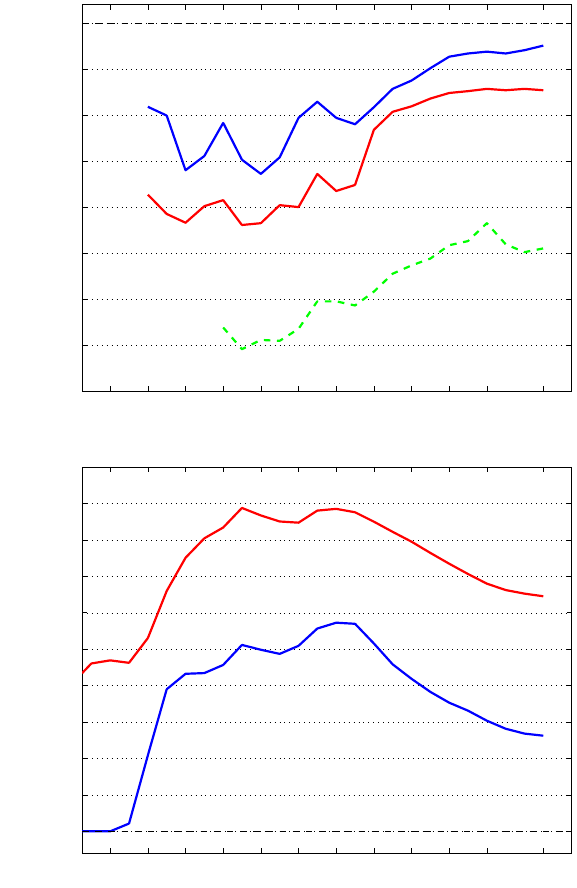

Yet the data are not kind to the exploding ARM theory. Figure 2 shows the path of

interest rates and defaults for three vintages of the most problematic type of ARM, so-

called subprime 2/28s. These mortgag es had fixed interest rates for the first two years, then

5

adjusted to “fully indexed” rates every six months for the loan’s 28 remaining years.

3

The

figure shows that, at least for subprime 2/28s, payment shocks did not lead to defaults. The

top left panel depicts interest rates and cumulative defaults for subprime 2/28s originated in

January 2005. For these mortgages, the initial interest rate was 7.5 percent for the first two

years. Two years later, in January 2007, the interest rate rose to 11.4 percent, resulting in a

payment shock of 4 percentag e points, or more than 50 percent in relative terms. However,

the lower part of the panel shows that delinquencies for the Januar y 2005 loans did not tick

up when this reset occurred. In fact, the delinquency plot shows no significant problems for

the 2005 borrowers two years into their mortgages when their resets occurred. The top right

panel displays data f or 2/28s orig inated in January 2006 . These loa ns had initial rates of

8.5 percent that reset to 9.9 percent in January 2008 . This increase o f 1.4 percentage points

results in a relative increase of about 16 percent, one-third the size of the payment shock

for the previous vintage. Yet even though the payment shock for the January 2006 loans

was smaller than that for the 2005 loans, their delinquency rate was higher. Finally, the

worst-performing loans, t hose originated in January 2007, are depicted in the figure’s bott om

panel. When these loans reset in January 2009, their fully indexed rates were actually lower

than their initial rates. However, the contract on the typical 2/28 mortgage sp ecified that

the interest rate could never go below the initial rate, so f or all practical purposes subprime

2/28s fro m January 2007 were fixed-rate loans. But as the lower part of the panel indicates,

these “fixed-rate” loans had the highest delinquency rates of any vintage shown in the figure.

As many have pointed out, subprime 2 /28s were not the only loans with payment shocks.

In 2004 and 2005, lenders originated many nontraditional, or “exotic,” mortgages, which often

had larger payment shocks and which we discuss in more detail below. Ta ble 1 attempts to

quantify the impact of payment shocks across the entire mortgage market by looking at

all foreclosures from 2007 through 2010, regardless of the type of mortgage. The go al is

to determine whether the monthly payments faced by borrowers when they first became

delinquent were higher than the initial monthly payments on their loans. The top panel of

this t able shows that this is true for only 12 percent of borrowers who eventually lost their

homes to for eclosure. The overwhelming majority of foreclosed bor r owers—84 percent—were

making the same payment at the time they first defaulted as when they originated their

loans. A main reason for this high percentag e is that fixed-rate mortgages (FRMs) account

for 59 percent of the foreclosures between 2007 and 2010.

Table 1 puts an upper bound on the role that deceptively low mortgage payments may

have played in causing the crisis. Basically, it t ells us that if we had replaced all of the complex

3

T

ypically, the fully indexed rate was a fixed amount over some short-term rate, for example 6 percentage

points above the six-month LIBO R.

6

mortgage products with fixed-rate mortgages, we would have prevented at most 12 percent

of the foreclosures during this t ime period. But even 12 percent is a substantial overestimate,

because the table shows that fixed-rate borrowers also lost their homes to foreclosure as well.

While FRMs accounted for most defaults, this does not mean that FRMs suffered higher

default rat es. In fact, fixed-rat e loans defaulted less often than adjustable-rate loans; the

predominance of fixed-rate loans among defaulted mortgages stems from the fact that FRMs

are more common than ARMs. Yet we should not overstate the better performance of fixed-

rate loans, particularly among subprime borrowers. The bottom panel of Table 1 shows

that 53 percent of subprime ARMs originated between 2005 and 2007 have experienced at

least one 90-day delinquency. The corresponding figure for FRMs is 48 percent, a difference

of only 5 percentage points.

4

Even this small difference does not indicate that subprime

ARMs were worse products t han FRMs. The lack of any relationship between the timing

of the initial delinquency and the t iming of the reset has led most researchers to conclude

that ARMs performed worse than FRMs because they attracted less creditworthy borrowers,

not because of something inherent in the ARM contract itself. Even if we did believe that

the ARM-versus-FRM performance difference was a causal effect and not a selection effect,

almost half of borr owers with subprime FRMs became seriously delinquent. The terrible

performance of subprime FRMs contradicts the claim of Martin Eakes, the head of the

Center for Responsible Lending, that “exploding ARMs are the single most important factor

causing financial crisis for millions” (Eakes 2007).

Fact 2: No mortgage was “designed to fail”

Some critics of the lending process have argued that the very existence of some types of

mortgages is prima facie evidence that bo r r owers were misled. These critics maintain that

reduced-documentation loans, loans to borrowers with poor credit histories, loans with no

downpayments, and option ARMs were all “designed t o fail,” so no reasonable borrower would

willingly enter into such transactions.

5

In fact, the large majority of these loa ns succeeded

for both borrower and lender alike.

In Figure 3, we graph failure rates for four categories of securitized nonprime loans. Along

the horizontal axis ar e years of originatio n, and the figure defines failure as being at least

4

To so me extent, this 5 percent difference understates the performance differential among subprime ARMs

and FRMs because originations of subprime FRMs were concentrated in the later vintages of loans which had

the highest default rates . We comment on this concentration be low. Also, a per formance gap between sub-

prime FRMs and ARMs is robust to a more sophisticated analysis that controls for observable cha racteristics

(Foote et al. 2008 ).

5

The phrase “designed to fail” appears in speeches by presidential candidate Hillary Clinton, Senator

Charles Schumer of New York, and press releases from prominent attorneys general including Martha Coakley

of Massachusetts and Catherine Cortez Masto of Nevada.

7

60 days delinquent two years after the loan was originated.

6

The figure shows that the vast

majority of loa ns originated from 2000 thro ugh 2005 were successful. For example, the lower

left panel shows that in 2007 , after the housing market had begun to sour, only 10 percent of

the bo r r owers who took out low- or no-documentation mortgages in 2005 were having serious

problems. Additionally, loans requiring no downpayments (top right panel) and even “risk-

layered” loans (bottom rig ht panel) originated before 2006 also display failure rates that are

well under 10 percent. Loans in the upper left panel were made to borrowers with credit

scores below 620, who typically had a history of serious debt repayment problems. Yet after

two years, more than 80 percent of low-scoring borrowers who originated loans before 2006

had either avoided seriously delinquency or had repaid their loa ns. Given their spotty credit

histories, the performance of these borr owers indicates remarkable success, not failure.

Some might argue that the loans in Figure 3 succeeded only because the borrowers were

able to refinance o r sell. But it would be wrong to classify prepayments as failures. In many

cases, the simple fact of making 12 consecutive monthly payments allowed the borrower to

qualify for a lower-cost loan. In such cases, t he refinance is a success for the borrower, who

gets a loan with better terms, as well as the lender, who is fully repaid.

In the end, the idea that subprime or Alt- A loans were designed to fail does not fit the

facts. This finding should not be surprising. Marketing products that do not work is usually a

bad business plan, even in the short r un, whether one is producing mortgages or motorcycles.

The fact that f ailure rates f or all the loans in Figure 3 rose at about the same time suggests

that t hese mortgages were not designed to fail. Instead, they were not designed to withstand

the stunning nationwide fall in house prices that began in 2 006. We will return to this theme

later.

Fact 3: There was little innovation in mortgage markets in the 2000s

Another popular claim is that the housing boom saw intense innovation in mortg age

markets. According to the conventional wisdom, lenders began to offer types of mortga ges

that they never had befor e, including loans with no downpayments, loans with balances that

increased over time,

7

and loans that lacked rig orous documentation of borrower income and

assets. In more nuanced versions o f the story, lenders did not innovate so much as expand

the market for nontraditional mortgages. As Allen Fishbein of the Consumer Federation of

America described these nontraditional mortgages in Congressional testimony:

Tr aditionally, these types of loans were niche products that were offered to upscale

6

Our choice of the two-year period does not influence our results. Figure 2 shows that default rates on

subprime loans did not spike after two years.

7

The balances of a traditional “amortizing ” mortgage decreases over time, because the borrower pays both

interest and pa rt of the outstanding principal each month.

8

borrowers with particular cash flow needs or to those expecting to remain in their

homes for a short time (Fishbein 2006).

Figure 3 shows t hat originations of riskier loans increased dramatically f r om 2002 to 2006

and commentators po int to such data as evidence of large-scale innovation.

The historical record paints a different picture. It is approximately tr ue to say that prior

to 1981, virtually all mortgages were either fixed-rate loans or something close to it.

8

Yet

the emergence of nontraditional mortgages still predates the 2000s mortgage boom by many

years. Perhaps the most extreme form of nontraditional mortgage is the “payment-option

ARM,” which allows a borrower to pay less than the interest due on the lo an in a given month.

The difference is made up by adding the arrears to the outstanding mortgage balance. This

type of loan was invented in 1980 and approved fo r widespread use by the Federal Home

Loan Ba nk Board a nd the Office of the Comptroller of the Currency in 1981 (Harriga n 1981;

Gerth 1981). Large California thrifts subsequently embraced the option ARM, which would

eventually play a central role in the Golden State’s housing market (Guttentag 19 84). By

1996, one-third of all originations in California were option AR Ms (Sta hl 199 6); we reproduce

a 1998 advertisement for this product in the left panel of Figure 4. The large volume of

option ARMs belies the claim that this instrument was a niche product. Indeed, the lender

most closely associated with option ARMs, Golden West, made a point of avoiding “upscale”

borrowers. Despite originating almost two-thirds o f its loans in California, the typical Golden

West mortgage in 2005 was for less than $400,000 (Savastano 2005).

Some confusion about the growth of option ARMs results from the fact that they were

almost exclusively held in bank portf olios until 2004. The loan was an attr active po r t folio

addition because it generated floating-r ate interest income a nd thus eliminated the lender’s

interest-rate risk. At the same time, the option ARM’s flexible treatment of amortization

smoothed out payment fluctuations for the borrower. In any event, even though option ARMs

were available in the 1980s and 1990s, they do not show up in datasets of securitized loans

until 2004.

9

Even t hen, the majority of securitized option ARMs were made in the markets

where they were already common as portfolio loans (Liu 2005).

Another type of nontraditional mortgage, the reduced-documentation loan, also began to

spread in t he 1980s; the right panel of Figure 4 shows a 1989 ad for such a loan. By 1990,

Fannie Mae reported that between 30 and 35 percent of the loans it insured were low- and

no-doc loans (Sichelman 1990). Ironically, commentators raised virtually identical concerns

about low-doc lending in the early 1990s as they did in 2005. For example, Lew Sichelman, a

8

One author’s father took out an interest-only adjustable-rate, balloon payment mortgage in 1967 but

that was an exceptional situation.

9

See, for example, Table 4 of Dokko et al. (2009).

9

veteran mortgage industry journalist, wrote in 1990 that “in recent years, lenders, spurred by

competitive pressures and secure in the knowledge that they could peddle questionable loans

to unsuspecting investors on the secondary market, have been approving low- and no-doc

loans with as little as 10 percent down” (Sichelman 1990).

Fact 4: Government policy toward the mortgage market did not change much

from 1990 to 2005

While the conventional wisdom blames the foreclosure crisis on t oo little government

regulation of the mortgage market, an influential minority believes that government inter-

ventions went too far.

10

According to this view, policymakers in the 1990s hoped to expand

homeownership, either for its own sake or a s a way to combat t he effects of rising income

inequality. Consequently, this narrative contends that policymakers allowed lenders to aban-

don traditional and prudent underwriting guidelines that had worked well for decades. In

reality, government officials talked at length about lending and homeownership in the 1990s

and early 2000s, but actual market interventions were modest. In fact, compared to the

massive federal interventions in the U.S. mortgage market during the immediate postwar

era, government interventions during the recent housing boom were virtually nonexistent.

For a concrete example, consider the size of required downpayments. Morgenson and Ros-

ner (2011) write that because of the Clinton Administration’s emphasis on homeownership:

[I]n just a few short years, all of the venerable rules governing the relationship

between bor r ower and lender went out the window, starting with the elimination

of the requirements that a borrower put down a substantial amount of cash in a

property (Morgenson and Rosner 2011, p. 3).

11

It is true that large downpayments were once required to purchase homes in the United

States. It is also true that the federal government was instrumental in reducing required

downpayments in an effort to expand homeownership. The problem for the bad government

theory is that the timing of government involvement is almost exactly 50 years off. The

key event was the Servicemen’s Readjustment Act of 1944, better known as the GI Bill, in

which the f ederal government promised to take a first-loss position equal to 50 percent of

the mortgage balance, up to $2,000 , on mortgages originated to returning veterans. The

limits on the Veteran’s Administration (VA) loans were subsequently and repeatedly raised,

while similar guarantees were later added to loans originated through the Federal Housing

Administration (FHA). The top panel of Figure 5 gra phs average loa n-to-value (LTV) ratios

10

See Morgenson and Rosner (2011) and Rajan (2010) for two leading examples of the genre.

11

This quotation goes on to claim that requirements to verify income and demonstrate repayment ability

were also reduced.

10

for various types of loans, including those with FHA and VA insurance. It shows that

borrowers t ook advantage of these government programs to buy houses with little or no

money down. By the late 1960s, t he average downpayment on a VA loa n was around 2

percent. A large fraction of borrowers put down nothing at all. Government involvement

in the early postwar mortgage market was broad; in no sense were FHA and VA mortgages

“niche products.” The bottom panel of Figure 5 shows that t ogether, the FHA and the VA

accounted for almost half of originations in the 1950s before tailing off somewhat in the 1960s.

In contrast to the heavy government involvement in housing during the immediate postwar

era, recent dat a on LTV ratios suggests no major federal mortgage market interventions

in the 1990s and 2000s. Figure 6 shows combined LTV ratios for purchase mortgages in

Massachusetts from 1990 to 2010, the period when government intervention is supposed to

have caused so much trouble.

12

To be sure, the boom years of 200 2–2006 saw an increase in

zero-down financing. But the data also show that even before the boom, most borrowers got

loans without needing t o post a 20 percent downpayment.

13

In particular, Morgenson and

Rosner (2011) point to the Clinton administration’s National Partners in Ho meownership

initiative in 1994 as the starting point for an ill-fated credit expansion that led to the crisis.

But inspection of Figure 6 does not support the assertion that underwriting behavior was

significantly changed by that program. The distribution of downpayments is remarkably

stable after 1994. The share of zero-down loans actually falls.

14

All told, it is impossible to find any government housing market initiative in r ecent years

that is remotely comparable to the scope of t he GI Bill and FHA’s subsequent expansion. It is

important to stress that the FHA and the VA were widely understood to encourage high- r isk

lending to less-qualified borrowers. The delinquency rates on the loans they guaranteed were

several times higher than delinquency rates on conventional loans. But the two government

programs were also considered successful because they enabled lower-income Americans to

own their own homes.

15

Fact 5: The originate-to-distribute model was not new

One of the most important motivating principles of the Dodd-Frank Act, passed in 2010

to reduce the chance of future financial crises, was that the originate-to-distribute (OTD)

model of lending shouldered much of the blame for t he foreclosure crisis. Congressman Barney

12

Combined LTV ratios, sometimes denoted CLTV ratios, include all mortgages taken out by the home-

owner at the time of purchase, including so-called piggyback mortgages.

13

Public records do not allow us to know whether a purchase corresponds to a first-time homebuyer. If it

were possible to focus on those purchases alone, the average downpayment would undoubtedly be even lower

than the averag e that includes all purchases.

14

Glaeser, Gottlieb, and Gyourko (2010) look at data for a bro ader set of cities and finds similar results.

15

See Herzog and Earley (1970) for a contempora ry analysis of default rates on FHA, VA, and conventional

mortgage s.

11

Frank, then the chairman of the House Financial Services Committee, put it this way: “ ‘If

I can make a whole bunch of loans and sell the entire right to collect those to somebody

else, at that point I don’t care...whether or not they pay off. We have to prohibit that.’ ”

16

The Dodd-Frank Act requires mortgage originators to retain a slice of the credit risk of the

mortgages they generate unless the credit quality of the mortgages is strong enough to earn

an exemption.

Yet the OTD model was central to the U.S. mortgage market for decades before the

financial crisis began. In t he immediate postwar era, an important manifestation of the

OTD model was the mortgage company. These firms borrowed money from banks in order

to fund mortgages for sale t o outside investors, who often held the mortgages as whole

loans. These lenders also “serviced” the loans on behalf of the investors and received a fixed

percentage of the loan balance every month as compensation. A 1959 National Bureau of

Economic Research study of mortgage companies lists the fundamental features of the OTD

model that would be familiar to modern originators as well:

The mo dern mortgage company is typically a closely held, priva t e corporation

whose principal activity is originating and servicing residential mortgag e loans

for institutional investors. It is subject to a minimum degree of federal or state

sup ervision, has a comparatively small capital investment relative to its volume

of business, and relies largely on commercial bank credit to finance its operations

and mortgage inventory. Such inventory is usually held o nly for a short interim

between closing mortgage loans and their delivery to ultimate investors (Klaman

1959, p. 239).

The importance of mortgage companies grew in the second half of the twentieth century. The

top left panel of Figure 7 shows that the market share of mortgage companies was around

20 percent in the 197 0s and reached nearly 60 percent by 1995.

A focus on mortgage companies alone understates the role of the OTD model, however.

Starting in the 1970s, the OTD model was adopted by other financial institutions, most

importantly savings and loans (S&Ls), which financed the majority of U.S. residential lending

in the postwar period. S&L’s had historically followed an originate-and-hold model. By the

late 1970s, however, rising interest rates had generated a catastrophic mismatch between the

low interest rates that S&Ls received on their existing mortgages and their current costs of

funds. This mismatch, which would eventually render more than half of S&Ls insolvent,

encouraged thrifts either to turn to adjustable-rate mortgages or to sell the mortgages they

originated to the secondary market. The top right panel of Figure 7 shows that by the

16

Congressman Frank is quoted in Arnold (2009).

12

late 1980s, S&Ls sold almost as many loans as they originated. In other words, most had

adopted the OTD model and had become, for all practical purposes, mortgage companies.

The bo t t om panel of Figure 7 shows that t he decline of the originate-to-hold model was well

underway 30 years before the boo m of the 2000s.

Over time, t he OTD model evolved. In the 1950s, mortgage companies typically sold

their loans to insurance companies, which kept them on portfolio as whole loans. Starting in

the 1970s, this f r amework gave way to mortgage-backed securities (MBS), which were largely

guaranteed by Ginnie Mae. The other government-sponsored housing agencies, Fannie Mae

and Fr eddie Mac, became dominant players in the early 1980s. This period also saw the

emergence of the private-label securities market, and in the 2000s, the privat e- la bel market

grew at the expense of the agency market. However, the institutional framework of the OTD

model remained more or less identical to what it was in the 1950s. Lenders originated loans

and sold t hem to other institutions. Typically the loans were then serviced by the originating

lender, but other servicing arrangements were also possible.

17

Fact 6: MBSs, CDOs, and other “complex financial products” had been widely

used for decades

Another source of potential confusion lies in the distinction between the OTD model and

securitization. Securitization implies originate-to-distribute, but the OTD model existed for

decades before securitization emerged. As noted above, early manifestations of the OTD

model generally featured the sale of whole loans into investor portfolios. Only in the 1970s

and 1980s did Ginnie Mae, Fannie Mae and Fr eddie Mac began to arrange and/or insure

pass-through securities, whereby investors could buy a pro-rated share of a pool of mort gages.

Private-label securities were also being developed at that time, but the emergence of these

securities proceeded in fits and starts. In 1977, Salomon Brothers arranged the first priva t e-

label MBS deal, which was considered something of a failure.

18

Among other problems,

existing state laws prevented most of the relevant investors from buying the bonds. Issuing

securities through Fannie Mae and Freddie Mac allowed issuers to address these laws, and

the collateralized mortgage obligation (CMO) emerged in the early 1980s a s a way to sell an

17

When recounting the history of the OTD mo del, it is important to dis ting uis h between mortgage brokers

and mortgage bankers. Jiang, Nelson, and Vytlacil (2011) claim that brokers “issue[d] loans on the bank’s

behalf for commissions but do not bear the long -term conse quences of low-quality loans,” but this statement

is incorrect. B rokers, who often have specific knowledge of a local market, can help match bor rowers with

lenders, but they do not underwrite or fund mortgages. Rather, mortgage banks, which include mortgage

companies and S&L’s, underwrite and fund loans. These lenders can choose to place a brokered loan in a

security, sell it to another lender, or keep it on p ortfolio. In short, there is no neces sary connection between

brokers and the OTD model; the decision to extend a loan rests entirely with the lender, because the lender

comes up with the money.

18

See Ranieri (1996) for a discussion.

13

array of complex securities with different repayment prop erties (principal-only, interest-only,

floating-rate notes, fixed-r ate notes, and so on) secured by a pool of mortgages. Until the

1986 Tax Reform Act, it r emained difficult to construct a complex mortgage deal without

Fannie Mae or Freddie Mac’s involvement. But that Act created a financial structure called a

Real Estate Mortgage Investment Conduit (REMIC), which allowed issuers to create complex

MBSs without the assistance of one of the GSEs.

The emergence of collateralized debt obligations (CDOs) was the next step in the secu-

ritization of debt. The CDO was invented in the early 1990s as a way f or banks to sell the

risk on pools of commercial loans (Tett 2009). Over time, financial institutions realized that

the CDO structure could also be used for pools of risky tranches from securities, including

private-label securities backed by mortgag es. In 2000, investment banks began to combine

the lower-rated tranches of mortgage securities, typically subprime asset-backed securities

(ABS), with other forms of securitized debt to create CDOs. The ABS CDO was born.

19

As

Cordell, Huang, and Williams ( 2011) shows, the poor performance of ABS CDOs in the early

2000s was widely blamed on the presence of nonmortgage assets like tranches from car-loan

or credit-card deals, so t he ABS CDO deals became dominated by tr anches from subprime

ABS. Consequently, as the housing market boomed in the mid-200 0s, ABS CDOs became

increasingly pure plays on the subprime mortg age market.

Looking back, a remarkable feature about the boom in securitized lending in the mid-

2000s is that the institutional and legal framework it required had been in place since at

least the early 1990s, a nd for some key components much earlier than that. In other words,

what is significant about the evolution of the mortgage market in the 2000s is how little

institutional change took place. As far as the mortga ge and mortgage-securities markets

were concerned, there were few legal or institutional changes, and certainly no major ones

in the period immediately preceding the lending boom. It is true that there was dramatic

growth in the use of subprime ABS to fund loans, as well as the use of ABS CDO s to fund

the lower-ra t ed tranches of subprime deals. But this growth did not occur because lenders

and investors had been unable to use those structures earlier. In short , the idea that the

boom in securitization was some exogenous event that sparked the housing boom receives no

suppo r t from the institutional history of the American mortgage market.

Fact 7: Mortgage investors had lots of information

One of the pillars of the inside job theory of the mortgage crisis is that mortgag e industry

19

In the industry, bonds backed by subprime loans were considered asset- backed securities (ABS) rather

than MBS, because subprime lending began as an alternative to unsec ured credit for troubled borrowers.

Thus, as an institutional matter, subprime lending was part of the consumer lending, or ABS market, not

the mortgage, or MBS mar ket.

14

insiders were stingy with information about the securities they structured and sold. In fact,

issuers supplied a great deal of information to potential investors. Simply put, the market

for mortgage investments was awash in information.

To start with, prospectuses for pools of loans provided detailed information on the under-

lying loans at the time they were originated. This information included the distributions of

the key credit-quality variables, such LTV ratios, documentation status, and borrower credit

scores. More importantly, they provided conditional distributions showing, for example, the

share of borrowers with FICO scores between 600 and 619 or the share of borrowers with

LTV ratios between 95 and 99 percent. In many cases, issuers provided loan-level details in

what wa s known as a “free writing prosp ectus.”

To nonexperts, one of the most confusing things about the mortgage securities market

is that issuers were quite careful to document the extent to which they did not document a

borrower’s income and assets. Loans were typically given a four-letter code that informed

investors whether the information a bout income (I) and assets (A) were either verified (V),

stated (S), or not collected at all (N). For example, the co de SIVA meant stated income-

verified assets.

20

The crucial point here is that investors knowingly bought low-doc/no-doc

loans. In fact, we now know that lenders provided loans to borrowers with damaged credit

without do cumenting their incomes not because of any after-the-fact forensic investigation,

but rather because lenders broadcasted this information to prospective investors. The orig-

ination data in Figure 3, which show the dramatic growth o f loans to bor r owers with low

credit scores and less-than-full income a nd asset verification, come from data provided to

investors—data that were known about and widely commented upon in real time.

The infor matio n flow continued after the deals were sold to investors. All issuers provided

monthly loan-level information on the characteristics of every loan in the pool, including the

monthly payment, the interest rate, the remaining principal balance and the delinquency

status of each loan. Issuers also disclosed the disposition of terminated loans, including

the dollar amounts of losses that stemmed from short sales or foreclosures. Again, these

data were publicly available free of charge, but most investors used a loan-level dataset from

the LoanPerfor mance company, which was a cleaned and standardized version of raw data

gathered from many different issuers and lenders.

Investors had access not only to important data, but also to tools that allowed them to

use these data to price securities. The MBS and CDOs that contained the mortgages (or

the mortgage risk) appeared complex on the surface, but they were in fact straightforward

20

The NINA loan is the basis for the apocryphal “NINJA” loan that is often used as an e xample of excesses

in the boom-era mortgage market. NINJA supposedly stood for “no-income, no job, no assets,” but no such

loan ever existed. Also, the NINA code, which did exist, did not signify a loan to a borrower with no income.

Rather, the code signified that the lender had no information about the borrower’s income.

15

to model. Most investors used a program called Intex that coded all of the rules from a

prospectus for the allocation of cash flows to different tranches of a deal. To forecast the

performance of a deal, an investor would input into Intex a scenario for the performance of the

underlying loans. Intex would then deliver cash flows, taking into account all of the complex

features of the deal, including so-called overcollateralization accounts and the treatment of

interest income earned on loans that were paid off in the middle of a month. Cordell, Huang,

and Williams (2011) shows that using Intex, one could accurately measure the losses and

value of ABS CDOs in real time throughout the crisis.

To illustra t e the information available to investors on a CDO transaction, Figure 8 shows

pages from the offer documents fo r the notorious Abacus AC-1 CDO.

21

These documents

provide amounts and CUSIPs

22

for every security in the deal. Armed with those CUSIPs, a

potential investor could use LoanPerformance data to obtain the origination information and

current delinquency status of every individual loan in each deal. Then, using Intex, the in-

vestor could forecast the cash flows for each reference security under different macroeconomic

scenarios.

Fact 8: Investors understo od the risks

Using dat a supplied by issuers and lenders, as well as quantitative tools designed to ex-

ploit this infor matio n efficiently, investors were able to predict with a fair degree of accuracy

how mortgages and related securities would perform under various macroeconomic scenar-

ios.

23

Table 2, taken from a Lehman Brothers analyst repo r t published in August 2005,

shows predicted losses for a pool of subprime loans originated in the second half of 2005

under different assumptions for U.S. house prices (Mago and Shu 2005). The to p three house

price scenarios, which range from “base” to “aggressive,” predict losses of between 1 and 6

percent. Such losses had been typical of previous subprime deals a nd implied that invest-

ments even in lower-rated tranches of subprime deals would be profitable. The report also

considers two adverse scenarios for house prices, one labeled “pessimistic” and the other la-

beled “meltdown.” These two scenarios assume near-term annualized growth in house prices

of 0 a nd –5 percent, respectively. For those scenarios, losses are dramatically worse. The

pessimistic scenario generates an 11.1 percent loss while the meltdown scenario generates a

21

Abacus was a dea l arranged by Goldman Sachs in 2007 that largely amounted to a bet on whether a

collection of BBB subprime s e c urities would default. Hedg e fund manager John Paulson took a short position

in the deal while IKB and ABN Amro took long positions. The SEC broug ht fraud charges agains t Goldman

Sachs, alleging that they did not properly disclose the fact that Paulson played a role in choosing the spec ific

securities that made up the deal.

22

A CUSIP is a 9-character code that identifies any North American security, and is used to facilitate the

clearing and settlement of financial trades.

23

The discussion of facts 8 and 9 is based on Gera rdi et al. (2008). We dir e c t interested readers to that

paper for a mo re complete discussion of the issues.

16

17.1 percent loss. The repor t goes on to point out that while the pessimistic scenario would

lead to write-offs of the lowest-ra t ed tranches of subprime deals, the meltdown scenario would

lead to massive losses on all but the highest-rated tranches.

Lehman analysts were not alone in understanding the strong relationship between house

prices and losses on subprime loans. As Gerardi et al. (2008) show, analysts at other banks

reached similar conclusions and were similarly accurate in their forecasts conditional on house

price appreciation outcomes. JPMorgan analysts used MSA-level variation in losses on 2003

subprime originations to produce remarkably accurate predictions about losses (Flanagan

et al. 2006a). A UBS slide presentation about subprime securities given in fall 2005 was

subtitled, “Its (Almost) All About Home Prices” (Zimmerman 2005).

The Lehman analysis, and others like it, are crucial documents for anyone hoping to

understand why investors lined up to buy securities backed by subprime loans. First, the

analysis shows that investors knew about the significant r isk inherent in subprime deals.

Expected losses on a typical prime deal were a fraction of 1 percent—even under the worst

scenarios prime losses might reach the low single digits.

24

According to Table 2, losses o n a

subprime deal could be many times higher. Given a 50 percent recovery rate in foreclosure,

the 17.1 percent loss implied in Lehman’s meltdown scenario assumes that lenders would

foreclose on one-third of the loans in the pool. The analysis underscores investors’ knowledge

about the sensitivity of subprime loans to adverse movements in housing prices, and it refutes

the idea that investors did not or could not determine how risky these loans were.

A second reason that Table 2 is important is that its forecasts proved to be accurate.

Despite its foreboding name, the “meltdown” scenario was actually optimistic with respect

to the observed fall in housing prices that began in 2006. The current forecast for losses on

deals in the ABX 2006-1 index, which largely contains loans originated in the second half of

2005, is about 22 percent (Jozoff et al. 2012). This is consistent with the relationship between

losses and house prices implied by the table. The bot t om line is that analysts working in real

time had little trouble figuring out how much subprime investors would lose if house prices

fell.

The next logical question: given how badly these loans were expected to perform if prices

fell, why did investors buy them? We turn to this question next.

Fact 9: Investors were optimistic about house prices

The answer to why investors purchased subprime securities is contained in the third

column of the same Lehman analysis cited above, which lists the probabilities that were

24

The prime losses here refer to losses on nonagency (“jumbo”) deals , which included mortgages that were

too big to be securitized by Fannie Mae or Freddie Mac. For agency MBS consisting o f so-called conforming

mortgage s, credit risk was born not by investors but by the agencies themselves.

17

assigned to each of the various house price scenarios. It indicates that the adverse price

scenarios received very little weight. In part icular, the meltdown scenario—the only scenario

generating losses that threatened repayment of any AAA-rated t r anche—was assigned only

a 5 percent probability. The more benign pessimistic scenario received only a 15 percent

probability. By contra st, the top two price scenarios, each of which assumes a t least 8

percent a nnual growth in house prices over the next several years, receive probabilities that

sum to 30 percent. In other words, the authors of the Lehman report were bullish about

subprime investments not because they believed that borrowers had some “moral obligation”

to repay mortgages, or because they didn’t realize that the lenders had not fully verified

borrower incomes. The authors were not concerned about losses because they thought that

house prices would continue to rise, and that steady increases in the value of the collateral

backing the loans would cover a ny losses generated by bor r owers who would not or could not

repay.

Relative to historical experience, even the baseline forecast was optimistic, and the two

stronger scenarios were almost euphoric. A widely circulated calculation by Shiller (2005)

showed that real house price appreciation over the period from 1890 to 2004 was less than 1

percent per year. A cursory look at the FHFA national price index gives slightly higher real

house price appreciation—more than 1 percent—from 1975 to 2000, but still offers nothing

to justify 5 percent nominal a nnual price appreciation, let alone 8 or 11 percent. Further,

even sustained periods o f elevated price appreciatio n are rare.

25

The optimism was not unique to the Lehman report. Table 3, based on reports from

analysts at JPMorg an, shows that optimism reigned even in 2006, after house prices had

crested and begun t o fall. Well into 2007, the analysts were convinced that the decline would

prove tra nsitory and that prices would soon resume their upward march.

Industry analysts were not the only ones optimistic about the housing market. Gerardi,

Foote, and Willen (2011) show that there was considerable real-time debate among academic

economists on whether house prices in the early 2000 s were justified by fundamentals or were

instead poised to fall. In any case, the contemporary evidence on what investors believed

about prices suggests that their widespread optimism encouraged t hem to purchase subprime

securities, despite the well-understood risks involved.

Fact 10: Mortgage market insiders were the biggest losers

Perhaps the most compelling evidence against the inside job theory of the crisis concerns

the distribution of gains and losses among market participants. If insiders took advantage

of outsiders, then those most closely associated with the origination and securitization of

25

A

uthors’ ca lculations using FHFA national price index deflated using deflator for co re PCE.

18

mortgages should have pocketed the most money or at least incurred the smallest losses.

Conversely, investors with little connection to the industry should have suffered the most. In

fact, the opposite pattern emerges.

First consider the losers. Table 4 displays losses related to the subprime crisis compiled by

Bloomberg as of June 2008. Six of the top 10 institutions in this unhappy group (Citigroup,

Merrill Lynch, HSBC, Bank of America, Morgan Stanley, a nd JPMorgan) not only securitized

subprime mortgages, they actually owned companies that originated them. Ironically, the

list omits Bear Stearns, the one firm most closely associated with the subprime market.

Bear Stearns was heavily involved in every aspect of subprime lending, from origination

to securitization to servicing. Yet Bear Stearns does not appear on this table because in

March 2008 JPMorgan had acquired the firm in an assisted sale to prevent it from filing for

bankruptcy.

In fact, a closer look at Bear Stearns’ particular story provides compelling evidence against

the view that mortgage industry insiders profited at the expense of outsiders. The company

began experiencing problems in June 2007. Two hedge f unds managed by the firm had

invested heavily in subprime-related securities and reported enormous losses, requiring Bear

Stearns to inject capital into the f unds to protect investors. Remarkably, Bear Stearns

executives were maj or investors in these funds.

26

In other words, the executives most likely

to understand the subprime-lending process had made personal investment decisions that

expo sed them to subprime risk.

27

Indeed, the large insider losses have led many researchers to question whether lenders

actually even used the OTD model. Table 5, r eprinted from Acharya and Richardson (2009),

shows that issuing institutions retained enormous amounts of bo t h the AAA-rated private-

label MBS and the CDOs tied to their lower-r ated tranches. This retention of subprime-

mortgage risk occurred “even though the ‘originate and distribute’ model of securitization

that many banks ostensibly followed was suppo sed to tra nsfer risk to those institutions better

able to bear it, such as unleveraged pension funds” (Kashyap 2010, p. 1).

28

Fact 11: Mortgage market outsiders were the biggest winners

When we turn to the winners the pattern is equally stark. The biggest b eneficiary from

the crisis was hedge fund manager John Paulson, who bought billions of dollars of credit

26

See p. 244 of Muolo and Padilla (2010) for further details.

27

Along these lines, Cheng , Raina, and Xiong (2012) show that managers invo lved in the securitization

process were no less likely to buy houses at the peak of the bubble than the population in general.

28

Erel, Nada uld, and Stulz (2011) take on the question of why banks held so many risky subprime securities

on their books and conclude that the best explanation is that they did so to signal the quality o f the p ools of

loans. In a sense, Erel, Nadauld, and Stulz (2011) is a perfect illustration of the arguments in Gr ossman and

Hart (1980). Rather than withhold private information, agents have an important incentive to fully disclose

information in order to obtain the best prices for their products.

19

protection on subprime deals in 2006 and 2007. When those deals defaulted en masse at the

end of 2007, Paulson made $15 billion in profits (Zuckerman 2010).

Paulson and his lieutenant, Paolo Pellegrini, were complete mortgage industry outsiders.

They had no investment experience in housing or mortga ge markets and they had never

traded mortgages before. Zuckerman (2010) discusses investors’ lukewarm respo nse to Paul-

son’s sales pitches, quoting one potential investor as saying:

‘Paulson was a merger-arb guy and suddenly he has strong views on housing and

subprime,’ [the potential investor] recalls. ‘The largest mortgage guys, including

[Michael] Vranos at Ellington, one of the gods of the market, were fa r more

positive o n subprime’ (p. 126).

Furthermore, Paulson and Pellegrini explicitly attributed their success not to insights about

the underwriting process, but rather to a successful bet on house prices. According to

Zuckerman (2010), their conclusion t hat house prices were going to fa ll was based on a

simple analysis of the time-series of house prices in the United States:

Housing prices had climbed a puny 1.4 percent annually between 1975 and 2000,

after inflation wa s taken int o consideration. But they had soared over 7 percent

in the following five years, until 2 005. The upshot: U.S. home prices would have

to drop by almost 40 percent to return to their historic trend line (p. 107).

It was this simple insight about prices—not any fact about credit, t he origination process,

or moral hazard—that led Paulson and Pellegrini to gamble on bearish bets on the sub-

prime mortgag e market. The chart showing that house prices would f all 40 percent was

Paulson’s “Rosetta stone, the key to making sense of the entire housing market” (Zuckerman

2010, p. 108). And even Zuckerman seems surprised by t he failure of the insider/outsider

theory of mortgage markets, posing this question a t the beginning of his book:

Why was it John Paulson, a relative amateur in real estate and not a celebrat ed

mortgage, bond, or housing specialist like Bill Gross or Mike Vranos who pulled

off the greatest trade in history? (p. 3)

Another winner, memorably described by Lewis (2010), was Michael Burry. His hedge

fund Scion Capital made almost $1 billion in profits using a similar strategy to Paulson,

although on a smaller scale. Lewis writes that Burry, a medical doctor by training, was

an outsider not only in the housing and mortgage industries but to society in general, as

he worked largely alone. Burry attributed his success to his willingness to r ead complex

prospectuses carefully:

20

Burry had devoted himself to finding exactly the right ones to bet against. He’d

read dozens of prospectuses and scoured hundreds more, looking for the dodgiest

pools of mortgages, and was still pretty certain even then (and dead certain lat er)

that he was the only human being on earth who read them, apart from the lawyers

who drafted them. In doing so, he likely also became the only investor to do the

sort of old-fashioned bank credit analysis on the home loans that should have

been done before they were made (Lewis, 2010, p. 50).

In other words, Burry’s bets were based on publicly available information.

Taking a broad view, the most useful demarcation to make when thinking about the

mortgage market is not between insiders and outsiders, the division made in the top panel of

Figure 1. Rather, it is between those people who thought house prices would continue to r ise

and those who were willing to bet that they would fall. Sadly for the economy, the overly

optimistic group included not only the investors at the end of the securitization chain, but

lenders and securitizers who sold t hem the bonds, and whose losses precipitated the financial

crisis.

Fact 12: Top-rated bonds backed by mortgages did not turn out to be “toxic.”

Top-rated bonds in collateralized debt obligations (CDOs) did.

No discussion of the causes of the financial crisis would be complete without some dis-

cussion of the rating agencies. To some analysts, the simple fact that rating agencies gave

AAA ratings to subprime securities is patently absurd. An AAA rating is supposed to sig-

nal a near-complete absence of credit risk. Yet these bonds were often backed by reduced

documentation loans to borrowers with previous credit problems. Other critics are more

specific, noting that the issuers paid the rating agencies to evaluate their deals. The implica-

tion is that for the agencies these payments generated a conflict of interest that encouraged

them to bestow unjustifiably high ratings. At the very least, commentators oft en claim that

rating agencies a betted finance industry insiders by endorsing securities backed by problem

mortgages. Yet the facts paint a more nuanced picture.

To start with, t he top-rated tranches of subprime securities fared better than many people

realize. The top panel of Figure 9 is generated fro m data on AAA-rated bonds created in

2006 from priva t e- la bel securitization deals.

29

Specifically, the panel shows the fraction of

these bonds on which investors suffered losses or , using industry jargon, the fraction that was

“impaired.” In some o f these deals, 70 percent of the underlying subprime loans terminated

in f oreclosure (Jozoff et al. 2012). Yet despite these massive losses, the figure shows that

investors lost money on less than 10 percent of private-label AAA-rated securities. How is

29

T

hese deals included subprime mor tgages, Alt-A mortgages, and jumbo mortgages.

21

that possible? As many have explained, the AAA-rated securities were protected by a series

of lower-ra t ed securities which absorbed most of the losses. If a borrower defaulted and

the lender was unable to recover the principal, the resulting loss would b e deducted from

the principal of the deal’s lower-rated tranches. For subprime deals, the degree of so-called

AAA credit pro t ection—the principal balance of the non-AAA securities—was often more

than 20 percent. Given a 50 percent recovery rate on foreclosed loans, 20 percent credit

protection meant that 40 percent of the b orrowers could suffer foreclosure before the AAA-

rated investors suffered a single dollar of loss. For riskier deals, credit protection was higher,

often substant ia lly so. The key takeaway is that for subprime securities, credit protection

largely worked, and investors in the AAA-rated securities were largely spared.

The relatively robust performance of private-label AAA-rated securities is explained

clearly in the final report of the Financial Crisis Inquiry Commission (2011), among other

sources. Yet it still surprises many people. If these AAA-rated securities didn’t suffer losses,

where were the famous “toxic mortgage-related securities” that caused the financial crisis?

The answer is that banks used lower-rated securities from private-label deals to construct

other securities, such as the CDOs discussed earlier. Recall that because these CDOs were

backed by tranches of subprime securities, which were technically labeled asset-backed secu-

rities (ABS), the resulting CDOs were called ABS CDOs. The main difference between the

original ABS and the ABS CDOs was that the CDOs were not backed by 2,000 or so subprime

loans, but rather a collection of 90–100 lower-rated tranches of subprime ABS deals, with

most of these tranches having BBB ratings. Yet t he organizing principal of CDOs and the

original ABS securities was the same: senior AAA-rated tranches were protected from losses

by lower-ra t ed tranches. For the original ABS, losses would occur if individual homeowners

defaulted. For the CDOs, losses would occur if the BBB-rated securities f r om the original

ABS deals defaulted.

The bottom panel of Fig ure 9 shows the share of 2006 ABS CDOs that were impaired. The

results are nearly the mirror image of the previous graph. Whereas investors suffered losses

on less than 10 percent of the AAA-rat ed tranches from the original subprime securities, they

suffered losses on a ll but 10 percent of AAA-rated ABS CDOs.

30

To make matters worse, a

large portio n of the ABS CDOs were known as “super-senior” securities because they were

senior even to the AAA-rated tranches of the CDO. Super-seniors were often retained by

the Wall Street firm that issued the CDO. But CDO losses were commonly large enough to

wipe out both the AAA tranches and super-senior ones, leaving the issuing institution with

large losses. In short, it was the ABS CDOs, not the original subprime ABS, that proved so

30

F

or a discussion of the link between CDOs and the underlying ABSs, see Ashcraft and Schuermann

(2008).

22

toxic to the financial system. And the main failure of the rating agencies was not a flawed

analysis of original subprime securities, but a flawed analysis of the CDOs composed of these

securities.

The disparate performance of top-rated tranches from ABS a nd CDOs is one of great

puzzles of the crisis. Because issuers were paid to rate both types of securities, it is hard

to blame the bad CDO ratings on the “issuer pays” model of rating-agency comp ensation.

But if a conflict of interest did not cause the bad ratings on the CDO s, what did? Some

institutional evidence provides a clue to the answer.

The key insight is that ABS and CDOs were evaluated by using very different methods.

This was true both at the investment banks that issued these two types of securities and the

agencies that r ated them. When fo r ecasting subprime ABS performance, analysts modeled

the default probabilities of the individual loans. Recall that the data for this type of analysis

was widely available, for example in the loan-level datasets collected and standardized by

LoanPerformance. To forecast the performance of a subprime pool, analysts could first

estimate an individual-level default model based on loan-level predictors like the credit score,

the debt-to-income ratio, the interest rate, and the current level of the borrower’s equity.

The current equity level could be inferred by t he or ig inal downpayment on the loan, the

loan’s amortization schedule, and the subsequent behavior of housing prices. Armed with an

individual-level model of default, the analyst could then simulate what would happen to all

the mortgages in the pool if housing prices declined by (say) 5 or 10 percent.

Three comments on this ABS analysis are in order to set up the contrast with the method

used to evaluate CDOs. The first is that the ABS analysis was accurate. Recall the Lehman

Brothers analysis from Table 2, which gives a basically accurate prediction for how bad ABS

losses would be if housing prices declined. Second, in the jargon of economists, the analysis

was structural, in that it modeled how individual decisions are likely to change as economic

conditions evolve. Falling prices make it more likely that a homeowner will have negative

equity, and economic theory predicts that “underwater” owners will default more often.

31

This prediction r eceives a great deal of suppor t in empirical default models, so analysts knew

that defaults would rise if prices declined. Moreover, they knew that lower-rated tranches of

subprime ABS would be wiped out if the price decline was especially large. This knowledge

encouraged the issuers of subprime ABS to build a great deal of credit protection into their

deals at the outset, in or der to ensure that their to p-rated bonds would pay off no matter

what happened to t he housing market.

31

Underwater owners who lose their jobs or suffer some other adverse life event are unable to sell their homes

for eno ugh to pay off their loans. Fore c losure is often the only possible outco me in this case. Additionally, if

negative equity is large enough, an underwater owner may simply walk away from his mortgage in a so-called

ruthless or strategic default.

23

A third point about the analysis o f private-label mortgage securities is that this analysis

could examine how correlation in individual mortgage defaults might arise.

32

The basic

idea behind securitizatio n is that individual loans might have high individual probabilities of

default, but these probabilities are not likely to be correlated with one other. This assumption

is violated, however, if there is some aggregate shock to all the mortgages in a pool, for

example if house prices declined on a nationwide basis. The loan-level models allowed analysts