Financial Literacy in Australia:

Insights from HILDA Data

Professor Alison Preston

UWA Business School

March 2020

Australia has a relatively high level of financial literacy when ranked globally.

In the 2014 Standard & Poor’s Ratings Services Global Financial Literacy

Survey of a 140 economies, Australia, for example, ranked in the top 10

countries for financial literacy.

1

Notwithstanding this favourable global

performance there is widespread financial illiteracy within Australia,

particularly amongst young people. There are also large and significant

gender gaps with women, on average, less financially literate than men.

Within Australia 63% of men and 48% of women demonstrate an

understanding of at least three basic financial literacy concepts. If

understanding three basic financial literacy concepts can be considered

financially literate, then these statistics suggests that around 8.5 million (or

45%) adults in Australia are financially illiterate.

Such widespread financial illiteracy is of increasing concern within the

context of highly complex financial markets, high levels of personal and

household indebtedness and easy access to credit opportunities (particularly

from non-traditional sources as Wallet Wizard and Nimble). As a minimum

individuals need to understand the concept of compound interest.

Introduction

Figure 1: Financial literacy rates; adults; Australia

In view of these concerns, this issues paper has been prepared as a way of highlighting

the level of financial literacy within and across Australia. The goal of the paper is to

engender debate amongst academics, practitioners and policy makers on the issues

related to financial illiteracy, identify issues in need of deeper research and contribute to

thought leadership on the ways through which the problems associated with financial

illiteracy may be addressed.

2

The analysis reported in this paper is primarily based on data gathered in

2016 via the Household, Income and Labour Dynamics in Australia (HILDA)

survey. HILDA is a large, nationally representative, longitudinal survey of

households. All individuals aged 15 or more within sample households are

interviewed and detailed information is gathered on a range of

socioeconomic characteristics, including information on wealth and financial

decision making. In 2016 the HILDA survey also included a series of

questions testing knowledge of basic financial literacy concepts. These data

provide important insights into the financial literacy of Australians and are

especially valuable on account of the nationally representative nature of the

survey.

There are a number of ways of measuring financial literacy. A common

approach is to define a person as financially literate if they can correctly

answer three questions (commonly known as the Big-3) testing knowledge

related to three key financial literacy concepts. These include: (a) an

understanding of interest rates, especially compound interest; (b) an

understanding of inflation; and (c) an understanding of diversification.

The HILDA data and the measurement of financial literacy

The actual number and complexity of the financial literacy questions included in various

surveys differs depending on the focus and length of the survey. As HILDA is a large and

detailed survey, time only permitted the inclusion five financial literacy questions. The

questions followed international best practice and were based on questions initially

developed by Annamaria Lusardi and Olivia Mitchell.

2

The five HILDA questions were as

follows:

• Q1: Interest Rate: “Suppose you put $100 into a no-fee savings account with a

guaranteed interest rate of 2% per year. You don’t make any further payments into this

account and you don’t withdraw any money. How much would be in the account at the

end of the first year, once the interest payment is made?”

• Q2: Inflation: “Imagine now that the interest rate on your savings account was 1% per

year and inflation was 2% per year. After one year, would you be able to buy more

than today, exactly the same as today, or less than today with the money in this

account?”

• Q3: Diversification: “Buying shares in a single company usually provides a safer return

than buying shares in a number of different companies.” [True, False]

• Q4: Risk: “An investment with a high return is likely to be high risk.” [True, False]

• Q5: Money Illusion: “Suppose that by the year 2020 your income has doubled, but the

prices of all of the things you buy have also doubled. In 2020, will you be able to buy

more than today, exactly the same as today, or less than today with your income?”

Respondents also had the option of a “don’t know” response or a “refuse to answer”

response.

3

When assessed using the Big-3 (questions 1-3 above) the HILDA estimates

show that just over half of all adult Australians (55%) are financially literate.

When disaggregated by sex it is apparent that there is a large gender gap in

financial literacy. While two-third (63%) of Australian men are financially

literate fewer than one in two (48%) of Australian women are financially

literate (Figure 1).

3

The gender gap is highly significant in a statistical sense.

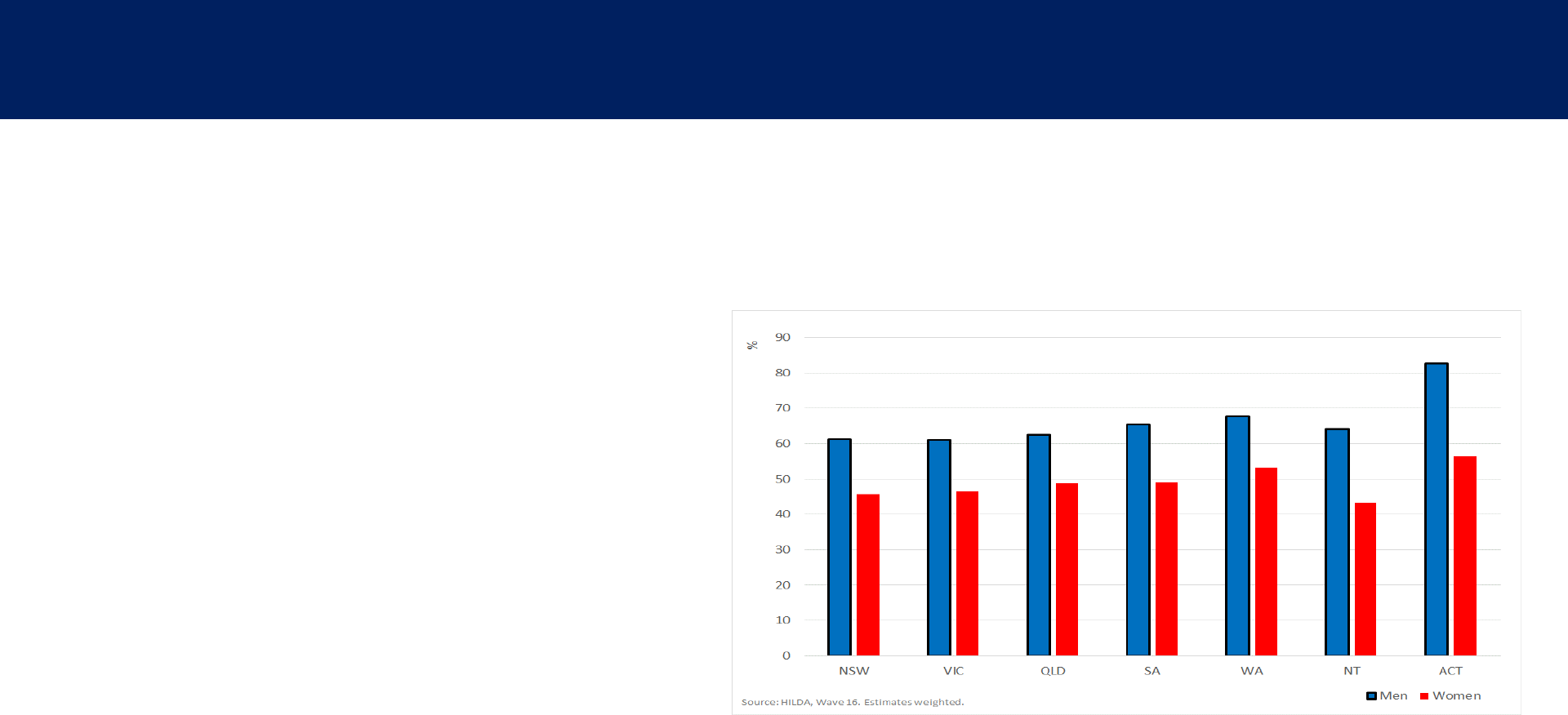

Figure 2 shows the variation in financial literacy across Australia’s States and

Territories. When benchmarked against the observed financial literacy rates

in New South Wales (NSW) it would appear that the financial literacy rates of

men and women are significantly higher in Western Australia (WA) and in

the Australian Capital Territory (ACT). There are nevertheless, large and

significant gender gaps in financial literacy within all States and Territories

(the exception being the Northern Territory where the observed gender gap

is not statistically significant).

How financially literate are adult Australians?

Figure 2: Financial literacy rates; adults; Australian States and Territories

4

Financial literacy not only varies by sex, it also varies by age and has an inverse U-Shape; i.e. is at

its lowest amongst young people, rises over the life course and then declines in older age (Figure

3). Such a pattern is found in most countries and Australia is no different in this respect. Within

Australia the turning point is around 50 years of age.

3

The declining financial literacy rates in

older ages relates, in part, to cognition effects.

There are also significant differences in financial literacy when disaggregated by socioeconomic

characteristics such as birthplace, marital status, education and employment (see Table 1).

Women, for example, who are migrants from a non-English speaking background country have a

financial literacy rate of 40.5%; this compares to 49.1% for Australian born women. Similarly,

women whose highest level of education was Year12 or less have a financial literacy rate of

38.3% while the rate for tertiary qualified women is 65.2%.

Figure 3: Financial literacy rates by age and sex, Australia

Married

Never

married

Australian

born

Migrant from a

non-English

speaking

background

High

School or

less

Tertiary

qualified

Employed

Not in the

labour

market

Men 69.1% 50.0% 63.5% 55.4% 48.2% 81.8% 65.7% 58.5%

Women 53.8% 34.9% 49.1% 40.5% 38.3% 65.2% 51.9% 42.5%

Difference:

Men-Women (%-point)

15.3 15.0 14.4 15.0 9.9 16.6 13.9 16.0

Table 1: Financial literacy rates by select characteristics

5

Source: HILDA.

Empirical research shows that financial literacy is important determinant of,

and correlate with, a range of outcomes including wealth accumulation and

planning for retirement, superannuation savings, and women’s economic

empowerment and domestic violence.

4

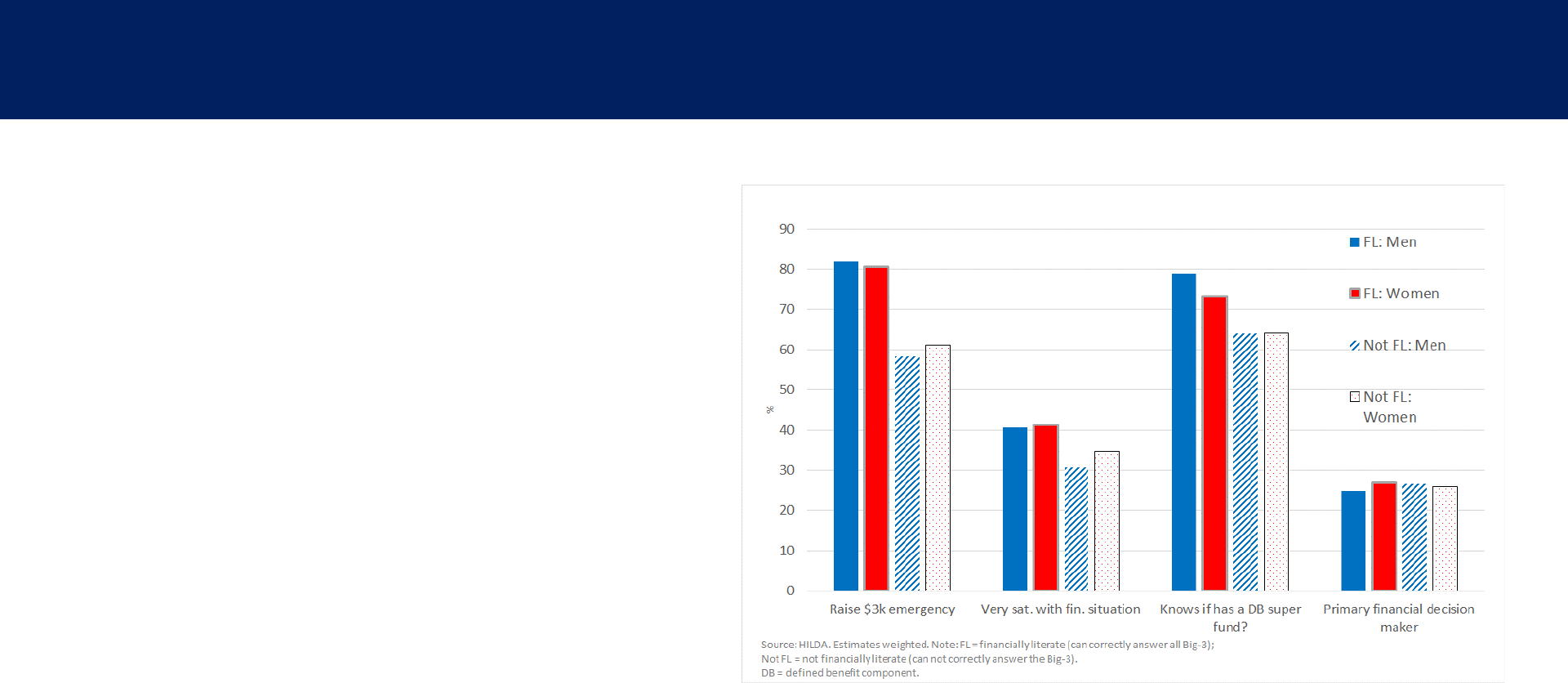

Figure 4 and 5 describes select

characteristics of adult men and women in Australia disaggregated by

whether or not they are financially literate. The purpose of the exercise is to

show that financial literacy correlates with important outcomes such as

savings and satisfaction with ones financial situation (an important predictor

of well-being).

The first two columns in Figure 4 shows that around 80% of men and women

who are financially literate are able to easily raise $3,000 in an emergency.

This compares to 60% for men and women who are not financially literate.

The second set of estimates pertain to ‘satisfaction with financial situation’.

Here we can see that around 40% of men and women who are financially

literate consider themselves to be very satisfied with their financial

situation. A significantly smaller share of financially illiterate men and

women consider themselves to be very satisfied with their financial

situation.

Does being financially literate matter?

Figure 4: Financial literacy by select characteristics

6

In the third set of estimates in Figure 4 the focus is on the type of superannuation

account that the respondent has. Australia is one of the few countries in the world

that requires employers to make a compulsory contribution into a retirement

savings account (known as a superannuation fund in Australia). The arrangement

has led to widespread superannuation coverage, however, a large portion of those

with superannuation do not understand how superannuation works. The 2018

HILDA survey included a special module on wealth and superannuation savings.

Respondents with a superannuation account were asked about the type of

superannuation account they had (i.e. whether or not they had a defined benefit

(DB) component) and also asked about the balance in their account. An analysis of

the responses for adult non-retirees (aged 20-64) shows that only 79% and 73% of

financially literate males and females, respectively, knew whether or not they had a

DB component. The corresponding shares amongst financially illiterate non-retirees

was 64% and 60%, respectively. Financially illiterate males and females were also

more likely to state that they did not know the balance in their superannuation

account.

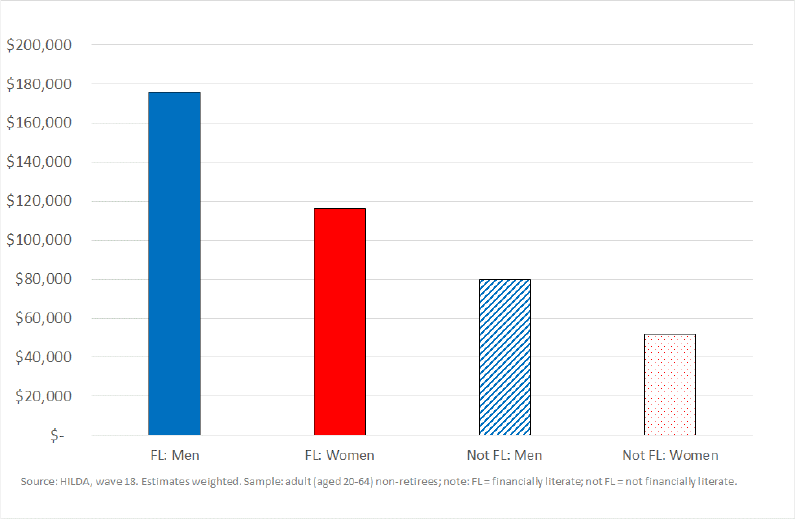

Figure 5: Financial literacy and superannuation balances, 2018

Figure 5 summarises the mean superannuation balance (savings) disaggregated by

financial literacy knowledge. As may be seen, men and women who are financially

literate have significantly higher superannuation balances. It is, of course, entirely

possible that having higher superannuation balances incentivises individuals to

become more financially literate. In other words, while there is a correlation,

without deeper analysis we are unable to state whether or not there is a causation

(ie. financial literacy leads to higher superannuation savings).

5

7

Figure 6 shows the extent of financial illiteracy amongst teenagers (aged 15-17) in

Australia (comparisons are also made with adults). There are no statistically

significant differences in the financial literacy rates of teenage males and females

across Australia’s States and Territories. In 2016 only 28% of teenage males and

15% of teenage females were able to correctly answer all of the Big-3 financial

literacy questions. This is significantly less than the mean share for adults (the

non-patterned bars). There is also a large gender gap. The low level of financial

literacy amongst young people is particularly concerning given the range of

financial decisions that young people are increasingly required to make, including

decisions about investing in education, saving, credit cards etc.

It is clear from the above that the observed gender gap in financial literacy in

adulthood stems from gender gaps in financial literacy that have emerged during

the teen and pre-teen years. Interventions to increase the financial literacy of

young people could, therefore, be expected to raise the financial literacy of people

in adulthood. Understanding the determinants of financial literacy amongst young

people is, therefore, an important research priority. Studies that have and are

investigating this suggests that there is an important household transmission

effect, particularly between mothers and daughters.

6

How financially literate are teenagers?

Figure 6: Financial literacy rates; teenagers and adults

8

Within and across Australia there is widespread financial illiteracy. Nationally one in three

adult men and one in two adult women do not understand key basic financial literacy

concepts such as interest rates, inflation and risk diversification. These are concerning shares,

particularly in the context of rising household debt, increased individual responsibility for

saving for retirement and easy access to credit. The costs of financial illiteracy to the society,

the economy and individuals are substantial. From a macroeconomic perspective it financial

literacy is central to the stability of the financial system

7

and from an individual and societal

perspective it matters for overall wellbeing.

At a national level the Australian Securities and Investment Commission (ASIC) is developing a

roadmap or strategy to develop the financial capabilities of all Austalians.

8

The UWA Public

Policy Institute (PPI) seeks to contribute to the strategy and policy making process and, to this

end, seeks your views and input. Key questions include:

1. What focus areas should be considered / prioritised?

2. What research is needed to better inform strategy and policy making?

3. What policies should we consider / prioritise?

4. What would you see as central to any financial capabilities strategy?

Where to from here?

Endnotes

1. Hasler, A. and Lusardi, A., 2017. The gender gap in financial literacy: a global perspective.

Global Financial Literacy Excellence Centre. The George Washington University School of

Business.

2. Lusardi, A. and Mitchell, O., 2011. ‘Financial literacy around the world: an overview’,

Journal of Pension Economics and Finance, 10(4): 497-508.

3. Preston, A. and Wright, R.E., 2019. ‘Understanding the gender gap in financial literacy:

evidence from Australia’, Economic Record, 95: 1-29.

4. Van Rooij, M., Lusardi, A. and Alessie, R., 2012. ‘Financial literacy, retirement planning and

household wealth’, Economic Journal, 122: 449-478.; Lusardi, A., and Mitchell, O., 2007.

‘Baby boomer retirement security: the roles of planning, financial literacy and household

wealth’, Journal of Monetary Economics 54(1): 205-224; Postmus J. et al., 2013. ‘Financial

literacy: building economic empowerment with survivors of violence’, Journal of Family

Economic Issues, 34: 275-284.

5. For a more detailed analysis of the relationship between financial literacy and the

superannuation savings of men and women see: Preston, A. and Wright, R.E., 2020. ‘The

impact of financial literacy on the superannuation (pension) savings of men and women’,

in Preston, A. (ed) Financial Literacy and Superannuation (Pension) Savings for Retirement:

Submission to the Australian Government Retirement Income Review

https://treasury.gov.au/sites/default/files/2020-02/preston030220.pdf

6. Bottazzi, L. and Lusardi, A. 2016. ‘Gender differences in financial literacy: evidence from

PISA data in Italy’

https://institute.eib.org/wp-content/uploads/2016/10/gender-diff.pdf

7. Hall, K., 2008. ‘The importance of financial literacy’, Reserve Bank of Australia Bulletin,

September: 13-18.

8. ASIC and RMIT, 2019. ‘Research Summit: Building Financial Capabilities Together.

Summary Report.

https://financialcapability.gov.au/files/summary-report-building-

financial-capabilities-together-research-summit.pdf

Disclaimer

Disclaimer: The HILDA Project was initiated and is funded by the Australian Government Department of Social Services (DSS) and is

managed by the Melbourne Institute of Applied Economic and Social Research (Melbourne Institute). The findings and views reported

in this paper, however, are those of the author and should not be attributed to either the DSS or the Melbourne Institute.

9